- Smart Packaging

- Strapping Devices Market

Strapping Devices Market Size, Share, and Growth Forecast, 2026 - 2033

Strapping Devices Market by Device Type (Manual Strapping Devices, Semi-Automatic Strapping Devices, Others), Application (Packaging, E-commerce, Others), End-user, Strapping Material, and Regional Analysis for 2026 - 2033

Strapping Devices Market Size and Trends Analysis

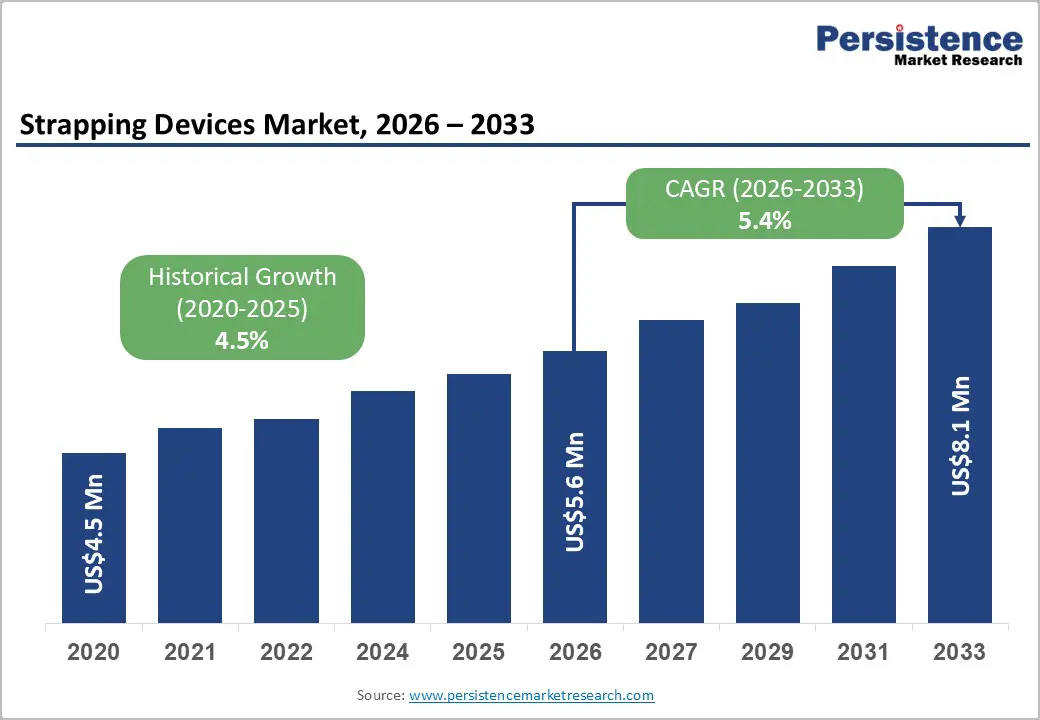

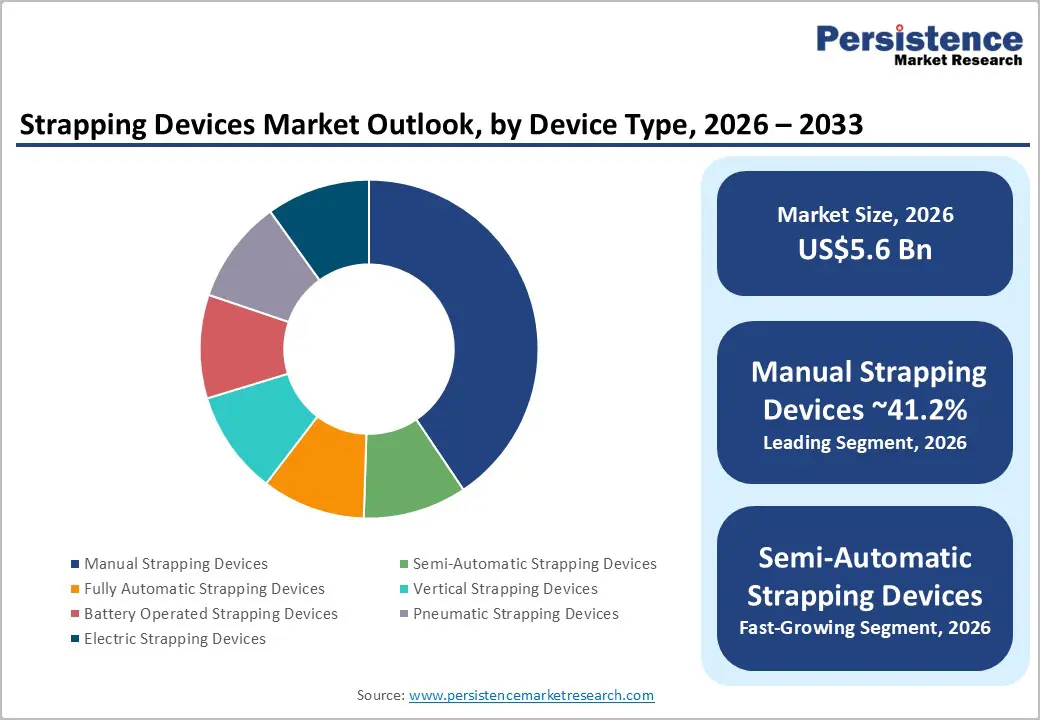

The global strapping devices market size is likely to be valued at US$ 5.6 billion in 2026 and is expected to reach US$ 8.1 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033, driven by rising packaged-goods throughput, expanding e-commerce logistics networks, and the shift toward semi-automatic and battery-operated tools that improve productivity and operator safety.

Developed markets are accelerating replacement cycles of legacy manual devices, while emerging economies continue to rely on manual and semi-automatic tools due to lower capital requirements. Sustainability considerations are encouraging greater use of recyclable PP and PET strapping, reinforcing demand for compatible devices. These combined factors create stable, structurally supported growth.

Key Industry Highlights:

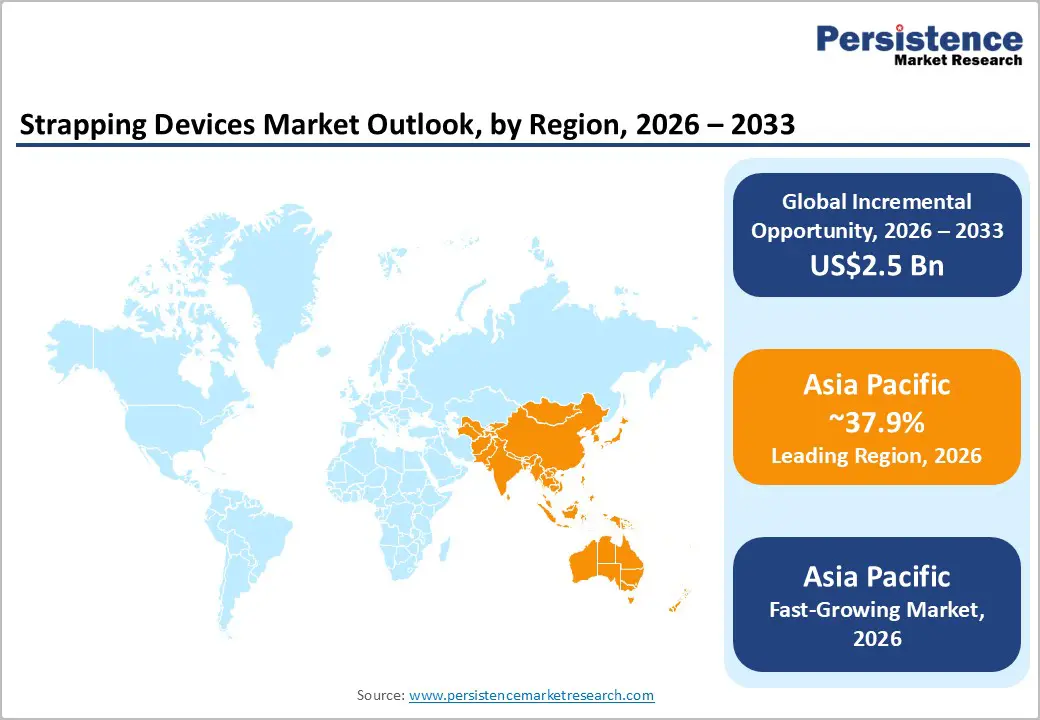

- Leading Region: Asia Pacific is projected to hold 37.9% market share, supported by large-scale manufacturing in China, automation maturity in Japan, and rapid SME upgrades in India and ASEAN economies.

- Fastest-Growing Region: Asia Pacific, driven by export-led industrialization, expanding e-commerce logistics, and increasing adoption of semi-automatic and battery-operated systems across emerging manufacturing hubs.

- Investment Plans: Focus on integrated packaging automation lines, service network expansion, and energy-efficient device platforms, particularly in North America and Europe. Leasing models and bundled maintenance agreements are gaining traction to manage capital expenditure constraints.

- Dominant Device Type: Manual strapping devices are anticipated to account for 41.2% share, maintaining leadership due to cost-effectiveness, mobility, and widespread use among SMEs and decentralized packaging operations.

- Leading Application: Packaging is anticipated to account for 45.6% share, leading the market due to high-volume pallet stabilization, bundling, and load consolidation across food and beverage, consumer goods, and industrial manufacturing sectors.

| Key Insights | Details |

|---|---|

| Strapping Devices Market Size (2026E) | US$5.6 Bn |

| Market Value Forecast (2033F) | US$8.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - E-Commerce and Logistics Volume Expansion

Rapid expansion of e-commerce and omnichannel retail models has significantly increased palletized and unitized shipments. Fulfillment centers require consistent, secure load stabilization to reduce product damage and meet tight delivery timelines. Higher parcel throughput increases demand for semi-automatic and fully automatic strapping systems that reduce cycle time and labor dependency. As logistics networks scale, investments in packaging automation grow in parallel.

Strapping devices are closely aligned with broader packaging equipment expenditure trends, supporting the forecast 5.4% CAGR through 2033. Increased system-level purchases (machine, tooling, installation, and service contracts) also elevate average selling prices and recurring revenue streams.

Automation and Ergonomic Upgrades

Manufacturers and third-party logistics providers are progressively replacing manual tensioners with battery-operated, semi-automatic, and fully automatic devices. These systems improve throughput, enhance sealing consistency, and reduce repetitive strain injuries among operators. Modern strapping devices incorporate programmable tension controls, battery management systems, and optional digital monitoring features. These capabilities improve process reliability and reduce operational downtime.

In developed markets with higher labor costs, automation provides a measurable return on investment, accelerating technology adoption. In Asia Pacific, high-volume manufacturing environments are driving similar transitions toward semi-automatic and automated solutions.

Shift toward Polymer-Based Strapping Materials

A gradual substitution of steel strapping with polypropylene (PP) and polyester (PET) in many industries supports demand for compatible strapping devices. Polymer straps offer corrosion resistance, lower handling risks, and cost advantages in non-heavy industrial applications. As end-users transition materials, they often require updated tensioning and sealing mechanisms optimized for PP or PET. This transition stimulates equipment replacement and technological upgrades. The growth of PET as a higher-strength alternative to steel in industrial packaging further expands device innovation opportunities.

Barrier Analysis - Capital Intensity of Fully Automated Systems

Fully automatic strapping systems require substantial upfront investment and integration with conveyor infrastructure. Small and medium-sized enterprises, particularly in emerging markets, may lack the capital expenditure capacity to adopt high-throughput automation. Adoption of fully automatic systems is typically justified in facilities processing more than 3,000 packages per day. This threshold limits the addressable market for premium automation solutions and slows penetration in lower-volume operations.

Raw Material and Supply Chain Volatility

Fluctuations in polypropylene, polyester, and steel prices affect overall packaging costs. When strap prices rise significantly, companies may postpone equipment upgrades and focus on operational efficiencies instead. Commodity price cycles historically produce short-term demand fluctuations in strapping devices. Although long-term growth remains intact, quarterly sales may experience moderate volatility linked to raw material pricing dynamics and broader macroeconomic conditions.

Opportunity Analysis - Aftermarket Services and Subscription Models

As devices become more technologically advanced, aftermarket services, including maintenance contracts, consumables supply, battery replacements, and extended warranties, generate recurring revenue streams. Bundling equipment with strap supply agreements and predictive maintenance services increases customer lifetime value. IoT-enabled monitoring and remote diagnostics provide further differentiation and strengthen long-term client relationships.

Emerging Market Industrialization and SME Upgrades

Manufacturing expansion across Southeast Asia, India, and parts of Latin America creates upgrade opportunities from manual tools to semi-automatic devices. These solutions deliver productivity improvements without requiring high capital expenditure. Financing models such as leasing, installment-based procurement, and equipment-as-a-service structures can accelerate penetration in price-sensitive markets. Government-supported industrial development programs also stimulate packaging equipment demand.

PET-Optimized and Sustainability-Focused Innovation

Devices engineered specifically for PET strapping, capable of higher tension and advanced friction welding, offer measurable performance advantages. Innovations that reduce strap waste, simplify reel changes, or improve recyclability management provide tangible total cost of ownership benefits. Suppliers that integrate sustainability metrics into device design can strengthen competitive positioning in environmentally regulated markets.

Category-wise Analysis

Device Type Insights

Manual strapping devices are anticipated to account for 41.2% of the market share in 2026, maintaining their position as the largest segment by volume. Their continued dominance reflects affordability, ease of use, minimal maintenance requirements, and suitability for decentralized packaging operations. These devices are widely deployed among small and medium-sized manufacturers, agricultural packers, construction material distributors, and regional warehouses where capital expenditure constraints limit large-scale automation investments.

Manual tools remain particularly prevalent in emerging markets across Asia Pacific, Latin America, and parts of Eastern Europe, where labor costs are comparatively lower, and production volumes vary seasonally.

For example, small-scale corrugated box manufacturers and agricultural exporters frequently rely on manual tensioners and sealers for pallet stabilization without conveyor integration. The large installed base ensures steady replacement demand for wear components, seals, and rechargeable battery units, particularly for hybrid manual-battery tools. While automation penetration is rising, manual devices retain essential utility for mobile applications, on-site strapping in construction, emergency repairs in logistics hubs, and low-volume production lines where automation does not provide sufficient ROI. Their cost-effectiveness and operational flexibility ensure long-term structural relevance within the market.

Semi-automatic strapping devices represent the fastest-growing segment within the device type category, supported by increasing mid-tier industrial automation adoption. These machines offer enhanced throughput compared to manual systems while maintaining moderate capital investment levels relative to fully automated lines. Semi-automatic devices provide programmable tension control, improved seal consistency, and compatibility with both polypropylene (PP) and polyester (PET) straps.

This flexibility makes them particularly attractive for mid-sized manufacturing facilities, third-party logistics providers, and regional distribution centers seeking productivity improvements without extensive infrastructure upgrades. For example, electronics assembly plants and FMCG distribution hubs increasingly deploy tabletop or stand-alone semi-automatic machines to standardize pallet loads and reduce operator fatigue. Their growth is closely aligned with rising labor cost pressures in North America and Europe and productivity mandates in Asia Pacific export facilities. These systems enable cycle-time improvements while preserving operational control, making them a transitional technology between manual handling and fully automated packaging lines.

Application Insights

Packaging applications are anticipated to account for 45.6% of the market share in 2026, making it the dominant application segment. Pallet stabilization, carton bundling, corrugated packaging reinforcement, and load consolidation across food and beverage, consumer goods, pharmaceuticals, and industrial manufacturing underpin this leadership position. High-volume packaging lines require consistent tension control and secure sealing to minimize freight damage, reduce product returns, and ensure regulatory compliance.

For example, beverage bottling facilities utilize automated or semi-automatic strapping devices to secure shrink-wrapped pallets before transportation, while pharmaceutical manufacturers apply precision tension settings to prevent carton deformation during international shipments. Automation investments in packaging infrastructure, particularly in facilities implementing Industry 4.0 principles, support stable device demand. Load integrity and seal consistency directly influence operational efficiency and insurance costs, reinforcing strapping devices as a critical component of end-of-line packaging systems.

E-commerce represents the fastest-growing application segment within the strapping devices market, driven by rising global parcel volumes, cross-border trade expansion, and omnichannel retail models. Rapid fulfillment cycles and return logistics increase the need for secure packaging solutions capable of maintaining load integrity across multiple transit points. Large fulfillment centers and third-party logistics providers prioritize speed, ergonomic efficiency, and reduced operator fatigue. This has accelerated the adoption of semi-automatic and battery-powered strapping devices in major logistics hubs across the U.S., Germany, China, and India.

For instance, regional fulfillment warehouses serving major online retailers deploy mobile battery-operated tools to strap outbound palletized shipments efficiently during peak seasonal demand. The growth of cross-border e-commerce, particularly in Asia Pacific export corridors, further strengthens demand for durable strapping compatible with long-distance maritime and air freight. As order volumes continue to expand, strapping devices will remain integral to maintaining supply chain reliability, minimizing product damage, and optimizing warehouse throughput efficiency.

Regional Insights

North America Strapping Devices Market Trends - Automation Upgrades and Safety-Driven Premium Demand

North America represents a mature yet technologically advanced segment of thestrapping devices market, characterized by high automation penetration and strong aftermarket revenue streams. The region accounts for a significant share of global revenues due to higher average selling prices (ASPs) for semi-automatic and fully automatic systems. The U.S. leads regional demand, supported by its extensive warehousing infrastructure and large-scale logistics ecosystem.

According to the U.S. Census Bureau and the Bureau of Transportation Statistics, U.S. e-commerce sales continue to account for over 15% of total retail sales, sustaining long-term packaging equipment demand. Canada contributes stable growth through export-driven manufacturing sectors, particularly in food processing, forestry products, and industrial goods. Technology-driven upgrades define regional expansion.

Companies such as Signode Industrial Group and PAC Strapping Products have expanded their battery-powered and fully automatic strapping portfolios to meet growing ergonomics and safety compliance requirements. In 2024-2025, several North American packaging integrators increased investments in integrated end-of-line automation systems, combining stretch wrapping, palletizing, and strapping within single control platforms. This integration trend aligns with Industry 4.0 adoption across distribution centers operated by major retailers and third-party logistics providers.

Workplace safety standards enforced by the Occupational Safety and Health Administration (OSHA) indirectly influence equipment upgrades. Employers increasingly replace fully manual tensioning tools with battery-operated or semi-automatic devices to reduce repetitive strain injuries and musculoskeletal risks. These ergonomic considerations directly support premium product demand. Investment patterns also reflect financial innovation. Leasing and equipment-as-a-service (EaaS) models are gaining traction among mid-sized manufacturers seeking to mitigate capital expenditure constraints amid fluctuating interest rates.

Companies such as FROMM Packaging Systems have strengthened North American service networks to provide bundled maintenance agreements, reinforcing recurring revenue streams. Overall, North America’s growth is steady rather than explosive, driven by automation upgrades, safety compliance, and digital integration across logistics hubs.

Europe Strapping Devices Market Trends - Regulatory Harmonization and High-Precision Industrial Automation

Europe maintains a structurally strong demand for strapping devices, supported by advanced manufacturing capacity, regulatory harmonization, and high automation density. Germany leads regional consumption due to its industrial base spanning automotive, machinery, and export-oriented manufacturing. The presence of leading automation suppliers such as Mosca GmbH strengthens domestic innovation capacity. German automotive manufacturers rely on fully automated strapping systems integrated within robotic palletizing lines, reinforcing demand for high-tension, precision-controlled equipment.

The U.K. demonstrates rising demand linked to logistics restructuring and post-Brexit supply chain realignment. Increased warehousing capacity and cross-border documentation requirements have intensified packaging security needs. France and Spain maintain balanced adoption patterns, with manual and semi-automatic devices widely used among SMEs in food processing and agricultural exports.

European regulatory frameworks strongly influence procurement decisions. CE marking requirements and EU Machinery Directive compliance standards ensure safety and interoperability across member states. Sustainability mandates under the European Green Deal encourage the adoption of energy-efficient devices and recyclable strapping materials. Companies such as StraPack Corp. and Signode Industrial Group have expanded European operations to deliver PET-compatible and low-energy-consumption platforms aligned with environmental targets.

In 2024, several European manufacturers accelerated investments in digital monitoring systems that enable predictive maintenance for strapping lines, reducing downtime in high-volume facilities. Industry 4.0 initiatives across Germany and Northern Europe continue to integrate sensors and programmable logic controllers (PLCs) into packaging equipment. These technological upgrades, combined with harmonized safety regulations, support stable regional expansion while reinforcing Europe’s position as a quality-driven and compliance-focused market.

Asia Pacific Strapping Devices Market Trends - Manufacturing Scale and SME Modernization Fuel Fastest Growth

Asia Pacific is the leading region in the market, commanding approximately 37.9% of the market share. The region also represents the fastest-growing market, supported by rapid industrialization, export-driven production, and accelerating e-commerce penetration. Manufacturing relocation trends and cost-competitive equipment production further strengthen regional dominance. China accounts for the largest share within Asia Pacific due to its manufacturing scale and domestic consumption growth.

According to China’s National Bureau of Statistics, industrial production and parcel delivery volumes continue to expand, reinforcing packaging equipment demand. Domestic equipment manufacturers such as Youngsun Intelligent Equipment Co., Ltd. have increased exports of automatic strapping systems across Southeast Asia and Latin America, enhancing China’s role as both a production and innovation hub.

India represents one of the fastest-growing national markets, supported by SME modernization programs and government-backed manufacturing initiatives. Under the “Make in India” framework, packaging equipment investments have increased in pharmaceuticals, FMCG, and automotive supply chains. Semi-automatic and battery-operated devices are particularly popular among mid-sized enterprises upgrading from manual systems. ASEAN countries, including Vietnam, Thailand, and Indonesia, are emerging growth hubs as global manufacturers diversify supply chains beyond China.

Increased foreign direct investment (FDI) into electronics and consumer goods manufacturing drives packaging line expansion. Regional logistics growth, supported by port modernization and cross-border trade agreements, sustains strapping equipment demand. Service network expansion remains critical. International players such as FROMM Packaging Systems and Mosca GmbH have strengthened distribution and technical service partnerships across Asia Pacific to support automation projects. Overall, Asia Pacific’s leadership stems from manufacturing scale, logistics expansion, and cost-efficient device production, positioning the region as the central growth engine for the market.

Competitive Landscape

The global strapping devices market is moderately consolidated at the global automation tier while remaining fragmented in manual and semi-automatic categories. Leading suppliers dominate high-end automated systems and integrated packaging lines, while numerous regional manufacturers compete in handheld and entry-level equipment. Competitive positioning depends on product reliability, service coverage, and consumables integration. Leading players focus on product innovation, service bundling, and geographic expansion. Integration of consumables supply with equipment sales strengthens recurring revenue. Competitive differentiation centers on reliability, ergonomics, and lifecycle support rather than solely price competition.

Key Industry Developments:

- In May 2025, OMS Group showcased its new 08L automated strapping machine with robotic integration at Ligna-2025, advancing smart packaging automation in the wood products industry by improving packaging speed and worker safety.

Companies Covered in Strapping Devices Market

- Signode Industrial Group

- FROMM Packaging Systems

- Mosca GmbH

- StraPack Corp.

- Dynaric Inc.

- Transpak Equipment Corp.

- PAC Strapping Products

- TITAN Umreifungstechnik GmbH & Co. KG

- Polychem Corporation

- Samuel Strapping Systems

- Youngsun Intelligent Equipment Co., Ltd.

- Messersì Packaging S.r.l.

- Itipack S.r.l.

- Linder GmbH

- Phoenix Strapping

- Cyklop International

- Teufelberger Holding AG

- Baosteel Packaging Co., Ltd.

Frequently Asked Questions

The global strapping devices market size is projected to be valued at US$5.6 billion in 2026.

The strapping devices market is expected to reach approximately US$8.1 billion by 2033.

Key trends include increasing adoption of semi-automatic and battery-operated devices, integration with automated packaging lines, rising demand from e-commerce fulfillment centers, a sustainability-driven shift toward PET strapping compatibility, and the growth of leasing/service-based equipment models.

Manual strapping devices lead the strapping devices market, accounting for an anticipated 41.2% share in 2026, supported by affordability, mobility, and widespread SME adoption.

The strapping devices market is projected to grow at a CAGR of 5.4% between 2026 and 2033.

Major players include Signode Industrial Group, FROMM Packaging Systems, Mosca GmbH, StraPack Corp., and Cyklop International.