- Pharmaceuticals

- Topical Pain Relief Market

Topical Pain Relief Market Size, Share, and Growth Forecast, 2026 – 2033

Topical Pain Relief Market by Formulation (Cream, Gel, Spray, Patch, Others), Product Type (Prescription, Over the Counter (OTC)), Distribution Channel (Pharmacy & Drug Stores, Retail Stores, Online Stores), and Regional Analysis for 2026-2033

Topical Pain Relief Market Share and Trends Analysis

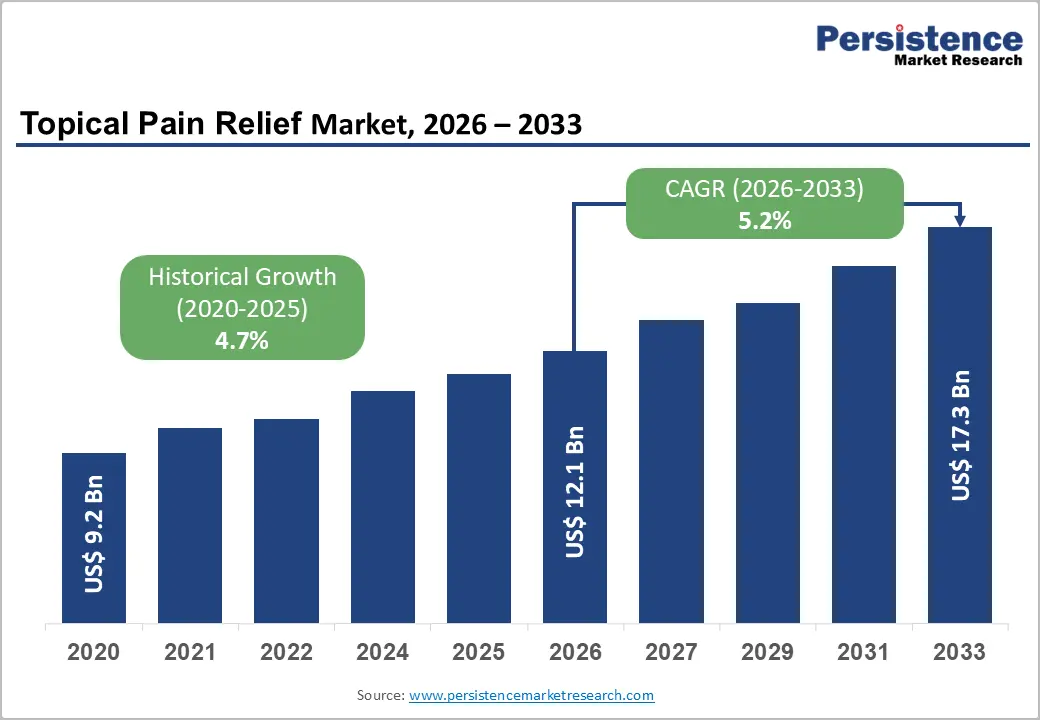

The global topical pain relief market size is likely to be valued at US$ 12.1 billion in 2026, and is projected to reach US$ 17.3 billion by 2033, growing at a CAGR of 5.2% during the forecast period 2026−2033.

Topical pain relief solutions are positioned as a preferred first-line and adjunct therapy across musculoskeletal, neuropathic, and inflammatory pain conditions, reflecting a structural shift toward localized, non-systemic treatment modalities. An expanding aging population with higher incidence of arthritis, joint degeneration, and chronic pain syndromes directly elevates demand for sustained, daily-use pain management options that minimize gastrointestinal, renal, and cardiovascular risks associated with systemic analgesics.

Clinical practice guidelines increasingly favor topical administration routes for mild-to-moderate pain, supported by updated treatment pathways published by national health authorities and orthopedic associations. Treatment adoption benefits from growing patient preference for self-managed, non-invasive care formats that integrate seamlessly into daily routines, reinforcing strong uptake in outpatient and homecare settings. Technological integration in formulation science, including enhanced skin-penetration systems and controlled-release matrices, improves therapeutic effectiveness while preserving safety profiles, strengthening physician confidence and repeat consumer use.

Key Industry Highlights

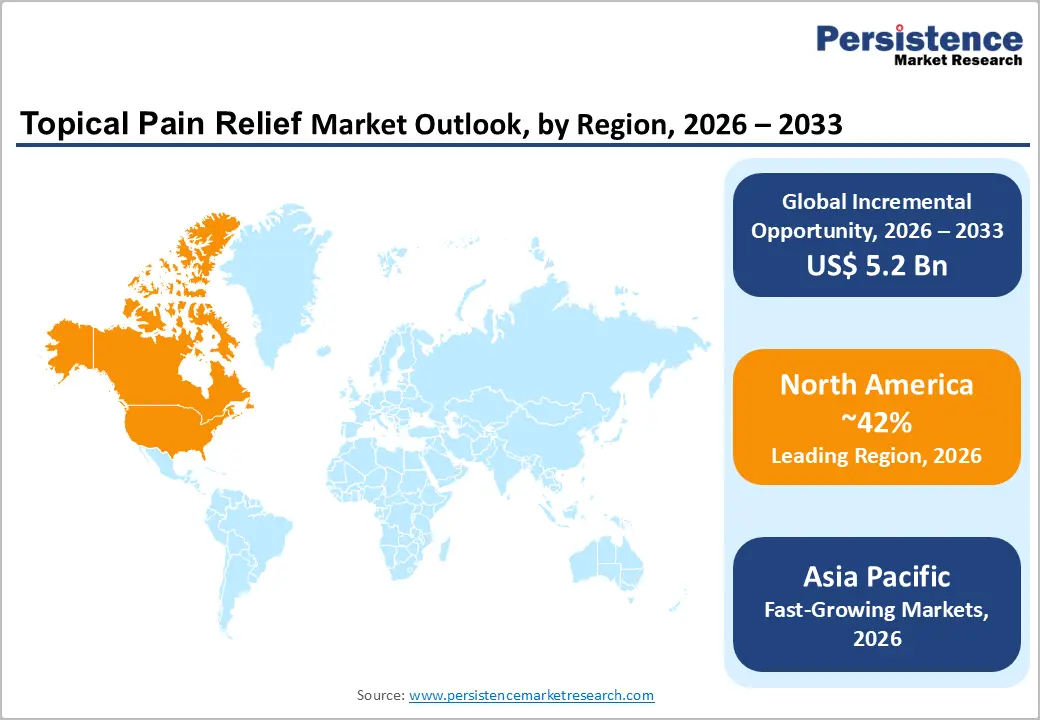

- Dominant Region: North America is set to dominate in 2026 with a 42% market share, supported by premium pricing tolerance and widespread aging workforce-related musculoskeletal pain prevalence.

- Fastest-growing Market: The Asia Pacific market is expected to grow the fastest through 2033, driven by rising self-care adoption and expanding retail and e-commerce access.

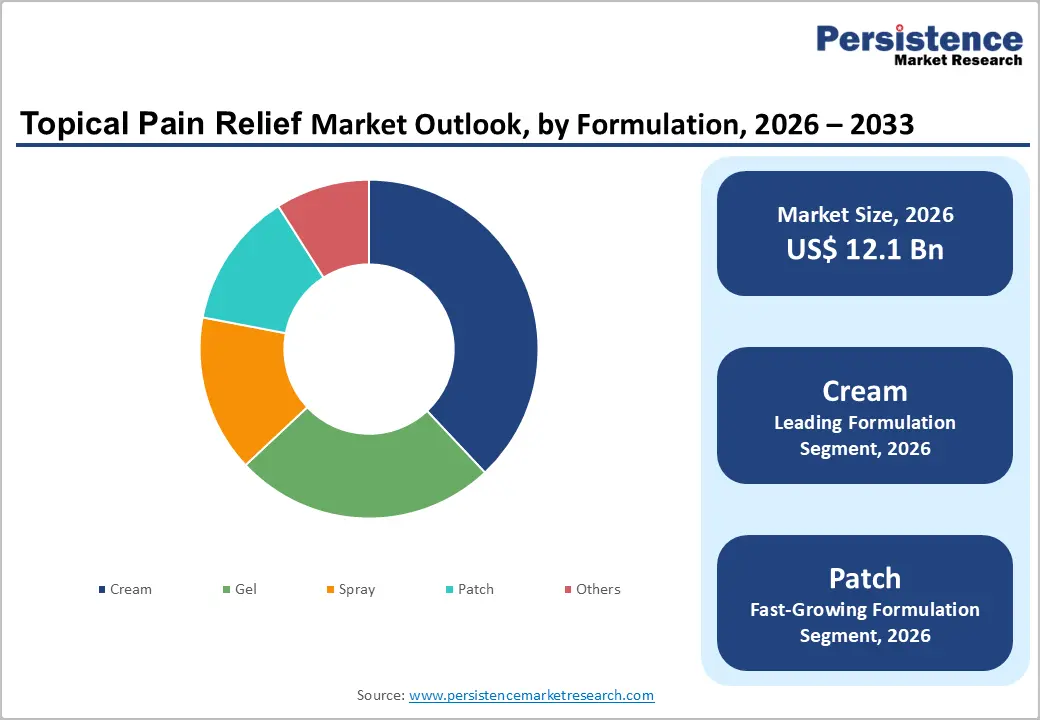

- Leading Formulation: Cream formulations are expected to hold around 38% of the market in 2026, driven by clinical acceptance, versatile active-ingredient delivery, and controlled absorption.

- Fastest-growing Formulation: Patch formulations are expected to be the fastest-growing segment from 2026 to 2033, owing to their extended-release delivery, consistent dosing, and enhanced transdermal efficiency.

- June 2025: N-Labs launched ArcticZen™, a cGMP-certified topical pain relief patch featuring plant-based ingredients such as Wormwood, Ginger, and Safflower for joint and muscle discomfort support.

| Key Insights | Details |

|---|---|

| Topical Pain Relief Market Size (2026E) | US$ 12.1 Bn |

| Market Value Forecast (2033F) | US$ 17.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Prevalence of Chronic Musculoskeletal and Degenerative Conditions

Escalating incidence of chronic musculoskeletal and degenerative disorders reshapes pain management priorities across healthcare systems and consumer segments. Long-lasting joint, muscle, and spine conditions generate recurring discomfort that interferes with mobility, sleep quality, and work continuity, prompting sustained demand for solutions suited for frequent use. Localized pain management formats align with this requirement through site-specific action, predictable relief patterns, and minimal systemic burden, supporting adherence over extended periods. Clinical practice increasingly emphasizes conservative, non-invasive interventions at early and maintenance stages of chronic pain, reinforcing routine recommendations of localized therapies. Patients demonstratea strong inclination toward self-directed care pathways that reduce dependence on prescriptions and clinical visits, supporting steady adoption across pharmacies, digital platforms, and wellness channels. These dynamics convert disease prevalence into consistent consumption rather than episodic purchasing behavior.

Degenerative disorders follow a progressive trajectory, extending treatment duration and intensifying cumulative demand over time. Aging demographics combined with prolonged workforce participation elevate exposure to repetitive strain, posture-related stress, and joint degeneration, sustaining daily pain management needs. One indicator of scale highlights the demand foundation: the World Health Organization estimates that around 1.71 billion people worldwide experience musculoskeletal conditions, underscoring a large and enduring consumer base for localized relief solutions. Professional endorsement from orthopedics and physiotherapy disciplines positions topical approaches as practical options for long-term symptom control, particularly where safety and tolerability influence therapy selection.

Variability in Therapeutic Perception and Clinical Outcomes

Inconsistent patient interpretation of efficacy weakens confidence in topical pain management solutions across consumer and professional channels. Perceived relief often varies by pain etiology, skin permeability, age profile, and prior exposure to systemic analgesics, creating uneven satisfaction levels. Short onset expectations shaped by oral drugs lead some users to undervalue localized formulations that deliver gradual or condition-specific benefits. Clinical feedback from practitioners reflects mixed outcomes in musculoskeletal, neuropathic, and inflammatory indications, complicating standardized treatment pathways. Such divergence in real-world response limits strong therapeutic positioning and constrains premium pricing strategies. Marketing claims face greater scrutiny when experiential outcomes differ across user cohorts, increasing reputational risk and raising the threshold for substantiating evidence in regulatory and institutional procurement settings.

Heterogeneity in clinical performance also challenges formulary inclusion and repeat utilization. Trial designs often demonstrate efficacy under controlled conditions, whereas post-launch performance shows greater dispersion, influenced by adherence patterns, application technique, and concurrent therapies. Physicians encounter difficulty predicting responders, leading to cautious recommendations and a preference for systemic alternatives with more predictable outcomes. Payers and retailers observe fluctuating repurchase rates tied to subjective relief assessment, reducing lifetime value per consumer. Product differentiation becomes complex when similar active ingredients yield dissimilar patient experiences, diluting brand loyalty and intensifying price competition. Investment decisions in innovation and line extensions face higher risk profiles as outcome variability complicates return forecasting.

Improving Healthcare Systems in Developing Economies

The growth of emerging healthcare systems creates a structural opening for wider adoption of non-prescription therapeutic solutions. Public health investments in primary care, retail pharmacy expansion, and digital health access increase product visibility and distribution reach across semi-urban and rural populations. Rising outpatient volumes and limited specialist availability position self-managed pain solutions as a practical first line of care. Cost sensitivity across these regions reinforces demand for affordable, fast-acting options that reduce dependency on clinical interventions. Regulatory frameworks in several developing economies increasingly support over-the-counter classifications, accelerating product approvals and market entry. These dynamics collectively elevate the penetration potential across large populations that were previously underserved by formal pain management pathways.

Shifts in consumer health behavior further strengthen this opportunity. Growing awareness of wellness, mobility preservation, and work-life productivity drives preference for convenient, topical formats that align with daily routines. Aging working populations and a high incidence of musculoskeletal strain from manual labor and sedentary occupations sustain recurring usage patterns. E-commerce platforms and mobile health education campaigns improve consumer familiarity with ingredient safety and usage benefits, strengthening brand trust. Local manufacturing partnerships and private-label strategies support price optimization and supply resilience, enhancing competitiveness in price-sensitive markets.

Category-wise Analysis

Formulation Insights

Cream formulations are anticipated to secure around 38% of the topical pain relief market share in 2026, reflecting widespread clinical acceptance, balanced absorption characteristics, and high patient familiarity. This leadership is reinforced by formulation versatility that supports a wide range of active ingredients across analgesic, anti-inflammatory, and counterirritant categories. Cream-based delivery enables controlled penetration without excessive residue, supporting routine use across diverse age groups.

High compatibility with sensitive skin profiles strengthens repeat usage in long-term pain conditions. From a commercial perspective, creams align well with private-label expansion and physician-endorsed brands, improving shelf visibility and promotional efficiency.

Patch formulations are expected to be the fastest-growing segment during the 2026–2033 forecast period, driven by extended-release capabilities, consistent dosing, and superior adherence support. Growth is supported by increasing demand for low-intervention pain management solutions that fit structured daily schedules. Patches deliver predictable therapeutic levels for extended periods, reducing the need for multiple daily applications and improving compliance. Advancements in transdermal science enable higher drug-loading efficiency while maintaining skin comfort.

Occupational health programs and sports rehabilitation protocols increasingly integrate patch-based therapy for localized pain control.

Product Type Insights

Over-the-counter (OTC) products are poised to dominate in 2026, forecast to command approximately 65% of the topical pain relief market share, powered by high consumer trust, regulatory accessibility, and strong retail penetration. This dominance reflects broad acceptance across age groups seeking convenient solutions for everyday musculoskeletal discomfort. Widespread placement across pharmacies, supermarkets, and online platforms increases purchase frequency and impulse purchases.

Consistent branding and clear usage instructions improve consumer confidence and correct application. Competitive pricing strategies and promotional bundling further accelerate volume sales. Manufacturers benefit from faster product rollout cycles and flexible marketing strategies under OTC frameworks, reinforcing scale advantages and long-term category leadership across developed and emerging economies.

Prescription pain relief products are estimated to register the highest 2026-2033 CAGR, fueled by increasing physician endorsement for targeted topical therapies in moderate pain and post-procedural recovery. Growth is supported by rising preference for localized treatment that limits systemic exposure. Advanced formulations with higher bioavailability improve therapeutic outcomes in controlled clinical settings. Physician familiarity and protocol-based prescribing enhance continuity of use beyond acute care. Hospital pharmacies and specialty clinics strengthen distribution reach for prescription formats.

Distribution Channel Insights

Pharmacies and drug stores are likely to be the leading segment, accounting for 47% of the topical pain relief market value in 2026, driven by clinical credibility, pharmacist counseling, and reimbursement linkage. These outlets maintain strong relationships with healthcare professionals, supporting recommendation-driven purchases and repeat usage. In-store guidance improves correct product selection based on pain type and duration, strengthening therapeutic outcomes. Integration with insurance reimbursement systems and loyalty programs supports consistent foot traffic.

Broad geographic presence across urban and semi-urban areas enhances accessibility for diverse consumer groups. Strategic shelf placement, in-pharmacy promotions, and collaboration with manufacturers reinforce visibility, sustaining channel leadership within structured and semi-structured healthcare ecosystems.

Online stores are expected to be the fastest-growing segment from 2026 to 2033, driven by digitalization, convenience, subscription models, and expanded availability of health content. Growth is reinforced by rising comfort with digital health purchasing and mobile-first consumer behavior. Personalized recommendations, reviews, and usage guidance enhance decision-making confidence. Subscription-based replenishment supports chronic pain management routines and predictable demand. Efficient last-mile delivery and competitive pricing improve value perception.

Integration with teleconsultation platforms strengthens clinical relevance, positioning online channels as scalable, data-driven distribution engines with strong long-term growth potential.

Regional Insights

North America Topical Pain Relief Market Trends

North America is positioned to dominate in 2026, capturing an estimated 42% of the topical pain relief market share, reflecting structurally higher consumption intensity rather than population scale. Demand concentration stems from strong over-the-counter penetration combined with premium pricing tolerance across mass and clinical retail channels. High incidence of chronic musculoskeletal pain linked to aging workforce demographics and sedentary occupational patterns sustains repeat usage frequency. Advanced retail pharmacy networks function as primary care extensions, accelerating sales driven by recommendations without physician visits.

Insurance-linked flexible spending accounts and wellness reimbursement programs indirectly subsidize topical therapy adoption, improving affordability perception. Brand loyalty remains elevated due to long-standing product familiarity and disciplined lifecycle management, enabling manufacturers to defend shelf space while introducing line extensions that lift average selling value.

Commercial leadership in North America is further reinforced by innovation velocity and regulatory efficiency. Shorter approval timelines for non-prescription reformulations enable rapid introduction of higher-efficacy actives and combination products. Strong clinical trial infrastructure supports physician confidence in topical alternatives for localized pain, reducing reliance on systemic therapies. Digital health ecosystems amplify dominance through direct-to-consumer education, data-driven targeting, and subscription-based replenishment models that stabilize demand.

Sports medicine, occupational health programs, and post-surgical recovery pathways increasingly integrate topical solutions as standard adjunct therapy, expanding institutional volumes. Manufacturing scale, marketing spend intensity, and mature logistics ensure consistent availability across urban and secondary markets, sustaining leadership and high entry barriers.

Europe Topical Pain Relief Market Trends

Europe is expected to maintain its position in the market for topical pain relief products through 2033, underpinned by high consumer awareness, established healthcare infrastructure, and strong adoption of non-invasive pain management solutions. Demand is supported by an aging population with elevated prevalence of chronic musculoskeletal disorders, osteoarthritis, and sedentary lifestyle-related pain. Well-developed retail pharmacy chains and e-commerce platforms ensure broad product accessibility, while healthcare professionals frequently recommend localized therapies as adjuncts to systemic treatment.

Preference for low-risk, non-invasive pain management aligns with public health initiatives encouraging self-care and reduced reliance on oral analgesics. Advanced formulation standards, including dermatologically tested creams, gels, and patches, enhance user confidence and reinforce repeat usage. Strategic brand positioning through clinical endorsements and targeted educational campaigns further strengthens consumption across diverse demographic groups.

Growth opportunities are reinforced by rising adoption of innovative delivery formats and personalized therapies. Sustained-release formulations and combination actives address both chronic and episodic pain, improving convenience and adherence. Collaboration between manufacturers and healthcare providers optimizes distribution networks and supports prescription-to-OTC transitions where applicable. High telemedicine adoption and digital health tools facilitate patient engagement, remote guidance, and adherence monitoring, ensuring continuity of care.

Regulatory frameworks promoting standardization and safety foster trust among users and clinicians. Lifestyle trends emphasizing wellness, mobility preservation, and occupational ergonomics further support proactive use of topical therapies.

Asia Pacific Topical Pain Relief Market Trends

Asia Pacific is projected to emerge as the fastest-growing market for topical pain relief solutions during the 2026–2033 forecast period, supported by an expanding base of first-time and repeat users driven by rising disposable income, increasing awareness of self-managed pain solutions, and structural improvements in healthcare access. Urbanization and industrial workforce expansion contribute to elevated incidence of musculoskeletal and occupational strain, creating sustained demand for localized, non-invasive therapies.

Expanding retail pharmacy networks and e-commerce platforms accelerate distribution, bridging gaps between urban and semi-urban populations. High smartphone penetration and digital literacy enable targeted consumer education campaigns, reinforcing correct usage and adherence. Rising preference for convenience-driven, home-based care supports uptake of topical formats over systemic alternatives, while progressive regulatory pathways for over-the-counter approvals accelerate product introduction and market penetration.

Innovation adoption and cost sensitivity further amplify growth potential. Increasing integration of advanced formulations, such as sustained-release patches and combination actives, appeals to both clinical and self-care segments seeking efficacy with minimal intervention. Strategic partnerships with local manufacturers and distributors optimize supply chain efficiency and pricing competitiveness, enabling broader reach in price-sensitive markets. Growing emphasis on preventive health, wellness, and mobility preservation drives recurring consumption among aging populations and active labor segments.

Digital health tools, teleconsultation services, and subscription-based delivery models improve access, continuity, and patient engagement, strengthening long-term adoption. Institutional integration within occupational health programs, rehabilitation centers, and sports clinics expands credibility, while targeted marketing campaigns leverage local cultural preferences and trust patterns to accelerate acceptance, collectively sustaining rapid market growth.

Competitive Landscape

The global topical pain relief market reflects a moderately fragmented structure, with leading multinational pharmaceutical and consumer healthcare companies such as Johnson & Johnson, Pfizer, Advacare Pharma, Teva Pharmaceutical Industries, Bayer Healthcare, and GlaxoSmithKline (GSK) accounting for a substantial combined share. These players leverage extensive research and development capabilities to deliver differentiated formulations, including creams, gels, and patches with enhanced bioavailability and sustained-release properties. Brand trust remains a critical competitive advantage, reinforced through clinical endorsements, physician recommendations, and patient familiarity. Distribution breadth across retail pharmacies, hospitals, and e-commerce platforms ensures consistent availability, enabling high-volume penetration across both urban and semi-urban markets. Pricing strategies, marketing investments, and lifecycle management further consolidate position, while smaller regional and local players compete primarily through niche offerings and cost-sensitive solutions.

Competitive positioning emphasizes formulation innovation, targeted marketing, and integrated supply chain efficiency. Johnson & Johnson and Pfizer Inc. capitalize on global brand recognition and clinical credibility to maintain loyalty, while Advacare Pharma and Teva Pharmaceutical Industries Ltd. focus on therapeutic innovation and specialty products. Bayer Healthcare and GSK leverage established distribution networks and regulatory compliance to optimize reach and trust. Companies prioritize continuous product improvement, including enhanced skin compatibility, reduced irritation, and multi-active combinations, to differentiate offerings in a crowded marketplace. Strategic partnerships with pharmacies and digital health platforms extend access and consumer engagement, reinforcing adoption rates.

Key Industry Developments

- In September 2025, TYLENOL® launched PRECISE™ Pain Relieving Patches with 4% maximum OTC lidocaine for targeted, 12-hour relief on back, knees, and shoulders. Featuring a transparent, flexible, breathable design, the patch moves with body motion/sweat, leaving no sticky residue and ensuring discreet, mess-free application.

- In August 2025, Nuance Medical launched Hurri-Freeze, a new FDA-cleared topical anesthetic spray designed to deliver rapid, safe pain relief with colder performance and significantly lower environmental impact compared with traditional formulations.

- In July 2025, Biofreeze expanded its retail lineup with new formats, including a mess-free Dry Stick and a high-strength lidocaine Ultraflex Patch, to meet evolving consumer demand for convenient, flexible topical pain relief options.

Companies Covered in Topical Pain Relief Market

- Johnson & Johnson

- Pfizer Inc.

- Advacare Pharma

- Teva Pharmaceutical Industries Ltd.

- Bayer Healthcare

- GlaxoSmithKline Plc (GSK)

- Cipla

- Novartis AG

- Sun Pharmaceutical Industries Ltd.

- Sanofi

- Topical Biomedics, Inc.

- Chattem, Inc.

- Hisamitsu Pharmaceutical Co., Inc.

- Exzell Pharma Inc.

- The Himalayan Drug Co.

- Reckitt Benckiser Group Plc.

Frequently Asked Questions

The global topical pain relief market is projected to reach US$ 12.1 billion in 2026.

Increasing prevalence of musculoskeletal disorders, aging populations, rising self-care awareness, and preference for non-invasive, localized pain management solutions are driving the market.

The market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Key market opportunities include expansion across healthcare systems in developing economies, widening self-care adoption, innovative formulation development, digital retail penetration, and growing demand for convenient, non-invasive pain management solutions.

Some of the key market players include Johnson & Johnson, Pfizer Inc., Advacare Pharma, Teva Pharmaceutical Industries Ltd., Bayer Healthcare, and GSK.