- Home Care & Utilities

- Stuffed & Plush Toys Market

Stuffed & Plush Toys Market Size, Share, and Growth Forecast 2025 - 2032

Stuffed & Plush Toys Market By Product Type (Stuffed Animals, Character Plush Toys, Interactive Plush Toys, Other), by Sales Channel (Offline Retail, Online Retail), Regional Analysis, 2025 - 2032

Stuffed & Plush Toys Market Size and Trend Analysis

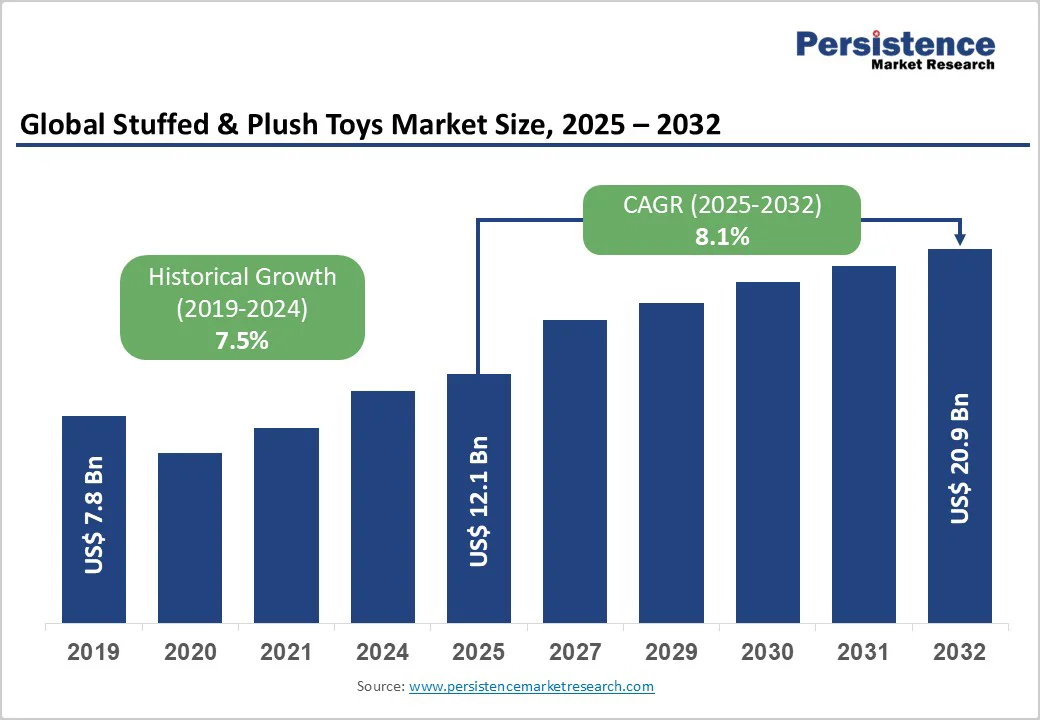

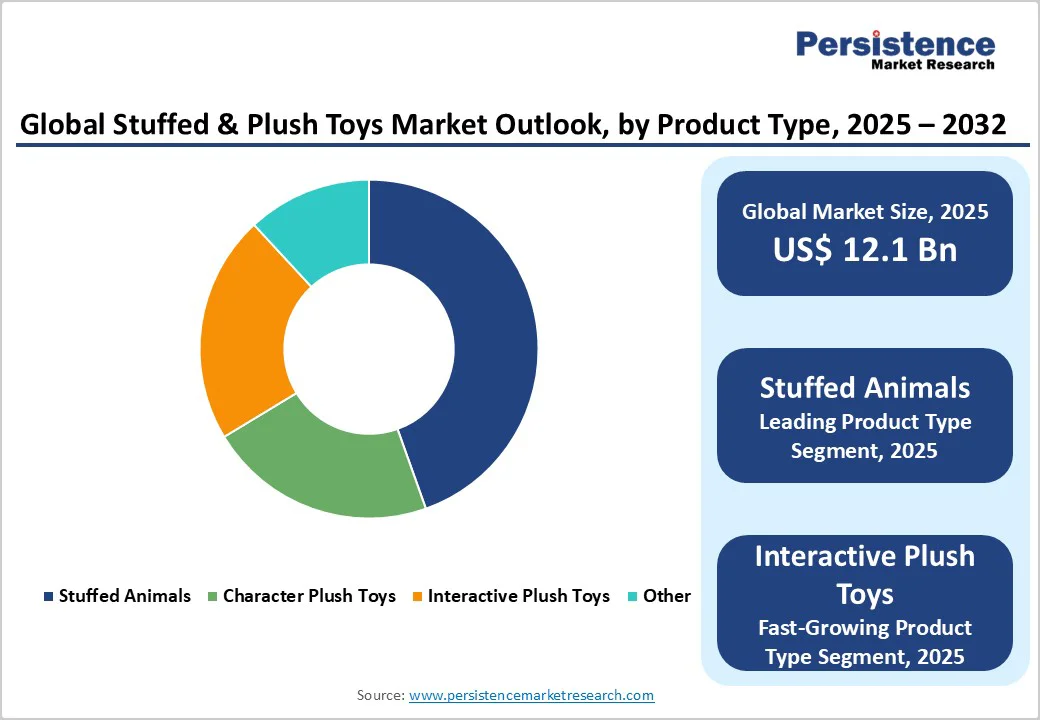

The global stuffed & plush toys market size is likely to value at US$ 12.1 billion in 2025 and is projected to reach US$ 20.9 billion by 2032, growing at a CAGR of 8.1% between 2025 and 2032.

Market expansion has been remarkable, driven by increasing emotional attachment to plush toys among all age groups, the surge in collectible character-based toys, and their therapeutic use for mental health and emotional support.

The rise of premium brands like Jellycat and Squishmallows has transformed the market from being mainly for children to encompassing adult lifestyle collectibles, with adults accounting for over 20% of plush toy sales in 2024.

Integration of technology in interactive plush toys featuring voice recognition, motion sensors, and AI-driven functions has further boosted demand and consumer engagement.

Key Market Highlights

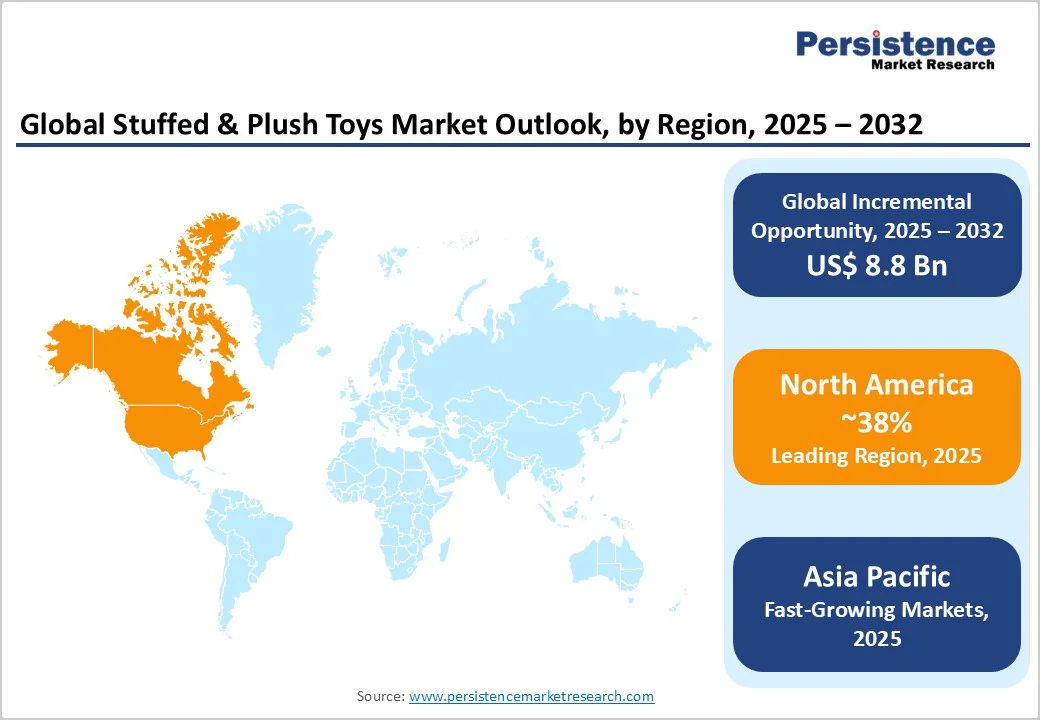

- Leading Region: North America leads the Stuffed & Plush Toys Market with a 38% share, driven by strong demand for licensed character toys, high e-commerce adoption, and robust consumer preference for collectible plush products.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with a 9.6% CAGR, fueled by rising disposable incomes, urbanization, increasing popularity of anime-themed plush toys, and rapid expansion of domestic and international toy manufacturers.

- Dominant Product Category: Stuffed Animals hold the largest market share at 41%, benefiting from their emotional, nostalgic appeal and strong demand among children and adult collectors for comforting, decorative, and collectible plush toys.

- Fastest-Growing Category: Interactive Plush Toys are the fastest-growing segment, driven by smart technology integration, such as AI, voice recognition, and motion sensors, enhancing play, educational value, and personalized consumer engagement globally.

- Key Opportunity: Eco-friendly plush toys represent a significant growth opportunity, with 68% of parents prioritizing sustainability, encouraging manufacturers to adopt recycled fibers, organic fabrics, and environmentally responsible production practices.

| Key Insights | Details |

|---|---|

| Stuffed & Plush Toys Market Size (2025E) | US$ 12.1 Bn |

| Market Value Forecast (2032F) | US$ 20.9 Bn |

| Projected Growth CAGR (2025 - 2032) | 8.1% |

| Historical Market Growth (2019 - 2024) | 7.5% |

Market Dynamics

Drivers - Proliferation of Character-Based Licensed Plush Toys Fuels Expansion

The surge in demand for licensed character plush toys representing popular franchises such as Disney, Marvel, Pokémon, and Star Wars remains a key growth driver for the market. These toys command premium pricing, foster repeat purchases, and create strong emotional connections with consumers.

For example, Squishmallows expanded to over 125 global licensees, including collaborations with McDonald’s Happy Meal in December 2023, selling over 485 million plush toys and ranking as the #2 global licensor in 2024.

Similarly, Hasbro extended multi-year licensing deals with Disney Consumer Products for Star Wars and Marvel plush toys globally. Such collaborations drive brand loyalty, seasonal sales peaks, and significant revenue growth, exemplified by Pop Mart, which reported RMB 13.04 billion in revenue for 2024, a 107% YoY increase, with 13 IPs generating over RMB 100 million each annually.

Adult Collector Market and Premiumization Boost Revenue Growth

Adults now account for over 20% of plush toy buyers, motivated by luxury, therapeutic value, and nostalgia. Premium brands such as Jellycat have recorded sales nearing £200 million, with one plush sold every 15 seconds at Selfridges. Exclusive adult-focused plushes can range from $66 to over $1,000, highlighting the premiumization trend.

The UK’s toys-for-adults market reached £2 billion, while collectible plush toys generate over $2 billion annually in the US. Surveys indicate 40% of adults sleep with stuffed animals, and 6.7% use them for anxiety relief. Manufacturers are investing in richer designs, limited editions, and exclusive collaborations, which elevate market margins and strengthen long-term consumer engagement.

Restraint - Competition from Digital Entertainment Reduces Toy Engagement

The rising popularity of video games, mobile apps, and online content is a significant restraint on the Stuffed & Plush Toys Market. Children increasingly favor digital entertainment over physical toys, and parents often face trade-offs between purchasing educational apps and tangible plush toys.

Safety concerns further impact consumer decisions, with the CPSC reporting approximately 200,000 toy-related injuries in the US in recent years. This shift in attention toward screens keeps younger consumers away from traditional plush toys, limiting overall engagement and constraining market demand despite the growth of interactive and character-based products.

Production Costs and Supply Chain Disruptions Squeeze Profits

Rising costs of polyester fills, fabrics, and labor in China which produces nearly 80% of US toys and 90% of Christmas-related goods are squeezing profit margins. Tariffs, shipping delays, and logistical complications create inventory management challenges, especially during peak seasons, with four- to five-month lead times for plush toy delivery.

Compliance with safety regulations such as ASTM F963, EN71, and CE adds $500-$1,500 per SKU, increasing production costs. Combined with intense market competition, manufacturers must carefully balance product quality, affordability, and regulatory adherence to maintain profitability and market share.

Opportunities - Eco-Friendly & Sustainable Plush Toys Driving Market Growth

Growing environmental consciousness among consumers is creating significant opportunities in the Stuffed & Plush Toys Market. Parents are increasingly seeking toys made from organic cotton, recycled polyester (rPET), and biodegradable fibers, with approximately 68% of parents prioritizing sustainability when purchasing plush products. Certifications such as GOTS, OEKO-TEX®, and other eco-labels enhance consumer trust and signal product quality.

Manufacturers are leveraging natural dyes and recycled plastic bottles for rPET fills to produce environmentally friendly plush toys. These sustainable practices not only align with consumer values but also allow brands to charge premium prices, foster long-term loyalty, and differentiate their offerings in a competitive market increasingly focused on ethical and eco-conscious products.

Interactive and AI-Enabled Plush Toys Transforming Consumer Engagement

The integration of smart technologies in plush toys presents another high-growth opportunity. AI-enabled, voice-recognition, motion-sensor, touch-responsive, and LED-featured plush toys are gaining popularity among children and adults alike. Studies indicate that AI-powered plush toys can enhance children’s cognitive recall by up to 22%, while interactive features allow products to be sold at 15-20% higher price points.

Interactive plush toys also have a growing therapeutic application. Voice-recognition and AI-enabled plushes are increasingly used to assist with anxiety, depression, and PTSD management. Innovations such as Haivivi’s ChatGPT-enabled plush toys demonstrate the dual appeal of these products for play and therapy, creating a strong potential market for both entertainment and healthcare-oriented applications.

Category-wise Insights

Product Type Analysis

Stuffed Animals are the leading product type, holding a 41% market share in 2025. Their universal appeal spans children and adults, serving purposes of play, comfort, and emotional support. Both realistic wildlife and fantasy creatures cater to gifts, collectibles, and therapeutic uses. Companies like Aurora World Inc., with 12 showrooms and distribution to over 25,000 outlets, exemplify leadership in this segment, supported by strong consumer attachment and seasonal gifting trends.

Interactive Plush Toys are the fastest-growing segment, fueled by AI, voice recognition, motion sensors, and LED features. These toys command premium prices, enhance cognitive and emotional engagement, and attract both children and adult collectors. The segment’s growth is driven by technological innovation, therapeutic applications, and increasing demand for smart, engaging play experiences.

Sales Channel Analysis

Offline Retail is the leading sales channel, capturing around 84% of plush toy sales in 2025. Supermarkets, specialty stores, gift shops, and department stores remain preferred for tactile experience, instant gratification, and personalized service. Iconic retailers like Harrods, Build-A-Bear Workshop, and Selfridges drive seasonal peaks and holiday promotions, particularly for children and gift buyers.

Online Retail is the fastest-growing channel, projected to achieve 9-10% CAGR through 2030. Platforms such as Amazon, Alibaba, and Flipkart provide variety, convenience, and exclusive editions, attracting adult collectors and premium buyers. E-commerce supports global reach, targeted marketing, and limited-edition launches, complementing offline retail while expanding overall market access.

Regional Insights

North America Stuffed & Plush Toys Market Trends

North America is the largest Stuffed and plush Toy Market, driven by strong consumer demand, advanced retail infrastructure, and sophisticated e-commerce adoption. Leading brands like Ty Inc. anchor the market with distribution in over 150 countries. Collectibles, custom plush, and anime-inspired toys are particularly popular among millennials and Gen Z, creating consistent demand across age groups.

E-commerce channels contribute a significant portion of sales, while holiday seasons such as Christmas and Valentine’s provide seasonal revenue spikes. Strict safety regulations, including CPSC and ASTM F963, alongside the growing popularity of therapeutic plush toys, expand the market boundaries and foster innovation in product offerings.

Europe Stuffed & Plush Toys Market Trends

Europe accounts for a substantial portion of global plush toy revenue, led by countries such as Germany, the UK, France, and Spain. Consumer preference is driven by quality, safety compliance (EN71, CE), and sustainability, with buyers willing to pay premiums for luxury and collectible plush items. Brands like Jellycat exemplify success in the region, leveraging pop-up experiential stores and unique product designs.

The European market benefits from regulatory harmonization and eco-friendly innovations, supporting premium product positioning. Online retail is expanding rapidly, especially for high-end and collectible toys, providing greater convenience, accessibility, and direct engagement with tech-savvy and adult collector consumers.

Asia Pacific Stuffed & Plush Toys Market Trends

Asia Pacific is the fastest-growing region, fueled by rising disposable incomes, urbanization, and growing birth rates in China, Japan, India, and ASEAN countries. China remains a major manufacturing hub, producing the majority of global plush toys, while domestic demand surges due to rising consumer interest and popular brands like Pop Mart, which achieve significant revenue growth through limited-edition collectibles.

In Japan and Korea, anime-themed plush dominates retail and online channels, while in India, government initiatives such as the Production Linked Incentive (PLI) Scheme support domestic manufacturing. The expansion of online retail platforms like Alibaba and Flipkart enhances market accessibility, allowing brands to reach both urban and rural consumers effectively.

Competitive Landscape

The global stuffed & plush toys market is moderately fragmented, with major players collectively holding around 45% of the market. Leading companies leverage licensing agreements, brand recognition, and product innovation, while numerous smaller firms focus on niche segments such as eco-friendly, custom, and limited-edition plush toys, catering to specialized consumer demands.

The market demonstrates a balance between premium and mass-market offerings. Premium brands emphasize sustainability, exclusivity, and interactive technologies to attract collectors and adult consumers, while mass-market companies provide affordable, high-volume options to reach broader audiences.

Efficient manufacturing strategies and direct-to-consumer channels further shape competition, driving innovation, seasonal promotions, and diverse product availability across the global market.

Key Market Developments:

- In March 2025, Pop Mart International Group Ltd. announced an aggressive global expansion strategy following a 188% profit surge in 2024, opening new flagship stores across North America and Europe. This expansion aims to strengthen brand presence, capture international collectors, and leverage growing demand for limited-edition and character-based plush toys.

- In May 2025, Jazwares’ Squishmallows expanded its licensing portfolio to over 125 global licensees, achieving the status of #2 Global Licensor with 485 million plush toys sold worldwide. This milestone highlights strong consumer demand, successful collaborations with popular franchises, and the brand’s growing influence in the global collectible and character-based plush toy segment.

- In April 2025, Hasbro announced a multi-year extension with Disney Consumer Products, securing global rights for Star Wars and Marvel plush toys. This strategic move strengthens Hasbro’s licensed product portfolio, ensures continued market dominance in character-based plush toys, and positions the company to benefit from franchise-driven seasonal sales peaks and collector interest.

Companies Covered in Stuffed & Plush Toys Market

- Gund

- Jellycat

- Squishmallows

- Aurora World

- Ty Inc.

- Steiff

- Pop Mart

- CustomPlush.com

- Bobo’s

- Adorable World

- HABA USA

- Cuddly Bear Plush Toys

- Shenzhen Yiwu Toys Co., Ltd.

- MS Teddy Bear

- Hansightoy

- Build-A-Bear Workshop

- Mattel Inc.

- Hasbro Inc.

- Spin Master Corp

- Kellytoy Holdings

- GIANTmicrobes

- Budsies

- Dan Dee International

- Ganz

Frequently Asked Questions

The global stuffed & plush toys market is US$ 12.1 billion in 2025, projected to reach US$ 20.9 billion by 2032 at 8.1% CAGR.

Key drivers are licensing character plush toys from Disney, Marvel, Pokémon and adult collector sales, with Squishmallows selling 485 million toys and Jellycat tripling its UK revenue.

Stuffed Animals dominate with 41% share, led by brands like Aurora World and Steiff.

North America leads with 38% share, driven by licensed character toys, high incomes, retail infrastructure, and e-commerce.

Eco-friendly plush using organic cotton, rPET, and certified materials present major growth, with 68% of parents seeking sustainable toys; interactive plush with AI and smart features also offer high growth.

Leaders include Ty Inc., Jellycat, Squishmallows, Aurora World, Steiff, Pop Mart, and Build-A-Bear Workshop.