- Smart Packaging

- Stand-up Zipper Pouches Market

Stand-up Zipper Pouches Market Size, Share, and Growth Forecast, 2026 - 2033

Stand-up Zipper Pouches Market by Pouch Type (Bottom Gusset, Spout Pouch, Others), Material Type (Plastic, Paper, Others), Application, and Regional Analysis for 2026 - 2033

Stand-up Zipper Pouches Market Size and Trends Analysis

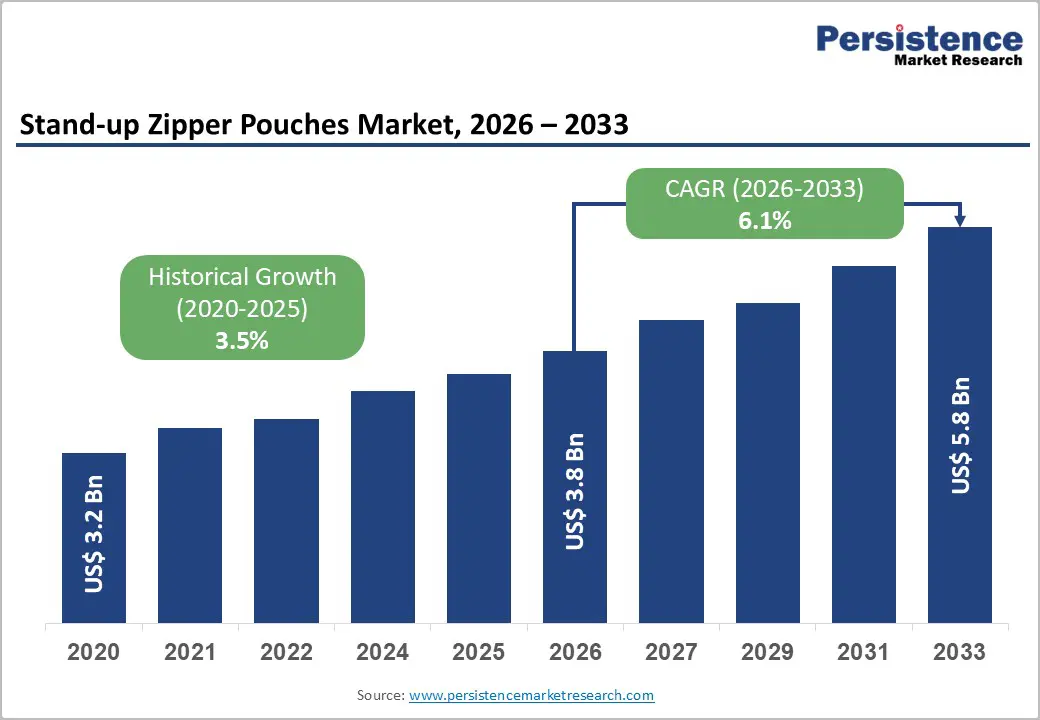

The global stand-up zipper pouches market size is likely to be valued at US$3.8 billion in 2026 and is expected to reach US$5.8 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033, driven by the ongoing shift from rigid to flexible packaging formats, alongside increased investment in recyclable and paper-based pouch technologies.

This expansion reflects broader structural changes toward lightweight, resealable, and convenience-focused packaging solutions, particularly across food & beverage and personal care sectors. Rising consumer demand for resealability, coupled with improved efficiency in e-commerce logistics, continues to support volume growth, even as pricing pressures weigh on per-unit margins.

Key Industry Highlights:

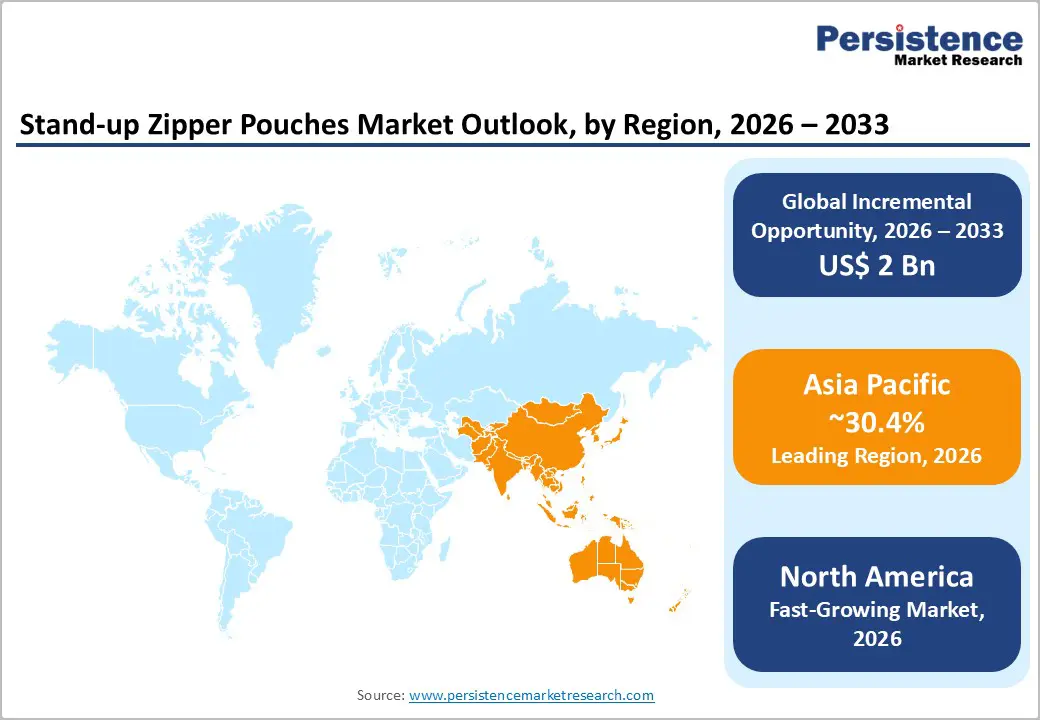

- Leading Region: Asia Pacific is projected to lead the market with 30.4% market share, supported by large-scale manufacturing hubs in China and India, expanding packaged food demand, and cost-competitive converting capacity.

- Fastest-growing Region: North America is projected to record the highest CAGR through 2033, driven by premium pouch adoption, refill initiatives, EPR-driven material innovation, and consolidation-led scale efficiencies among major converters.

- Investment Plans: Leading converters are accelerating capital deployment into mono-material recyclable laminates, paper-based pouch technologies, digital printing lines, and advanced spout insertion systems, alongside M&A activity such as large-scale acquisitions strengthening R&D and production footprint.

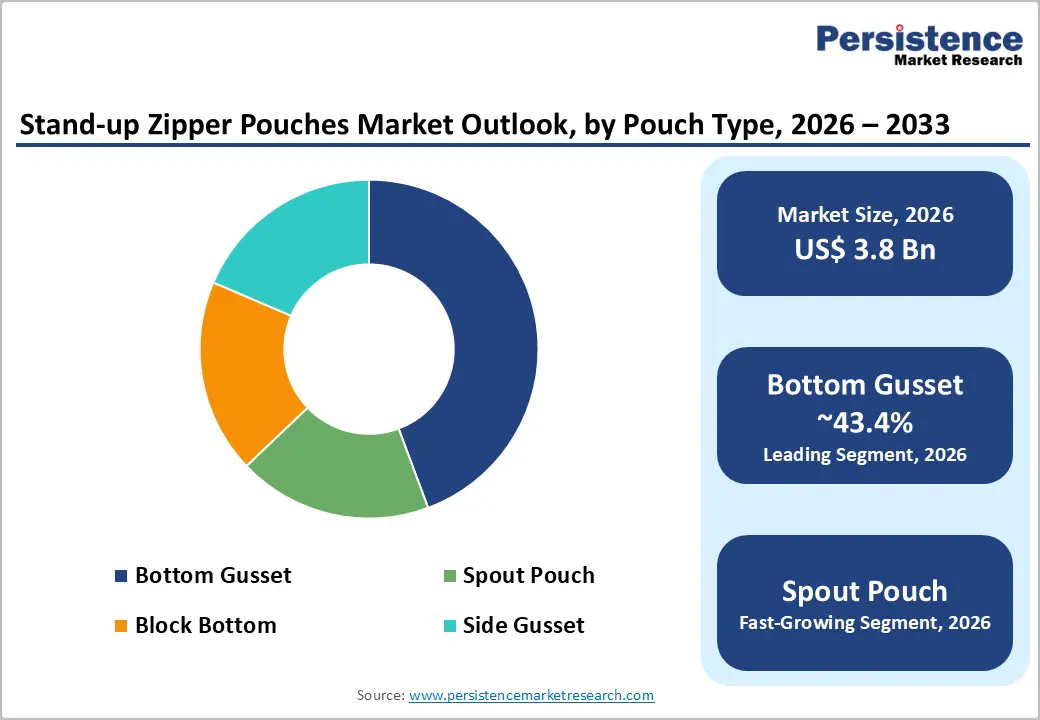

- Dominant Pouch Type: Bottom gusset stand-up zipper pouches are anticipated to account for 43.4% market share, due to shelf stability and strong retail merchandising advantages.

- Leading Material Type: Plastic laminates are estimated to hold approximately 61.3% market share, maintaining dominance through superior barrier performance, cost efficiency, and compatibility with high-speed converting operations.

| Key Insights | Details |

|---|---|

| Stand-up Zipper Pouches Market Size (2026E) | US$3.8 Bn |

| Market Value Forecast (2033F) | US$5.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Convenience and E-commerce Expansion

The rapid growth of online grocery, direct-to-consumer brands, and omnichannel retail models has accelerated demand for lightweight, resealable packaging formats. Stand-up zipper pouches reduce transportation weight relative to rigid containers, thereby improving freight economics and warehouse efficiency. In addition, resealability enhances product freshness and reduces waste, aligning with consumer expectations for convenience. Brands are increasingly converting stock-keeping units in snacks, pet food, powdered beverages, and specialty foods into pouch formats. This transition increases SKU complexity and short-run production requirements, strengthening demand for digital printing, flexible lamination systems, and zipper-insertion technology. The format’s structural stability and shelf presence also improve retail merchandising performance, further reinforcing adoption across grocery and club store channels.

Sustainability, Innovation, and Recyclable Formats

Environmental regulation and corporate ESG commitments are reshaping material selection in flexible packaging. Manufacturers are investing in recyclable mono-material laminates and paper-based barrier structures designed to improve end-of-life outcomes. Stand-up zipper pouches are increasingly being reformulated to meet recyclability standards in markets with established collection systems. Recyclable formats command premium prices relative to conventional multilayer laminates, thereby raising average selling prices in developed markets. Brands adopting certified recyclable pouches improve compliance with extended producer responsibility frameworks and retailer sustainability mandates. Adoption is strongest in regions where regulatory pressure and consumer awareness converge. As a result, converters capable of running recyclable or fiber-based laminates at scale are strengthening their competitive positioning and securing long-term supply agreements.

Advances in Material Science and Format Diversification

Ongoing innovation in lamination, barrier coatings, and sealing technology has expanded the functional scope of stand-up zipper pouches. Water-based coatings, metal-free barrier films, and bio-based polymers allow improved moisture and oxygen protection while reducing environmental impact. Advances in zipper insertion and spout welding equipment have reduced defect rates and improved cost efficiency. These improvements enable pouch penetration into higher-barrier and liquid applications, including sauces, detergents, and refill products. Larger multi-liter spouted pouches are replacing rigid containers in selected homecare and beverage categories. Converters investing in high-speed sealing, advanced web handling, and fitment integration are capturing higher-margin segments, while legacy producers without modernization face a competitive disadvantage.

Barrier Analysis - Recycling Infrastructure and Regulatory Fragmentation

Adoption of recyclable and paper-based zipper pouches depends heavily on regional waste collection and sorting infrastructure. In markets with underdeveloped recycling systems, recovery rates for flexible materials remain limited. This restricts large-scale brand conversion despite technical recyclability. Regulatory fragmentation across states and countries increases compliance complexity. Extended producer responsibility rules, labeling requirements, and restrictions on specific chemical additives raise operational costs. Markets lacking mature recycling ecosystems may experience adoption rates for recyclable pouch formats that are 30 to 50% slower than infrastructure-ready regions.

Cost and Conversion Challenges

Recyclable mono-material laminates and advanced barrier papers often carry higher raw material and tooling costs than legacy multi-layer plastics. Equipment upgrades for sealing and lamination also require capital expenditure. Small and mid-sized brands may face minimum order quantities that limit experimentation. In price-sensitive markets, increased packaging costs can delay format conversion until economies of scale reduce price differentials. These cost barriers compress margins during early adoption phases and extend payback periods for converters investing in new technology platforms.

Opportunity Analysis - Premiumization and Value-Added Fitments

Premium stand-up zipper pouches incorporating high-definition printing, matte finishes, enhanced barrier layers, and spouted fitments create incremental value over standard commodity formats. In developed markets, premium configurations can generate approximately 12 to 18% higher revenue per unit. Brands in the specialty food, organic products, and private-label segments are willing to pay for differentiated shelf presentation. Converters offering integrated design services, short-run digital printing, and rapid turnaround gain a competitive advantage. Premiumization enhances profitability and strengthens brand-converter partnerships.

Refillable and Concentrated Formats

Refillable spouted stand-up pouches for detergents, beverages, and personal care products reduce plastic use relative to rigid containers. Concentrated liquid formats enable smaller packaging footprints and support subscription models. Refill-oriented initiatives may capture 2 to 4% of total pouch volumes over the next five years in early-adopter markets. Technical priorities include puncture resistance, spout integrity, and consumer-friendly dispensing systems. Partnerships between retailers, brands, and converters accelerate pilot programs and scale adoption.

Emerging Markets and Localized Converting

Southeast Asia, India, and Latin America present high-growth opportunities driven by urbanization, demand for packaged food, and the expansion of modern retail networks. Converters that localize production and tailor pouch sizes to regional purchasing power can achieve unit growth rates of 20 to 30% annually in targeted segments. Investment in regional converting capacity, digital printing, and local film sourcing reduces lead times and logistics costs. Localization strengthens relationships with regional private label brands and multinational manufacturers seeking cost-efficient supply chains.

Category-wise Analysis

Pouch Type Insights

Bottom gusset stand-up zipper pouches are expected to retain a leading position, accounting for approximately 43.4% of market share in 2026. Their superior structural stability, strong shelf presence, and expansive printable surface area make them well-suited for snacks, pet food, coffee, powdered beverages, and bulk dry goods. Food brands and private-label producers favor bottom gusset formats for mid-shelf retail placement due to consistent upright performance and support for high-impact graphics. Ongoing investments in tooling upgrades and high-speed production lines further strengthen economies of scale and cost efficiency. In addition, bottom gusset designs accommodate high-barrier laminates required for oxygen- and moisture-sensitive products such as roasted coffee and pet treats. Club-store multipacks and value-size SKUs also prefer this format for its durability in transport and enhanced shelf visibility, reinforcing the segment’s dominant share.

Spouted stand-up zipper pouches are the fastest-growing format, driven by rising adoption in liquid and semi-liquid applications such as beverages, sauces, baby food, detergents, and refill concentrates. Integrated spouts improve dispensing control and resealability while reducing dependence on rigid plastic packaging, aligning with convenience and material-reduction objectives. Large-format spouted pouches (1-2 liters) are gaining momentum in homecare and concentrated beverage categories, particularly as detergent and fabric softener refills replace traditional HDPE bottles. Smaller spouted pouches are also increasingly used for baby food and smoothies, supporting portability and portion control. Converters investing in advanced spout insertion, ultrasonic welding, and leak-resistance technologies are capturing higher-margin opportunities as brands shift toward refill-driven and subscription-based distribution models.

Material Type Insights

Plastic laminates are anticipated to retain leadership, holding approximately 61.3% of market share over the forecast period. Multi-layer film structures combining PET, PE, and BOPP deliver strong moisture, oxygen, and aroma barrier properties at competitive cost points. These laminates are compatible with high-speed vertical and horizontal form-fill-seal equipment, reinforcing operational efficiency for large-scale food manufacturers. Plastic remains particularly dominant in high-volume food and beverage applications such as snack foods, pet food, frozen ingredients, and powdered drink mixes, where shelf life and cost control are primary considerations. Established film producers leverage vertically integrated supply chains and continuous barrier enhancements, including metallized films and EVOH layers, to maintain performance advantages. The material’s proven reliability and processing efficiency continue to underpin its substantial market share.

Paper-based zipper pouches are projected to be the fastest-growing material segment, supported by accelerating sustainability commitments and regulatory momentum. Brands focused on improving recyclability and reducing carbon footprints are actively piloting fiber-based and mono-material paper laminates. Advances in water-based coatings and dispersion barrier technologies now enable improved grease, moisture, and oxygen resistance for dry foods, confectionery, and certain semi-moist applications. Adoption is strongest in regions with established recycling infrastructure and retailer sustainability mandates. For example, premium coffee roasters and organic snack brands increasingly adopt paper-based stand-up zipper pouches to reinforce natural positioning and environmentally responsible branding. Retailers promoting recyclable packaging targets encourage suppliers to shift toward certified paper-based formats. The aesthetic appeal of paper, combined with enhanced technical performance, positions this segment for sustained above-average growth over the forecast horizon.

Regional Insights

North America Stand-up Zipper Pouches Market Trends-Sustainability-Led Innovation and Premium Brand Adoption

North America is expected to be the fastest-growing region, underpinned by advanced retail infrastructure, a strong consumer packaged goods (CPG) ecosystem, and high per-capita packaged food consumption. The U.S. leads regional demand, with premium resealable pouches widely adopted across snacks, pet food, coffee, and homecare applications. Major brand owners, including PepsiCo, Kraft Heinz, General Mills, and Mars Petcare, continue to expand flexible pouch formats to improve shelf efficiency, enhance branding, and reduce transportation and logistics costs. Growth in private label programs at leading retailers such as Walmart, Costco, and Kroger further supports sustained volume demand for zipper pouch packaging.

Regulatory developments are increasingly shaping material selection and package design. Extended producer responsibility (EPR) legislation enacted in states such as California, Colorado, and Maine is accelerating the shift toward recyclable and mono-material pouch structures. Canada is advancing similar producer responsibility frameworks at the provincial level, reinforcing regional momentum. These policies are driving reformulation strategies and speeding the commercialization of recyclable polyethylene-based zipper pouches, as well as emerging fiber-based alternatives. Industry associations and major converters are collaborating with retailers on store drop-off programs and film recycling initiatives to improve circularity.

North America’s innovation ecosystem enables rapid scaling of sustainable packaging formats. Amcor’s commercialization of its AmFiber™ paper-based pouch portfolio has supported trials in dry beverage and snack applications, while ProAmpac’s recycle-ready PE laminates are gaining traction with food and pet care brands aligned with retailer sustainability goals. ePac Flexible Packaging continues to expand digitally printed pouch facilities, supporting short-run and direct-to-consumer brands. Investments in digital printing, mono-material laminates, and advanced spout insertion technologies are modernizing converting capacity. The completion of Amcor’s combination with Berry Global in 2025 further strengthened scale efficiencies, material science capabilities, and regional manufacturing reach, reinforcing North America’s position as the fastest-growing market during the forecast period.

Europe Stand-up Zipper Pouches Market Trends - Regulation-Driven Shift to Recyclable and Fiber-Based Pouches

Europe is defined by regulatory harmonization, strong environmental enforcement, and retailer-driven sustainability standards. Germany, the United Kingdom, France, and Spain represent core markets with high packaged food consumption and well-established flexible packaging infrastructure. European consumers demonstrate a strong preference for recyclable and fiber-based solutions, influencing purchasing behavior and brand positioning strategies. Retailers such as Tesco, Carrefour, Aldi, and Lidl enforce strict packaging guidelines aligned with European Union circular economy objectives. These requirements accelerate the shift toward mono-material polyethylene laminates and paper-based stand-up zipper pouches. Mondi has expanded its recyclable paper-based flexible packaging portfolio across European markets, supplying dry food and confectionery brands transitioning away from multi-layer plastics. Similarly, Amcor has launched recycle-ready pouch solutions certified under European fiber-based recycling streams, enabling broader retail acceptance.

Regulatory frameworks, including extended producer responsibility schemes and packaging waste directives, incentivize material innovation while raising compliance standards. France’s Anti-Waste Law and Germany’s Packaging Act impose reporting and recyclability obligations that directly influence material design decisions. As a result, converters are investing heavily in testing, certification, and barrier coating development to ensure compatibility with national recycling systems. Paper-based stand-up zipper pouches and certified mono-material laminates continue gaining traction as brands align with environmental commitments.

For example, European coffee roasters and organic snack brands increasingly adopt paper-based zipper pouches to enhance sustainability credentials while maintaining premium shelf presence. Investment in sustainable materials research and cross-industry collaborations sustains Europe’s steady growth trajectory in high-value, environmentally compliant pouch formats.

Asia Pacific Stand-up Zipper Pouches Market Trends - High-Volume Growth from Urbanization, Manufacturing Scale, and E-Commerce

Asia Pacific is projected to account for 30.4% of the market share, making it the largest regional market for stand-up zipper pouches. The region benefits from high population density, rapid urbanization, expanding modern retail infrastructure, and rising consumption of packaged convenience foods. China and India serve as major manufacturing hubs, supported by cost-competitive converting operations and integrated film production capabilities.

China’s flexible packaging industry supports both domestic brands and export markets. Major multinational brands such as Nestlé and Unilever operate extensive manufacturing and packaging networks in China, increasing demand for high-volume pouch formats across snacks, beverages, and homecare. India’s rapidly growing packaged food sector, driven by brands such as ITC, Britannia, and Tata Consumer Products, continues to adopt zipper pouches for spices, snacks, and ready-to-eat categories.

Local converters, including Uflex Ltd., have expanded recyclable laminate offerings and digital printing capabilities to meet both domestic and export requirements. Japan represents a premium sub-market emphasizing high-barrier and aesthetically refined pouch solutions. Japanese food and personal care brands prioritize advanced oxygen and moisture barriers, supporting demand for precision lamination technologies. In ASEAN markets such as Indonesia, Thailand, and Vietnam, rapid retail modernization and convenience store expansion are increasing the adoption of stand-up zipper pouches for small-format snack and beverage products.

E-commerce expansion across China, India, and Southeast Asia reinforces demand for lightweight, durable, resealable packaging that optimizes shipping efficiency. Regulatory frameworks vary widely across the region. China and India are strengthening packaging waste management policies, yet recycling infrastructure remains uneven, creating a dual market dynamic. High-volume plastic laminate pouches continue dominating value-sensitive segments, while premium recyclable and paper-based pilots expand in urban and export-oriented markets. Investment in high-speed pouch lines, spout welding systems, and digital printing technology continues across Asia Pacific. Regional players are scaling localized production to serve multinational brand portfolios efficiently, reinforcing Asia Pacific’s position as both the largest revenue contributor and a key engine of future unit growth.

Competitive Landscape

The global stand-up zipper pouches market is moderately concentrated among global converters with extensive film production and research capabilities, while regional players serve localized demand. Leading companies command a significant share in premium and sustainable segments, supported by global supply chains and advanced material science expertise.

Key strategies include investment in recyclable mono-material solutions, expansion through mergers and acquisitions, geographic diversification into high-growth regions, and digital printing adoption for short-run customization. Competitive differentiation increasingly depends on sustainability certification, barrier innovation, and co-development partnerships with brand owners.

Key Industry Developments:

- In April 2025, Amcor plc completed the acquisition of Berry Global Group, Inc., expanding its global packaging footprint and broadening its product offerings across flexible films, rigid containers, closures, and dispensing packaging.

- In March 2025, Amcor unveiled its AmFiber Performance Paper stand-up pouch for dry beverages, a recyclable paper-based refill solution that supports reduced environmental impact and lower extended producer responsibility fees for brands.

Companies Covered in Stand-up Zipper Pouches Market

- Amcor plc

- Mondi Group

- Sealed Air Corporation

- Berry Global Group, Inc.

- Huhtamaki Oyj

- Sonoco Products Company

- Constantia Flexibles

- ProAmpac

- Coveris Holdings S.A.

- Uflex Ltd.

- Printpack

- ePac Flexible Packaging

- Winpak Ltd.

- Clondalkin Group

- Glenroy, Inc.

- American Packaging Corporation

- Transcontinental Inc.

- TC Transcontinental Packaging

Frequently Asked Questions

The global stand-up zipper pouches market size is projected to be valued at US$3.8 billion in 2026.

The stand-up zipper pouches market is expected to reach US$5.8 billion by 2033.

Key trends include the transition toward recyclable and mono-material laminates, expansion of paper-based pouch technologies, rising adoption of spouted refill formats, increasing use of digital printing for short-run customization, and consolidation among major flexible packaging manufacturers to enhance R&D and scale efficiencies.

The bottom gusset pouch segment leads the market, accounting for 43.4% share, supported by strong shelf stability, high printable surface area, and broad use in snacks, pet food, and coffee packaging.

The stand-up zipper pouches market is projected to grow at a CAGR of 6.1% between 2026 and 2033.

Major players include Amcor plc, Mondi Group, Sealed Air Corporation, Huhtamaki Oyj, and Constantia Flexibles.