- Medical Devices

- Ureteroscope Market

Ureteroscope Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Ureteroscope Market by Product Type (Flexible Ureteroscopes, Semi-rigid Ureteroscopes, and Rigid Ureteroscopes), by Application (Urolithiasis, Ureteral Strictures, Urothelial Carcinoma, Urinary Tract Infections, Hematuria Evaluation, Foreign Body Retrieval, Congenital Abnormalities, and Others) by End User (Hospitals, Ambulatory Surgical Centers (ASCs), Urology Clinics, Diagnostic Centers, and Academic & Research Institutes), and Regional Analysis from 2026 - 2033

Ureteroscope Market Share and Trend Analysis

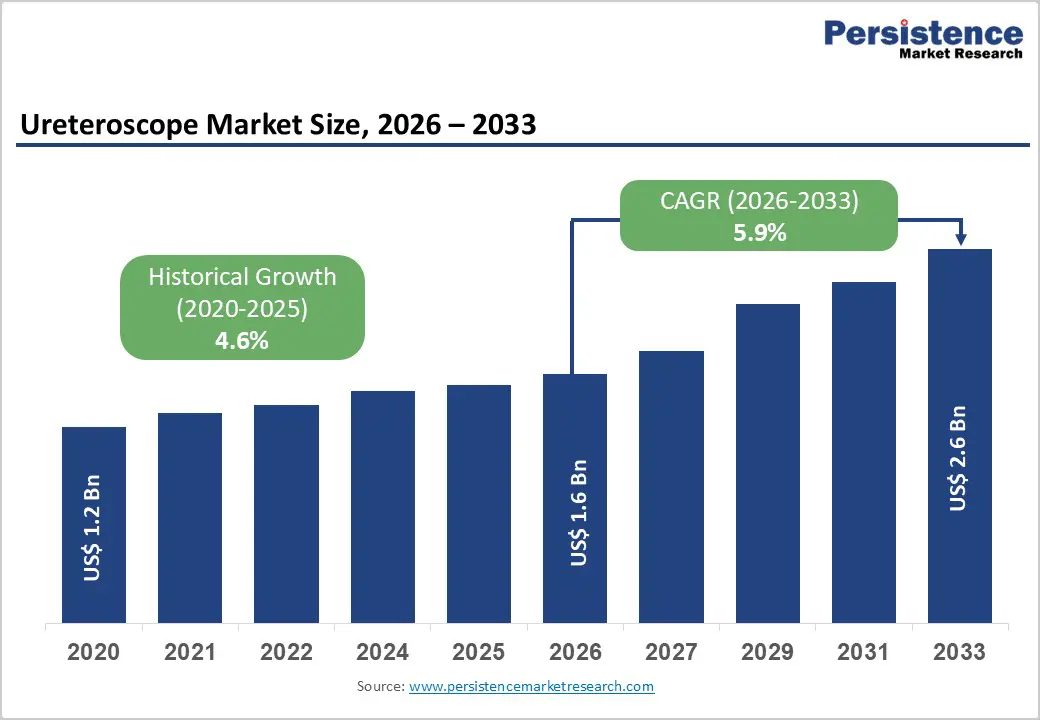

The global ureteroscope market size is estimated to grow from US$ 1.6 billion in 2026 to US$ 2.6 billion by 2033. The market is projected to record a CAGR of 5.9% during the forecast period from 2026 to 2033.

Growing preference for minimally invasive urological interventions is steadily accelerating the adoption of advanced ureteroscopic technologies worldwide. These devices enable direct visualization of the urinary tract, allowing clinicians to diagnose and treat conditions such as kidney stones, strictures, and urothelial tumors with high precision. The increasing incidence of urolithiasis, driven by lifestyle changes, dehydration, and metabolic disorders, is significantly contributing to rising procedural volumes. Modern ureteroscopes, particularly flexible and digital variants, offer enhanced maneuverability and high-definition imaging, improving stone clearance rates and overall treatment outcomes.

Healthcare facilities are increasingly integrating ureteroscopic systems with laser lithotripsy and advanced imaging platforms to enhance procedural efficiency and reduce complications. The transition toward outpatient care settings and shorter hospital stays is further supporting the demand for minimally invasive solutions. Continuous improvements in device durability, deflection mechanisms, and single-use technologies are also strengthening clinical adoption. Simultaneously, expanding urology training programs and rising healthcare investments in emerging economies are improving access to advanced treatment options. As healthcare systems emphasize patient safety, cost efficiency, and faster recovery, ureteroscopy continues to evolve as a critical tool in modern urological practice.

Key Industry Highlights

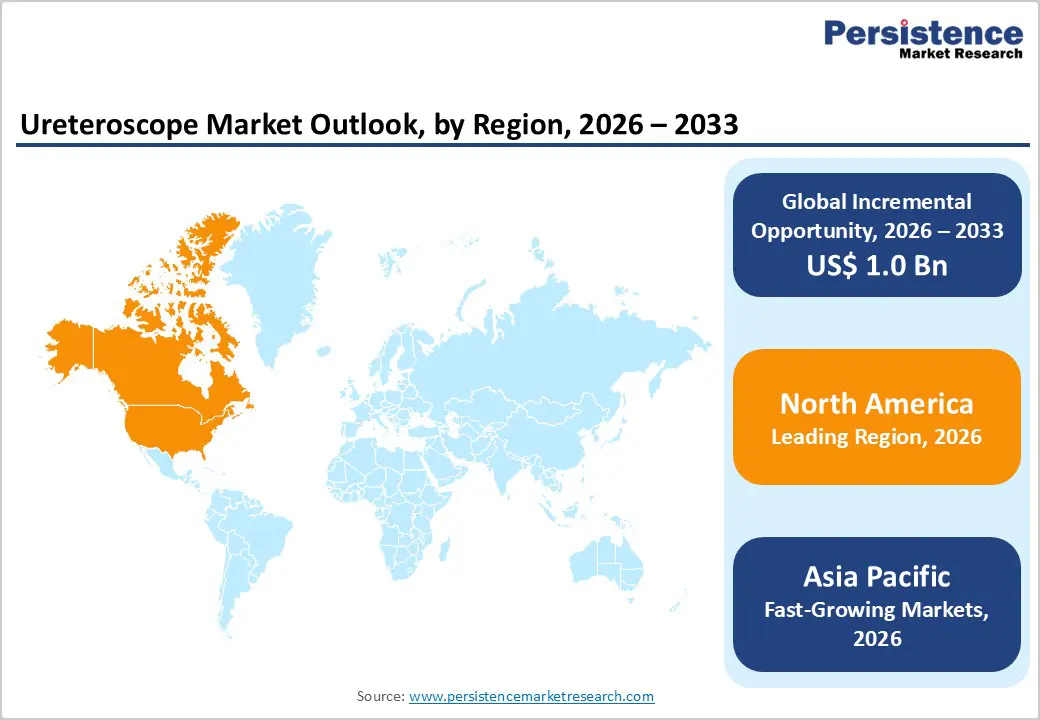

- Leading Region: North America holds the largest share at 46.7%, supported by advanced healthcare systems, high procedural volumes for kidney stone management, strong clinical adoption of minimally invasive technologies, and the presence of established medical device manufacturers.

- Fastest-Growing Region: Asia Pacific is witnessing the fastest expansion due to rapid healthcare infrastructure development, increasing prevalence of urolithiasis, rising awareness, and improved access to advanced urological care across countries such as China and India.

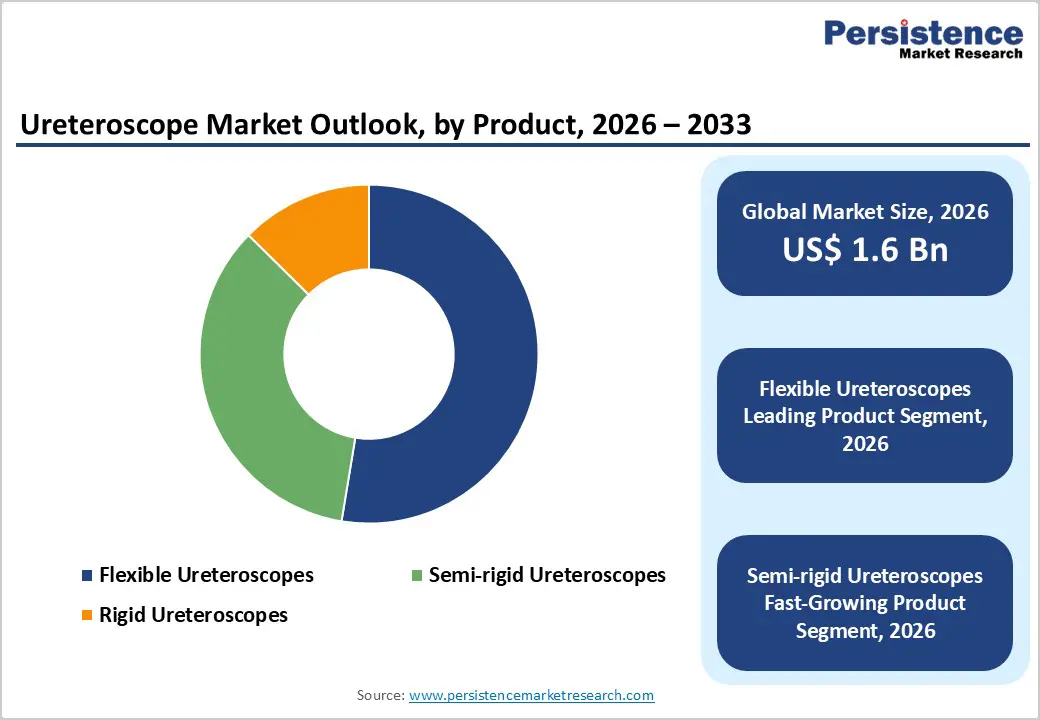

- Leading Product Type Segment: Flexible ureteroscopes dominate the market, driven by their superior navigation capabilities, ability to access complex renal anatomy, and increasing preference in minimally invasive stone management procedures.

- Fastest-Growing Product Type Segment: Semi-rigid ureteroscopes are gaining momentum as cost-effective alternatives, particularly in emerging markets and routine ureteral procedures where high flexibility is not always required.

- Leading Application Segment: Urolithiasis accounts for the largest share, supported by the growing global burden of kidney stones and the widespread adoption of ureteroscopy as a primary treatment modality.

- Fastest-Growing Application Segment: Ureteral strictures are emerging as a high-growth area, driven by increasing procedural interventions and the need for precise endoscopic management techniques.

| Key Insights | Details |

|---|---|

| Ureteroscope Market Size (2026E) | US$ 1.6 Bn |

| Market Value Forecast (2033F) | US$ 2.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Driver - Rising Burden of Kidney Stone Disease and Shift Toward Minimally Invasive Urological Procedures

The growing incidence of urolithiasis across both developed and emerging regions is a major force accelerating demand for ureteroscopic interventions. Factors such as sedentary lifestyles, dehydration, dietary imbalances, and metabolic disorders are contributing to a steady increase in kidney stone cases globally. This has led to a higher procedural volume of ureteroscopy, which is widely preferred due to its minimally invasive nature and high success rates in stone removal. Compared to open or percutaneous surgeries, ureteroscopic procedures offer reduced hospitalization time, faster recovery, and lower complication risks, making them increasingly favorable among both clinicians and patients.

Technological advancements have further strengthened adoption, particularly with the introduction of flexible and digital ureteroscopes that provide superior visualization and improved maneuverability within complex urinary tract anatomy. The integration of laser lithotripsy systems has also enhanced procedural efficiency, enabling precise fragmentation of stones with minimal tissue damage. In addition, increasing awareness regarding early diagnosis and treatment of urological disorders is driving patient inflow into healthcare facilities. As healthcare systems continue prioritizing minimally invasive treatment approaches and improved patient outcomes, ureteroscopy is becoming a standard of care, thereby significantly driving market expansion.

Restraints - High Device Costs, Reprocessing Challenges, and Limited Accessibility in Low-Resource Settings

Despite strong clinical adoption, several structural and economic constraints continue to limit the broader penetration of ureteroscopic technologies. One of the primary challenges is the high cost associated with advanced ureteroscopes, particularly digital and flexible variants, which require significant capital investment. In addition to procurement costs, healthcare facilities must account for ongoing expenses related to maintenance, repairs, and sterilization processes. Reusable ureteroscopes are especially prone to wear and tear due to their delicate construction, leading to frequent repairs that increase operational expenditure over time. Reprocessing requirements also present a notable challenge, as improper sterilization can lead to cross-contamination and hospital-acquired infections. This has prompted stricter regulatory guidelines, increasing compliance burdens for healthcare providers. While single-use ureteroscopes offer a solution to infection control issues, their recurring costs can be prohibitive for smaller hospitals and clinics.

Furthermore, limited access to advanced urological care in rural and low-income regions restricts market growth. Many healthcare facilities in developing areas lack the necessary infrastructure, trained professionals, and financial resources to adopt modern ureteroscopic systems. These combined cost, maintenance, and accessibility constraints continue to act as barriers, particularly in price-sensitive healthcare markets.

Opportunity - Emergence of Single-use Technologies and Advancements in Digital Imaging Solutions

Ongoing innovation in device design and imaging capabilities is creating significant growth opportunities within the ureteroscope landscape. One of the most transformative trends is the increasing adoption of single-use ureteroscopes, which eliminate the need for complex reprocessing and reduce the risk of cross-contamination. These devices are particularly beneficial in high-volume centers and settings where sterilization infrastructure is limited. As manufacturing efficiencies improve, the cost gap between reusable and disposable devices is gradually narrowing, making single-use options more commercially viable. Additionally, the advancements in digital imaging and visualization technologies. Modern ureteroscopes are being equipped with high-definition cameras, improved light sources, and enhanced image processing capabilities, enabling clearer visualization of the urinary tract. This improves diagnostic accuracy and procedural outcomes, especially in complex cases.

Moreover, integration with complementary technologies such as laser lithotripsy systems and robotic-assisted platforms is enhancing overall procedural precision. Expanding healthcare investments in emerging economies are also creating new avenues for market growth, as hospitals upgrade their surgical capabilities. As innovation continues to focus on efficiency, safety, and usability, next-generation ureteroscopic solutions are expected to witness strong demand globally.

Category-wise Analysis

Product Type Insights

Flexible ureteroscopes are projected to command 52.6% of the global market in 2026, primarily due to their ability to access complex anatomical regions within the kidney and ureter. Their advanced deflection capabilities enable urologists to reach lower pole stones and intricate calyceal structures that are otherwise difficult to treat using rigid or semi-rigid devices. Increasing preference for minimally invasive procedures has further strengthened their adoption, as these instruments reduce patient trauma, hospital stay duration, and recovery time. Technological advancements such as digital imaging, enhanced durability, and improved irrigation systems are also elevating procedural efficiency. Additionally, the growing use of single-use flexible ureteroscopes is minimizing cross-contamination risks and reprocessing costs. As procedural volumes for kidney stone management continue to rise globally, flexible ureteroscopes remain the most clinically versatile and widely utilized product category.

Application Insights

The urolithiasis segment is expected to account for 48.7% of the ureteroscope market in 2026, driven by the increasing global prevalence of kidney stone disease. Rising incidence linked to dietary habits, dehydration, and metabolic disorders has significantly increased the demand for ureteroscopic interventions. Ureteroscopy has become a standard treatment modality due to its high success rates and ability to manage stones across various locations within the urinary tract. The integration of laser lithotripsy technologies further enhances treatment outcomes by enabling precise stone fragmentation. In addition, advancements in imaging and scope flexibility allow better visualization and improved stone clearance rates. Healthcare providers are increasingly adopting minimally invasive approaches over traditional surgical methods, further reinforcing segment growth. As awareness, diagnosis rates, and treatment accessibility improve worldwide, urolithiasis continues to dominate procedural demand within the ureteroscope market.

End-user Insights

Hospitals are anticipated to hold 49.5% of the global ureteroscope market in 2026, supported by their comprehensive surgical infrastructure and availability of specialized urology departments. These facilities handle a large volume of complex urological procedures, including kidney stone removal, tumor evaluation, and ureteral interventions. The presence of skilled urologists, access to advanced imaging systems, and integration of laser technologies make hospitals the preferred setting for ureteroscopy procedures. Additionally, hospitals are more likely to invest in high-cost digital and flexible ureteroscopes, ensuring better patient outcomes and procedural success rates. Many large healthcare institutions are also adopting disposable ureteroscopes to improve infection control and operational efficiency. Furthermore, hospitals often serve as training and research centers, facilitating the adoption of new technologies and techniques. This combination of clinical capability, infrastructure, and innovation continues to position hospitals as the dominant end-user segment.

Regional Insights

North America Ureteroscope Market Trends

North America is expected to account for 46.7% of the global ureteroscope market in 2026, maintaining its position as the leading regional contributor. The region benefits from a highly developed healthcare ecosystem, widespread access to advanced urological care, and strong adoption of minimally invasive surgical techniques. The United States plays a central role, with a high volume of ureteroscopy procedures performed annually due to the increasing prevalence of kidney stones and related disorders. Hospitals and ambulatory surgical centers are equipped with advanced endoscopic systems, including digital and single-use ureteroscopes, which enhance procedural outcomes and efficiency.

Additionally, the presence of leading medical device manufacturers actively investing in product innovation, including improvements in imaging quality, scope durability, and ergonomic design. Favorable reimbursement frameworks further support the adoption of advanced technologies. Additionally, ongoing clinical research and collaborations between healthcare providers and industry players are driving the introduction of next-generation ureteroscopic solutions. With strong technological adoption and a mature healthcare infrastructure, North America continues to set benchmarks in urological device utilization.

Europe Ureteroscope Market Trends

Europe remains a technologically advanced and steadily growing market for ureteroscopes, supported by strong healthcare systems and a focus on precision medical technologies. Countries such as Germany, the United Kingdom, France, and Italy are at the forefront of adopting minimally invasive urological procedures. The region emphasizes high-quality patient care, encouraging the use of advanced endoscopic devices that improve surgical outcomes and reduce complications. Healthcare institutions across Europe are increasingly integrating digital ureteroscopes and laser-based treatment systems into routine clinical practice. Government-supported healthcare frameworks play a crucial role in facilitating access to modern surgical equipment, particularly in public hospitals.

Additionally, Europe is recognized for its robust medical device manufacturing base and continuous innovation in endoscopy technologies. Collaborative research initiatives between academic institutions and industry participants are further advancing device performance and clinical applications. The region is also witnessing growing adoption of single-use ureteroscopes, driven by infection control concerns and cost optimization strategies. With sustained investments in healthcare modernization and a strong regulatory environment ensuring product quality, Europe continues to be a key contributor to the global ureteroscope market.

Asia Pacific Ureteroscope Market Trends

Asia Pacific is projected to be the fastest-growing region in the ureteroscope market, with a CAGR of approximately 8.0% from 2026 to 2033. Rapid expansion of healthcare infrastructure, increasing healthcare expenditure, and improving access to specialized urological care are key factors driving regional growth. Countries such as China, India, Japan, and South Korea are experiencing a surge in kidney stone cases, largely due to changing dietary patterns, urbanization, and climatic conditions. Hospitals across the region are increasingly adopting minimally invasive procedures to manage urological disorders, leading to higher demand for advanced ureteroscopic devices. Government initiatives aimed at strengthening healthcare systems and expanding surgical capabilities are also contributing to market expansion. In emerging economies like India and China, rising awareness and improved diagnostic capabilities are resulting in earlier detection and treatment of urological conditions.

Furthermore, global medical device companies are forming strategic partnerships with local distributors and healthcare providers to expand their regional presence. Training programs for urologists and investments in modern surgical infrastructure are accelerating technology adoption. As affordability improves and healthcare access broadens, Asia Pacific is poised to become the most dynamic and high-growth market for ureteroscopes globally.

Competitive Landscape

The global ureteroscope market is highly competitive, with strong participation from Stryker Corporation, Richard Wolf GmbH, PENTAX Medical, Olympus Corporation, KARL STORZ SE & Co. KG, and Advanced Endoscopy Devices, Inc.. These players leverage global distribution networks, strong brand equity, and continuous innovation in flexible and digital ureteroscopes, imaging systems, and disposable technologies for urological procedures.

Rising demand for minimally invasive stone management is accelerating product development, with focus on high-definition visualization, improved deflection, single-use devices, and collaborations with hospitals to expand adoption.

Key Industry Developments:

- In February 2026, Stryker Corporation expanded its urology portfolio with the introduction of a new flexible ureteroscope. This launch strengthens its position in minimally invasive urological solutions by enhancing visualization, maneuverability, and procedural efficiency for kidney stone management.

- In October 2025, Dornier MedTech America introduced its Dornier Hoover Flexible and Navigable Suction Ureteral Access Sheath (FANS) and the Dornier Axis II Slim single-use ureteroscope with a 5.6 Fr distal tip in the United States, both of which received clearance from the U.S. Food and Drug Administration.

- In September 2025, Dornier MedTech America announced the U.S. commercial availability of its Dornier Hoover Flexible and Navigable Suction Ureteral Access Sheath (FANS) along with the Dornier Axis II Slim single-use ureteroscope featuring a 5.6 Fr distal tip for kidney stone treatment.

- In July 2024, U.S. Food and Drug Administration granted 510(k) clearance to Ambu A/S for its ureteroscopy solution, which includes the single-use digital flexible ureteroscope aScope 5 Uretero and the full-HD endoscopy system aBox 2.

- In April 2024, Olympus Corporation announced that the U.S. Food and Drug Administration granted 510(k) clearance for its first single-use ureteroscope system, RenaFlex™, with full commercial availability in the U.S. to be announced at a later stage.

Companies Covered in Ureteroscope Market

- Stryker Corporation

- Richard Wolf GmbH

- PENTAX Medical (Division of HOYA Corporation)

- Olympus Corporation

- KARL STORZ SE & Co. KG

- Advanced Endoscopy Devices, Inc. (AED)

- ELMED Electronics & Medical Industry & Trade Inc.

- Clarion Medical Technologies Inc.

- Shanghai SeeGen Photoelectric Technology Co., Ltd.

- Advin Health Care

- Innovex Medical Co., Ltd.

- Boston Scientific Corporation

- Cook Medical (Cook Group Incorporated)

- Dornier MedTech GmbH

- B. Braun Melsungen AG

- Others

Frequently Asked Questions

The global ureteroscope market is projected to be valued at US$ 1.6 Bn in 2026.

Rising prevalence of urolithiasis, increasing adoption of minimally invasive urological procedures, and rapid shift toward disposable and digital ureteroscopes.

The global Ureteroscope Market is poised to witness a CAGR of 5.9% between 2026 and 2033.

Expansion in emerging markets, growing demand for single-use ureteroscopes, and technological advancements in high-definition imaging and robotic-assisted urology.

Stryker Corporation, Richard Wolf GmbH, PENTAX Medical (Division of HOYA Corporation), Olympus Corporation, KARL STORZ SE & Co. KG, and Advanced Endoscopy Devices, Inc. (AED). are some of the key players in the ureteroscope market.