- Sporting Goods & Equipment

- Surfboard Market

Surfboard Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Surfboard Market by Product Type (Shortboards, Longboards, Fish Boards, Gun Boards, Others), Material (Polyurethane, Foam, Wood, Others), Application (Amateurs, Professionals), by Sales Channel (Wholesalers/Distributors, Hypermarkets/Supermarkets, Specialty Stores, Independent Small Stores, Online Retailers, Others), and Regional Analysis, 2026 - 2033

Surfboard Market Size and Trend Analysis

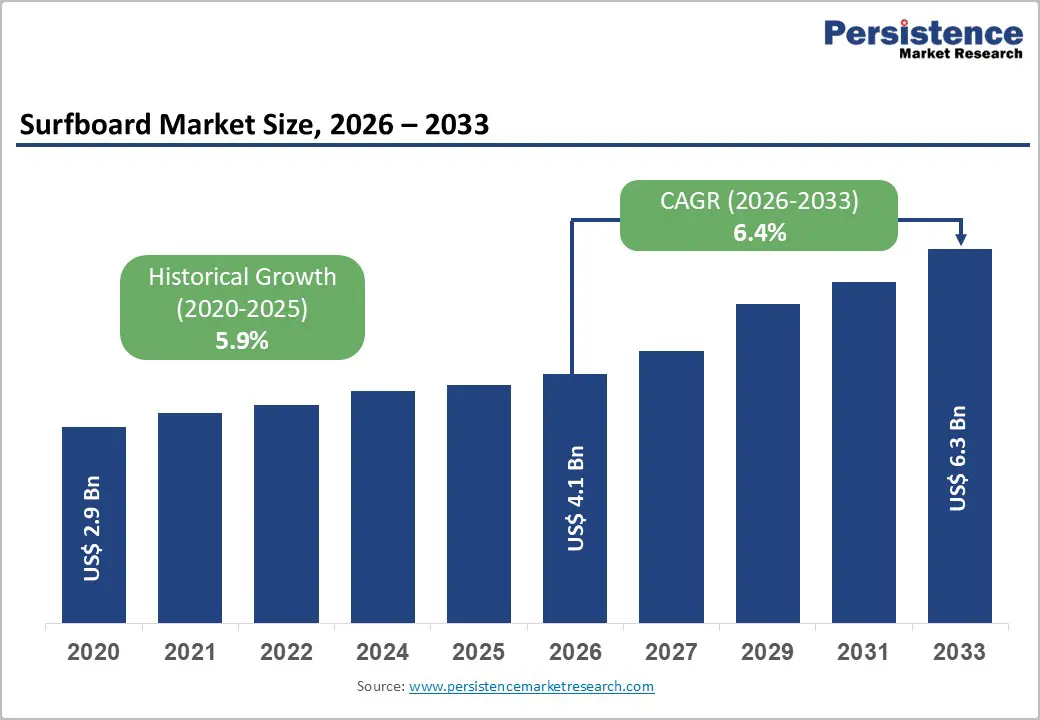

The global surfboard market is projected to reach US$4.1 billion in 2026 and US$6.3 billion by 2033, with a CAGR of 6.4% over the period. Rising participation in recreational water sports and expanding surf tourism are key contributors to this steady growth trajectory.

The inclusion of surfing in the Olympic Games has significantly increased global visibility and participation. Increasing investments in artificial wave pools are improving inland accessibility and broadening the consumer base. Furthermore, advancements in sustainable and high-performance materials are reshaping product innovation, attracting environmentally conscious millennials and Gen Z consumers worldwide.

Key Industry Highlights:

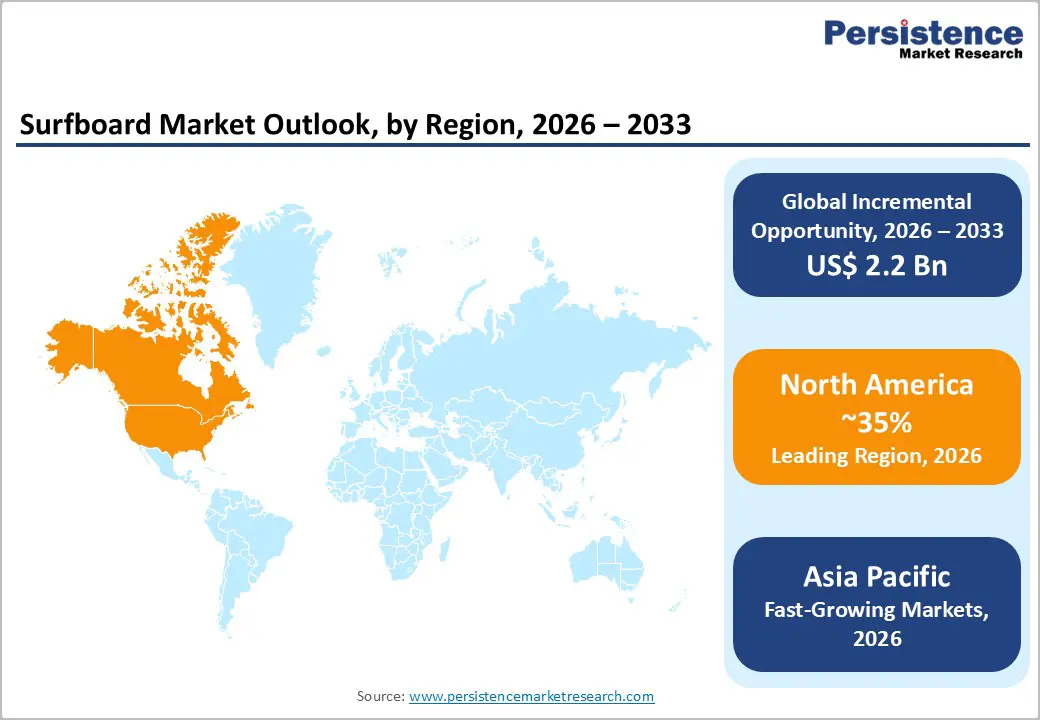

- Leading Region: North America leads the Surfboard Market with a 35% share in 2025, supported by strong U.S. surfing culture and nearly 4 million active participants.

- Fastest Growing Region: Asia Pacific holds a 32% share in 2025 and continues to expand rapidly due to rising participation and coastal infrastructure development.

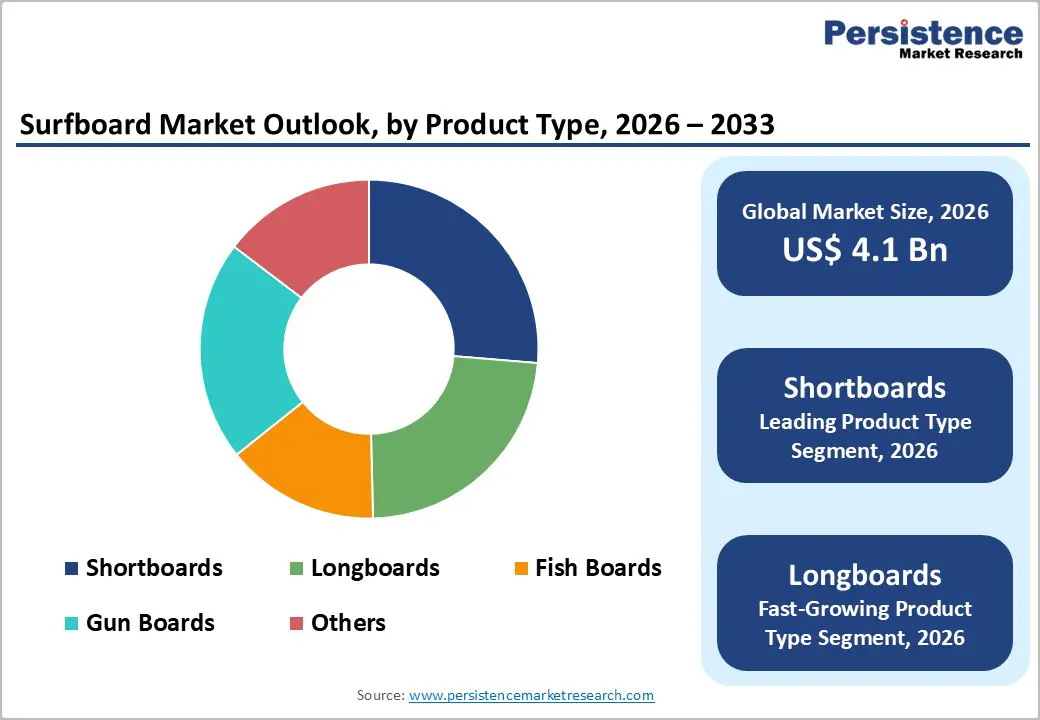

- Leading Product Type: Shortboards dominate the market with a 39% share in 2025, favored for high maneuverability and professional performance.

- Leading Material Segment: Polyurethane accounts for 42% share in 2025, maintaining strong preference for its traditional responsiveness and versatility.

- Leading Application Segment: Amateur surfers represent 66% of the market in 2025, supported by growing recreational and beginner participation globally.

- Key Market Opportunity: Surf tourism expansion in emerging markets presents a significant opportunity, particularly targeting beginner surfers and rental-driven demand growth.

| Key Insights | Details |

|---|---|

|

Surfboard Market Size (2026E) |

US$ 4.1 billion |

|

Market Value Forecast (2033F) |

US$ 6.3 billion |

|

Projected Growth CAGR(2026-2033) |

6.4% |

|

Historical Market Growth (2020-2025) |

5.9% |

Market Dynamics

Drivers - Growing Global Participation and Olympic Recognition Strengthening Surfing Demand

The surge in global surfing participation significantly drives surfboard demand. The International Surfing Association (ISA) estimates over 35 million active surfers worldwide, with the Americas accounting for nearly 13.5 million participants. Surfing’s debut at the Tokyo 2020 Olympics enhanced global visibility, inspiring new entrants through extensive media coverage and professional endorsements. This exposure has accelerated recreational adoption across coastal and emerging inland markets.

In the United States alone, surfing participation approached 4 million in 2023, marking notable annual growth and stimulating demand for beginner and performance boards. Additionally, surf tourism supports more than 3,200 coastal resorts globally, generating consistent equipment sales. Growing surf schools, rental services, and competitive events further sustain repeat purchases, reinforcing long-term market expansion.

Technological Advancements in Sustainable Materials Driving Product Innovation

Innovations in eco-friendly surfboard construction are emerging as a major market catalyst. Manufacturers are increasingly adopting bio-based resins, recycled foam cores, and responsibly sourced wood materials to address environmental concerns such as ocean plastic pollution. The ISA continues to promote sustainability initiatives, encouraging brands to integrate greener production practices and reduce carbon footprints across supply chains.

Approximately 61% of eco-resort surfboards incorporate handcrafted balsa wood or alternative sustainable materials, reflecting shifting consumer preferences. Environmentally conscious millennials and Gen Z buyers are actively favoring sustainable products, enabling brands to command premium pricing. These advancements also align with tightening environmental regulations, strengthening long-term market resilience and competitive differentiation.

Restraints - Rising Raw Material Costs and Supply Chain Volatility Limiting Profit Margins

High production and procurement costs present a significant restraint for the surfboard market. Polyurethane foam, a primary core material, remains heavily dependent on petrochemical inputs, leading to price volatility and unpredictable supply fluctuations. Rising labor costs, transportation expenses, and import dependencies further increase manufacturing overheads, particularly for small and mid-sized shapers operating with limited margins.

Economic downturns further intensify pressure, as surfboards are largely discretionary purchases. During recessionary cycles, consumers often delay spending on premium or custom boards, slowing sales momentum. Additionally, environmental compliance requirements necessitate investment in sustainable alternatives, increasing research, certification, and production costs, thereby constraining profitability and market scalability.

Seasonal Demand Patterns and Limited Accessibility Restricting Market Penetration

The surfboard market is highly influenced by seasonal weather conditions, limiting year-round demand in many regions. Nearly 40% of surfing activities are concentrated within favorable climate months, resulting in uneven sales cycles and inventory challenges for retailers. Coastal erosion affects approximately 18% of beaches globally, reducing the availability of optimal surfing locations and impacting participation rates.

High equipment costs discourage nearly 15% of potential first-time buyers, particularly in emerging markets. Safety concerns, physical skill requirements, and limited training infrastructure further restrict adoption. Beginners often require larger, more stable boards, increasing entry costs and slowing widespread market penetration.

Opportunities - Rising Surf Tourism and Infrastructure Development in Emerging Coastal Economies

The expansion of surf tourism across Asia Pacific presents strong growth potential for the surfboard market. The region hosts nearly 6 million surfers, with Australia accounting for about 1.7 million participants and Indonesia emerging as a global surf destination. Increasing investments in artificial wave pools and coastal tourism infrastructure in countries such as China and India are enabling year-round surfing access.

These developments support equipment demand from both domestic participants and international travelers. Approximately 34% of surfers are beginners, creating opportunities for rental programs and entry-level board sales. With over 3,200 surf-oriented resorts worldwide, operators can bundle experiential packages, strengthening recurring equipment demand and brand visibility.

Growth of E-commerce Platforms and Personalized Surfboard Offerings

The rapid adoption of digital sales channels is transforming surfboard distribution strategies. Online platforms facilitate direct-to-consumer sales, with global online volumes reaching approximately 1.5 million units annually. Brand leveraging customization tools allow surfers to personalize board dimensions, materials, and graphics, enhancing customer engagement and brand loyalty.

Direct models, such as those implemented by leading performance brands, reduce intermediary markups while generating valuable rider data for research and development. This approach aligns well with rising disposable incomes and expanding e-commerce penetration in Asia Pacific. Digital scalability enables manufacturers to access global markets with lower operational overhead and improved margin control.

Category-wise Analysis

Product Type Insights

Shortboards lead the surfboard market with an estimated 39% share in 2025, driven by strong adoption among advanced and professional surfers. Typically measuring between 5 and 7 feet, these boards are preferred for superior maneuverability, speed, and responsiveness in competitive environments. Their dominance is reinforced by usage in international tournaments governed by the International Surfing Association (ISA), along with strong visibility in U.S. competitions and professional athlete endorsements.

Meanwhile, foam and soft-top boards are emerging as the fastest-growing product segment. Their enhanced stability, safety, and beginner-friendly design make them highly suitable for surf schools and first-time participants. Rising surfing participation and expanding training programs globally are accelerating demand for these accessible and low-risk board types.

Material Insights

Polyurethane (PU) holds a leading 42% share of the surfboard market in 2025, supported by its dense and responsive core structure that delivers a traditional surfing feel. More than 1.9 million PU-based units were produced in 2024, reflecting its widespread adoption across commercial and recreational segments. Its flexibility and lightweight properties make it suitable for over 700 surf schools worldwide, sustaining consistent institutional demand.

Epoxy and sustainable composite materials represent the fastest-growing material segment. Increasing environmental awareness and regulatory pressures are encouraging manufacturers to adopt bio-based resins, recycled foams, and alternative cores. These materials offer improved durability and lighter weight, attracting performance-oriented and environmentally conscious consumers seeking modern board construction technologies.

Application Insights

Amateur surfers account for approximately 66% of the surfboard market in 2025, supported by strong recreational growth following surfing’s Olympic inclusion. With an estimated 35 million global surfers, a large proportion consists of beginners and intermediate participants seeking stable, easy-to-handle boards. Growth in surf schools and tourism activities, along with rising U.S. participation nearing 4 million individuals, continues to drive entry-level and mid-range board sales.

Professional and competitive surfing is the fastest-growing application segment. Increased sponsorships, international competitions, and media visibility are expanding interest in high-performance boards. The professional ecosystem is fostering innovation in board design, influencing product development trends, and encouraging performance-focused upgrades among experienced surfers.

Sales Channel Insights

Specialty surf stores lead the market with a 34% share in 2025, as consumers prefer in-person product evaluation and expert guidance before purchasing. These stores provide hands-on inspection, personalized recommendations, and community engagement, strengthening brand loyalty. Consignment models and local shaping collaborations further enhance offline retail dominance, particularly for custom-fit and performance-oriented boards.

Online retail channels are emerging as the fastest-growing distribution segment. E-commerce platforms enable wider product availability, customization tools, and direct-to-consumer sales strategies. Digital channels allow brands to expand geographically with lower overhead costs while offering personalized configurations, attracting tech-savvy and younger consumer groups seeking convenience and product variety.

Regional Insights

North America Surfboard Market Trends

North America leads the global surfboard market with a 35% share in 2025, driven primarily by the United States. Surfing remains deeply embedded in the culture of California and Hawaii, supporting a strong consumer base and professional ecosystem. Nearly 4 million Americans participated in surfing in 2023, reflecting steady growth supported by high disposable incomes and established brands such as Channel Islands. Regulatory oversight and event promotion by organizations like USA Surfing further strengthen industry structure.

Innovation remains a defining characteristic of the region, with Olympic-driven momentum accelerating performance technology and artificial wave pool development. Expanding inland surfing facilities are broadening accessibility beyond coastal areas. Fitness and outdoor recreation trends continue to reinforce participation, ensuring sustained equipment demand across recreational and competitive segments.

Europe Surfboard Market Trends

Europe accounts for a significant share of global participation and is projected to expand at a CAGR of 6.8% through the forecast period. The United Kingdom, France, Spain, and Portugal form the core surfing hubs, with approximately 0.5 million surfers each in the U.K. and France. Coastal destinations such as Portugal’s Nazaré and France’s Biarritz host international competitions, strengthening equipment demand and tourism-linked purchases.

Sustainability regulations under European Union frameworks are accelerating the adoption of eco-friendly surfboard materials. Growing environmental awareness among consumers aligns with this transition, encouraging innovation in bio-based resins and recyclable cores. Expanding surf tourism and structured training programs further support steady regional growth.

Asia Pacific Surfboard Market Trends

Asia Pacific holds an estimated 32% share of the global surfboard market in 2025 and is the fastest-growing region, supported by expanding participation and tourism. The region hosts nearly 6 million surfers, led by Australia with approximately 1.7 million participants and Indonesia as a major international surf destination. Strong coastal tourism and favorable climatic conditions reinforce equipment demand across both domestic and inbound traveler segments.

Rapid infrastructure investments in China, India, and Japan, including artificial wave pools, are improving accessibility and year-round participation. Rising disposable incomes and increasing interest in adventure sports are further stimulating growth. The region’s manufacturing capabilities also provide cost advantages, supporting both domestic consumption and export-oriented production.

Competitive Landscape

The surfboard market remains highly fragmented, characterized by the presence of independent artisan shapers alongside established global brands. Competition is driven by product differentiation, craftsmanship quality, and performance innovation. Manufacturers increasingly focus on advanced materials such as epoxy resins and sustainable composites to enhance durability, weight efficiency, and environmental appeal. Custom shaping capabilities and performance-driven designs remain central to brand positioning.

Strategic expansion efforts center on direct-to-consumer channels, digital customization platforms, and partnerships with surf tourism operators. Companies are leveraging e-commerce to broaden geographic reach while collecting rider data to support research and development. Sustainability, personalization, and technological innovation continue to shape competitive dynamics.

Key Developments:

- In July 2024, professional surfer John Florence, in collaboration with renowned shaper Jon Pyzel, introduced the Power Tiger surfboard, engineered to enhance speed, drive, and control across a wide range of wave conditions. The model integrates refined rail contours and advanced shaping techniques to optimize high-performance surfing.

- In February 2025, industry reports highlighted that leading surf brands Quiksilver and Rip Curl are accelerating the adoption of sustainable materials, including bio-based resins and eco-friendly composites. These initiatives reflect broader efforts to reduce environmental impact while maintaining board durability, performance standards, and long-term product innovation.

Companies Covered in Surfboard Market

- Global Surf Industries

- Gerflor SAS

- Tarkett SA

- Forbo

- Beachbeat Surfboards

- Kiefer USA

- Bauwerk Boen Group

- EPI Group

- Channel Island Surfboards Inc.

- Horner Surfboard

- Signature Sports

- Robbins Sports Surfaces

- Aacer Flooring

- Brusurf LLC

Frequently Asked Questions

The global surfboard market is projected to reach US$ 4.1 billion in 2026, driven by rising participation and strong amateur demand accounting for 66% share in 2025.

Rising surfing participation, with 35 million global surfers and Olympics boost, drives demand.

North America leads the market with a 35% share in 2025, supported by strong U.S. surfing culture and established retail networks including specialty stores holding 34% share.

Surf tourism expansion across Asia Pacific presents strong growth potential, particularly targeting beginner and amateur surfers who represent 66% of the market.

Leading players include Global Surf Industries, Gerflor SAS, Tarkett SA, Forbo, and Beachbeat Surfboards.