- LED & Lighting (Optoelectronics)

- Street Lighting Market

Street Lighting Market Size, Share, and Growth Forecast, 2025 - 2032

Street Lighting Market by Product Type (Smart Street Lights, Conventional Street Lights, Hybrid Street Lights), Technology (LED, Solar, Traditional), End-use (Residential, Commercial, Industrial, Municipal), and Regional Analysis for 2025 - 2032

Street Lighting Market Size and Trends Analysis

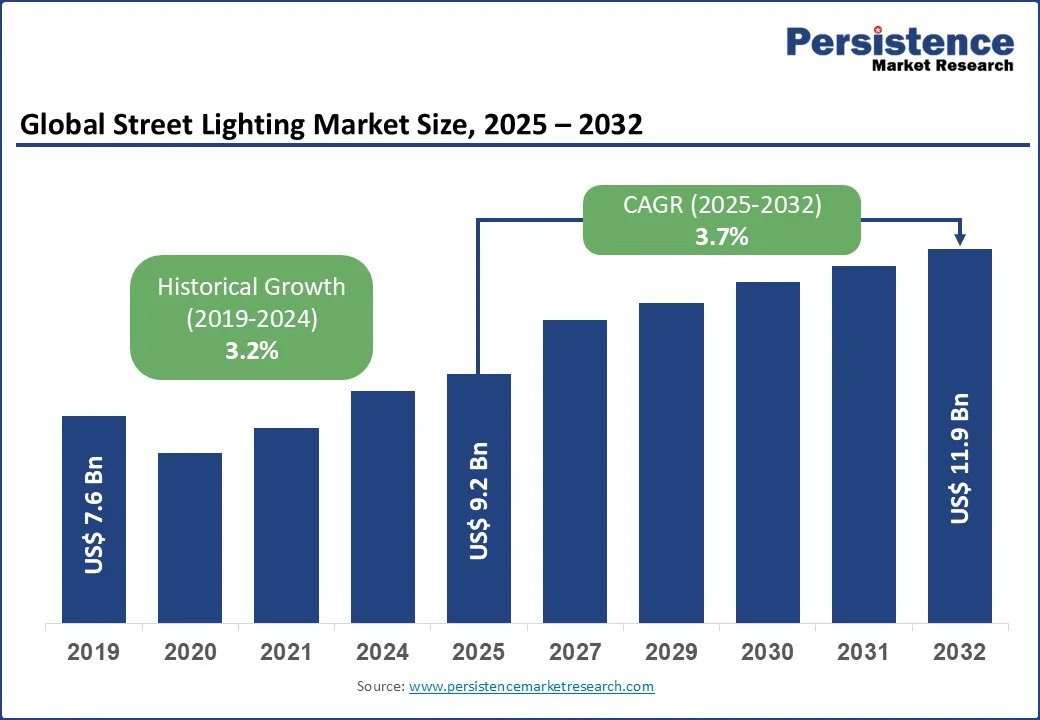

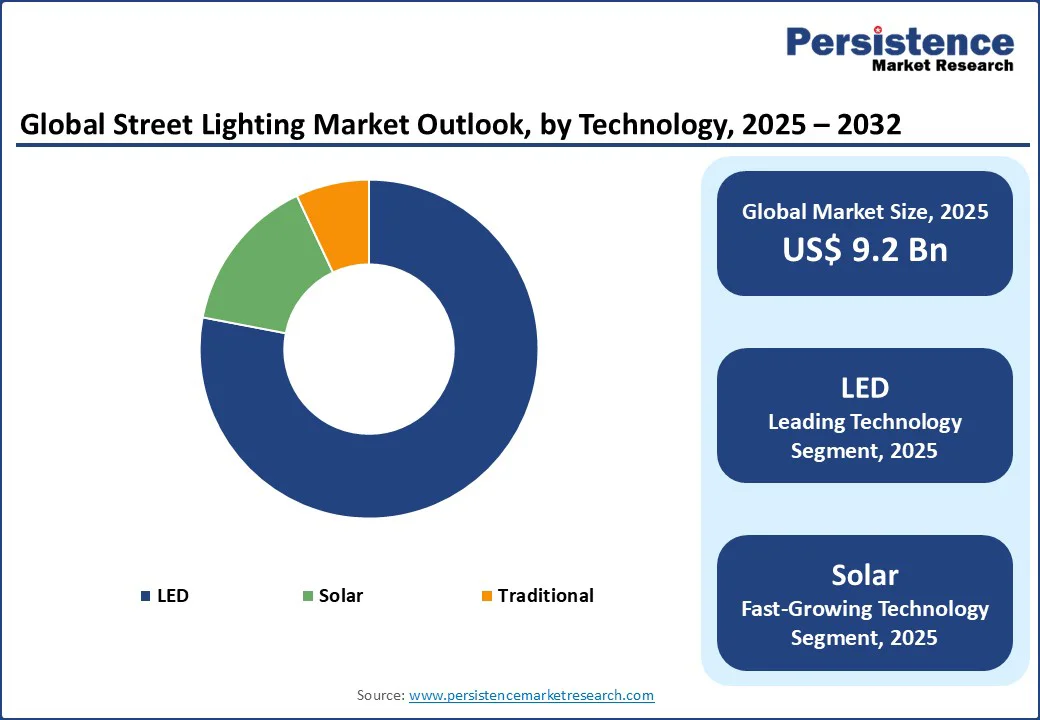

The global street lighting market is projected to grow from US$ 9.2 Bn in 2025 to US$ 11.9 Bn by 2032, registering a CAGR of 3.7% during the forecast period from 2025 to 2032.

Increasing focus on urban infrastructure development, rising energy efficiency mandates, and the pervasive influence of smart city initiatives are prevalent in shaping street lighting aesthetics.

The demand for street lighting is further fueled by innovations in energy-saving technologies, growing awareness of sustainability and public safety, and the expansion of IoT-enabled platforms in emerging economies. The industry is supported by the critical role street lighting plays in enhancing road visibility and reducing energy consumption, making it a cornerstone of the urban development and energy management sector across various applications.

Key Industry Highlights:

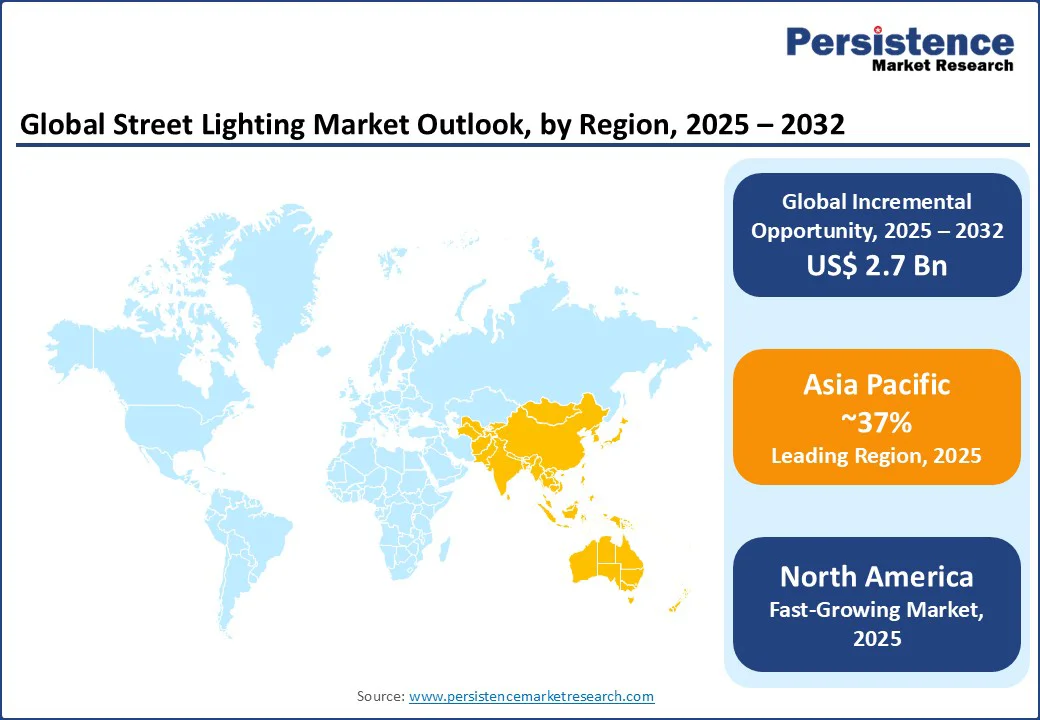

- Leading Region: Asia Pacific, holding a 37% market share in 2025, driven by rapid urbanization, smart city projects, and product innovation focused on LED and solar lighting.

- Fastest-growing Region: North America, fueled by infrastructure upgrades and adoption of smart lighting systems. Europe holds a significant share of the domain, credited to stringent energy regulations, innovative deployments, and strong government incentives.

- Dominant Product Type: Conventional Street Lights, commanding nearly 26% market share, reflecting their affordability and widespread appeal across diverse infrastructure segments.

- Leading Technology: LED, accounting for over 78% of market revenue, driven by the global demand for energy-efficient and long-lasting lighting solutions.

- Historical Growth: The sector registered a CAGR of 3.2% from 2019 to 2024, driven by increasing demand for efficient lighting products and growing access to urban development funding.

|

Global Market Attribute |

Key Insights |

|

Street Lighting Market Size (2025E) |

US$ 9.2 Bn |

|

Market Value Forecast (2032F) |

US$ 11.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.2% |

Market Dynamics

Driver - Rapid urbanization and infrastructure development

Rapid urbanization has become one of the most powerful growth drivers in the street lighting market, shaping infrastructure needs and accelerating product adoption. Cities worldwide are expanding at an unprecedented rate, with the United Nations projecting that 68% of the global population will live in urban areas by 2050, up from 55% in 2018. This surge creates a pressing demand for reliable, efficient street lighting to ensure public safety, reduce crime rates, and support economic activities after dark.

Governments and municipalities are investing heavily in road and highway expansions, where street lighting plays a vital role in preventing accidents, studies from the World Health Organization indicate that proper lighting can reduce nighttime road fatalities by up to 30%.

China's Belt and Road Initiative has incorporated advanced LED and solar street lighting in new urban corridors, enhancing visibility and energy efficiency. Moreover, private-public partnerships are leveraging data from IoT-integrated lights to optimize traffic flow and urban planning.

User feedback and real-time monitoring also allow for quick adaptations to local needs. Overall, rapid urbanization not only enhances market visibility but also transforms how governments discover, evaluate, and deploy street lighting, making it a central driver of market growth.

Restraint - High initial installation and maintenance costs

The growth of the street lighting market is hindered by the high initial installation and maintenance costs associated with advanced technologies. Governments and municipalities face budget constraints when transitioning from traditional to LED or smart systems, with upfront costs for LED fixtures being 2-3 times higher than conventional lamps, according to the International Energy Agency.

For instance, in the U.S., replacing a single street light with an LED equivalent can cost up to $500, including labor, while solar-integrated options add further expenses due to batteries and panels. Emerging markets such as those in Africa and Latin America struggle with these costs amid limited funding, often delaying projects.

Regulatory requirements for safety certifications and environmental compliance further escalate expenses, particularly for smaller vendors. While long-term savings in energy (up to 50% reduction) and maintenance (due to 50,000-hour lifespans) are evident, the immediate financial burden limits adoption.

Consumer and municipal demand for cost-effective solutions intensifies pressure on manufacturers to innovate affordable alternatives. While essential for progress, these cost demands can delay deployments, limit scalability, and restrain overall market expansion.

Opportunity - Growing adoption of smart and IoT-enabled lighting solutions

The global street lighting market is witnessing a significant opportunity with the rising adoption of smart and IoT-enabled lighting systems. These advanced solutions go beyond basic illumination by integrating sensors, connectivity, and data analytics to enhance energy efficiency, safety, and operational management.

Smart street lights can automatically adjust brightness based on traffic flow or ambient conditions, helping municipalities reduce energy consumption and lower costs. Additionally, IoT-enabled platforms provide remote monitoring and predictive maintenance, allowing authorities to detect outages, schedule repairs, and optimize overall performance in real time. This reduces downtime and improves service reliability, which is critical for urban areas aiming to enhance sustainability.

Furthermore, the integration of smart lighting into broader smart city initiatives enables additional functionalities such as surveillance, traffic management, and environmental monitoring. For instance, Barcelona has deployed over 3,000 smart street lights equipped with sensors that adjust brightness and collect environmental data, contributing to nearly 30% energy savings while supporting its broader smart city initiatives.

As governments and city planners increasingly prioritize sustainability and digital infrastructure, the demand for smart street lighting is expected to rise steadily, creating substantial growth opportunities for manufacturers and technology providers worldwide.

Category-wise Insights

Product Type Insights

Conventional street lights dominate and account for approximately 60% of share in 2025. Their dominance stems from their affordability, wide availability, and appeal to a broad infrastructure base, particularly in emerging markets.

Conventional products, such as high-pressure sodium lamps, cater to budget-sensitive municipalities while maintaining reliability, making them a preferred choice for basic deployments. Brands such as Osram and Eaton leverage economies of scale to offer cost-effective products, driving their widespread adoption.

The smart street lights segment is the fastest-growing, driven by increasing willingness to invest in IoT-integrated, energy-efficient lighting. Smart products, such as those offered by Philips and Schneider Electric, appeal to users seeking advanced features such as remote control and sensor-based dimming.

The rise of smart city initiatives showcasing connected lighting, coupled with growing infrastructure budgets in regions such as North America, is accelerating the adoption of smart products, particularly among tech-savvy urban planners.

End-use Insights

Municipal holds the largest market share, accounting for approximately 70% of revenue. Its dominance is driven by the established role in public infrastructure, including roadways and highways, where safety and visibility are paramount.

Municipalities prefer reliable systems for large-scale deployments, with government funding enhancing the experience through trials and integrations. Major players such as Acuity Brands and Zumtobel Group support this segment’s lead with tailored solutions.

Commercial is the fastest-growing segment, fueled by the rapid expansion of business districts and private developments. The convenience of energy-efficient lighting, coupled with the rise of IoT tools for cost savings, has transformed the landscape. The increasing penetration of urban commercial spaces in emerging markets, particularly in the Asia Pacific, further accelerates the adoption of commercial end-use channels.

Technology Insights

LED leads the street lighting market, holding a 78% share. The segment’s dominance is driven by the widespread demand for energy-efficient, durable solutions that are staples in modern infrastructure. The global rise in sustainability consciousness, fueled by regulations such as the EU's energy directives, has boosted the adoption of LED. Major brands such as Philips and Osram continuously innovate with high-lumen and low-power formulations, further solidifying this segment’s lead.

The solar segment is the fastest-growing, driven by the increasing popularity of renewable energy and off-grid solutions, such as integrated panels and batteries. Campaigns highlighting solar's zero-emission benefits, such as those in India's rural electrification, underscore the influence of environmental endorsements. The growing demand for sustainable solar products, coupled with rising experimentation in remote areas, is accelerating the adoption of this segment globally.

Regional Insights

North America Street Lighting Market Trends

North America holds a significant share of the street lighting market, supported by its strong infrastructure base, high investment levels, and advanced technology ecosystem. Consumers in the U.S. and Canada show a strong inclination toward energy-efficient and smart lighting products, making the region one of the most lucrative markets for international and domestic brands.

The rapid adoption of IoT platforms has transformed the landscape, with government initiatives, tech-driven campaigns, and funding channels playing a pivotal role in driving sales. Leading players are consistently launching new LED and solar formulations, adaptive controls, and hybrid systems that combine efficiency and connectivity to appeal to diverse groups.

Moreover, the growing demand for sustainable, low-emission, and IoT-enabled products is shaping brand strategies, as younger urban planners prioritize green consumption. Traditional infrastructure also remains strong, with utilities and public-private partnerships offering an integrated upgrade experience.

Overall, North America’s combination of funding power, innovation-driven loyalty, and tech engagement cements its position as a dominant and trendsetting market in the global street lighting industry.

The U.S. market trends highlight a focus on infrastructure modernization under programs such as the Infrastructure Investment and Jobs Act, allocating billions for energy-efficient upgrades. Cities such as Los Angeles have replaced thousands of lights with LEDs, achieving substantial savings, while trends toward smart systems in New York emphasize data analytics for traffic management.

Europe Street Lighting Market Trends

Driven by its emphasis on energy efficiency, high regulatory standards, and strong focus on quality and sustainability, Europe reveals a robust pattern in energy consumption. The growing adoption of LED and smart technologies has significantly boosted demand for advanced systems, such as those with motion sensors and dimming capabilities. Additionally, European stakeholders demonstrate a strong preference for eco-friendly formulations, aligning with the rising green movement and strict frameworks such as the EU's Green Deal.

This has encouraged brands to innovate with recyclable materials, low-carbon designs, and compliance claims to maintain trust. The region is also home to many leading firms, such as Osram and Zumtobel Group, which continue to lead through premium positioning and diversification.

E-infrastructure adoption has surged, with platforms playing a vital role in expanding accessibility. Combined with growing demand for connectivity and eco-conscious solutions, Europe remains a critical hub for innovation, shaping global trends in the street lighting industry.

Leading countries include Germany, with drivers such as industrial urbanization and renewable energy mandates; the UK, fueled by smart city funding and post-Brexit infrastructure pushes; and France, driven by sustainability goals and urban renewal projects.

Asia Pacific Street Lighting Market Trends

Asia Pacific is the largest and most dominant region in the global street lighting market, projected to hold around 37% market share in 2025. The growth is primarily fueled by rapid urbanization, increasing infrastructure investments, and a rapidly expanding population with growing interest in efficient and safe lighting.

The influence of smart city trends has been especially transformative, promoting innovative formats such as IoT-connected LEDs and solar hybrids infused with energy-saving benefits. Younger stakeholders are driving demand for advanced, experimental systems while also showing heightened awareness of cost and sustainability.

This has accelerated the adoption of LED and solar street lighting across the region. Digital platforms are vital in shaping decisions, as influencers and e-procurement continue to grow. Moreover, international brands are tailoring solutions to cater to diverse needs, while local players are gaining prominence through affordable offerings. With its blend of cultural influence, innovation, and scale, Asia Pacific remains the most dynamic hub for street lighting globally.

Leading countries include China, with drivers such as massive smart city initiatives and government subsidies for LEDs; India, fueled by the Street Light National Programme and rural electrification; and Japan, driven by technological advancements and disaster-resilient designs.

Competitive Landscape

The global street lighting market is characterized by intense competition, regional strengths, and a mix of global and local players. In developed regions such as North America and Europe, large firms such as Philips, Osram, and Eaton dominate through scale, advanced R&D capabilities, and established partnerships with governments and utilities.

In the Asia Pacific, rapid growth in urbanization, expanding smart city ecosystems, and rising energy demands are attracting significant investments from both international players, such as Schneider Electric and Acuity Brands, and regional leaders such as Havells in India.

Companies are focusing on technology innovation, affordability, and strategic alliances with IoT providers and municipalities to gain a competitive edge. The development of energy-efficient, hybrid LED-solar formulations and sustainable designs has emerged as a key differentiator, enabling faster market adoption and stronger loyalty. Strategic collaborations, acquisitions, and tech-first campaigns are further intensifying the competitive landscape.

Key Developments

- In April 2024, Philips (Signify) expanded its smart lighting portfolio with the launch of the Interact City IoT-enabled street light series. These advanced systems are designed to integrate seamlessly into smart city infrastructure, offering features such as remote monitoring, adaptive brightness control, and energy optimization.

- In October 2019, Eaton Lighting partnered with Telensa, a smart street lighting and smart city applications provider, to deliver connected smart city and street lighting solutions. This collaboration focused on integrating Eaton’s lighting expertise with Telensa’s wireless controls and data platforms to improve energy efficiency, connectivity, and scalability in global urban infrastructure.

Companies Covered in Street Lighting Market

- Sylvania

- LSIS

- Schneider Electric

- Philips

- Acuity Brands

- Osram

- Eaton

- Legrand

- Havells

- Honeywell

- Zumtobel Group

- Others

Frequently Asked Questions

The global Street Lighting market is projected to reach US$ 9.2 Bn in 2025.

Rapid urbanization and infrastructure development are key drivers.

The Street Lighting market is poised to witness a CAGR of 3.7% from 2025 to 2032.

The growing adoption of smart and IoT-enabled lighting solutions is a key opportunity.

Sylvania, LSIS, Schneider Electric, Philips, Acuity Brands, Osram, Eaton, Legrand, Havells, Honeywell, and Zumtobel Group are key players.