- Non-food Packaging

- Spirits Miniatures Market

Spirits Miniatures Market Size, Share, and Growth Forecast, 2026 - 2033

Spirits Miniatures Market by Spirit Type (Whiskey, Gin, Others), Distribution Channel (Travel Retail/Duty-Free, E-commerce, Others), Packaging Material, and Regional Analysis for 2026 - 2033

Spirits Miniatures Market Size and Trends Analysis

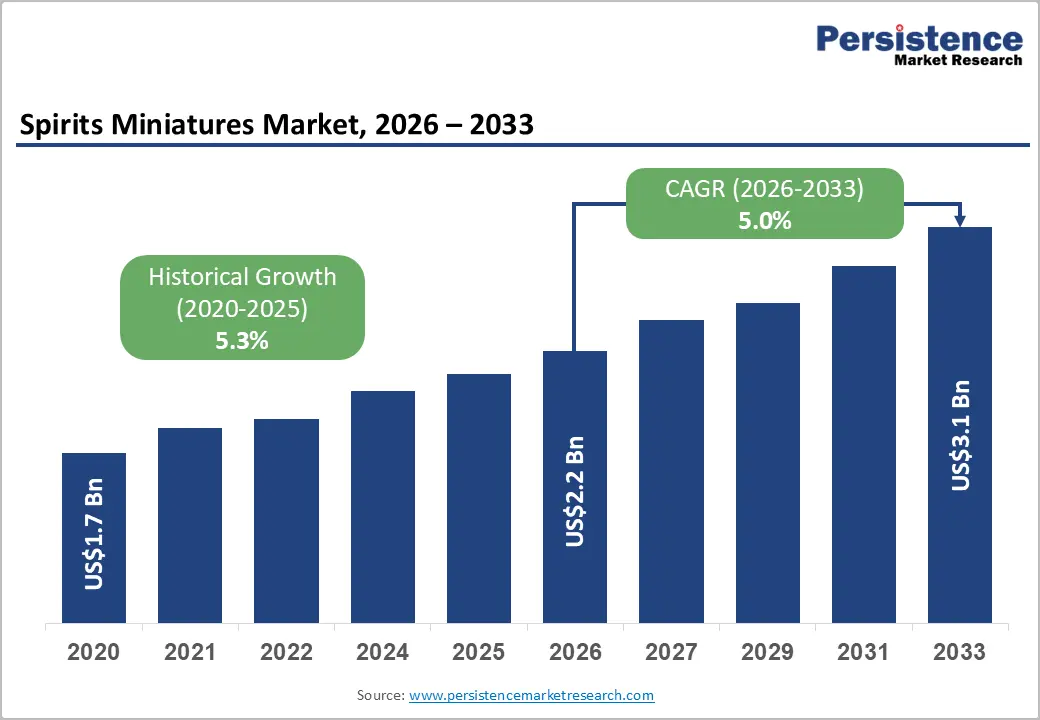

The global spirits miniatures market size is likely to be valued at US$2.2 billion in 2026 and is expected to reach US$3.1 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033, driven by ongoing premiumization in on-the-go consumption and gifting segments, the resilience of travel-retail channels, and the accelerating shift toward digital platforms that facilitate direct-to-consumer (DTC) sampling and curated tasting collections.

Rising consumer interest in trial-sized formats and limited-edition offerings continues to bolster demand for small-volume SKUs. Advancements in packaging design and greater supply chain efficiencies are helping reduce per-unit logistics costs, partially mitigating regulatory and compliance-related expenses.

Key Industry Highlights:

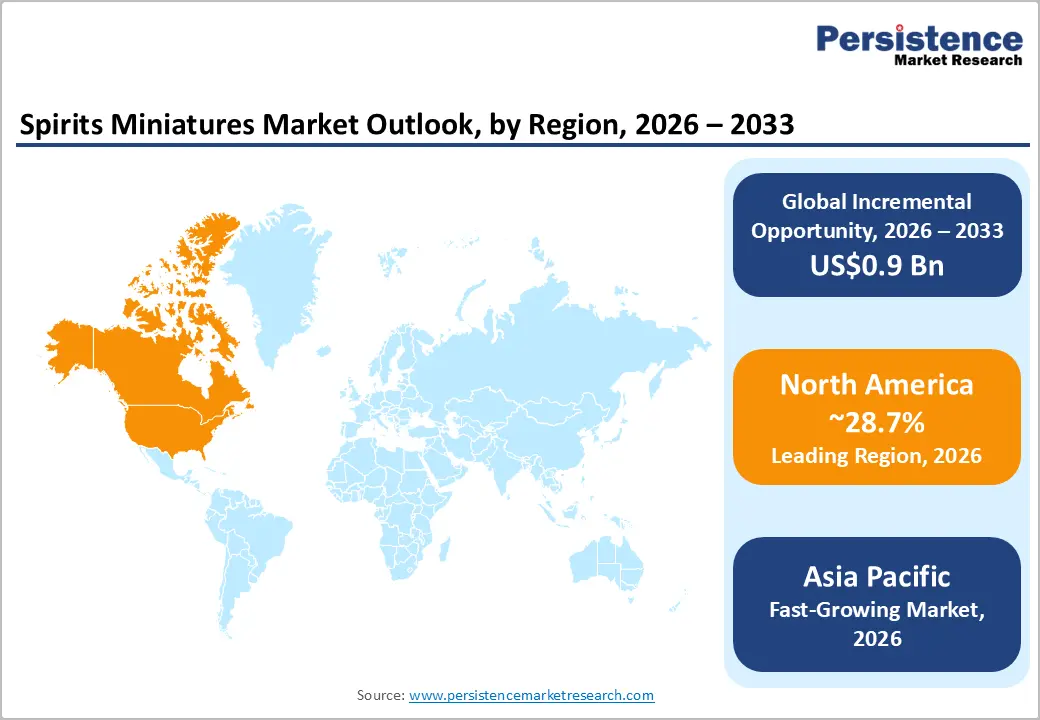

- Leading Region: North America is projected to account for approximately 28.7% of the market share, driven by strong U.S. premium whiskey demand, advanced travel-retail infrastructure, and high DTC penetration.

- Fastest-growing Region: Asia Pacific is projected to register the highest growth rate through 2033, supported by accelerating premiumization in China and India and rapid e-commerce expansion across ASEAN markets.

- Investment Plans: Major producers are investing in automated micro-filling lines, sustainable packaging innovations (recycled glass and lightweight PET), and travel-retail-exclusive portfolios, aligning with a projected 5.0% CAGR (2026 - 2033).

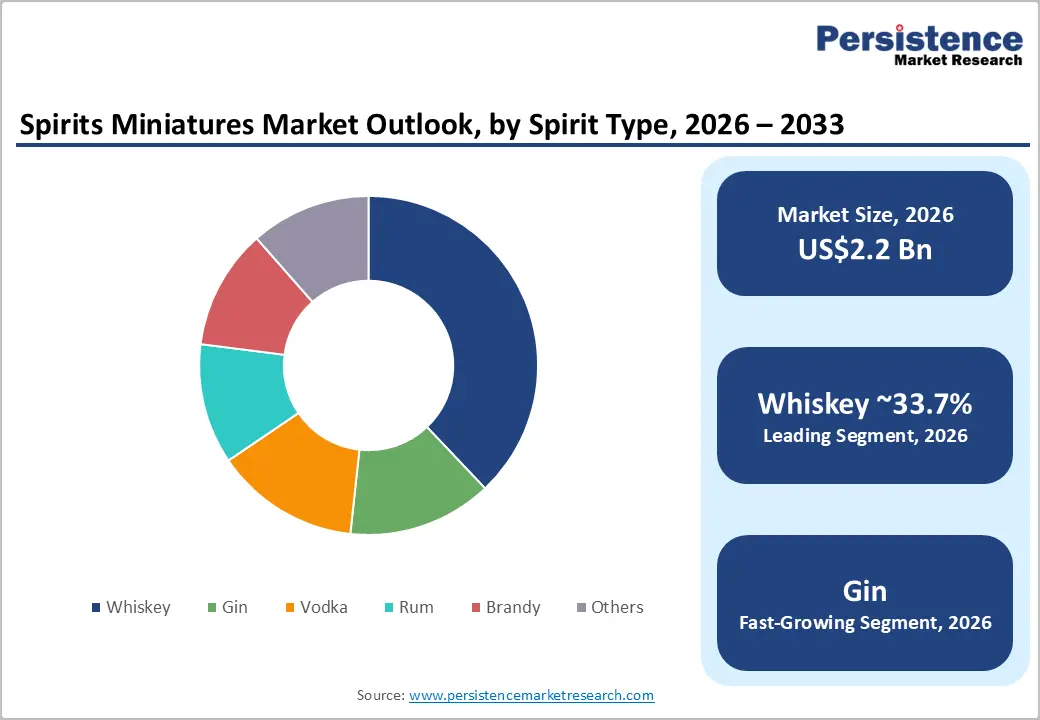

- Dominant Spirit Type: Whiskey is anticipated to lead, holding 33.7% of market share, reflecting premium positioning, gifting demand, and collector-focused travel-retail releases.

- Leading Distribution Channel: Travel Retail/Duty-Free dominates with an estimated 36.2% share, supported by impulse purchasing behavior, curated miniature assortments, and high-margin exclusive launches.

| Key Insights | Details |

|---|---|

| Spirits Miniatures Market Size (2026E) | US$2.2 Bn |

| Market Value Forecast (2033F) | US$3.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Travel Retail & Duty-Free Recovery and Expansion

Travel retail remains a structural growth engine for premium single-serve spirits. Airports, cruise terminals, and cross-border retail hubs have expanded experience-led assortments that prioritize curated, gift-ready products. Passenger traffic recovery and the reopening of international routes have reinforced demand for impulse and souvenir purchases, directly benefiting miniature formats. Miniatures benefit disproportionately from this channel due to their compact size, which aligns with airline carry-on policies, gifting culture, and premium sampling needs.

Retailers favor curated sampler packs and prestige miniatures to enhance per-square-foot productivity. For spirits producers, travel retail increases SKU velocity, strengthens brand visibility among international consumers, and lowers acquisition costs compared to large-format promotional campaigns. Companies that secure airport listings and design channel-exclusive miniature collections achieve higher margins and stronger brand trial rates.

E-commerce and Direct-to-Consumer Sampling

The rapid expansion of online alcohol retail has significantly influenced sales of miniature spirits. Licensed online platforms and brand-owned DTC stores allow producers to sell sampler packs, curated tasting boxes, and limited-edition miniatures directly to consumers. Digital storefronts reduce shelf-space constraints and facilitate personalized marketing campaigns. Miniatures serve as discovery tools in the online channel. Subscription tasting services and sampler bundles reduce customer acquisition costs and increase repeat purchases by encouraging trial across multiple SKUs.

Digital sales also generate first-party consumer data, enabling producers to test new variants and refine launch strategies before committing to full-scale distribution. Embedding miniatures in subscription and loyalty programs enables brands to increase lifetime customer value while mitigating inventory risk.

Premiumization and Craft-Driven Trial

Premium spirit categories, particularly whiskey and craft gin, continue to grow faster than value segments in many markets. Consumers increasingly seek differentiated experiences, including aged expressions, botanical innovations, and regionally distinctive finishes. Miniature packaging enables consumers to experience premium brands at a lower absolute spend while maintaining perceived exclusivity. Premium miniatures, typically ranging from 30 mL to 200 mL, command higher price-per-milliliter margins than full-size bottles.

Producers deploy these formats to test limited cask finishes, regionally exclusive releases, and small-batch craft spirits before scaling production. When supported by strong storytelling, provenance claims, and gift-ready packaging, miniature spirits achieve premium positioning and margin resilience.

Barrier Analysis - Regulatory and Compliance Cost Pressure

Regulatory oversight on labeling, age verification, health warnings, and packaging waste has intensified across major markets. Small-format bottles impose a disproportionately higher compliance burden because labeling space is limited, while regulatory disclosures remain mandatory. The per-unit compliance cost is therefore higher for miniatures than for standard bottles. Adjustments to labeling requirements or packaging materials can increase per-unit costs by several cents, which materially affects margins at scale.

Producers must invest in regulatory expertise, packaging redesign, and traceability systems to mitigate risks of recalls or fines. While these requirements create barriers to entry, they also compress margins for smaller producers without dedicated compliance infrastructure.

Logistics and Unit Economics for Small Formats

Miniature bottles introduce SKU complexity and increase handling intensity per milliliter sold. Glass micro-bottles are susceptible to breakage, leading to higher protective packaging requirements and fulfillment costs. In lower-margin retail channels, these logistics pressures can erode profitability. Breakage mitigation and enhanced secondary packaging may increase fulfillment expenses by a mid-single-digit percentage. Premium pricing in travel retail and online channels helps offset these costs; however, value-oriented retail environments remain sensitive to price increases. Operational optimization through centralized co-packing, automated filling lines, and lightweight packaging alternatives is essential to preserve margin integrity.

Emerging Markets and Regional Premiumization

Urban centers in India, Southeast Asia, and parts of China demonstrate rising premium spirits consumption alongside expanding tourism flows. These trends create meaningful opportunities for curated miniature offerings targeted at gifting, sampling, and experiential consumption. If 5-8% of incremental premium spirits spending in these markets shifts toward miniature formats over the next three to five years, the category could capture hundreds of millions of dollars in additional global revenue. Strategic partnerships with regional travel-retail operators and licensed e-commerce platforms can accelerate adoption. Localized limited editions tailored to cultural preferences enhance resonance and brand equity.

Sustainable and Lightweight Packaging

Sustainability priorities and evolving packaging regulations encourage innovation in recyclable and lightweight miniature formats. Recycled-content glass, certified food-grade PET, and aluminum solutions for ready-to-drink (RTD) applications offer opportunities to reduce logistics costs and carbon intensity. If sustainably packaged SKUs capture 10-15% of premium miniature sales over the forecast period, producers can achieve pricing differentiation while lowering transportation expenses.

Piloting eco-certified miniatures in travel retail environments strengthens brand perception and supports trade negotiations. Lifecycle emissions reporting and clear sustainability labeling improve consumer trust and justify premium positioning.

Category-wise Analysis

Spirit Type Insights

Whiskey is anticipated to account for approximately 33.7% of market share in 2026, maintaining its leadership through 2033. Its dominance reflects sustained global demand for premium single malts, blended Scotch whisky, Irish whiskey, American bourbon, and Japanese whisky. The miniature format aligns closely with whiskey’s premium storytelling attributes, age statements, cask finishes (e.g., sherry or port cask), terroir, and distillation heritage, making it particularly attractive for collectors, corporate gifting, and travel retail.

Major producers such as Diageo (Johnnie Walker Blue Label miniatures), Pernod Ricard (Chivas Regal travel exclusives), and Brown-Forman (Jack Daniel’s limited-edition samplers) actively leverage 50-100 mL formats for airport retail and curated tasting kits. These SKUs enable consumers to experience high-value expressions at a lower upfront cost, supporting trial conversion into full-sized purchases. Miniature whiskey bottles also serve as strategic entry points for emerging premium consumers in Asia Pacific and Latin America, where aspirational purchasing behavior drives experimentation. From a portfolio perspective, whiskey remains the revenue anchor for multinational spirits producers due to its pricing power and brand equity.

Gin is the fastest-growing spirit category in the miniatures market, driven by craft distillery expansion, botanical innovation, and the global resurgence of cocktail culture. The proliferation of small-batch producers in the United Kingdom, Spain, Germany, and Australia has expanded flavor diversity, ranging from citrus-forward and floral gins to regionally inspired botanicals. Miniature packaging enables producers to introduce these experimental SKUs with limited capital risk. For example, craft-focused brands frequently offer 50 mL sampler sets featuring multiple botanical profiles, allowing consumers to compare variants before purchasing standard 700 mL bottles.

Travel retail operators increasingly dedicate shelf space to curated “gin discovery” packs, capitalizing on cocktail tourism trends. Gin miniatures also align with experiential consumption patterns among younger demographics who value variety and authenticity. Subscription tasting boxes and digital cocktail kits further accelerate trial frequency. While whiskey secures structural revenue stability, expanding gin miniatures provides producers with incremental growth, higher SKU turnover, and stronger engagement with mixology-driven consumers.

Distribution Channel Insights

Travel retail and duty-free channels are projected to account for approximately 36.2% of the market in 2026, reinforcing their position as the dominant distribution channels. Airports, cruise terminals, and border shops prioritize high-margin, gift-ready formats, making miniatures a natural fit. The compact size supports airline carry-on regulations and impulse gifting behavior, particularly among international travelers. Leading operators such as Dufry (Avolta) and Lagardère Travel Retail collaborate with major spirits producers to curate premium miniature assortments and travel-exclusive releases.

For instance, brands frequently launch limited-edition miniature gift packs tied to regional themes or seasonal travel peaks. These formats not only increase average transaction value but also stimulate cross-selling into full-size bottles. Travel retail environments emphasize premium presentation and experiential merchandising, enhancing brand visibility. For producers, this channel offers higher margin potential and concentrated access to international consumers. Strategic investments in exclusive SKUs, premium packaging, and in-terminal marketing activations remain central to sustaining leadership in this segment.

E-commerce is the fastest-growing distribution channel for spirits miniatures, supported by expanding online alcohol regulations, subscription models, and direct-to-consumer (DTC) engagement strategies. Licensed digital platforms and brand-owned websites enable curated tasting kits, limited releases, and personalized bundles that are not constrained by physical shelf space. Brands such as Diageo and Pernod Ricard have strengthened their DTC ecosystems, offering sampler packs that allow consumers to explore multiple labels within a single purchase.

Online marketplaces also facilitate targeted marketing campaigns using customer data analytics, increasing conversion rates and repeat purchases. Miniatures are particularly well-suited to digital channels because they reduce the financial barrier to experimentation and enable seasonal promotional bundles. Subscription-based tasting services in North America and Europe have further expanded the discovery model, encouraging recurring revenue streams. An optimized omni-channel strategy, combining travel retail exclusives with data-driven e-commerce bundles, enhances profitability, diversifies revenue streams, and strengthens long-term customer loyalty. Producers that integrate inventory management systems and digital marketing analytics into miniature portfolios will achieve superior channel performance through 2033.

Regional Insights

North America Spirits Miniatures Market Trends - Premium Whiskey-Led Travel Retail and DTC Expansion amid Regulatory Complexity

North America accounts for an estimated 28.7% of the global spirits miniatures market, with the United States clearly anchoring regional demand. The region benefits from a deeply entrenched premium spirits culture, high brand awareness, and strong consumer familiarity with sampling formats. Miniatures are widely used across travel retail, corporate gifting, and increasingly within digital tasting and subscription models. Major U.S. airports such as JFK, LAX, and Atlanta Hartsfield-Jackson serve as high-volume travel-retail hubs where premium whiskey and bourbon miniatures perform strongly, supported by consistent international passenger flows.

Premium whiskey consumption remains a core driver of demand. Brands under Brown-Forman (Jack Daniel’s), Diageo (Bulleit, Johnnie Walker), and Beam Suntory (Maker’s Mark, Knob Creek) actively deploy miniature SKUs for trial, gifting, and limited-edition travel exclusives. These formats are also used to introduce experimental cask finishes and small-batch releases before wider rollouts. The expansion of licensed direct-to-consumer (DTC) platforms in states such as California, New York, and Florida has strengthened online sampler sales, particularly for curated whiskey and gin tasting sets.

Regulatory complexity also remains a defining constraint. The U.S. three-tier distribution system, combined with state-level variations in alcohol shipping, labeling, and bottle-deposit laws, increases compliance and operational costs for microbreweries. Interstate shipping restrictions limit the full national scalability of DTC, requiring producers to maintain state-specific fulfillment strategies.

Europe Spirits Miniatures Market Trends-Duty-Free Dominance, Craft Gin Discovery Packs, and EPR-Driven Packaging Shifts

Europe accounts for a substantial share of global demand for spirits miniatures, underpinned by long-established duty-free networks, dense cross-border travel, and strong gifting traditions. The U.K., Germany, France, and Spain remain the most influential markets, collectively shaping regional consumption patterns. European travelers show high acceptance of miniature spirits as souvenirs and premium gifts, particularly within whiskey, gin, and liqueur categories.

The U.K. plays a pivotal role due to its dominant position in both Scotch whisky production and gin innovation. Leading distillers such as Diageo, Pernod Ricard, and William Grant & Sons continue to launch travel-retail-exclusive miniature packs featuring multiple expressions within a single brand family. In parallel, Europe’s craft gin ecosystem, especially in the U.K., Spain, and Germany, has driven demand for botanical gin miniatures, frequently marketed as discovery or tasting collections.

Regulatory harmonization across the European Union influences packaging and materials strategy. Extended Producer Responsibility (EPR) rules and packaging waste directives have increased compliance costs for small-format glass bottles, prompting producers to invest in lightweight glass, higher recycled-content materials, and redesigned secondary packaging. While this raises per-unit costs, it also accelerates sustainability-led innovation.

Asia Pacific Spirits Miniatures Market Trends - Rapid Premiumization, Airport Retail Growth, and Aspirational Entry-Level Luxury Sampling

Asia-Pacific is likely to be the fastest-growing regional market for spirits miniatures, driven by rapid premiumization, expanding middle-class populations, and strong growth in international and domestic travel. China, Japan, India, and key ASEAN economies are central to this expansion, with miniatures increasingly positioned as aspirational entry points into global luxury spirits brands.

In China, demand for premium whiskey and imported gin has accelerated, supported by gifting culture and experiential consumption. International producers such as Diageo and Pernod Ricard have expanded miniature offerings in airport retail locations in Beijing, Shanghai, and Guangzhou, using sampler formats to introduce high-end Scotch and Irish whiskey labels.

Japan, with its strong domestic whisky heritage, has also seen increased interest in miniature expressions of Japanese single malts, particularly among international travelers. India and Southeast Asia contribute to growth through rising urban disposable incomes and the rapid adoption of e-commerce. Licensed online platforms and city-based alcohol delivery services increasingly offer miniature bundles and tasting kits, especially in metropolitan markets. Manufacturing scale advantages in parts of Asia enable cost-efficient production of small bottles, supporting limited-run and experimental launches.

Competitive Landscape

The global spirits miniatures market is moderately fragmented. Large multinational spirits producers dominate premium travel-retail and global DTC channels, while craft distillers contribute innovation and niche appeal. Competitive positioning centers on brand equity, distribution access, packaging efficiency, and compliance capability.

Key strategies include channel specialization, premium limited-edition releases, and packaging optimization. Leaders differentiate through exclusive travel-retail partnerships, centralized miniature production capabilities, and data-driven digital marketing models.

Key Industry Developments:

- In October 2025, Maison Hennessy unveiled the Paradis Zodiac Miniatures Collection, launching a set of premium miniature cognacs as travel-retail exclusives at major Asia Pacific airports, including Singapore Changi and Kuala Lumpur International, enhancing gifting and collector appeal in key international hubs.

Companies Covered in Spirits Miniatures Market

- Diageo

- Pernod Ricard

- Brown-Forman

- Beam Suntory

- Bacardi Limited

- Rémy Cointreau

- Campari Group

- Sazerac Company

- William Grant & Sons

- Moët Hennessy

- Constellation Brands (Spirits Division)

- Mast-Jägermeister SE

- Edrington Group

- Asahi Group Holdings

- Di Profaci Spirits

- Distell Group

- Heaven Hill Brands

- Casa Cuervo

Frequently Asked Questions

The global spirits miniatures market is projected to be valued at US$2.2 billion in 2026.

The spirits miniatures market is expected to reach US$3.1 billion by 2033.

Key trends include premium whiskey and craft gin miniatures, expansion of travel-retail exclusive launches, increasing e-commerce and direct-to-consumer (DTC) sampling models, and rising adoption of sustainable and lightweight packaging formats such as recycled glass and PET.

Whiskey leads the market with an anticipated 33.7% share, driven by premium aged expressions, collector-oriented travel-retail editions, and gifting demand.

The spirits miniatures market is forecast to grow at a CAGR of 5.0% between 2026 and 2033.

Major players include Diageo, Pernod Ricard, Brown-Forman, Beam Suntory, and Bacardi Limited.