- Inks, Coatings, Adhesives & Sealants (ICAS)

- Underbody Anti-Rust Coating Market

Underbody Anti-Rust Coating Market Size, Share, and Growth Forecast, 2026 – 2033

Underbody Anti-Rust Coating Market by Product Type (Water-based Coatings, Solvent-based Coatings, Powder Coatings, Elastomeric Coatings), Application (Brush Application, Spray Application, Roller Application, Dip Application), End-User (Automotive, Aerospace, Marine, Construction, Industrial Machinery), and Regional Analysis for 2026-2033

Underbody Anti-Rust Coating Market Share and Trends Analysis

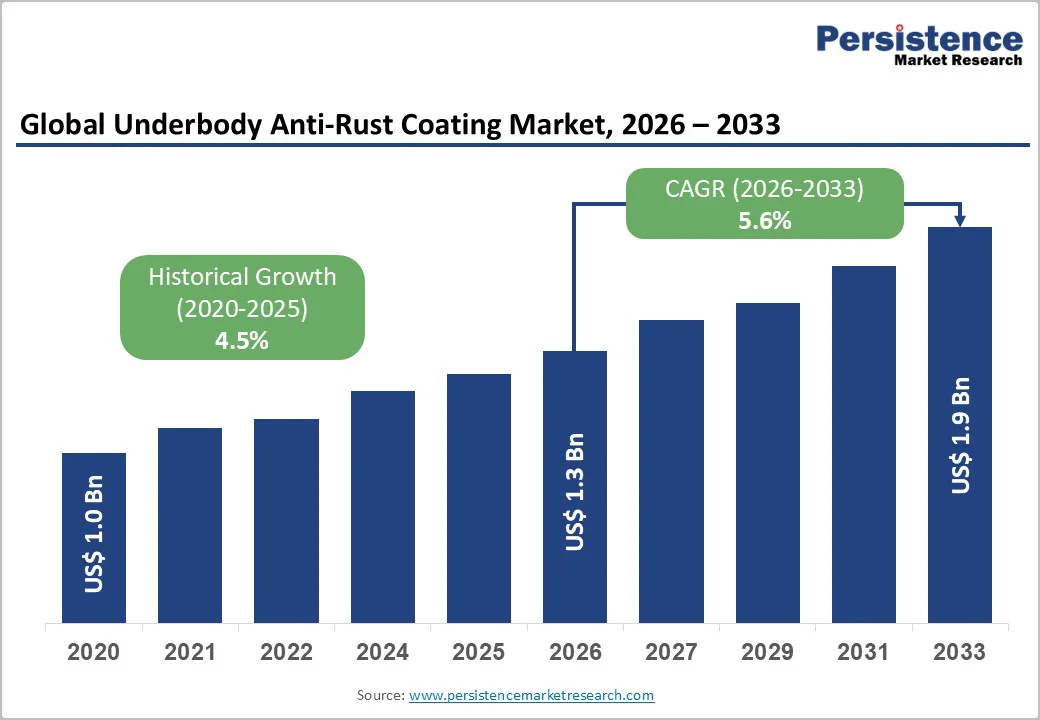

The global underbody anti-rust coating market size is likely to be valued at US$ 1.3 billion in 2026 and is estimated to reach US$ 1.9 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026−2033. The primary growth is driven by increasing automotive production worldwide, especially in emerging economies, along with stricter environmental and anticorrosion regulatory standards, pushing the adoption of advanced coatings. Additional demand for rust protection solutions arises from growth in non-automotive sectors such as industrial machinery and marine industries, while technological advances in eco-friendly and durable formulations support market expansion.

Key Industry Highlights

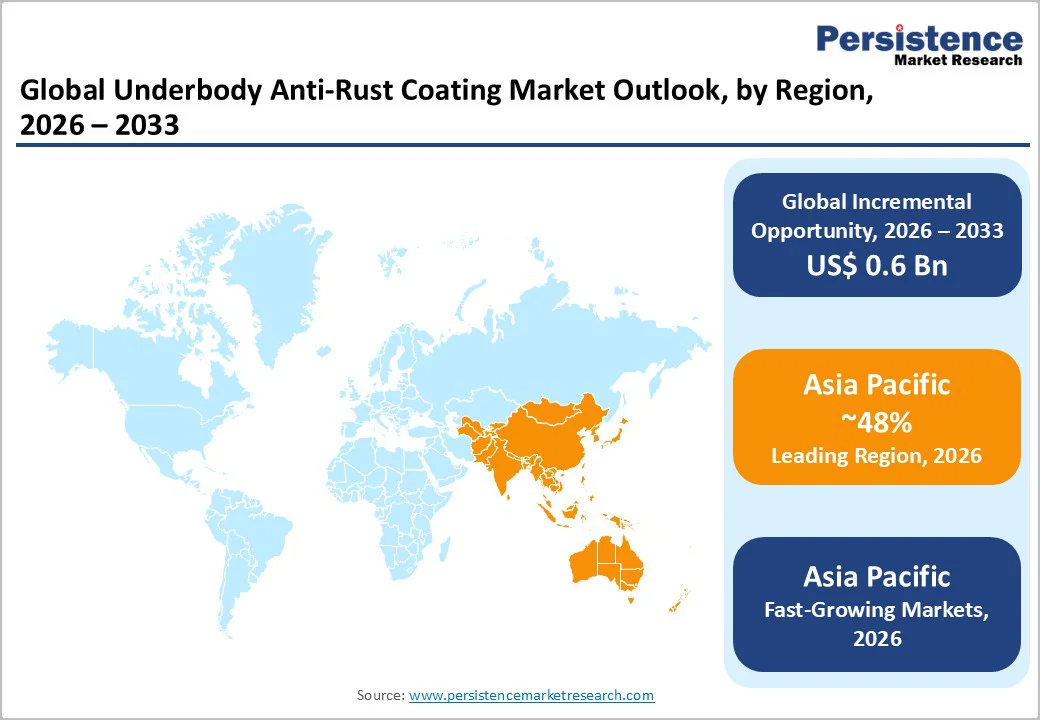

- Dominant Region: Asia Pacific is forecast to hold a 48% market share in 2026, driven by large automotive manufacturing, localized supply chains, and strengthening environmental policies.

- Fastest-growing Regional Market: Asia Pacific is also likely to be the fastest-growing market through 2033, fueled by an exponential increase in vehicle ownership in India, China, and the ASEAN bloc.

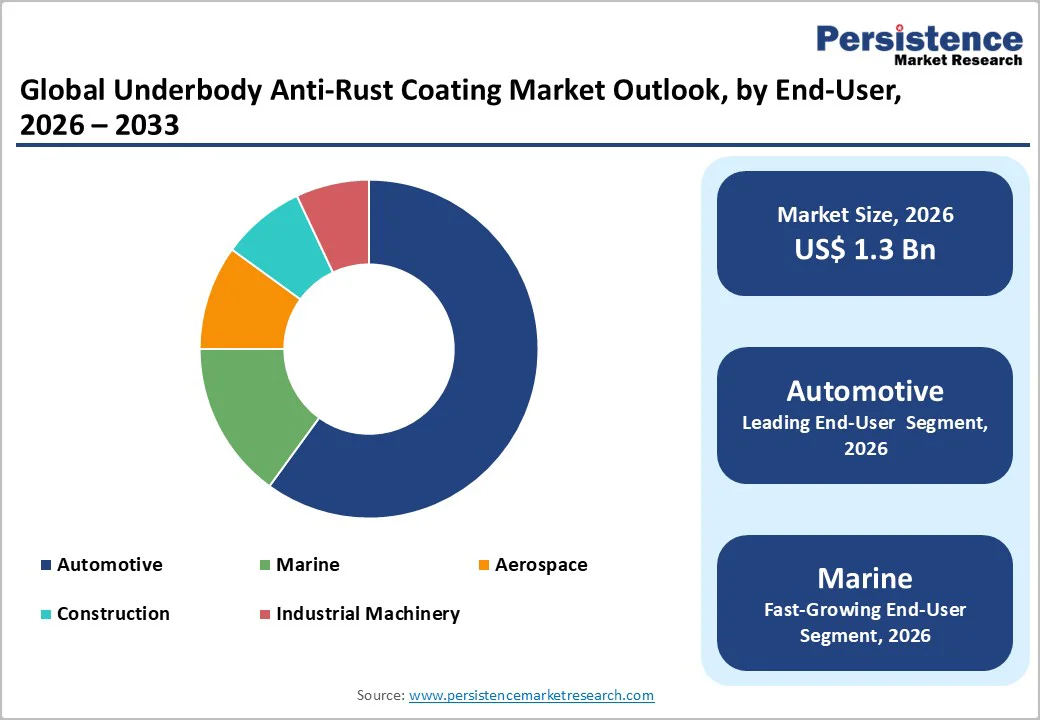

- Leading End-User: Automotive is forecast to lead with a 60% market share in 2026, driven by continuous growth in global vehicle production and strict corrosion standards.

- Fastest-growing End-User: Marine is projected to be the fastest-growing segment for the 2026-2033 period, owing to high salinity exposure, fleet expansion, and urgent need for durable, low-maintenance underbody protection.

| Key Insights | Details |

|---|---|

| Underbody Anti-Rust Coating Market Size (2026E) | US$ 1.3 Bn |

| Market Value Forecast (2033F) | US$ 1.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Automotive Production and Vehicle Longevity Needs

Higher production levels of vehicles have raised the baseline demand for protective coatings, as original equipment manufacturers (OEMs) aim to maintain structural integrity standards and deliver vehicles capable of performing under varied climatic and road conditions. As production hubs scale up in emerging economies, exposure to humidity, salinity, and unpaved terrain strengthens the requirement for robust underbody protection during initial assembly.

Longer operational life expectations for modern vehicles further elevate the relevance of protective coatings. Consumers seek extended durability, prompting manufacturers and service providers to apply solutions that safeguard essential components from premature degradation. Underbody coatings support lifecycle efficiency by reducing maintenance costs and preserving chassis performance throughout extended usage cycles. This strategic focus aligns with industry goals centered on reliability, value retention, and long-term fleet performance, reinforcing the role of corrosion-resistant technologies within the wider automotive ecosystem.

High Raw Material Costs and Supply Chain Volatility Needs

The high prices of raw materials have remained major restraint for the market, as key inputs such as specialty polymers, additives, and corrosion-resistant chemicals face frequent cost fluctuations driven by global commodity cycles and energy price movements. These materials form the core of protective formulations, so any spike elevates production expenses and pressures margins. Manufacturers often struggle to maintain stable pricing, creating challenges for long-term planning and contract commitments. This cost sensitivity limits the ability of suppliers to scale operations or invest in advanced formulations, influencing overall competitiveness.

Supply chain volatility further intensifies the constraint. Disruptions in logistics, shortages of chemical intermediates, and inconsistent availability of critical inputs extend lead times and reduce production reliability. These uncertainties complicate inventory strategies and elevate operational risk for both producers and end-use industries. Volatility also slows down technology deployment, as companies prioritize short-term continuity over innovation. Such instability impacts delivery performance and affects buyer confidence, creating hurdles for sustained adoption and market penetration.

Strong Automotive Sector Growth in Asia Pacific

The explosive expansion of automotive manufacturing across the developing economies of Asia Pacific presents an unprecedented market opportunity. Skyrocketing vehicle ownership, rapid urban development, and expanding manufacturing ecosystems in the region have accelerated the demand for protective solutions. Governments are investing heavily in road networks, industrial corridors, and freight infrastructure, increasing exposure of vehicles and machinery to harsh environmental conditions. This creates a strategic need for robust corrosion protection, prompting original equipment manufacturers and aftermarket service providers to integrate advanced coating technologies into their offerings.

Local production growth, rising disposable incomes, and the shift toward modern mobility platforms strengthen the outlook further. Automotive plants, component suppliers, and industrial equipment manufacturers are scaling capacity to meet surging domestic demand, creating a large addressable base for protective materials. This environment supports long-term volume growth, encourages partnerships with regional manufacturers, and positions suppliers to capture value through localized, high-performance formulations tailored to climate challenges such as humidity, rainfall, and coastal exposure.

Category-wise Analysis

Product Type Insights

Water-based coatings are projected to command leadership with a approximately 45% of the underbody anti-rust coating market revenue share in 2026, driven by regulatory alignment and lower volatile organic compound profiles that facilitate compliance. OEMs favor these formulations for consistent adhesion in moisture-prone environments, seamless integration into production lines, and predictable lifecycle performance. This positioning reinforces procurement strategies and long-term supplier relationships for corrosion protection.

Elastomeric coatings are anticipated to expand at the fastest pace from 2026 to 2033 due to their superior flexibility and resilience on substrates exposed to continuous vibration and stress. Fleet operators and marine constructors seek formulations that maintain sealing and impact resistance under dynamic loads, making these coatings attractive for retrofit and new projects. Suppliers can capture share effectively through targeted product positioning, technical service and localized supply arrangements.

Application Insights

Spray application is anticipated to maintain leadership with around 50% market share in 2026, supported by its ability to deliver consistent, uniform coverage across large surfaces. High throughput capability aligns with the needs of high-volume automotive production, enabling manufacturers to meet cycle time targets while ensuring reliable corrosion protection. Its operational efficiency strengthens adoption across established and emerging assembly programs.

Dip application is expected to advance as the fastest-expanding method between 2026 and 2033, as a result of its strong suitability for complex geometries and enclosed underbody structures. The process enhances material utilization, supports reduced coating waste and delivers full surface penetration, making it valuable for aerospace, specialty vehicles and industrial equipment. Its controlled application environment improves consistency, positioning it as a strategic choice for precision-driven manufacturing operations.

End-User Insights

Automotive is forecast to retain leadership with about 60% market share in 2026, supported by expansive global vehicle production and stringent corrosion protection standards embedded into original equipment manufacturer specifications. High output volumes, structured procurement cycles and integration of protective coatings into mandatory assembly processes reinforce its dominant position across passenger, commercial and utility vehicle platforms.

Marine is projected to showcase the highest CAGR during the 2026-2033 forecast period, as vessels operate in high salinity, high humidity and abrasive environments that accelerate corrosion risk. Rising fleet additions, expanding coastal logistics activity and increased maintenance requirements strengthen the need for durable underbody protection solutions. Shipbuilders and operators prioritize formulations that deliver extended service life, operational reliability and reduced maintenance downtime in ocean-exposed conditions.

Regional Insights

North America Underbody Anti-Rust Coating Market Trends

North America maintains a strong position in the market due to its mature automotive industry, high vehicle production volumes, and stringent environmental and safety regulations. Regional OEMs have prioritized corrosion-resistant materials to meet federal and state standards, while a well-established aftermarket ecosystem reinforces the adoption of advanced coatings, ensuring long-term vehicle durability and performance across passenger and commercial fleets.

Regional market growth is also being driven by an increasing demand for durable and long-lasting vehicles, expansion of commercial and electric vehicle fleets, and exposure to harsh winter conditions that accelerate corrosion from road salts and de-icing chemicals. Technological advancements, including water-based and eco-friendly formulations, support regulatory compliance without compromising performance. Investments in automated application systems across assembly lines and service networks enhance efficiency and uniformity, positioning North America as a stable market with sustained adoption of protective underbody coatings across both original equipment and aftermarket segments.

Europe Underbody Anti-Rust Coating Market Trends

Europe holds a significant position in the market, aided by stringent automotive regulations, high vehicle safety standards, and widespread adoption of advanced manufacturing technologies. In order to comply with the directives of the European Union (EU) on vehicle durability and environmental impact, OEMs have been emphasizing on durable corrosion protection solutions. The mature automotive industry, combined with strong consumer expectations for long-lasting vehicles, reinforces consistent demand for high-performance coatings.

Market growth in Europe is supported by increasing production of premium and electric vehicles (EVs), which require specialized underbody protection to ensure longevity and safety. Harsh winter conditions, high humidity in coastal regions, and frequent exposure to road salts amplify corrosion risks, creating a steady need for advanced coatings. Investments in eco-friendly formulations, automated application processes, and localized research and development centers enhance coating performance and regulatory compliance, enabling manufacturers to maintain efficiency and competitiveness in the European automotive and industrial sectors.

Asia Pacific Underbody Anti-Rust Coating Market Trends

Asia Pacific is forecast to hold an estimated 48% of the underbody anti-rust coating market share in 2026, supported by its structurally large automotive manufacturing ecosystem and deep localization of supply chains. The region’s leadership stems from the concentration of high-capacity assembly plants, integrated steel and component clusters, and a cost-competitive manufacturing base that encourages early adoption of protective technologies. Accelerated wear from monsoon exposure, coastal humidity, and uneven road infrastructure intensifies the need for durable underbody protection, prompting OEMs to standardize advanced coating layers across new vehicle platforms. Policy frameworks promoting reduced emissions and improved material efficiency further drive the transition toward environmentally compliant formulations, strengthening the region’s structural advantage.

Asia Pacific is also poised to be the fastest-growing regional market through 2033 due to expanding middle-class mobility, rising commercial fleet utilization, and increasing aftermarket penetration as vehicles remain in service for longer cycles. Growth is reinforced by infrastructure expansion across Southeast Asia, which heightens exposure to corrosive environments and elevates maintenance requirements. Shipbuilding hubs, industrial equipment producers, and logistics operators are adopting high-performance coatings to extend asset life in high-salinity and high-moisture corridors. Strategic investments by coating manufacturers in localized R&D centers and automated application facilities enhance technological readiness, enabling faster deployment of tailored solutions and securing sustained regional growth momentum.

Competitive Landscape

Multinational chemical and coating enterprises command the global underbody anti-rust coatings market landscape in developed economies through established brand recognition, unwavering regulatory compliance, and rigorous quality protocols. These industry leaders secure substantial market positions and durable partnerships with OEMs and fleet operators by delivering consistently reliable corrosion protection solutions. The concentration reflects their capacity to invest in advanced formulation research, manufacturing infrastructure, and technical support systems that smaller competitors cannot replicate. Stringent environmental and performance standards in developed markets favor companies with sophisticated compliance frameworks and certification capabilities.

Emerging market segments display fundamentally different competitive characteristics, where numerous regional and localized suppliers gain traction through aggressive pricing strategies and streamlined operations. Lower regulatory stringency and cost-conscious purchasing decisions enable smaller firms to maintain viable market positions across Asia, Latin America, and Africa. This bifurcated market structure creates distinct strategic imperatives. Multinational players pursue innovation and premium positioning in mature geographies while selectively penetrating emerging regions through acquisitions, partnerships, or localized product development. Regional suppliers sustain competitiveness through supply chain efficiency and operational flexibility, though consolidation pressures may reshape this fragmentation over time as global environmental regulations intensify and customer expectations converge toward higher performance standards.

Key Industry Developments

- In August 2025, researchers from India and Germany developed a multifunctional epoxy/polyvinylidene fluoride (PVDF) coating incorporating zeolitic imidazolate framework (ZIF-8) nanosensors for mild steel corrosion protection. The system combines benzotriazole-loaded particles for self-healing through pH-responsive inhibitor release, phenanthroline-modified particles for Fe²? ion detection with visual red-complex formation, and superhydrophobic properties up to 157-degree contact angles.

- In June 2025, researchers at the Hebrew University of Jerusalem developed a duplex anti-corrosion system for iron that combines an N-heterocyclic carbene (NHC) monolayer primer with a UV-cured cross-linked polymer network (CPN), dramatically improving adhesion and durability. In 3.5% sodium chloride tests, the NHC + CPN coating reduced corrosion current by over two orders of magnitude and achieved about 99.6% rust protection after 24 hours without blistering or delamination.

- In March 2025, Sherwin-Williams Protective & Marine expanded its Global Core coatings with Zinc Clad 2500 inorganic zinc primer, Macropoxy 4600 and 2600 epoxy primers or intermediates, and Acrolon 7700 acrylic polyurethane topcoat. These products feature fast drying, low-temperature cure, and simplified mix ratios, formulated to protect carbon steel in severe C5 and higher corrosive environments across infrastructure, energy, manufacturing, and water treatment applications.

Companies Covered in Underbody Anti-Rust Coating Market

- 3M

- DuPont

- PPG Industries

- AkzoNobel

- BASF

- Henkel

- Sherwin-Williams

- Axalta Coating

- ThreeBond

- KATS Coatings

- Guangzhou Carelay

- Usha Chemicals

- Sunstar Engineering

Frequently Asked Questions

The global underbody anti-rust coating market is projected to reach US$ 1.3 billion in 2026.

Massive global vehicle production, stringent corrosion and environmental regulations, and demand for durable, eco-friendly protective coatings drive the market.

The market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Growth in marine and industrial applications and strengthening adoption of advanced eco-friendly formulations present key market opportunities.

Some of the key market players include 3M, DuPont, PPG Industries, AkzoNobel, BASF, Henkel, Sherwin-Williams, and Axalta Coating.