- Healthcare Services

- Topical Hemostat Market

Topical Hemostat Market Size, Share, and Growth Forecast, 2026 – 2033

Topical Hemostat Market by Material Type (Collagen-Based Hemostats, Gelatin-Based Hemostats, Oxidized Regenerated Others), Application (General Surgery, Cardiovascular Surgery, Others), End-user (Hospitals, Ambulatory Surgical Centers (ASCs), Others), and Regional Analysis for 2026 - 2033

Topical Hemostat Market Share and Trends Analysis

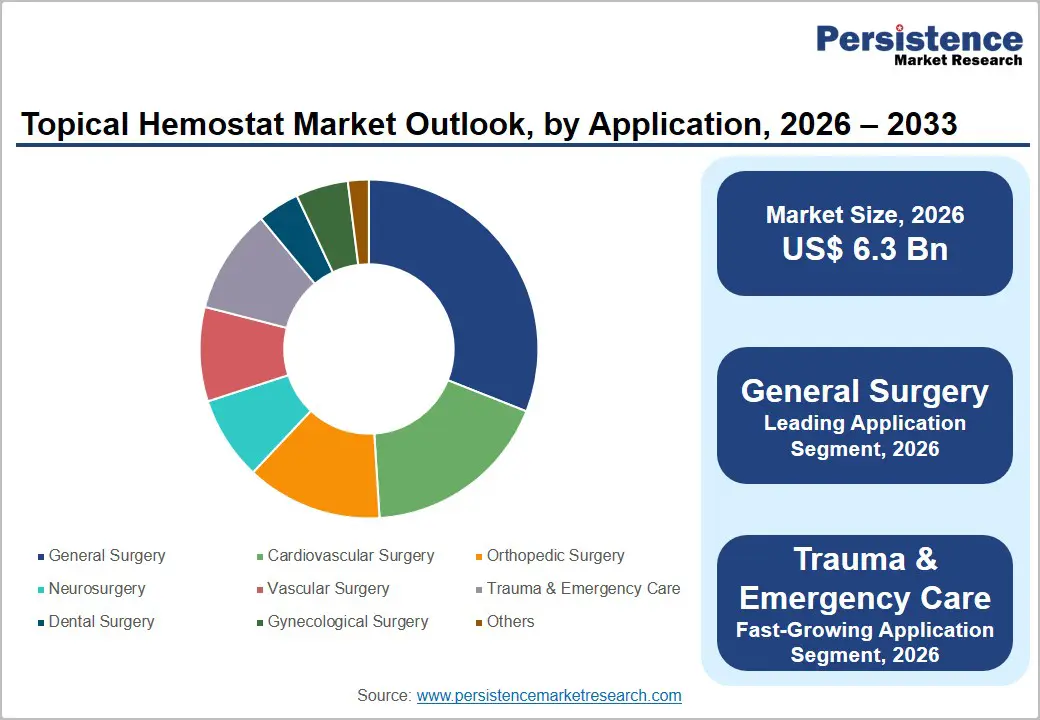

The global topical hemostat market size is likely to be valued at US$6.3 billion in 2026 and is estimated to reach US$12.1 billion by 2033, growing at a CAGR of 9.8% during the forecast period from 2026 to 2033, driven by rising surgical volumes, expanding healthcare infrastructure, and increasing adoption of advanced bleeding management technologies. Growth is supported by aging populations that require higher rates of cardiovascular, orthopedic, and general surgical interventions. Regulatory emphasis on patient safety and blood-loss reduction is accelerating utilization across hospital settings. Continuous innovation in biologically active and synthetic hemostatic materials is improving procedural efficiency and clinical outcomes.

Key Industry Highlights:

- Leading Material Type: Collagen-based hemostats are set to hold around 29% market share in 2026, driven by broad utilization across surgical procedures.

- Fastest-growing Material Type: Cyanoacrylate-based hemostats are projected as the fastest-growing segment, driven by increasing adoption in minimally invasive interventions.

- Leading Application: General surgery is estimated to hold roughly a 31% market share in 2026, driven by high procedural volumes.

- Fastest-Growing Application: Trauma & emergency care is forecast to record the fastest growth, driven by increasing emphasis on rapid hemorrhage management.

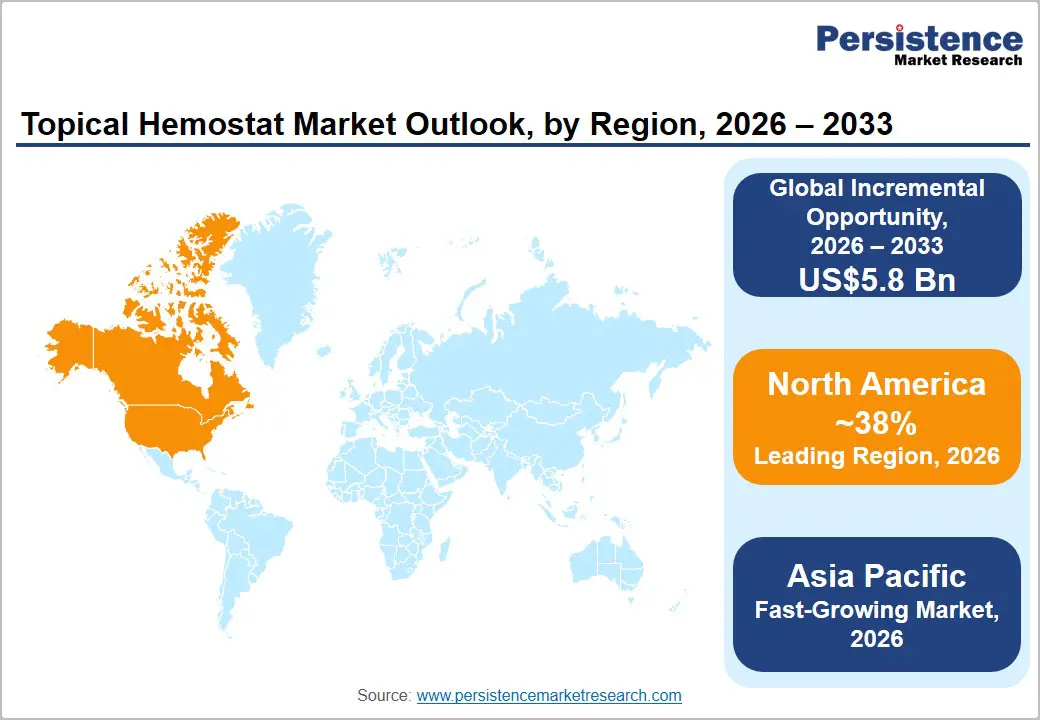

- Regional Leadership: North America is projected to capture roughly 38% of market share by 2026, driven by advanced healthcare infrastructure.

- Competitive Environment: The market reflects a moderately fragmented structure, with companies including Johnson & Johnson, Baxter International, and B. Braun leveraging innovation and clinical expertise.

- Innovation Trends: The development of synthetic hemostatic materials, bioengineered formulations, and procedure-specific bleeding-control technologies is shaping future investment direction.

DRO Analysis

Driver - Expansion of Advanced Healthcare Infrastructure

Investment in healthcare infrastructure is increasing access to sophisticated surgical care across hospitals, ambulatory facilities, and trauma centers. Modern operating rooms are incorporating advanced technologies designed to improve patient safety and clinical efficiency. The growing availability of minimally invasive and complex surgical procedures is generating demand for specialized bleeding-control solutions capable of functioning effectively in challenging operative environments.

According to the U.S. Centers for Medicare & Medicaid Services (CMS), national healthcare expenditure is projected to continue expanding through 2025, reflecting sustained investment in healthcare capacity and service delivery. Infrastructure expansion enables higher surgical throughput and broader adoption of advanced surgical consumables. Healthcare providers are integrating premium hemostatic solutions into standard procedural protocols to improve efficiency, reduce complications, and support value-based care objectives.

Restraint - Complex Supply Chain and Raw Material Dependence

Many advanced hemostatic products depend on biological materials, specialized enzymes, and tightly regulated manufacturing inputs. Limited supplier availability creates vulnerability to production disruptions and procurement delays. Quality assurance requirements further restrict sourcing flexibility, creating operational challenges for manufacturers seeking rapid capacity expansion.

Supply interruptions can increase inventory costs and delay product availability across healthcare networks. Scalability becomes constrained when manufacturers encounter shortages of critical inputs or regulatory bottlenecks. These conditions can affect production efficiency, limit market responsiveness, and create challenges in maintaining consistent margins across global operations.

Opportunity - Expansion of Ambulatory and Outpatient Surgical Care

Healthcare systems are shifting a growing proportion of procedures toward ambulatory surgical centers and outpatient settings. This transition creates demand for hemostatic solutions that support rapid bleeding control, efficient workflow management, and accelerated patient discharge. Manufacturers can develop products specifically designed for minimally invasive procedures and same-day surgical protocols, strengthening adoption across expanding outpatient networks.

Policy initiatives promoting cost-effective care delivery are encouraging healthcare providers to increase utilization of outpatient surgical services. Product developers who align offerings with efficiency-focused clinical pathways can secure new growth avenues. Integration of easy-to-apply, fast-acting hemostatic technologies into outpatient procedures can improve procedural outcomes while supporting broader healthcare system productivity objectives.

Category-wise Analysis

Product Type Insights

Collagen-based hemostats are anticipated to secure around 29% of the topical hemostat market share in 2026, reflecting strong clinical acceptance, broad surgical applicability, and reliable coagulation support during complex procedures. Collagen matrices facilitate rapid platelet activation and effective bleeding control. Collagen hemostatic solutions from leading manufacturers are widely used in cardiovascular surgeries. Consistent surgeon familiarity and established safety profiles continue to support sustained demand across healthcare facilities globally.

Cyanoacrylate-based hemostats are expected to be the fastest-growing segment, propelled by increasing demand for rapid tissue sealing, minimally invasive procedures, and enhanced wound management efficiency. These products provide strong adhesion and effective bleeding control in challenging clinical settings. Advanced surgical adhesive technologies are gaining acceptance in outpatient interventions. Continuous innovation in synthetic formulations is expanding clinical applications and accelerating adoption across diverse surgical specialties.

Application Insights

General surgery is poised to dominate with a forecast market share of over 31% in 2026, powered by high procedure volumes, broad treatment applications, and routine requirements for effective bleeding management. Surgical teams increasingly incorporate advanced hemostatic agents to improve procedural efficiency. Abdominal and gastrointestinal surgeries frequently utilize topical hemostats to support operative control. Rising surgical demand continues to reinforce segment leadership across healthcare institutions worldwide.

Trauma & emergency care is estimated to be the fastest-growing segment, fueled by increasing focus on rapid hemorrhage control and emergency response preparedness. Healthcare providers are adopting advanced solutions capable of delivering immediate bleeding management in critical situations. Trauma centers increasingly utilize portable hemostatic technologies during acute interventions. Expansion of emergency care infrastructure and disaster preparedness initiatives continues to support accelerated growth across this segment.

End-user Insights

Hospitals are likely to be the leading segment with a projected 58% of the topical hemostat market share in 2026 due to the concentration of complex surgical procedures, advanced operating facilities, and specialized clinical expertise. Hospitals perform large volumes of cardiovascular, orthopedic, and neurological surgeries requiring reliable bleeding management. Tertiary care institutions routinely integrate topical hemostatic products into surgical protocols. Strong procedural demand continues to support dominant segment positioning globally.

Ambulatory surgical centers (ASCs) are anticipated to be the fastest-growing segment, fueled by increasing preference for cost-efficient outpatient procedures and shorter recovery pathways. These facilities require products that support procedural efficiency and rapid patient turnover. For example, minimally invasive orthopedic and general surgeries performed in ambulatory settings increasingly incorporate advanced hemostatic technologies. Expansion of outpatient care models continues creating favorable conditions for accelerated segment growth.

Regional Insights

North America Topical Hemostat Market Trends

North America is expected to lead with an estimated 38% of the topical hemostat market share in 2026, supported by high surgical procedure volumes, advanced healthcare infrastructure, and widespread adoption of premium bleeding-management technologies. Strong regulatory oversight from healthcare authorities encourages the deployment of clinically validated products. Major participants, including Johnson & Johnson, Baxter International, and Pfizer, continue expanding product portfolios and clinical collaborations.

U.S. Topical Hemostat Market Insights

The U.S. is projected to account for nearly 84% of North America's revenue in 2026, supported by the increasing prevalence of cardiovascular disease, cancer surgeries, and orthopedic procedures. Expanding ambulatory surgical center capacity is increasing utilization of advanced hemostatic solutions. Product enhancements from leading manufacturers are improving procedural efficiency. Continued healthcare expenditure growth is creating favorable conditions for technology adoption across hospital networks.

Canada Topical Hemostat Market Insights

The Canada market is forecast to represent approximately 11% of North America's revenue in 2026, driven by the expansion of surgical services and investment in hospital infrastructure. Healthcare authorities are emphasizing patient safety and blood-loss reduction strategies during complex procedures. Increasing utilization of minimally invasive surgery is supporting the adoption of advanced hemostatic technologies. Public healthcare investment programs are strengthening procurement activity across major healthcare institutions.

Europe Topical Hemostat Market Trends

Europe is projected to hold around 29% of the topical hemostat market share in 2026, supported by established surgical care systems, aging populations, and strong clinical adoption of advanced surgical adjuncts. Growing emphasis on healthcare efficiency is increasing demand for technologies that reduce operative complications.

Germany Topical Hemostat Market Insights

Germany is expected to contribute nearly 22% of Europe's revenue in 2026, supported by a large hospital network, strong surgical procedure volumes, and advanced operating-room capabilities. Healthcare providers are integrating innovative bleeding-management products into cardiovascular and orthopedic surgeries. Investments in medical technology modernization are improving access to advanced surgical consumables. Clinical focus on reducing transfusion requirements continues to support adoption.

France Topical Hemostat Market Insights

France is forecast to account for approximately 16% of Europe's revenue in 2026, driven by increasing surgical demand and healthcare modernization initiatives. Hospitals are adopting advanced hemostatic products to support procedural efficiency and patient safety objectives. Growth in minimally invasive surgery is creating opportunities for specialized product deployment. Strategic partnerships between healthcare providers and medical technology suppliers are strengthening market penetration.

Asia Pacific Topical Hemostat Market Trends

Asia Pacific is forecast to be the fastest-growing market for topical hemostats, stimulated by rapid healthcare infrastructure expansion, increasing surgical volumes, and growing access to advanced medical technologies. Rising healthcare expenditure and expansion of trauma care networks are accelerating product adoption. International manufacturers are strengthening regional distribution capabilities and local partnerships.

China Topical Hemostat Market Insights

China is projected to account for nearly 37% of Asia Pacific revenue in 2026, supported by extensive hospital construction programs and increasing availability of advanced surgical procedures. Government initiatives focused on healthcare access are expanding utilization of modern surgical technologies. Domestic and international manufacturers are increasing production capacity and distribution reach. Rising procedure volumes are creating substantial opportunities for hemostatic product adoption.

India Topical Hemostat Market Insights

India is expected to contribute approximately 19% of Asia Pacific revenue in 2026, driven by healthcare infrastructure development, increasing surgical interventions, and growth in private hospital networks. The adoption of advanced hemostatic technologies is increasing across multispecialty hospitals and trauma centers. Government healthcare initiatives aimed at improving treatment access are supporting procedural growth. Expanding medical device availability is contributing to broader utilization across healthcare facilities.

Competitive Landscape

The global topical hemostat market is moderately fragmented, with competition shaped by product innovation, regulatory compliance, clinical evidence generation, and distribution strength. Major participants include Johnson & Johnson, Baxter International, B. Braun, Pfizer, and Advanced Medical Solutions Group. These companies maintain competitive positions through diversified product portfolios and established healthcare relationships.

Market competition is increasingly focused on bioengineered materials, synthetic formulations, and procedure-specific solutions. Strategic investments in manufacturing efficiency, research programs, and geographic expansion are strengthening commercial positioning. Clinical performance, surgeon familiarity, and procurement partnerships remain important factors influencing purchasing decisions across healthcare institutions.

Key Industry Developments:

In April 2025, Baxter International launched the room-temperature HEMOPATCH Sealing Hemostat, an absorbable collagen-based topical hemostat designed for rapid bleeding control and tissue sealing in both open and minimally invasive surgical procedures, reinforcing innovation in surgical hemostasis and operating-room efficiency.

Companies Covered in Topical Hemostat Market

- Johnson & Johnson

- Baxter International

- B. Braun

- Pfizer

- Advanced Medical Solutions Group

- Teleflex

- Integra LifeSciences

- BD

- Medtronic

- Stryker

- Artivion

- Marine Polymer Technologies

- Biocer Entwicklungs-GmbH

- Hemostasis LLC

- Gelita Medical

Frequently Asked Questions

The global topical hemostat market is projected to reach US$6.3 billion in 2026.

The topical hemostat market is driven by rising surgical procedure volumes, increasing prevalence of chronic diseases requiring surgery, and growing adoption of advanced bleeding-control technologies to improve surgical outcomes.

The topical hemostat market is poised to witness a CAGR of 9.8% from 2026 to 2033.

Key market opportunities lie in the expansion of ambulatory surgical centers, increasing adoption of minimally invasive procedures, and innovation in synthetic and bioengineered hemostatic technologies.

Some of the key market players include Johnson & Johnson, Baxter International, B. Braun, Pfizer, and Advanced Medical Solutions Group.