- Specialty & Fine Chemicals

- Urea Formaldehyde (UF) Market

Urea Formaldehyde (UF) Market Size, Share, and Growth Forecast, 2025 - 2032

Urea Formaldehyde (UF) Market by Product Type (Liquid Urea Formaldehyde Resin, Modified Urea Formaldehyde Resin, Powder Urea Formaldehyde Resin), Form (Powder, Liquid, Concentrate), Application, and Regional Analysis for 2025 - 2032

Urea Formaldehyde (UF) Market Share and Trends Analysis

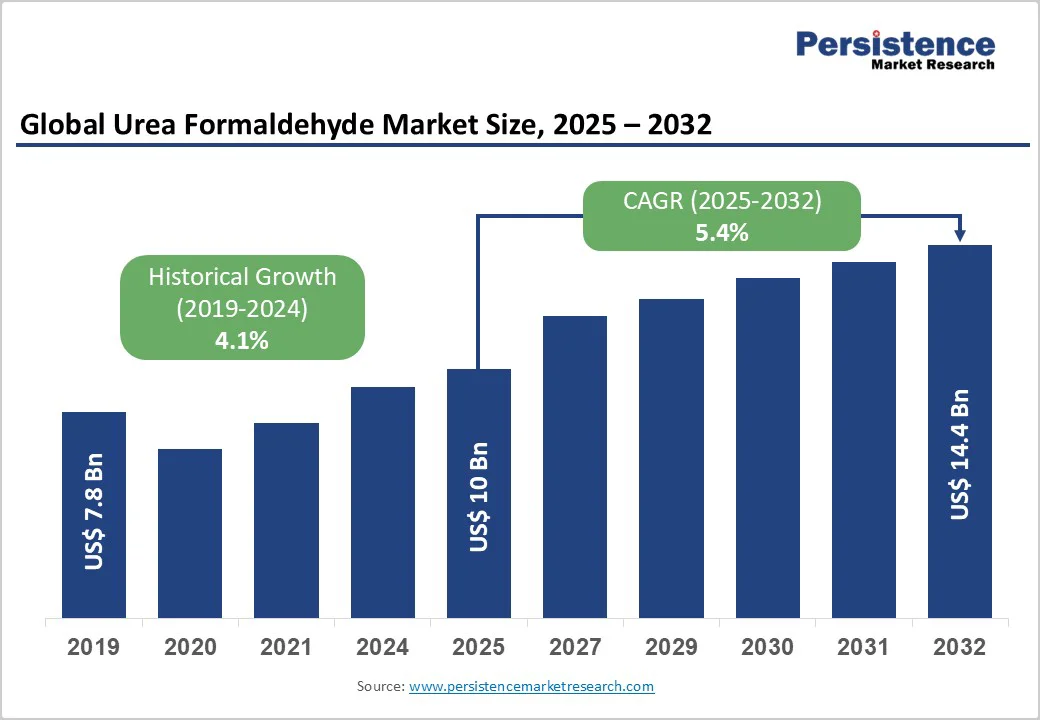

The global urea-formaldehyde (UF) market size is likely to be valued at US$10.0 billion in 2025 and is projected to reach US$14.4 billion by 2032, growing at a CAGR of 5.4% during the forecast period 2025 - 2032.

The demand for UF is driven by the expanding furniture & woodworking and building & construction industries, which are seeking cost-effective adhesives. At the same time, regulatory emphasis on low-emission resins is expected to spur innovation in the formulation of low-free formaldehyde and bio-based UF alternatives, bolstered by rising environmental standards and consumer awareness.

Key Industry Highlights

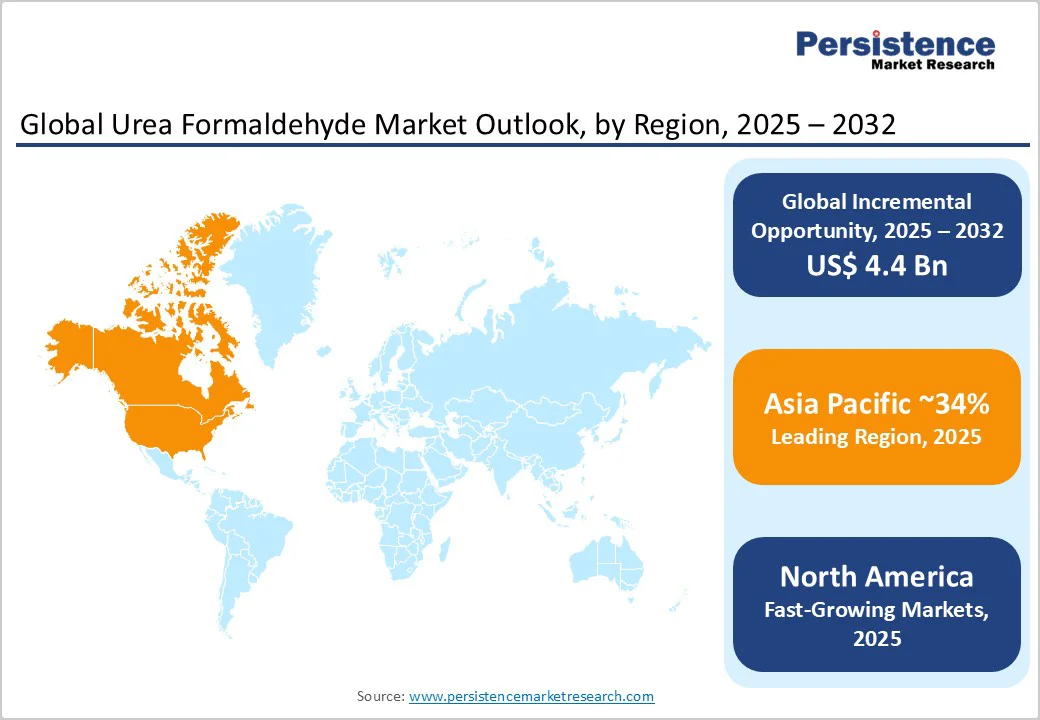

- Leading Region: Asia Pacific is slated to dominate the market in 2025, driven by widespread furniture and construction activity and supported by local manufacturing capacity.

- Fastest-growing Regional Market: North America is poised to be the fastest-growing regional market through 2032, propelled by stringent emission regulations and R&D incentives for low-free formaldehyde technologies.

- Dominant Application: The adhesives & binders segment is expected to lead in 2025, owing to urea formaldehyde's strong bonding properties and rapid curing characteristics.

- Fastest-growing Formulation Type: Low-free formaldehyde resin is expected to post the highest CAGR from 2025 to 2032, driven by regulatory push and health awareness.

- Key Market Opportunity: The expansion of bio-based UF alternatives through biorefinery partnerships to meet sustainability goals is envisioned to create vast growth opportunities.

| Key Insights | Details |

|---|---|

| Urea Formaldehyde Market Size (2025E) | US$10.0 Bn |

| Market Value Forecast (2032F) | US$14.4 Bn |

| Projected Growth CAGR (2025 - 2032) | 5.4% |

| Historical Market Growth (2019-2024) | 4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expanding Building & Construction Sector

The global surge in the building and construction industry, driven by rapid urbanization, population growth, and extensive infrastructure investments, has significantly increased demand for urea-formaldehyde resins. These resins are extensively used as adhesives in plywood, particleboard, and fiberboard due to their superior bonding strength, thermal stability, and cost-effectiveness.

Construction spending in emerging economies is widening the consumption of UF resins in residential and commercial projects. Furthermore, government initiatives promoting affordable housing and low-cost construction materials, such as India’s Pradhan Mantri Awas Yojana and China’s urban housing programs, are accelerating the adoption of UF resins.

Health and Environmental Concerns

Formaldehyde, a key component in UF resin production, is classified as a human carcinogen by the World Health Organization (WHO) and several regional health agencies. This has led to stringent regulations governing volatile organic compound (VOC) emissions and product labeling, particularly in North America and Europe. Manufacturers face significant challenges in reformulating traditional UF resins to meet these standards without compromising performance or cost efficiency.

The need for continuous emission testing, certification, and compliance monitoring has increased operational costs; smaller resin producers, in particular, face profitability pressures due to these regulatory burdens. Moreover, growing consumer environmental awareness and the shift toward eco-friendly materials in furniture and building applications further limit UF resin market expansion in regions with strict environmental policies.

Growth in Bio-Based UF Alternatives

The transition toward sustainable chemistry is opening significant growth opportunities for bio-based UF resin alternatives. Continuous R&D efforts have enabled the development of resins derived from renewable sources such as lignin, soy protein, and starch, offering comparable adhesive strength with reduced environmental footprint.

Major chemical companies are investing in collaborative ventures with agricultural biorefineries to ensure consistent bio-feedstock availability and cost stability. As the global bio-adhesives market experiences rapid expansion, urea-formaldehyde resin producers can leverage their technical expertise to diversify their product portfolios and enter emerging green adhesive segments. This strategic shift not only mitigates regulatory risks but also enhances brand positioning among environmentally conscious industries and consumers.

On the other hand, the automotive industry’s evolution toward lightweight, cost-efficient, and sustainable materials presents new opportunities for UF resin applications in interior components. With vehicle production surging worldwide, demand for UF-based composites, paneling, and carpet backings is likely to grow rapidly.

Modified UF resin formulations provide improved heat resistance, dimensional stability, and aesthetic appeal, all vital to modern automotive design. Furthermore, partnerships between UF resin manufacturers and original equipment manufacturers (OEMs) are fostering the development of tailored adhesive solutions that meet stringent automotive performance standards.

Category-wise Analysis

Product Type Insights

Liquid UF resin is currently the dominant product type, accounting for approximately 45% of the urea formaldehyde market revenue share in 2025. Its widespread use is driven by its ease of handling, rapid curing properties at ambient temperatures, and compatibility with large-scale industrial application methods such as spray and roll-coating processes.

The growth of liquid UF formulations is primarily fueled by extensive utilization in engineered wood applications, including board lamination and textile treatments. The balance of performance, cost efficiency, and processing flexibility offered by liquid UF resin makes it the preferred choice for manufacturers seeking to optimize production throughput without compromising adhesive quality.

Liquid UF resins often incorporate features such as low emissions and enhanced bonding capabilities, supporting regulatory compliance and meeting evolving customer demands.

Form Insights

Powder resin holds the largest market share, around 50% as of 2025. The preference for powder UF resin stems from its superior storage stability, which significantly extends shelf life compared to liquid alternatives. Furthermore, powder forms reduce transportation costs by eliminating the risks and logistics complications associated with liquid handling, such as spillage and evaporation.

These factors make powder resin the material of choice in molding compound manufacturing, where precise formulation control and batch consistency are critical. The growing demand for high-quality, moisture-resistant molded products in automotive, electrical, and industrial markets is projected to maintain the powder resin's dominant position, supported by ongoing formulation innovations enhancing product performance and environmental profiles.

Application Insights

The adhesives & binders segment is estimated to hold 55% market share in 2025. Adhesives and binders benefit from UF resin’s strong bonding characteristics, fast curing rates, and economic advantages, driving substantial adoption in the production of plywood, medium-density fiberboard (MDF), and particleboard. The steady growth of this segment is driven by rising demand for urea-formaldehyde in the construction and furniture manufacturing industries.

The segment's expansion is also driven by technological advancements, including low-formaldehyde formulations that align with stricter environmental regulations and green building standards. These factors collectively reinforce the dominance of adhesives and binders, cementing UF resins as a cornerstone for cost-effective, high-performance bonding solutions in engineered wood applications.

Regional Insights

North America Urea Formaldehyde Market Trends

North America is anticipated to lead the urea formaldehyde market share in 2025, driven by stringent formaldehyde emissions regulations under the U.S. Environmental Protection Agency (EPA) and a robust housing sector.

Investment in low-emission UF technologies has accelerated, with major producers establishing regional R&D centers. Meanwhile, Canada’s emphasis on green building certifications boosts the adoption of bio-based UF alternatives, encouraging collaborative programs between resin suppliers and construction firms.

Industrial innovation ecosystems in California and Texas foster pilot-scale production of advanced UF formulations that integrate next-generation curing catalysts. Government incentives for sustainable materials research have financed over US$50 billion in grants from 2022 to 2025, reinforcing the region’s leadership in low-impact UF resin development.

Europe Urea Formaldehyde Market Trends

In Europe, regulatory harmonization under REACH is stimulating the adoption of ultra-low formaldehyde resins, with manufacturers investing in automated production lines to maintain compliance. France and the U.K. are focusing on energy-efficient UF resin processes, seeking to reduce CO2 emissions per ton of resin produced.

Moreover, collaboration among European Union (EU) member states on circular economy initiatives has promoted recycling of wood composites, indirectly boosting UF resin demand for re-bonding applications. Regulatory frameworks across Europe prioritize worker safety and environmental impact, accelerating the shift toward low-free formaldehyde resin in decorative laminates and floorings.

Asia Pacific Urea Formaldehyde Market Trends

China leads the Asia Pacific market, driven by its massive furniture and textile manufacturing sectors, which together account for over 50% of regional UF resin consumption. Rapid urbanization in India has spurred demand for low-cost housing, elevating UF resin use in particleboard and plywood. ASEAN countries leverage favorable raw material availability and lower production costs, fostering investment in new UF resin plants.

Japan’s focus on high-performance modified resins for electrical insulation has been strengthening, with significant annual expansions in production capacity. Regional manufacturers benefit from government-backed R&D grants exceeding US$20 billion between 2021 and 2024 to develop bio-based alternatives, bolstering the position of the Asia Pacific in sustainable urea formaldehyde technologies.

Competitive Landscape

The global urea-formaldehyde market exhibits a moderately consolidated structure, with key players such as BASF SE, Hexion, and Acron PJSC commanding significant market share through expansive product portfolios and global distribution networks.

Companies pursue capex investments in low-emission resin lines and strategic partnerships with raw material suppliers. Innovation in catalyst systems and green chemistry serves as a key differentiator. At the same time, emerging business models focus on licensing of proprietary resin formulations to local producers, enhancing market reach and flexibility.

Key Industry Developments

- In October 2025, Al-Ahram Chemicals announced that it will be investing US$10 million to build a formaldehyde and derivatives production complex in the Sokhna Industrial Zone, with operations expected to start in early 2027. The facility will produce 25,000 tons each of formaldehyde and form urea annually, creating around 150 jobs. The project supports Egypt’s strategy to localize chemical manufacturing, reduce import dependence, and boost export-oriented industrial growth within the Suez Canal Economic Zone, leveraging its strategic location and investment incentives.

- In August 2025, Acron Group expanded its ammonium nitrate production capacity at its Voskresensk plant, with a new high-capacity granulator entering operation. This investment aims to meet growing domestic and international demand for ammonium nitrate, a key fertilizer component. The new granulator will enhance production efficiency, product quality, and compliance with environmental standards. Acron’s expansion reflects ongoing efforts to strengthen its supply chain and support agricultural productivity growth while adhering to sustainable manufacturing practices.

- In April 2025, Mitsubishi Gas Chemical Company (MGC), in collaboration with Panasonic Electric Works, developed an eco-friendly urea resin using methanol produced from CO22. This innovative resin reduces CO2 emissions by 20-30% compared to conventional urea resins and is intended for use in wiring devices such as electrical outlets. The new resin offers the same molding and physical properties as traditional urea resin, enabling it to be processed with existing equipment while contributing to carbon recycling. MGC produces methanol from CO2, waste, and biomass, leveraging its Carbopath™ platform to support a decarbonized, recycling-oriented future through cross-sector collaborations.

Companies Covered in Urea Formaldehyde (UF) Market

- Acron PJSC

- ARCL Organics Ltd.

- Asta Chemicals

- Bakelite Synthetics

- BASF SE

- Biqem

- Capital Resin Corporation

- Hexion

- LRBG Chemicals

- Metadynea

- Sadepan

- Advachem SA

- Hexzachem Sarawak Sdn Bhd

- Additional: DSM

- Dynea

- Sumitomo Bakelite

Frequently Asked Questions

The global urea formaldehyde (UF) market is projected to reach US$ 10.0 billion in 2025.

The massive expansion of the building & construction sector, fueled by unprecedented urbanization and large-scale infrastructure projects, is the primary market driver.

The market is poised to witness a CAGR of 5.4% from 2025 to 2032.

Developing bio-based UF alternatives via partnerships with agricultural biorefineries presents the most significant growth opportunity.

BASF SE, Hexion, and Acron PJSC are few of the key market players.