- Automation & Robotics

- Turbidimeter Market

Turbidimeter Market Size, Share and Growth Forecast, 2026 – 2033

Turbidimeter Market by Optical Configuration (Single-Beam, Multi-Channel), Data Communication (Analog, Others), Product Type (In-line/Online, Others), Application (Water & Wastewater, Others), and Regional Analysis 2026 – 2033.

Turbidimeter Market Size and Trends Analysis

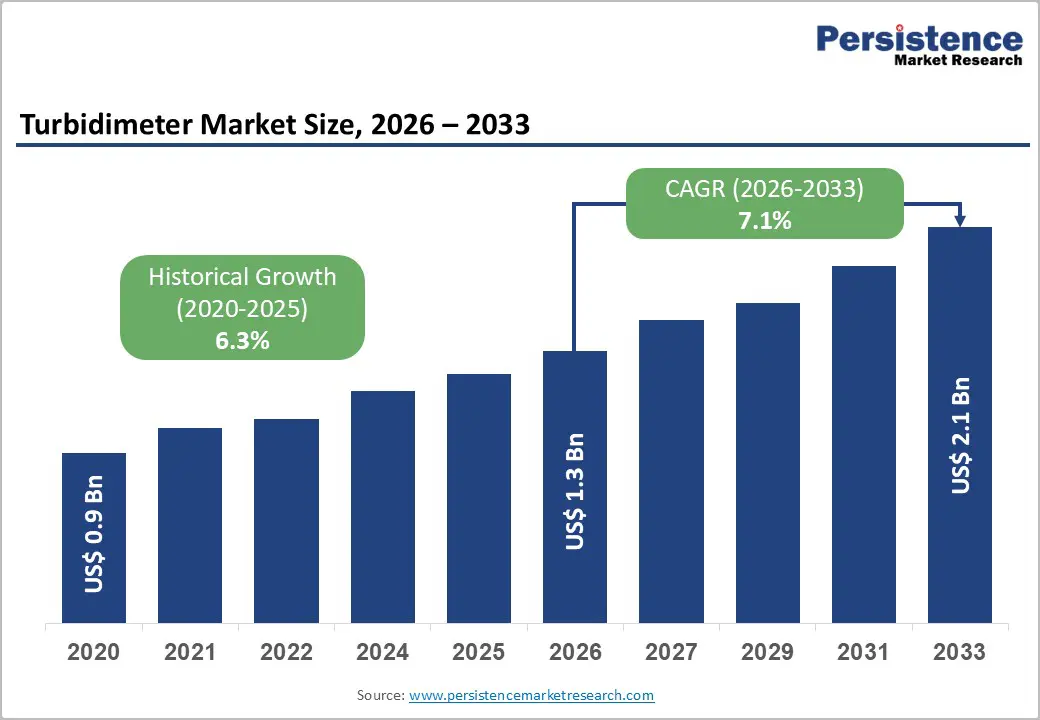

The global turbidimeter market size is likely to be valued at US$1.3 billion in 2026 and is expected to reach US$2.1 billion by 2033, growing at a CAGR of 7.1% during the forecast period from 2026 to 2033, driven by stringent water quality regulations and rising industrial demand for precise turbidity monitoring.

The expansion of the market is further driven by increasingly stringent global water quality regulations, which require strict turbidity monitoring in both municipal and industrial wastewater treatment.

The shift toward Industry 4.0 is accelerating the adoption of smart, IoT-enabled process turbidimeters for real-time water analysis. Growing investments in water reclamation initiatives and Zero Liquid Discharge (ZLD) systems in water-scarce regions are increasing demand for high-precision optical measurement instruments.

Key Industry Highlights:

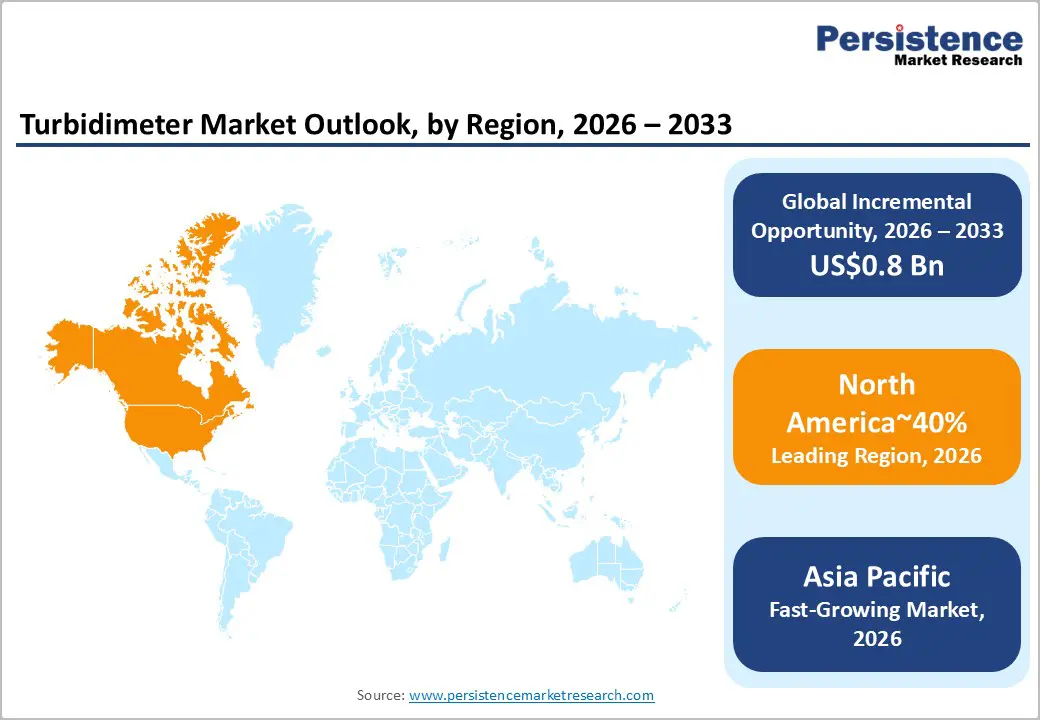

- Leading Region: North America is expected to remain the leading region in the turbidimeter market, accounting for 40%, supported by mature water infrastructure, regulatory oversight, and widespread adoption of digital and IoT-enabled monitoring platforms.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing region, driven by accelerated urbanization, industrial capacity expansion, and policy mandates for online water quality monitoring.

- Leading Optical Configuration: Single-Beam configuration is anticipated to remain dominant with roughly 62% share, favored for regulatory monitoring, linear response, and low maintenance requirements.

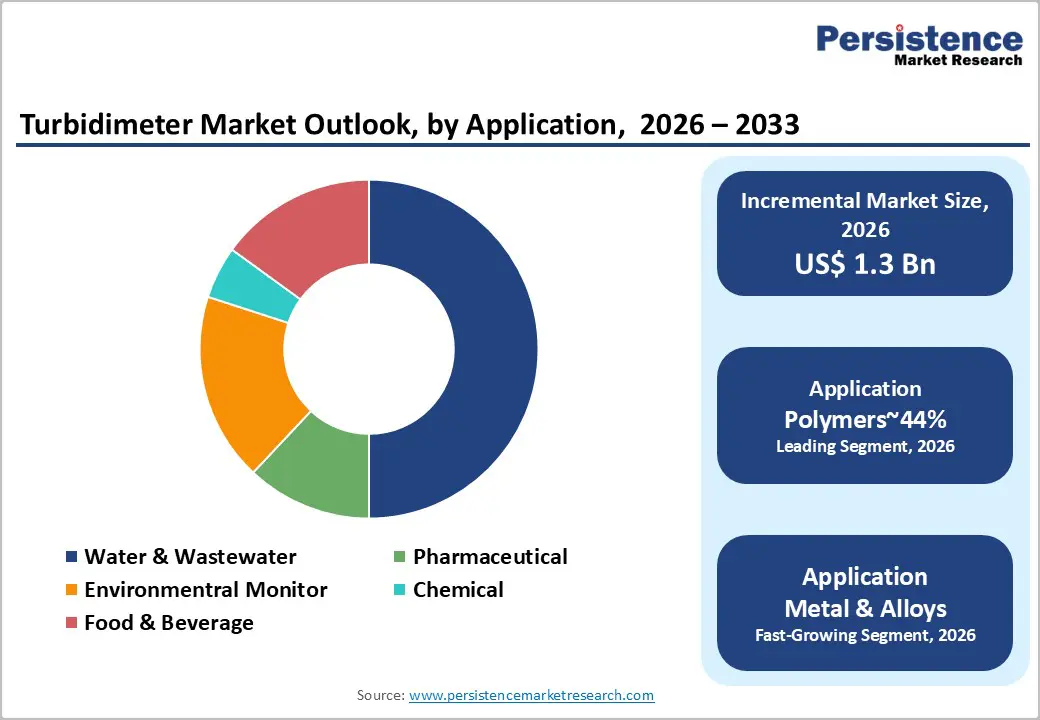

- Leading Application: Water and wastewater treatment is expected to lead with 35% share, anchored by regulatory compliance, dense sensor deployment, and long service-life requirements.

| Key Insights | Details |

|---|---|

| Turbidimeter Market Size (2026E) | US$1.3 Bn |

| Market Value Forecast (2033F) | US$2.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulatory-Driven Demand for Continuous Water Quality Monitoring

The turbidimeter market is driven by regulatory enforcement, infrastructure modernization, and increasing public awareness of water quality. Turbidity is a critical parameter in wastewater treatment, essential for optimizing processes such as settling, filtration, and tertiary polishing. Utilities and industrial operators are increasingly adopting online and in-line turbidimeters for real-time optimization, especially for automated dosing of coagulants and flocculants.

This improves treatment efficiency, reduces chemical use, energy consumption, and unplanned downtime, while protecting downstream assets such as membranes and UV disinfection systems from fouling. Growing industrial water reuse, particularly in sectors like textiles, paper, and chemicals, further emphasizes the need for turbidity monitoring.

Regulatory standards across various jurisdictions require stringent turbidity control for both drinking water and effluent discharge, making continuous monitoring a legal necessity. Infrastructure upgrades and national water protection programs prioritize digital, sensor-driven solutions. Public and corporate focus on health and environmental risks reinforces turbidity's role in risk management, as high turbidity can undermine disinfection and erode trust in water safety.

The launch of cloud-managed turbidity and pH meters in October 2025 exemplifies the trend toward digital solutions. These platforms enable remote data access, reducing manual intervention and facilitating real-time analytics, pushing turbidity measurement to the forefront of modern water management.

Measurement Accuracy Constraints in Complex and Harsh Process Media

The turbidimeter market faces significant challenges in industrial settings where process fluids have high color, entrained air, or unstable flow conditions. Single-beam optical designs are prone to signal distortion when pigments, dyes, or dissolved organics scatter or absorb light, leading to inaccurate turbidity readings. Microbubbles from agitation, pumping, or chemical reactions further introduce transient noise, reducing measurement stability.

Advanced multi-channel instruments can mitigate these issues but come with higher costs, slowing adoption in non-regulated industries like food processing, chemicals, and mining, where reliable turbidity measurements are crucial for process control.

Durability issues also limit automation in abrasive and high-solids environments, such as mineral processing, pulp and paper, and cement. Optical windows in these applications are vulnerable to erosion, scaling, and fouling, which degrade sensor performance and increase maintenance needs. Frequent cleaning, window replacements, and recalibrations disrupt production and increase lifecycle costs, undermining confidence in continuous turbidity monitoring.

Many operators continue to rely on intermittent grab sampling or lab analysis. Without more robust sensor housings, window materials, and self-cleaning mechanisms, the adoption of automated turbidity measurement in complex industrial fluids will remain limited.

Technological Convergence with IoT and AI for Smart Water Monitoring

The convergence of Internet of Things (IoT) and Artificial Intelligence (AI) is transforming turbidimeters from standalone devices into integrated nodes within connected water management ecosystems. IoT-enabled turbidimeters transmit continuous, time-stamped data to centralized platforms, providing remote visibility over assets such as treatment plants, pumping stations, and river basins.

AI analytics convert raw turbidity data into actionable insights, enabling operators to anticipate process deviations, optimize workflows, and respond quickly to contamination events. This shift is critical as utilities seek to maintain high service reliability with limited manpower, making connected turbidimetry essential for autonomous operations.

Beyond instrumentation, AI-driven analytics support predictive maintenance by identifying sensor degradation and fouling patterns before they impact performance. Edge computing allows real-time alerts during turbidity spikes, improving response times in drinking water and effluent discharge contexts. Integration with digital twins enhances resilience planning by simulating runoff events, load shocks, and process changes.

Increasingly, vendors offer IoT turbidimeters as part of data-as-a-service models, bundling hardware with cloud dashboards, automated reporting, and compliance documentation. Sensor fusion enhances this by correlating turbidity with parameters such as pH and conductivity to provide a comprehensive picture of water quality. In March 2025, Xylem partnered with Horiba to integrate turbidity data from YSI EXO platforms with Horiba systems, enhancing data compatibility and supporting advanced ecosystem solutions in research and field applications. This convergence expands the market from devices to intelligent platforms, driving long-term revenue through software and services.

Category–wise Analysis

Optical Configuration Insights

The single-beam segment is expected to lead the turbidimeter market with an estimated 62% share in 2026, as it remains the standard configuration for high-volume regulatory monitoring across municipal water utilities, food processing plants, and general industrial facilities.

Operators continue to prioritize single-beam platforms for routine influent and effluent measurement because they offer low acquisition cost, simple installation, and predictable maintenance cycles, which are critical for large installed bases.

Mature portfolios from Hach, ABB, Yokogawa, and Sigrist-Photometer support established ISO 7027 and EPA 180.1 measurement workflows, reinforcing standardization across brownfield plants. Procurement strategies favor technologies with widely available spares, established service ecosystems, and seamless integration with legacy SCADA and DCS architectures. In low-to-moderate turbidity applications, single-beam sensors provide sufficient linearity and response stability for compliance-driven monitoring requirements at scale.

Multi-channel turbidimeter configurations are expected to represent the fastest growing technology segment as monitoring requirements evolve from basic compliance toward real-time process control in optically challenging fluids. Ratiometric dual-beam and four-beam designs mitigate signal drift caused by LED aging, window fouling, color interference, and entrained air through multi-angle detection and embedded signal processing.

Adoption is being reinforced by industrial automation programs, ZLD-oriented wastewater treatment upgrades, and advanced bioprocessing environments where measurement stability under high-solids conditions is operationally critical. Hybrid optical architectures that combine infrared and white-light sources support cross-standard deployment, reducing recalibration frequency and operational disruption.

As plants intensify digitalization of treatment and production workflows, multi-channel platforms are increasingly positioned as the reference architecture for interference-tolerant, closed-loop turbidity measurement.

Application Insights

The water and wastewater segment is expected to remain the leading application segment in the turbidimeter market with an estimated share of about 35% in 2026, driven by its role as the regulatory backbone of turbidity measurement adoption. Municipal treatment systems rely on continuous turbidity monitoring as a primary proxy for filtration performance and pathogen risk management, making instrumentation spending largely non-discretionary.

Large installed treatment infrastructures require dense sensor deployment across intake, clarification, filtration, and discharge points, which structurally anchors demand. The transition toward continuous monitoring architectures, smart water platforms, and automated cleaning mechanisms such as wipers and ultrasonic anti-fouling, has reinforced replacement demand and technology upgrades within this segment.

Compliance-driven procurement, interoperability with utility SCADA systems, and long service life expectations further entrench water and wastewater as the volume leader across mature and emerging treatment networks.

Pharmaceutical manufacturing is anticipated to be the fastest-growing application area for turbidimeters as production models shift toward continuous processing and advanced biologics. Turbidity has evolved from a waste monitoring parameter into a core in-line process analytical signal for biomass tracking, protein aggregation detection, and ultrapure water assurance.

Growth is supported by rising deployment of single-use systems, in-line PAT instrumentation, and digitally integrated quality frameworks that require high sensitivity and audit-ready data capture. Replacement cycles are accelerating as legacy analog instruments are displaced by fully digital, clean-in-place compatible platforms designed for sterile environments. The expansion of regional biologics and vaccine manufacturing capacity, combined with tighter data integrity and validation expectations, is structurally increasing sensor density per facility and elevating the strategic importance of high specification turbidimetry in pharmaceutical process control.

Regional Insights

North America Turbidimeter Market Trends

North America is expected to remain the leading region in the turbidimeter market, accounting for 40% of the global market share in 2026, supported by a mature water treatment infrastructure, stringent regulatory oversight, and early adoption of digital and IoT-enabled monitoring platforms.

The region is likely to maintain strong demand as municipal utilities and industrial operators continue to replace legacy turbidity meters with connected, high-accuracy online systems. Compliance-driven monitoring across drinking water, wastewater, and industrial process water is anticipated to anchor baseline demand, while infrastructure renewal programs are expected to accelerate upgrades of stationary and in-line turbidimeters.

Technology suppliers are increasingly focusing on edge-enabled sensors, remote calibration support, and secure data integration with SCADA and digital water platforms to improve compliance reporting, asset reliability, and operational efficiency.

The U.S. is expected to anchor regional performance due to the scale of its municipal water infrastructure, regulatory enforcement across treatment plants, and widespread adoption of online turbidimeters in pharmaceuticals, food and beverage, and industrial water reuse. Canada is expected to maintain a steady uptake, driven by municipal modernization programs and environmental monitoring requirements for surface water and drinking water systems.

Regional demand is likely to be shaped by established brands expanding advanced product portfolios, including Hach with its TU5 and 1720E low-level online turbidimeters, Thermo Fisher Scientific with Orion process turbidity systems for regulated environments, Xylem’s YSI and WTW online turbidity platforms for municipal and industrial applications, and Hanna Instruments with portable and benchtop turbidity meters for field and laboratory compliance workflows.

Europe Turbidimeter Market Trends

Europe will remain a key region for the turbidimeter market, driven by a regulatory-first environment, strong institutionalization of ISO-compliant water quality monitoring, and accelerating digitalization of utility operations. Demand will be sustained by stricter enforcement under pan-European water quality frameworks, increased investments in wastewater reuse, and the rollout of digitally enabled monitoring systems aligned with "smart water" and digital twin initiatives across utilities and industrial sectors. Adoption is expected to focus on high-precision nephelometric and in-situ optical probes that enable low-turbidity detection, reagent-free operation, and long service intervals.

The market will also benefit from the transition to modular, serviceable sensor architectures that reduce lifecycle costs and support circular economy goals, as well as growing demand for field-integrated, network-ready instruments compatible with industrial communication protocols in automated plants.

Germany is anticipated to lead demand due to its high concentration of industrial wastewater generators, advanced municipal treatment infrastructure, and extensive use of digital process instrumentation across chemicals, food and beverage, and manufacturing sectors. France will also be a key demand center, driven by large utility operators standardizing the procurement of compliant turbidity-monitoring systems.

European suppliers like Endress+Hauser, Sigrist-Photometer, ABB, Tintometer, and Hach Lange will shape market competition with ISO-aligned product portfolios, including continuous process monitoring sensors, laser-based instruments, and online turbidimeters for municipal and industrial applications.

Asia Pacific Turbidimeter Market Trends

The Asia-Pacific region is expected to remain the fastest-growing region for turbidimeters, supported by accelerated urbanization, sustained industrial capacity additions, and a policy shift toward digitally enforced environmental compliance. Growth is being shaped by large-scale investments in municipal water and wastewater infrastructure, stricter discharge standards across manufacturing clusters, and the rapid institutionalization of continuous online monitoring at treatment plants and industrial outfalls.

Utilities and industrial operators are increasingly standardizing on networked, low-maintenance optical turbidimeters that integrate with plant automation systems and centralized compliance dashboards. Adoption is also being reinforced by water reuse mandates in water-stressed economies, driving demand for higher-resolution turbidity control in closed-loop recycling systems and advanced tertiary treatment stages.

India is anticipated to represent the primary growth engine, supported by nationwide drinking water programs, expanding wastewater treatment capacity, and regulatory requirements for real-time digital reporting that are accelerating the replacement of manual and laboratory-based turbidity testing with online sensors.

China is expected to anchor regional volumes due to the scale of its industrial wastewater treatment footprint, regulatory enforcement of continuous effluent monitoring, and broad deployment of in-line optical probes across industrial parks and municipal utilities.

Competitive dynamics in the region are driven by global and regional suppliers expanding localized product portfolios. Hach and Endress+Hauser address municipal and industrial compliance with online process turbidimeters and in-line optical probes integrated into plant control systems. Xylem (YSI) and Thermo Fisher Scientific cover continuous monitoring and regulated laboratory/process testing across environmental and wastewater workflows.

Competitive Landscape

The global turbidimeter market is moderately consolidated, led by influential players such as Hach (Danaher), Thermo Fisher Scientific, Endress+Hauser, and Xylem, which shape product standards and adoption through broad portfolios, regulatory-aligned instrumentation, and global distribution reach. These companies matter because their installed base, compliance-oriented technologies, and integrated digital platforms position them as preferred partners for utilities and industrial users. Competition remains active, with fragmentation more visible in portable and low-cost segments, where regional manufacturers and niche entrants compete on affordability and application-specific designs.

Competitive positioning is increasingly defined by software capabilities and sensor-to-cloud ecosystems, as leaders move beyond hardware toward connected monitoring, analytics, and service-led models. Industry behavior reflects sustained emphasis on technology integration, compliance enablement, and platform expansion, while strategic partnerships and acquisitions continue to reinforce digital water management capabilities. Competitive pressure is expected to intensify as connectivity, automation, and service differentiation reshape procurement priorities.

Key Industry Developments:

- In September 2025, HORIBA launched the LAQUA-TB220 portable turbidity meter. This new addition to the LAQUA series improves on-the-go measurement with enhanced user-friendliness and precision, creating opportunities for wider adoption in environmental testing and regulatory compliance.

- In September 2025, Industrial Test Systems (Sensafe) soft-launched the eXact Turbo Turbidity Meter. This rugged, compact device with app synchronization enhances field usability and data logging, creating opportunities for quick adoption in municipal and environmental monitoring.

Companies Covered in Turbidimeter Market

- Hach (Danaher Corporation)

- Thermo Fisher Scientific

- Xylem Inc.

- Endress Hauser

- Mettler Toledo

- ABB Ltd.

- Emerson Electric Co. (Rosemount)

- Yokogawa Electric Corporation

- Horiba, Ltd.

- Lovibond (The Tintometer Group)

- DKK-TOA Corporation

- HF Scientific

- Hanna Instruments

- Palintest

- Swan Analytical Instruments

- KROHNE Group

- Optek-Danulat

Frequently Asked Questions

The global turbidimeter market is valued at US$1.3 billion in 2026, driven by regulatory compliance, industrial water monitoring, and the adoption of smart IoT-enabled instruments for continuous turbidity measurement in municipal and industrial applications.

Demand is increasing due to stringent water quality regulations, expansion of wastewater treatment and water reuse projects, digitalization with IoT/AI platforms, and the need for real-time process optimization to protect downstream assets and ensure operational efficiency.

The turbidimeter market is projected to grow at a CAGR of 7.1% between 2026 and 2033, supported by rising urbanization, industrial expansion, ZLD system adoption, and the transition toward smart, connected monitoring across municipal and industrial water networks.

The Asia Pacific region is the fastest-growing market, driven by accelerated urbanization, industrial water capacity expansion, policy mandates for online monitoring, and growing investments in digital water management platforms.

Key players include Hach (Danaher), Thermo Fisher Scientific, Xylem, Endress+Hauser, Mettler Toledo, ABB, Emerson Electric (Rosemount), Yokogawa, Horiba, Lovibond (Tintometer Group), DKK-TOA, HF Scientific, Hanna Instruments, Palintest, Swan Analytical Instruments, and KROHNE Group.