- Food Ingredients & Additives

- Transglutaminase Market

Transglutaminase Market Size, Share, and Growth Forecast, 2025 - 2032

Transglutaminase Market By Source (Microbial, Animal-derived, Others), Form (Powder, Liquid / Stabilized, Others), Activity Grade, Application, and Regional Analysis for 2025 - 2032

Transglutaminase Market Size and Trends Analysis

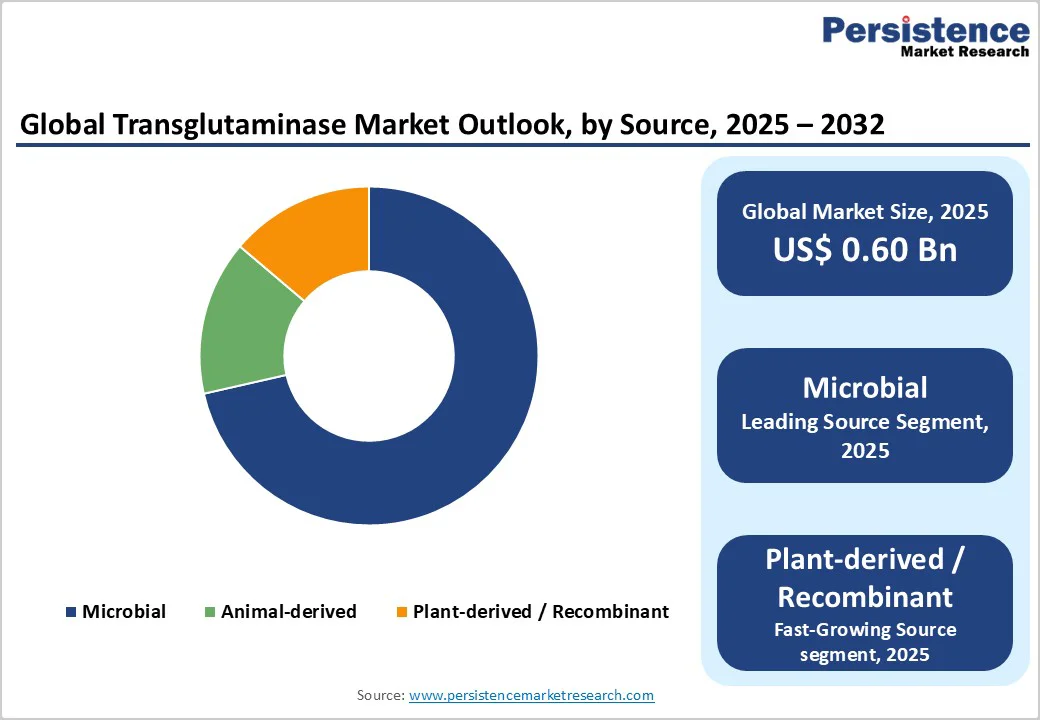

The global transglutaminase market size is likely to be valued at US$0.60 Billion in 2025 and is expected to reach US$1.00 Billion by 2032, growing at a CAGR of approximately 7.6% during the forecast period from 2025 to 2032, driven by the rising use of transglutaminase (TG) in meat restructuring, dairy yield optimization, and the formulation of plant-based protein products.

Regulatory acceptance in major food markets and advances in enzyme formulations are widening its industrial use. Key challenges include public perception issues and labeling scrutiny in some regions. The strongest opportunity lies in specialized TG blends tailored for plant proteins and clean-label requirements.

Key Industry Highlights

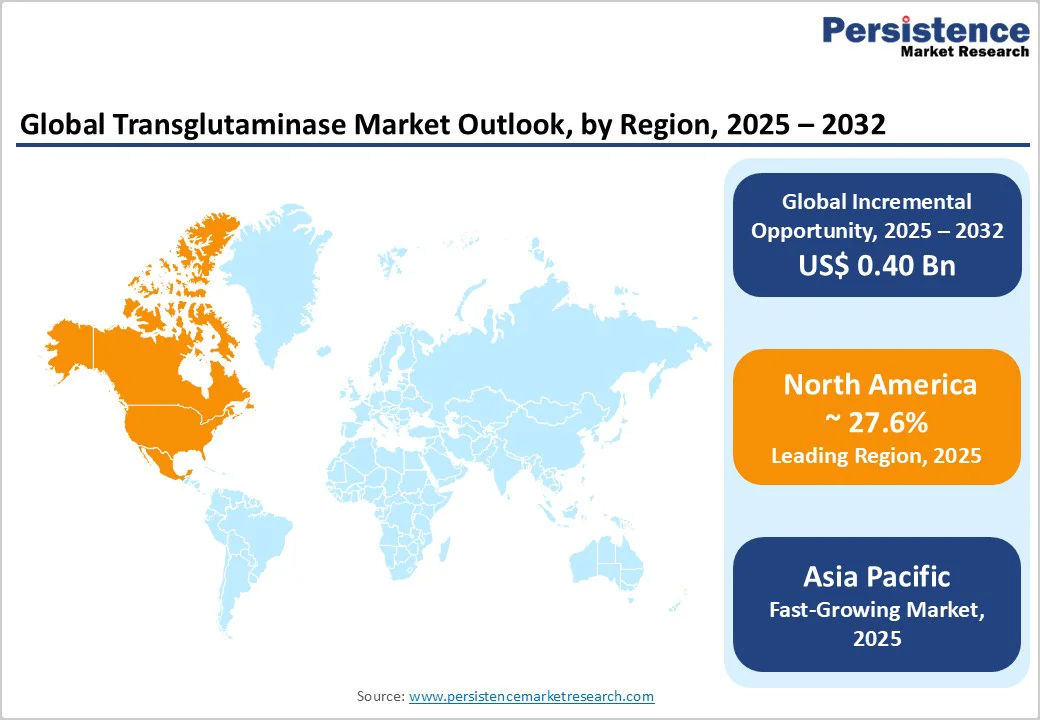

- Leading Region: North America, accounting for approximately 27.6% of global transglutaminase market revenue, driven by a large processed-protein sector, established regulatory clarity, and strong adoption across meat, dairy, bakery, and plant-based products.

- Fastest-growing Region: Asia Pacific, supported by rapid growth in processed meat and seafood industries, rising protein consumption, competitive fermentation manufacturing, and rapidly rising demand from plant-based product developers.

- Investment Plans: Manufacturers are increasing fermentation capacity by an estimated 10-15% in key producing countries, upgrading continuous-processing lines to support liquid TG adoption, and establishing application labs for plant-protein and dairy innovation across North America, Europe, and Asia.

- Dominant Source: Microbial Transglutaminase (MTGase), holding the largest share at roughly 72.5% of the total market share, due to its cost efficiency, scalability, and broad applicability across meat, seafood, dairy, and bakery systems.

- Leading Formulation: Powder TG, representing an estimated 64.5% of total formulation demand, supported by long shelf life, global distribution readiness, and suitability for dry-mix and batch-processing operations.

| Key Insights | Details |

|---|---|

| Transglutaminase Market Size (2025E) | US$0.60 Bn |

| Market Value Forecast (2032F) | US$1.00 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Processed-Protein Consumption and Meat-Restructuring Demand

Manufacturers increasingly rely on TG to improve product yield, texture uniformity, and water-holding capacity in processed meat and seafood systems. Binding meat trimmings into standardized cuts reduces waste and improves production efficiency. Industrial meat processors and foodservice suppliers view TG as essential for producing consistent portion sizes that meet retail and distribution requirements.

With processed meat output expanding in Asia, Latin America, and several mature markets, demand for TG remains structurally strong. Industry-level analyses routinely highlight meat processing as the single largest end-use category, accounting for a substantial portion of global TG consumption.

Growing Adoption in Plant-Based and Alternative-Protein Formulations

The expansion of plant-based meat and dairy alternatives has significantly increased the need for functional proteins that replicate meat-like texture. TG enables cross-linking between plant proteins such as soy, pea, and wheat gluten, creating improved bite, cohesion, and juiciness.

As plant-based brands scale production and traditional protein companies diversify into alternative lines, formulation teams increasingly integrate TG to achieve consistent structure in high-moisture extrusion and formed products. Suppliers have developed TG blends specifically optimized for plant matrices, and adoption rates in this segment consistently outpace those in traditional applications, making alternative proteins one of the fastest-growing demand drivers.

Regulatory Clarity and Advances in Enzyme Innovation

Clear regulatory pathways in major markets have reduced uncertainty around TG usage in foods. Regulatory reviews in North America, Europe, and Asia have recognized TG preparations as acceptable within specified manufacturing conditions. This clarity encourages processors to standardize TG use across dairy, bakery, meat, and plant-based lines.

Technological advances, including activity-graded preparations, improved stabilization, and tailored blends for specific substrates, further expand usability. Liquid and powder variants optimized for shelf life, handling ease, and performance in diverse processing environments have created new adoption avenues. Combined regulatory and technological progress continues to lower entry barriers for manufacturers.

Barrier Analysis - Consumer Perception and Labeling Sensitivity

Public perception challenges persist due to the association of TG with the “meat glue” label, which can trigger skepticism about product authenticity. Even though TG is widely recognized as safe, negative publicity can influence retailer policies and consumer acceptance, especially in markets where ingredient transparency is emphasized.

Companies using TG must navigate labeling requirements carefully and may incur additional communication or reformulation costs. These perception-driven risks can slow adoption in certain retail and foodservice channels.

Price Sensitivity and Supply Concentration

TG production depends on fermentation capacity, raw-material inputs, and specialized purification processes, all of which require capital-intensive infrastructure. Limited global production clusters and varying media costs can lead to periodic price fluctuations.

For smaller or cost-sensitive processors, enzyme pricing may pose a barrier unless efficiency gains offset expenses. Concentration among a limited number of producers heightens vulnerability during periods of supply constraint, contributing to price volatility and extended lead times.

Opportunity Analysis - Customized TG Blends for Plant Proteins and Clean-Label Applications

Demand for optimized TG formulations that enhance the functionality of pea, soy, wheat, and emerging plant proteins continues to grow. Manufacturers seeking clean-label credentials increasingly favor enzyme-based solutions over hydrocolloids, creating opportunities for blends containing minimal auxiliary ingredients.

Even moderate shifts in plant-based product portfolios can significantly raise TG consumption due to higher value per unit of functional improvement. Suppliers able to offer substrate-specific blends and validated performance data stand to secure long-term, premium contracts with fast-growing plant-protein brands.

Dairy Yield Enhancement and Lower-Stabilizer Formulations

TG enables improved casein cross-linking in dairy systems, resulting in higher yields in cheese and yogurt production and reduced whey separation. This functional benefit supports manufacturers facing rising ingredient costs and consumer demand for products with fewer stabilizers.

Applications in high-protein yogurt, unripened cheeses, and low-additive dairy formulations represent steady revenue opportunities. Even small yield improvements scale significantly in large dairy operations, making TG-based solutions economically attractive and strategically important.

Category-wise Insights

Source Insights

Microbial TG produced through controlled fermentation remains the leading source in the global market, holding a market share of 72.5%. Its consistent activity across a broad pH range, calcium-independent activation, and adaptability to diverse food matrices make it the preferred option for industrial users.

Most TG utilized in meat restructuring, seafood texturization, dairy protein binding, and bakery volume enhancement is derived from microbial strains. The combination of large-scale fermenter production, stable supply availability, and favorable cost structures reinforces MTGase as the dominant commercial category.

Plant-based and recombinant TG products, although holding a smaller current share, are expanding at a noticeably faster pace. Demand is supported by the global movement toward non-animal inputs, vegan-label compliance, and customized enzyme solutions compatible with plant proteins such as soy and pea.

Recombinant technologies enable precise control over activity levels, substrate specificity, and thermal stability. As food manufacturers shift toward clean-label formulations and alternative-protein innovation accelerates, these emerging TG sources exhibit the highest growth momentum.

Formulation Insights

Powdered TG constitutes the largest share of the formulation market, holding a market share of 64.5%. Long shelf life, straightforward logistics, and compatibility with dry-blend processing systems support its extensive use across meat processing, bakery mixes, cheese production, and functional ingredient blends.

Global supply chains are optimized around dry enzyme formats, enabling efficient warehousing and distribution. Industries that rely on controlled dosing and batch processing continue to prefer powder TG as their primary option.

Liquid TG formulations are experiencing the fastest adoption as processors modernize production lines. These stabilized liquids deliver operational advantages such as reduced airborne particulates, improved worker safety, and seamless integration with automated dispensing equipment.

Their compatibility with continuous mixing, high-moisture systems, and precision dosing technologies positions them as an attractive alternative for advanced processing facilities. As manufacturers invest in automation and high-throughput systems, demand for liquid TG continues to rise at an accelerated rate.

Regional Insights

North America Transglutaminase Market - Regulatory Stability and Protein-Processing Innovation

North America remains one of the world’s most significant TG markets, supported by a large processed-protein sector, extensive foodservice industry, and active adoption of functional food ingredients. The region accounts for an estimated 27.6% of global revenue.

High per-capita consumption of processed meat, cheese, and convenience foods sustains industrial demand. The U.S. leads regional consumption due to its scale of meat, poultry, and dairy operations and the prevalence of large industrial processors.

Regulatory clarity, particularly through established safety assessments and recognized usage guidelines, enables wide adoption of TG in North America. Manufacturers benefit from a predictable regulatory environment that allows TG use across meat, dairy, bakery, and plant-based products under standard manufacturing controls.

The region is also a hub for alternative-protein innovation, with numerous brands formulating plant-based meats, high-protein dairy alternatives, and next-generation protein products.

Product differentiation emphasizes performance consistency, non-GMO assurance, supply reliability, and technical support. Many suppliers maintain application labs offering pilot trials and formulation support. Investment activity in the region includes co-development partnerships between enzyme makers and food brands, pilot-scale innovation centers, and upgrading of continuous-processing infrastructure.

Opportunities include expanding plant-based production capacity, enhancing dairy yield through TG-enabled casein cross-linking, and modernizing meat processing with liquid TG systems designed for automated dosing. The combination of regulatory certainty, manufacturing sophistication, and consumer demand for high-quality protein products positions North America as a long-term anchor market for TG.

Europe Transglutaminase Market - Advanced Applications Driven by Clean-Label Standards

Europe represents a mature and technically sophisticated market for food enzymes, including TG. Demand is supported by strong dairy and bakery industries, high consumer expectations for product quality, and a well-developed clean-label movement.

The region’s regulatory structure requires safety evaluation and inclusion of enzymes on authorized lists before use in food, creating a higher compliance threshold. Once approved, however, TG benefits from harmonized market access across the European Union.

Key markets such as Germany, France, Spain, and the U.K. exhibit strong adoption across meat, dairy, and bakery applications. European dairy producers rely on TG to improve yield, reduce syneresis, and maintain texture in cheese and yogurt, while bakeries use TG to enhance dough elasticity and gluten-reduced formulations.

Many suppliers offer highly specialized TG blends tailored for specific substrates, including dairy proteins, wheat-based bakery systems, and vegan formulations. Pricing can be more demanding than in other regions due to strict regulatory processes and a preference for premium clean-label solutions.

Investment trends include collaborative R&D programs with food-science institutes, pilot-scale testing partnerships, and expansions in TG blends designed for specific European regulatory and labeling requirements. With an increasing number of plant-based brands originating in Europe, the region is positioned to remain a growth center for TG formulations targeting alternative proteins.

Asia Pacific Transglutaminase Market - Fast-Growth Hub with Strong Production and Processing Expansion

Asia Pacific is the fastest-growing regional market for TG, supported by rapid food-processing expansion, rising protein consumption, and competitive manufacturing capabilities. The region is also a major production hub for TG, with numerous fermentation-based manufacturers supplying both domestic and international markets. China's large-scale production of processed meat, seafood, noodles, and convenience foods positions it as the region’s largest consumer.

Japan has a long history of TG use in surimi and processed seafood, making it one of the most mature TG markets globally. India and Southeast Asia continue to experience rapid urbanization and retail modernization, increasing demand for processed protein foods. Key drivers include cost-efficient manufacturing, expanding meat and seafood processing industries, and accelerating innovation in plant-based products.

As Asian consumers adopt more convenience foods, demand for TG’s yield and textural benefits rises correspondingly. Many regional producers also supply export-oriented TG that meets international certification standards such as non-GMO, halal, and FSSC-compliant manufacturing, enhancing global competitiveness.

Competitive Landscape

The global transglutaminase market is moderately concentrated, with a mix of large international ingredient companies and a long tail of regional manufacturers specializing in fermentation-based enzymes. Multinational suppliers lead the premium TG segment with branded, activity-graded products, while regional players compete strongly on cost and flexibility.

Rapid growth in Asia Pacific has increased global supply capacity, enabling new entrants to compete effectively if they can scale fermentation operations and maintain high manufacturing standards. Market competition emphasizes performance, certifications, and the ability to support technical trials.

Leading companies emphasize technical differentiation through substrate-specific blends, vertical integration of fermentation and formulation, and expansion into plant-based protein and high-value dairy applications. Competitive strategies also include application-lab support, pilot-scale testing, and certification-driven branding. Cost competition remains strong among regional producers supplying commodity-grade TG.

Key Industry Developments

- In May 2024, Food Standards Australia New Zealand (FSANZ) approved the use of a genetically-modified Bacillus licheniformis-derived transglutaminase (encoding gene from Streptomyces mobaraensis) as a processing aid in bakery, meat, fish, cheese, fermented dairy, and analog products, under Good Manufacturing Practice (GMP) limits.

- In March 2025, Ajinomoto Co., Inc. introduced an upgraded microbial transglutaminase line optimized for high-moisture meat analog processing, aiming to support global expansion in plant-based protein applications.

Companies Covered in Transglutaminase Market

- Ajinomoto Co., Inc.

- Nagase Group

- AB Enzymes

- Enzyme Development Corporation

- innoWHEYte

- DSM

- Novozymes

- Amano Enzyme

- Jiangsu Yiming Biological

- Yiming Biotechnology

- Micro-Tech Foods Ingredients

- Kinry Food Ingredients

- Fufeng Group

- Pangbo Biological

- Yiduoli Biotechnology

- Hunan Fengan Biotech

- Henan Boyang Biological

- Taixing Dongsheng Bio-Tech

- Meito Sangyo

- Codexis

Frequently Asked Questions

The global transglutaminase market size in 2025 is estimated at US$0.60 Billion.

By 2032, the transglutaminase market is projected to reach US$1.00 Billion.

Key trends include rising adoption of microbial transglutaminase in processed meat and dairy products, increasing demand for clean-label texture modification, and rapid growth of plant-based food applications.

Microbial transglutaminase (MTGase) leads the market due to its scalability and versatility across meat, seafood, dairy, and bakery applications. Powder formulations dominate thanks to their longer shelf life and ease of handling.

The transglutaminase market is expected to grow at a CAGR of 7.6% between 2025 and 2032.

Major companies include Ajinomoto Co., Inc., Nagase Group, AB Enzymes, innoWHEYte, and Enzyme Development Corporation.