- Medical Devices

- Tele-Care Medical Equipment Market

Tele-Care Medical Equipment Market Size, Share, and Growth Forecast, 2026-2033

Tele-Care Medical Equipment Market by Equipment Type (RPM Devices, Wearable Tele-Care Devices, Telehealth Platforms & Software, Emergency & Response Systems, Medication Management Devices), Application (Chronic Disease Management, Elderly & Independent Living Care, Rehabilitation Care, Preventive & Wellness Monitoring, Emergency Detection), Connectivity (IoT & Connected Devices, Wireless Connectivity Tech, Cloud Platforms, AI & Analytics Modules, Others), and Regional Analysis for 2026-2033

Tele-Care Medical Equipment Market Share and Trends Analysis

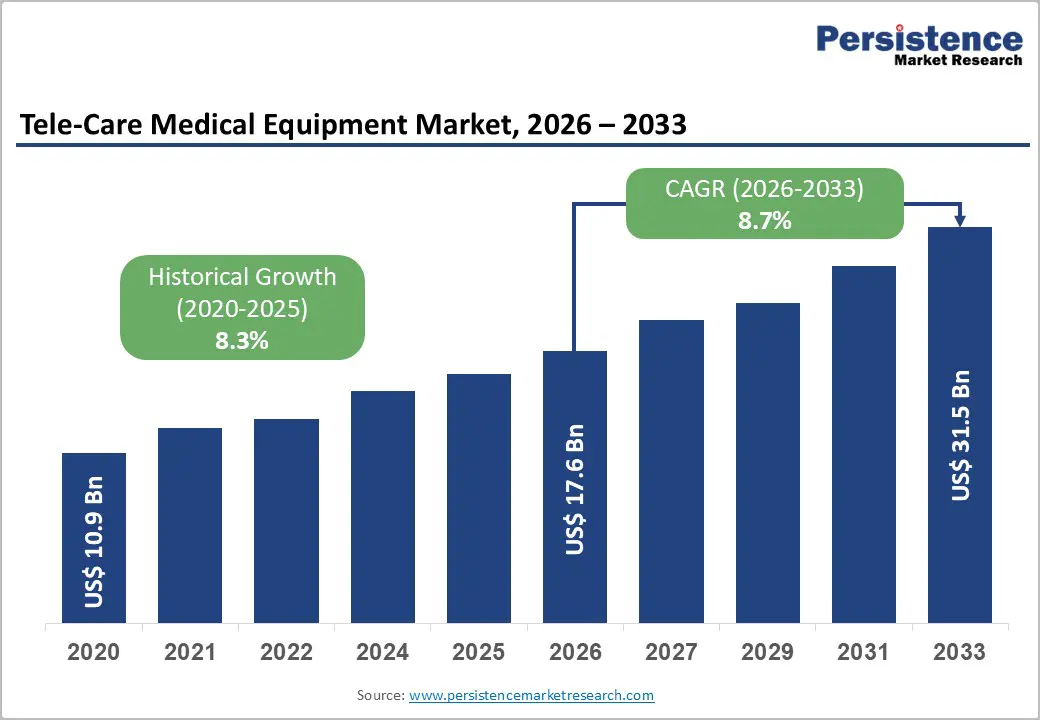

The global tele-care medical equipment market size is likely to be valued at US$ 17.6 billion in 2026, and is projected to reach US$ 31.5 billion by 2033, growing at a CAGR of 8.7% during the forecast period 2026–2033. Growth is being driven by the rapid adoption of remote patient monitoring solutions across hospitals, clinics, and home healthcare settings. The rising prevalence of chronic conditions such as diabetes, cardiovascular disorders, and respiratory illnesses is increasing the need for continuous health tracking outside traditional clinical environments. Governments and regulatory bodies are supporting digital health initiatives through reimbursement reforms and telemedicine infrastructure investments.

Healthcare providers are transitioning toward decentralized care delivery models to reduce hospitalization costs and improve patient engagement. As health systems prioritize preventive management and early intervention, demand for connected medical equipment is increasing across multiple care pathways. Technological advancement is reinforcing long-term demand for tele-care platforms. Internet of Things (IoT)-enabled medical devices are facilitating real-time data transmission from patients’ homes to centralized clinical systems.

Cloud-based analytics tools are improving data aggregation, enabling healthcare professionals to monitor trends and identify risk patterns more efficiently. Artificial intelligence (AI)-driven clinical decision support systems are assisting physicians in interpreting remote patient data with greater accuracy. Integration with electronic health records is improving continuity of care and workflow efficiency. Manufacturers are investing in device interoperability, cybersecurity compliance, and user-friendly interfaces to support broader adoption.

Key Industry Highlights

- Dominant Equipment: Remote patient monitoring (RPM) devices are expected to lead with 38% revenue share in 2026, while wearable tele-care devices are projected to grow the fastest during 2026–2033, driven by clinical-grade wearable adoption.

- High-Growth Technology Enablers: IoT & connected devices are likely to account for 34% share in 2026, whereas AI & analytics modules are forecast to register the highest growth at 11.4% CAGR through 2033 as predictive care gains traction.

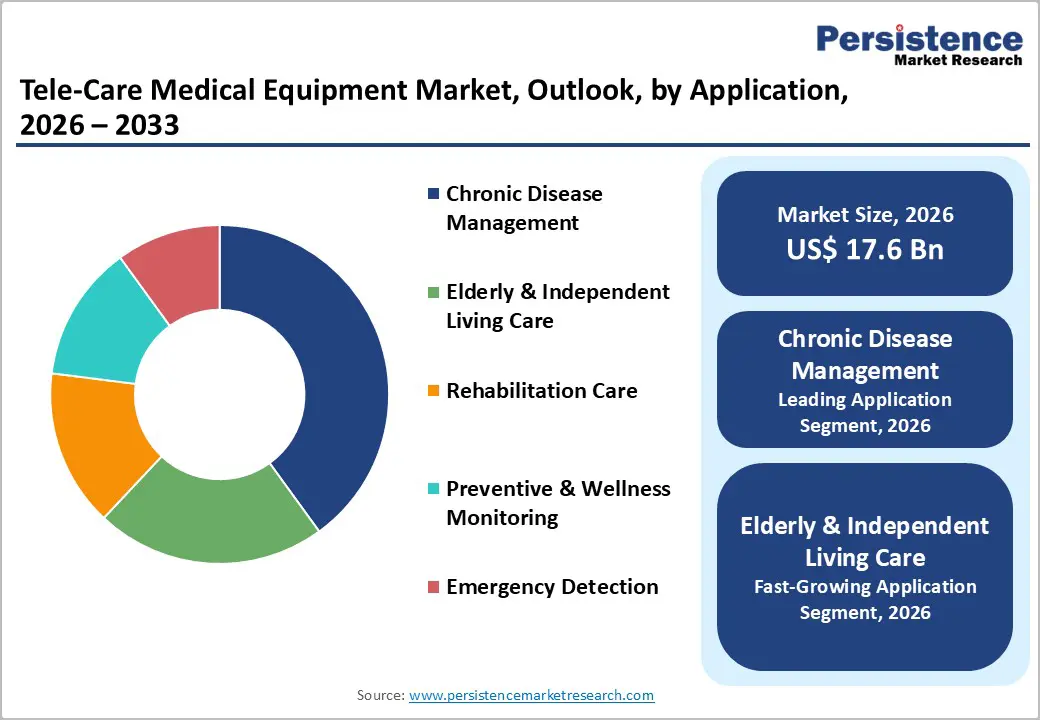

- Application Leadership: Chronic disease management is anticipated to dominate with roughly 40% revenue share in 2026, while elderly & independent living care is projected to grow the fastest at about 9.8% CAGR, supported by rising home-based care adoption.

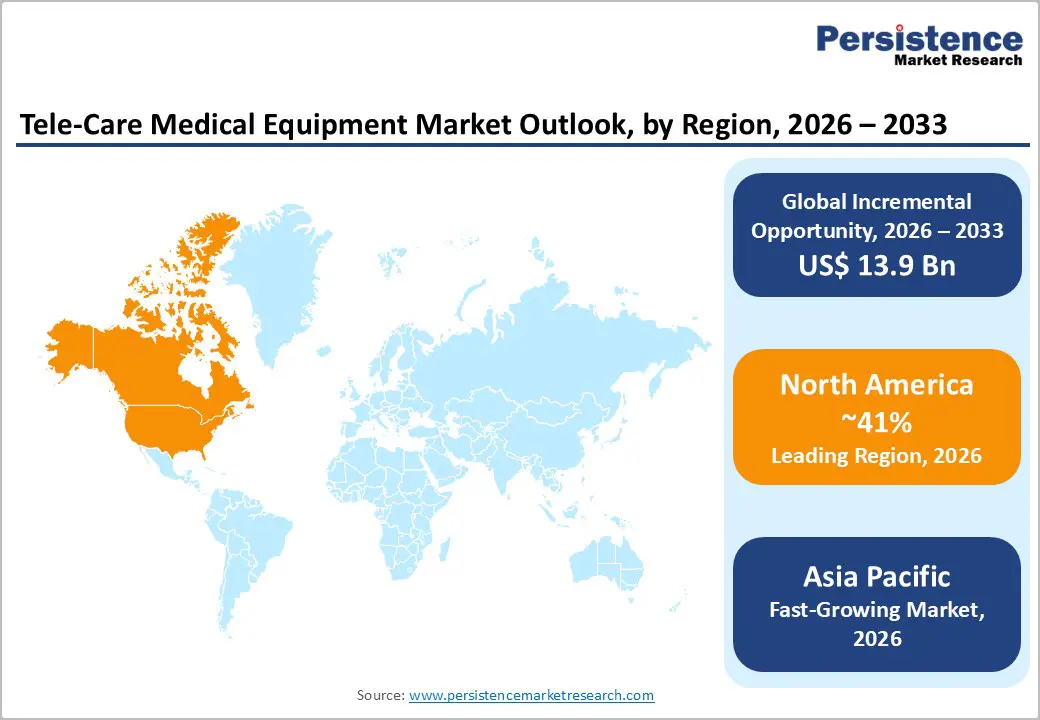

- Regional Dynamics: North America is projected to lead with approximately 41% market share in 2026, while the Asia-Pacific market is expected to record the fastest regional growth at a 9.6% CAGR through 2033.

- Demand Driver: Reimbursement expansion and aging population are accelerating the adoption of home-based and hospital-at-home care models, ensuring long-term demand growth.

- Competitive Differentiators: Market leadership is being increasingly determined by platform integration, interoperability, and predictive analytics, shifting competition from devices to end-to-end tele-care ecosystems.

| Global Market Attributes | Key Insights |

|---|---|

| Tele-Care Medical Equipment Market Size (2026E) | US$ 17.6 Bn |

| Market Value Forecast (2033F) | US$ 31.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Reimbursement Reform and Digital Care Effectiveness to Meet Chronic Care Demand

The burden of chronic diseases such as diabetes, cardiovascular disorders, and respiratory conditions has reached structurally high levels. According to the World Health Organization (WHO), non-communicable diseases (NCDs) account for over 74% of all deaths worldwide. Most of these conditions require continuous monitoring rather than episodic clinical intervention. This shift is significantly increasing demand for tele-care medical equipment, particularly remote patient monitoring devices and connected wearables. Health systems are steadily moving toward continuous, home-based care models. In the United States, the Centers for Medicare & Medicaid Services (CMS) has expanded reimbursement coverage for remote physiological monitoring (RPM) and telehealth services, permanently integrating several pandemic-era provisions into standard care pathways. This policy clarity has strengthened provider confidence and accelerated adoption.

Telecare solutions deliver substantial clinical and economic value to the market. Tele-care solutions have demonstrated reductions of 15–30% in avoidable hospitalizations in large-scale pilot programs reported by public health agencies. These outcomes directly support cost-containment objectives for payers and providers. Fewer hospital admissions improve capacity utilization and care delivery efficiency. Advances in IoT connectivity, cloud platforms, and AI-driven analytics are taking device intelligence to the next level. Modern systems now support predictive alerts and seamless data integration. Together, these factors enable scalable deployments and long-term procurement opportunities for telecare equipment manufacturers.

High Cost, Regulatory, and Operational Challenges Limiting Adoption

Despite falling sensor and connectivity costs, upfront investments in telecare medical equipment, backend IT infrastructure, and cybersecurity compliance remain major barriers. Enterprise-grade remote monitoring deployments can require US$500–US$1,500 per patient annually, depending on device complexity and data services. These costs disproportionately impact smaller providers and low-resource settings, slowing adoption in price-sensitive markets. Uneven broadband penetration, limited digital literacy, and low patient engagement in some regions further restrict effective utilization. The interoperability challenges across EHRs and hospital IT systems create fragmented workflows, reducing clinical efficiency and hindering large-scale deployment.

Regulatory and operational complexities add another layer of restraint. Compliance with the Health Insurance Portability and Accountability Act (HIPAA) of the U.S., the General Data Protection Regulation (GDPR) of the European Union (EU), and country-specific medical device laws increases development timelines and costs. Cybersecurity risks continue to rise, with double-digit annual growth in healthcare-related data breaches reported, prompting heightened scrutiny of data protection. Supply chain bottlenecks for specialized sensors and components can delay device availability, particularly for high-demand wearables and smart pill dispensers. Limited reimbursement frameworks in emerging markets further restrict adoption, as out-of-pocket costs remain high. These combined challenges constrain market expansion and necessitate strategic mitigation to achieve sustainable growth.

Expanding Care Models and Technology-Enabled Preventive Solutions

Aging populations and rising chronic disease burden are driving sustained demand for home-based care, elderly care, and post-acute monitoring solutions. Telecare devices, such as remote monitoring systems, fall-detection units, and medication management systems, are increasingly deployed to support independent living and reduce hospital readmissions. Spending on home-care equipment in developed markets is projected to exceed 35% of total demand by 2030, while emerging markets offer additional growth potential due to underserved populations. Hospitals, rehabilitation centers, and corporate wellness programs are adopting remote monitoring for chronic disease management, post-acute care, and preventive health, creating recurring revenue streams for device manufacturers and platform providers.

Real-world deployments highlight the scale of these opportunities. The National Health Service (NHS) Virtual Wards program in England now treats more than 30,000 patients per month using wearable monitors and connected devices, enabling patients to receive hospital-level care at home. These programs reduce hospital strain while improving patient outcomes, demonstrating the value of tele-care integration. Simultaneously, AI-driven predictive solutions detect early deterioration among patients with chronic conditions, reducing acute care episodes by 20–25%. Vendors can monetize this through subscription platforms, analytics modules, and outcome-linked services, while expansion into emerging markets and mobile health integration offers additional avenues for growth and long-term adoption.

Category-wise Analysis

Equipment Type Insight

RPM devices are expected to remain the leading product type, accounting for approximately 38% of the telecare medical equipment market revenue in 2026. Adoption is likely to be driven by chronic care and post-acute follow-up needs. For instance, Philips’ launch of the Smart Telemetry Platform and Telemetry Monitor 5500 is anticipated to support broader RPM deployment across hospital networks, enabling continuous cardiac monitoring and improved clinical oversight. These devices are projected to reduce avoidable hospitalizations and support large-scale home-based care models. Integration with analytics dashboards may enhance early intervention capabilities, while ongoing reimbursement support is expected to sustain demand.

Wearable tele-care devices are projected to be the fastest-growing equipment type, with an estimated CAGR of 10.2% through 2033. Growth is likely to be driven by sensor miniaturization, mobile health integration, and consumer acceptance. For example, Sempulse’s Halo™ Vital Signs Monitoring System demonstrates the potential of compact, cloud-connected wearables for remote monitoring and wellness tracking. These devices are expected to expand adoption in preventive care, chronic condition management, and real-time patient engagement. Integration with mobile platforms and predictive analytics is likely to strengthen their market penetration. The segment’s projected growth is driven by rising interest from both providers and consumers, making wearables a key opportunity in telecare.

Application Insights

Chronic disease management is projected to remain the dominant application, accounting for roughly 40% of the telecare medical equipment market share in 2026. Sustained monitoring needs and payer-supported care pathways are expected to drive adoption. For instance, Teladoc Health’s acquisition of Australia-based Telecare may expand virtual care capabilities and integrate RPM into specialist workflows, supporting projected growth in chronic disease monitoring. Deployment of remote monitoring data in routine clinical practice is likely to enhance early intervention and improve cost efficiency. The segment is expected to benefit from ongoing digital health policy support and from the rising prevalence of chronic diseases. Integration with mobile and cloud platforms may further strengthen adoption and recurring revenue opportunities. Overall, chronic disease management is expected to remain the largest revenue contributor in telecare.

Elderly & independent living care is projected to be the fastest-growing application at a 2026-2033 CAGR of 9.8%, driven by aging populations and rising demand for home-based safety monitoring. For example, Prevounce Health’s deployment of cellular-connected devices and cloud software is anticipated to support mobility tracking and fall detection for older adults. Adoption of such solutions is expected to increase across private residences, assisted living, and public care programs. Government initiatives and insurance reimbursement may further encourage uptake. Integration with AI-driven alerts and remote monitoring platforms is likely to enhance caregiver response capabilities. This segment is projected to grow rapidly as independent living solutions expand in developed and high-income emerging markets.

Connectivity Insights

IoT & connected devices are expected to remain the leading technology segment, capturing an estimated revenue share of 34% in 2026, forming the backbone of the real-time tele-care ecosystem. Teladoc’s virtual care platform expansions leveraging connected devices are projected to enable continuous vital monitoring, remote care coordination, and support for hospital-at-home programs. The adoption of connected devices is likely to increase operational efficiency and clinical oversight across both hospital and home-based programs. Scalability and interoperability with wearables and stationary monitoring units are expected to sustain their market leadership. This segment is expected to continue to enable integrated telecare solutions, supporting projected revenue growth across multiple applications.

AI & analytics modules are anticipated to be the fastest-growing technology layer, with an estimated CAGR of 11.4% through 2033, as predictive healthcare and preventive monitoring gain traction. For example, Current Health’s AI-enabled monitoring platform demonstrates the potential to synthesize wearable data with contextual patient information to generate actionable risk alerts. Adoption of such AI tools is expected to increase across hospital, home, and community care settings. Health systems are likely to prioritize platforms that provide predictive insights and support early intervention. Integration with cloud and mobile platforms may further accelerate market growth. The segment is projected to gain prominence as providers shift from reactive to proactive care models.

Regional Insights

North America Tele-Care Medical Equipment Market Trends

North America is projected to account for approximately 41% of the global market in 2026, led by the United States, where telecare adoption continues to grow alongside innovative healthcare delivery models. Starr Regional Medical Center in Georgia implemented a 24/7 tele-ICU service using connected care technology that links on-site critical care teams with remote intensivists, enhancing care quality for critically ill patients without travel. This initiative reflects how tele-care solutions are extending beyond routine monitoring into specialized clinical care delivery and supporting hospital efficiency. Increasing integration of monitoring platforms with electronic health records further strengthens the usability and impact of tele-care across hospital networks.

The U.S. tele-care landscape is also seeing expanded RPM use for chronic conditions, such as companies integrating continuous glucose monitoring data into clinician dashboards to support diabetes programs, demonstrating practical device-to-provider workflows. Such deployments improve access to specialist care in non-urban settings and are anticipated to drive long-term demand. Continued investment in connected health infrastructure, reimbursement reforms, and value-based care models is expected to further anchor tele-care devices and platforms in mainstream care delivery throughout the region. Partnerships among device manufacturers, payers, and hospital networks are also expected to accelerate innovation and adoption, thereby strengthening North America's market position.

Europe Tele-Care Medical Equipment Market Trends

The market for telecare medical equipment in Europe is projected to grow steadily over the 2026-2033 forecast period, driven by government initiatives and evolving care models in Germany, the U.K., France, Spain, and other EU countries. Bupa announced plans to open the Blua Valdebebas Hospital in Madrid, a hybrid digital-physical care facility that combines in-person services with virtual consultations and at-home monitoring support. This initiative highlights how European providers are integrating tele-care with traditional care pathways to enhance patient convenience, improve continuity of care, and support more efficient hospital operations. The facility also demonstrates the region’s commitment to adopting innovative monitoring technologies, including connected devices and cloud-based platforms, to extend healthcare delivery beyond hospital walls.

Europe’s aging population and coordinated policy frameworks are also driving the expansion of virtual ward programs and hospital-at-home models, which rely on remote monitoring and connected devices to deliver hospital-level care outside traditional settings. Continued emphasis on interoperability, cloud-based telecare platforms, and integration into public health systems is expected to support sustained adoption of telecare equipment, reduce pressure on acute care capacity, and improve clinical outcomes. Partnerships between device manufacturers, healthcare providers, and digital health startups are likely to accelerate technology adoption. Regional investments in training and digital infrastructure further strengthen market potential for tele-care solutions.

Asia Pacific Tele-Care Medical Equipment Market Trends

Asia Pacific is forecast to be the fastest-growing regional market for tele-care medical equipment, expected to register an estimated 9.6% CAGR between 2026 and 2033, supported by rapid digital health evolution and government-led telemedicine initiatives. The National University Health System (NUHS) in Singapore expanded its NUHS@Home hospital-at-home program, enabling eligible patients to receive hospital-level services in their own homes using remote monitoring and virtual consultations. This expansion has served thousands of patients, alleviating demand for hospital beds and demonstrating the scalability of telecare deployment in a developed Asia-Pacific healthcare system. The program highlights the growing integration of connected devices, mobile health applications, and clinician dashboards to support continuous care and early intervention.

Across the region, increasing smartphone penetration, investments in digital health infrastructure, and hybrid care models are driving the adoption of mobile-integrated tele-care platforms for chronic disease management and preventive monitoring. A major example is India’s eSanjeevani national telemedicine platform, rolled out across tens of thousands of health facilities, enabling remote consultations for hundreds of millions of patients. This deployment demonstrates how government-led digital health infrastructure can rapidly expand tele-care utilization, creating opportunities for connected monitoring devices, mobile health integration, and analytics-driven care models across public and private systems.

Competitive Landscape

The global tele-care medical equipment market structure is moderately consolidated, led by major players such as Philips Healthcare, GE Healthcare, Medtronic, Abbott Laboratories, Boston Scientific, and Honeywell Life Sciences, who leverage broad portfolios spanning remote patient monitoring, wearable devices, and telehealth platforms. Strategic partnerships and technology integrations, such as Cisco Systems collaborating with Teladoc Health to enhance video-enabled remote care, illustrate the shift toward platform-centric solutions.

Regional and niche competitors such as Nihon Kohden, Masimo, Biotronik, and Spacelabs Healthcare focus on specialized devices and ambulatory monitoring. Regulatory compliance, system integration, and cybersecurity remain barriers for new entrants, while software-driven and mobile-integrated platforms enable smaller players to participate. Competitive differentiation increasingly depends on interoperability, predictive analytics, and cloud-based care ecosystems, with gradual consolidation expected through acquisitions and collaborative partnerships to expand geographic and technological reach.

Key Industry Developments

- In October 2025, Abbott introduced the world’s first dual-chamber leadless pacemaker system, enabling synchronized pacing of the atrium and ventricle without traditional leads or surgical pockets. Using proprietary implant-to-implant (i2i™) communication, the system reduces infection risk and lead-related complications. Clinical trials showed a 98.3% implant success rate and normal atrio-ventricular synchrony in over 97% of patients.

- In October 2025, Vonage, part of Ericsson, collaborated with Collette Health to integrate the Vonage Video API into its tele-care platform, supporting real-time remote patient observation. The solution enhances virtual nursing, fall prevention, and patient safety using AI-powered risk identification and secure, high-quality video.

- In May 2025, TELUS Health finalized the US$ 500 million acquisition of WPO, expanding its global digital-first health and wellbeing portfolio. The combined entity now serves over 150 million lives across 200+ countries, integrating mental, physical, and financial health programs with TELUS Health’s AI-driven services.

Companies Covered in Tele-Care Medical Equipment Market

- Philips Healthcare

- Medtronic

- GE HealthCare

- Siemens Healthineers

- Abbott Laboratories

- Boston Scientific

- ResMed

- Omron Healthcare

- Honeywell Life Care Solutions

- BioTelemetry

- Masimo

- Roche Diagnostics

Frequently Asked Questions

The global tele-care medical equipment market is projected to reach US$ 17.6 billion in 2026.

Rising chronic disease prevalence, aging populations, and supportive reimbursement policies are driving the market.

The market is poised to witness a CAGR of 8.7% from 2026 to 2033.

Expansion of home-based care, AI-driven predictive monitoring, and emerging markets adoption are key opportunities.

Key players include Philips Healthcare, GE Healthcare, Medtronic, Abbott Laboratories, Boston Scientific, Honeywell Life Sciences, Nihon Kohden, Masimo, Biotronik, and Spacelabs Healthcare.