- Industrial Machinery

- Turbo Compressor Market

Turbo Compressor Market Size, Share, and Growth Forecast, 2026 – 2033

Turbo Compressor Market by Product Type (Centrifugal, Axial), Stage (Single-Stage, Multi-Stage), Application (Oil & Gas, Power Generation, Chemical, Water & Wastewater, Automotive, Mining, Others), Regional Analysis for 2026–2033

Turbo Compressor Market Share and Trends Analysis

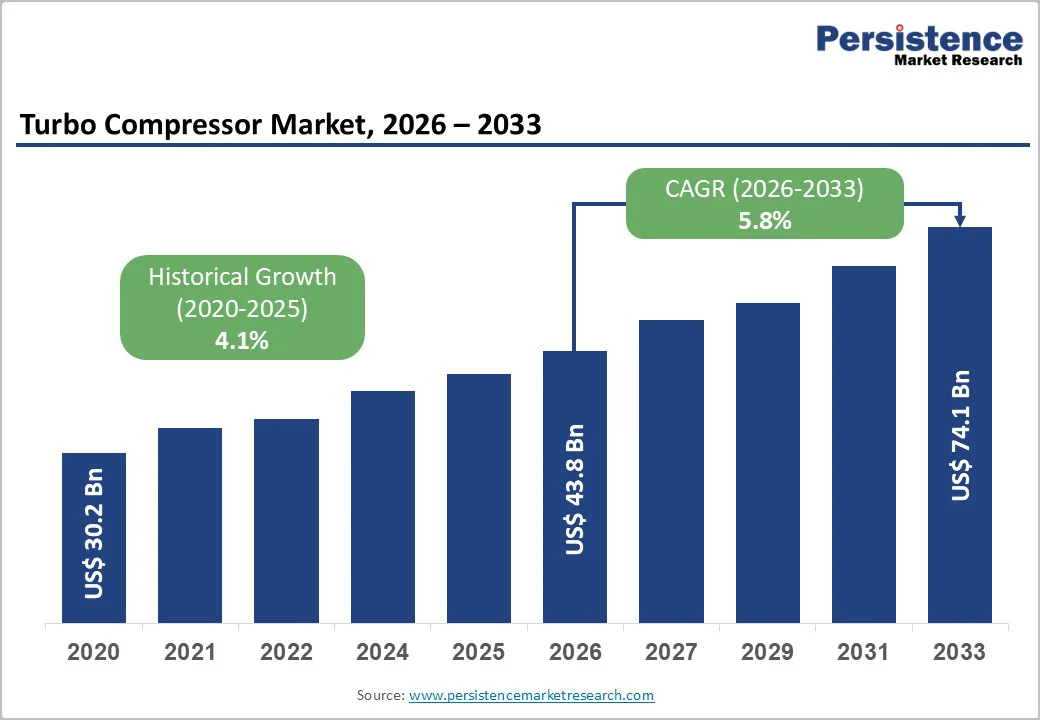

The global turbo compressor market size is likely to be valued at US$ 22.3 billion in 2026, and is projected to reach US$ 33.1 billion by 2033, growing at a CAGR of 5.8% during the forecast period 2026-2033. This robust growth trajectory is underpinned by sustained demand across critical industries such as energy, chemicals, and infrastructure, where efficient gas compression is essential for operational continuity and productivity. Rising industrialization in emerging markets, coupled with increasing requirements for reliable compression solutions in oil and gas and power generation applications, continues to drive market expansion and investment in high-performance compressor technologies that can operate under demanding conditions. Improvements in turbo compressor efficiency, reliability, and maintenance profiles are expanding their adoption beyond traditional sectors into areas such as water and wastewater treatment, mining operations, and specialized chemical processing. These innovations enable operators to reduce energy consumption and lifecycle costs while meeting increasingly stringent environmental and performance standards.

Key Industry Highlights

- Dominant Product Type: Centrifugal compressors are likely to dominate in 2026 with around 60% revenue share due to their wide industrial adoption and efficiency.

- Fastest-Growing Product Type: Axial compressors are set to grow the fastest through 2033, driven by their high-flow property and large-scale, cross-industry demand.

- Leading Stage Type: Single-stage compressors are projected to lead in 2026 with an estimated 45% share, owing to their cost efficiency and suitability for moderate pressures.

- Fastest-Growing Stage Type: Multi-stage compressors are likely to expand the fastest through 2033, as high-pressure needs rise in LNG and petrochemicals.

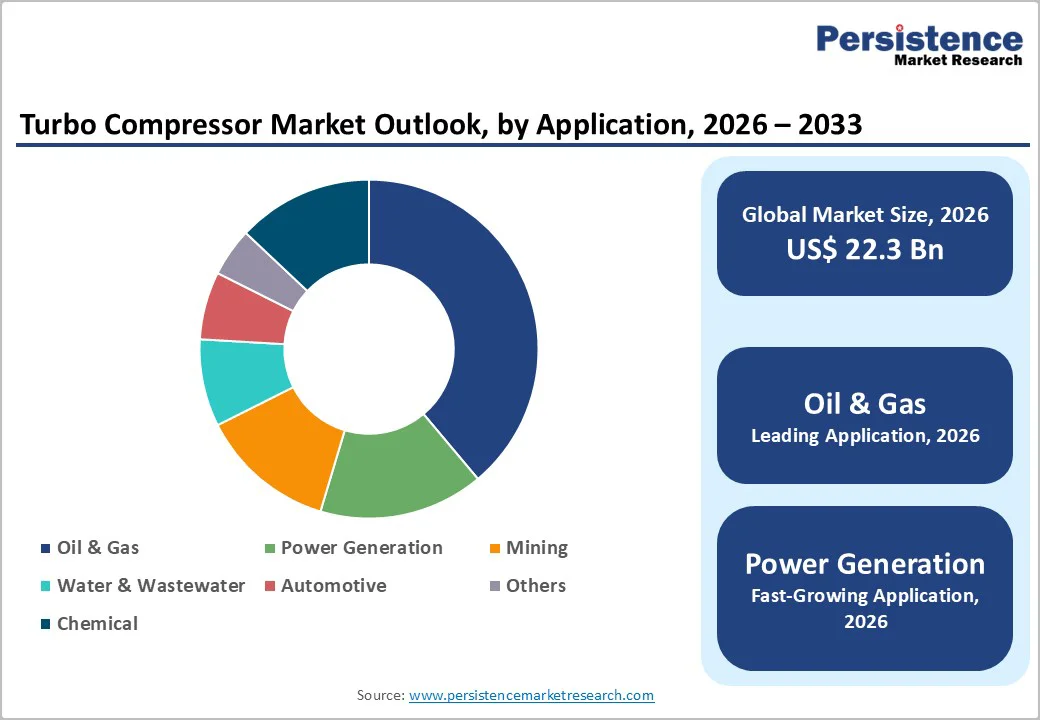

- Dominant Application: Oil & gas is expected to be the most dominant segment in 2026, supported by persistent gas compression demand.

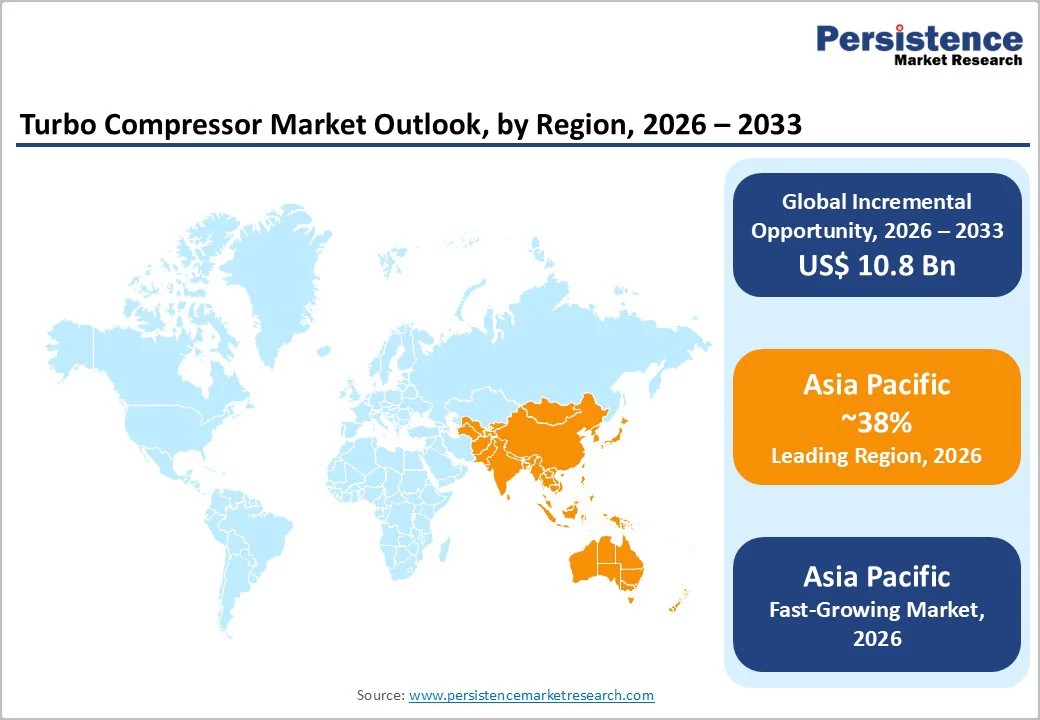

- Leading Region: Asia Pacific is expected to lead between 2026 and 2033, fueled by rapid industrialization and infrastructure expansion.

| Key Insights | Details |

|---|---|

| Turbo Compressor Market Size (2026E) | US$ 22.3 Bn |

| Market Value Forecast (2033F) | US$ 33.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Industrial Demand and Efficiency-Focused Modernization Drives

The turbo compressor market growth is driven by expanding energy, chemical, and industrial activity, with oil & gas and petrochemicals remaining core demand centers due to continuous, high-capacity gas handling requirements. Rising exploration, higher natural gas transport volumes, and scaling of downstream chemical processing intensify the need for reliable compression systems. Rapidly growing applications in power generation, water & wastewater, mining, and manufacturing add momentum, especially in emerging economies with expanding infrastructure. Policy and funding support, including Japan’s Green Innovation Fund (GIF) and Joint Crediting Mechanism (JCM) FY2025 allocations up to ¥ 15 billion, further encourage adoption of high-efficiency industrial technologies.

Industries are increasingly prioritizing energy efficiency and lower emissions, accelerating adoption of advanced centrifugal and multi-stage compressors for stable, high-volume performance. Government-backed programs such as GIF and JCM underscore commitment to energy transition and industrial modernization, fostering cleaner, more efficient equipment deployment. As companies upgrade facilities and replace aging systems, demand for energy-efficient compressors grows across established and emerging markets. This alignment of industrial demand, technology upgrades, and policy support strengthens global turbo compressor deployment and shapes long-term market expansion.

High Cost Burdens and Supply Chain Pressures

The turbo compressor market expansion faces a significant restraint rooted in the high capital and operational costs associated with advanced compression systems, particularly large centrifugal and axial units that require substantial investment for installation and commissioning. Their maintenance demands, often involving precision components, specialized servicing, and skilled technicians, add to lifecycle expenses, limiting adoption among smaller operators and cost-sensitive industries. These financial barriers can delay modernization plans, extend the use of older equipment, or shift preference toward more affordable compression alternatives.

Compounding the cost challenge are ongoing supply chain constraints and raw material price fluctuations that affect the availability of high-grade steel, engineered parts, and critical components essential for manufacturing high-performance compressors. Disruptions in sourcing or extended lead times can impede production schedules, drive up procurement costs, and reduce the ability of end users to plan timely replacements. Such uncertainties not only elevate total ownership costs but also weaken investment confidence, collectively slowing market expansion across key industrial sectors.

Advanced Technologies and Expanding Industrial Applications

The growth prospects of the market are gaining strength owing to the rising adoption of modern, energy-efficient, and digitally enabled technologies that enhance performance, reduce lifecycle costs, and enable predictive maintenance. For example, IHI’s TRZ Series centrifugal compressors, launched in May 2025, offer roughly 15% higher flow, improved efficiency, and lower operating costs. Combined with innovations such as magnetic bearings and variable-speed control, these next-generation compressors provide reliable, sustainable, and cost-effective solutions. End users prioritizing energy efficiency and reduced downtime are increasingly favoring technologically advanced systems, opening opportunities for higher-value segments and long-term service partnerships.

Parallel to this trend, expanding infrastructure and industrial activity in emerging economies are creating new demand for turbo compressors across water and wastewater treatment, mining, and diversified manufacturing. Investments in ventilation, dewatering, process aeration, and high-volume gas handling are driving under-penetrated markets. Fast-growing economies accelerating energy, utilities, and heavy industry development present strong opportunities for manufacturers delivering efficient, scalable, and region-specific turbo compressor solutions.

Category-wise Analysis

Product Type Insights

Centrifugal compressors are projected to hold the dominant position with an estimated 60% market share in 2026, driven by their versatility, high efficiency, and ability to handle large gas volumes across critical industries such as oil & gas, chemicals, and power generation. Their stable operation, lower maintenance requirements, and suitability for continuous-duty environments reinforce their leadership. In 2025, for instance, Mitsubishi Heavy Industries developed electric centrifugal compressors for fuel-cell systems with lightweight rotors, oil-free air bearings, and high-efficiency designs, demonstrating the technology’s relevance beyond traditional industrial applications. These innovations highlight the continued modernization and expansion of centrifugal compressors into emerging sectors.

Axial compressors, while representing a smaller installed base, are projected to grow at a CAGR of approximately 7.2% through 2033, making them the fastest-growing product type. The adoption of these compressors is accelerating in high-flow, high-speed applications such as gas turbines, propulsion systems, and large-scale ventilation or energy systems. Rising demand for higher throughput, improved aerodynamic efficiency, and advanced large-volume handling systems, along with emerging opportunities in renewable energy and motor-driven power systems, is supporting their growth trajectory.

Stage Type Insights

Single-stage turbo compressors are likely to lead the market with an estimated 45% revenue share in 2026, on account of their simpler design, lower operational cost, and suitability for moderate-pressure industrial processes. Their ease of installation, reduced maintenance needs, and strong reliability make them ideal for applications such as general manufacturing, heating, ventilation, & air conditioning (HVAC) systems, and medium-duty continuous operations. Industries that prioritize lower lifecycle costs without requiring extreme discharge pressures continue to favor these systems, reinforcing their broad industrial adoption.

Multi-stage compressors are expected to grow at an estimated CAGR of 6.5% during the 2026-2033 forecast period, propelled by increasing demand for high-pressure applications across LNG terminals, petrochemical synthesis units, gas pipelines, and expanding heavy industrial projects. For example, in 2025, MAN Energy Solutions supplied multi-shaft, multi-stage CO? compressor trains (type RG90?8) to the Tangguh LNG plant in Indonesia, designed to compress CO? up to 165 bar, demonstrating the critical role of multi-stage systems in high-pressure industrial operations. These configurations deliver higher discharge pressures, improved performance stability, and greater suitability for large-scale, high-demand applications, supporting long-term growth.

Application Insights

Oil & gas are slated to remain the largest application segment, capturing 42% of the turbo compressor market revenue share in 2026, reflecting its essential need for gas compression across upstream extraction, midstream transportation, and downstream refining. Turbo compressors play a central role in gas reinjection, pipeline boosting, refinery operations, and the processing of natural gas liquids. Their reliability and ability to operate under demanding pressure and flow conditions make them indispensable in ensuring operational continuity across the energy value chain, sustaining their long-standing market leadership.

Power generation and water & wastewater collectively represent the fastest-growing application areas with an estimated CAGR of 6.8% through 2033, driven by rising global energy demands, expansion of thermal and turbine-based plants, and intensifying investments in modern water treatment infrastructure. These sectors increasingly require efficient, stable, and high-capacity compression systems to support aeration, ventilation, and process gas handling. Growing mining activity and industrial diversification further support uptake, as facilities seek durable, high-performance compressors to meet escalating operational loads and regulatory expectations.

Regional Insights

North America Turbo Compressor Market Trends

North America remains one of the most influential regions in the turbo compressor market landscape, predicted to hold an estimated 32% market share in 2026, powered by its advanced industrial ecosystem and well-established oil & gas infrastructure. The United States leads with extensive deployment across refineries, gas pipelines, petrochemical plants, and combined-cycle power facilities. Strong regulatory focus on emission control, energy efficiency, and modernization is prompting industries to replace older equipment with next-generation centrifugal and axial compressors. The regional market also benefits from robust engineering capability, strong R&D investment, and the availability of advanced high-efficiency compressor technologies.

Despite its maturity, North America continues to experience stable, technology-driven growth supported by retrofit projects, LNG capacity additions, and upgrades across industrial facilities. Regional manufacturers are also playing a major role in exporting compressor modules and engineered systems to global markets. Growth is more incremental than expansionary, shaped by demand for reliability, reduced downtime, and operational optimization. As industrial operations transition toward digital monitoring and predictive maintenance, the adoption of modern, IoT-enabled compressors is rising. North America thus remains a leading and innovation-centric market, emphasizing efficiency upgrades and performance enhancement over large-scale new installations.

Europe Turbo Compressor Market Trends

Europe is expected to hold approximately 26% of the turbo compressor market share in 2026, supported by strong demand in chemical processing, power generation, refining, and advanced manufacturing. Countries such as Germany, France, the U.K., Italy, and Spain are key contributors, driven by stringent energy-efficiency and emission-control regulations that encourage modernization of industrial compression systems. The region is steadily shifting toward high-efficiency, low-emission centrifugal and axial compressors to meet evolving sustainability standards. Enhancements in hydrogen, biogas, carbon-capture systems, and clean-fuel infrastructure are also opening new avenues for compressor deployment.

While the Europe market growth is moderate, it remains consistent due to a large installed base requiring refurbishment, technology upgrades, and long-term maintenance contracts. Growth is driven more by replacement cycles than new Greenfield projects, reflecting the region’s industrial maturity. Integration of renewable energy systems also encourages deployment of flexible compression technologies for grid support and gas handling. The competitive landscape is dominated by advanced original equipment manufacturers (OEMs) offering digitally enhanced and energy-optimized solutions. Europe continues to evolve as a stable, regulation-driven market focused on high-performance equipment and long-term service partnerships, contributing steadily to global demand.

Asia Pacific Turbo Compressor Market Trends

Asia Pacific is expected to be the fastest-growing as well as the leading market for turbo compressors, expanding at an estimated CAGR of 7.5% through 2033 and projected to secure around 38% of the global market share in 2026. The region’s rapid industrialization is fueled by major investments in oil refineries, petrochemical complexes, LNG terminals, power generation plants, mining operations, and large-scale water & wastewater treatment facilities. Countries such as China, India, and Southeast Asian economies are increasing their reliance on high-capacity, energy-efficient turbo compressors to support expanding manufacturing and infrastructure development. Government-backed industrial programs and rising energy demand are likely to further accelerate adoption.

Asia Pacific is not only a major consumer but also emerging as a competitive manufacturing hub for compressor components and engineered systems. Rising environmental regulations, industrial emissions control, and focus on energy-efficient systems are fostering demand for modern centrifugal and axial compressors. Lower production costs, availability of skilled labor, and growing export-oriented ecosystems strengthen the region’s global presence. As industrial capacity scales across sectors including chemicals, power, metals, and water management, the demand for advanced compression technologies continues to surge. The strong upward trajectory of Asia Pacific positions it as the most dynamic and strategically critical market for the turbo compressor market growth.

Competitive Landscape

The global turbo compressor market structure is moderately consolidated, dominated by leading industrial machinery manufacturers such as Siemens Energy, Mitsubishi Heavy Industries, Atlas Copco, MAN Energy Solutions, Kawasaki Heavy Industries, Ingersoll Rand, and Elliott Group. These companies maintain strong control over technology development, large-scale production, and global service networks, enabling reliable support for oil & gas, chemical, LNG, and power generation sectors. Their competitive strength is built on advanced centrifugal and axial compressor designs, high-efficiency performance, and long-term maintenance contracts. Continuous investments in digital monitoring, energy-efficient architectures, magnetic bearings, and low-emission technologies reinforce their global leadership. As industrial modernization accelerates, these players continue shaping product standards and innovation pathways.

Emerging and regional manufacturers, including Hanwha Power Systems, Shanghai Electric, Burckhardt Compression, FS-Elliott, and Sundyne, are rapidly expanding their presence, particularly in Asia Pacific, the Middle East, and Latin America. Their focus on cost-efficient production, localized support, and customized configurations enables them to meet rising demand in water & wastewater treatment, mining, general manufacturing, and mid-scale power applications. Competitive advantages include flexible delivery capabilities, responsiveness to regional project requirements, and increasing participation in infrastructure development programs. As industries prioritize energy efficiency and predictive maintenance, competition is expected to intensify around IoT-enabled systems, lifecycle optimization, and emerging opportunities in hydrogen and renewable-gas compression.

Key Industry Developments

In June 2025, Honeywell announced the US$ 2.16 billion acquisition of Sundyne, strengthening its compressor and pump portfolio and expanding its presence in the energy, petrochemical, and aftermarket service segments.

In March 2025, Kawasaki Heavy Industries began constructing a hydrogen compressor demonstration facility to test its KM Comp-H? centrifugal hydrogen compressor, the first of its kind for hydrogen liquefaction plants, with completion expected by November 2025, followed by a year of operational trials.

In March 2025, MAN Energy Solutions secured a multi-year maintenance and service contract with EDF PEI running through 2031, covering engines, turbo-compressors, and auxiliary systems, reinforcing its long-term service capabilities across island power plants.

Companies Covered in Turbo Compressor Market

• Atlas Copco

• Siemens / Siemens Energy

• Ingersoll Rand

• Mitsubishi Heavy Industries (MHI)

• Kobe Steel (Kobelco)

• Gardner Denver

• BOGE Kompressors

• Howden Group

• GE (GE Oil & Gas / GE Vernova / Baker Hughes)

• MAN Energy Solutions

• Elliott Group

• Kawasaki Heavy Industries

• Hitachi Ltd.

• IHI Corporation

• Sundyne

Frequently Asked Questions

The global turbo compressor market is projected to reach US$ 22.3 billion in 2026.

Key market drivers include expanding industrialization, energy efficiency priorities, high-capacity gas compression needs, and growing infrastructure projects in emerging and developed economies.

The market is poised to witness a CAGR of 5.8% from 2026 to 2033.

Major opportunities are opening up in water & wastewater, mining, renewable energy, hydrogen, and low-carbon gas compression, as well as IoT-enabled and energy-efficient compressor solutions.

Prominent companies include Atlas Copco, Siemens Energy, Ingersoll Rand, Mitsubishi Heavy Industries, and Kawasaki Heavy Industries, among others.