- Healthcare Services

- Speech Therapy Service Market

Speech Therapy Service Market Size, Share, and Growth Forecast 2026 – 2033

Speech Therapy Service Market by Therapy Type (Articulation Therapy, Oral Motor Therapy), Age Group (Pediatric, Adult, Geriatric), End-user (Hospitals and Clinics, Others), and Regional Analysis 2026 – 2033

Speech Therapy Service Market Size and Trends Analysis

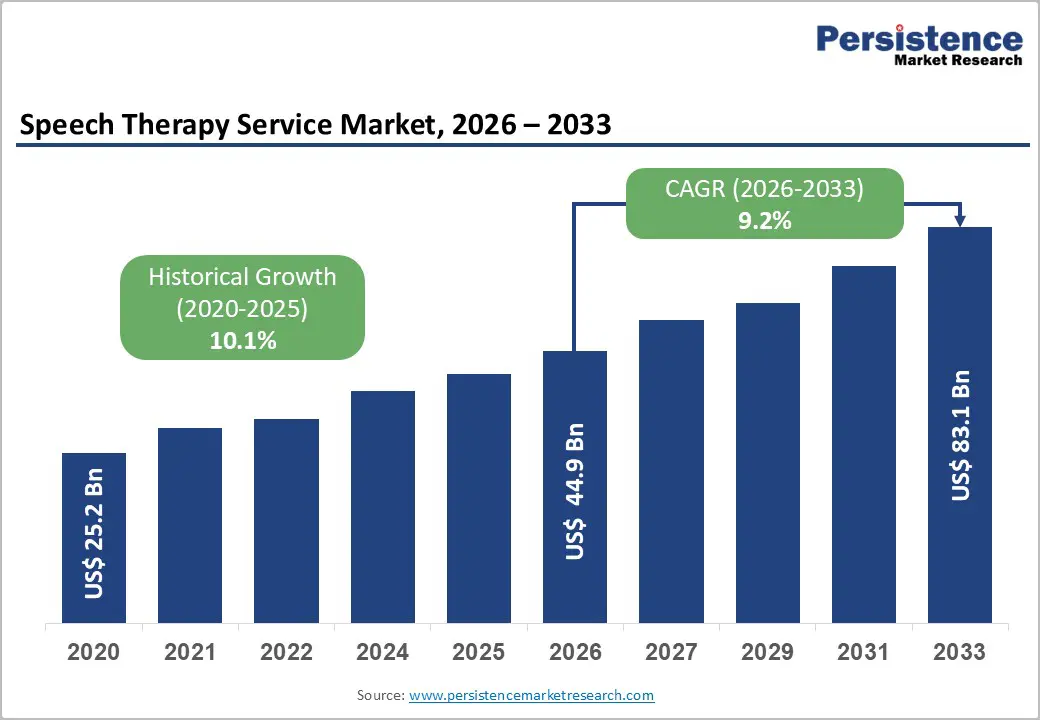

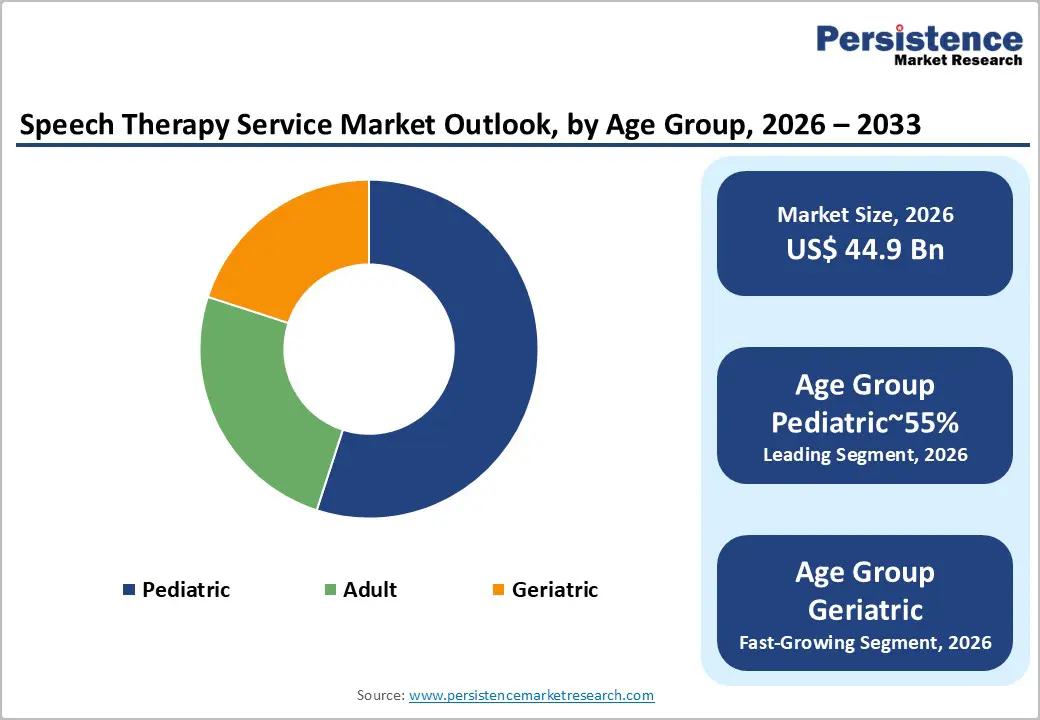

The global speech therapy service market size is expected to be valued at US$44.9 billion in 2026 and is projected to reach US$83.1 billion by 2033, growing at a CAGR of 9.2% during the forecast period 2026-2033, driven by the rising prevalence of speech and communication disorders, supported by an aging population and increasing awareness of early interventions. The adoption of telepractice and digital health platforms is expected to improve accessibility and reduce treatment barriers, while the expanding elderly population is likely to further boost demand for specialized geriatric communication care.

Key Industry Highlights:

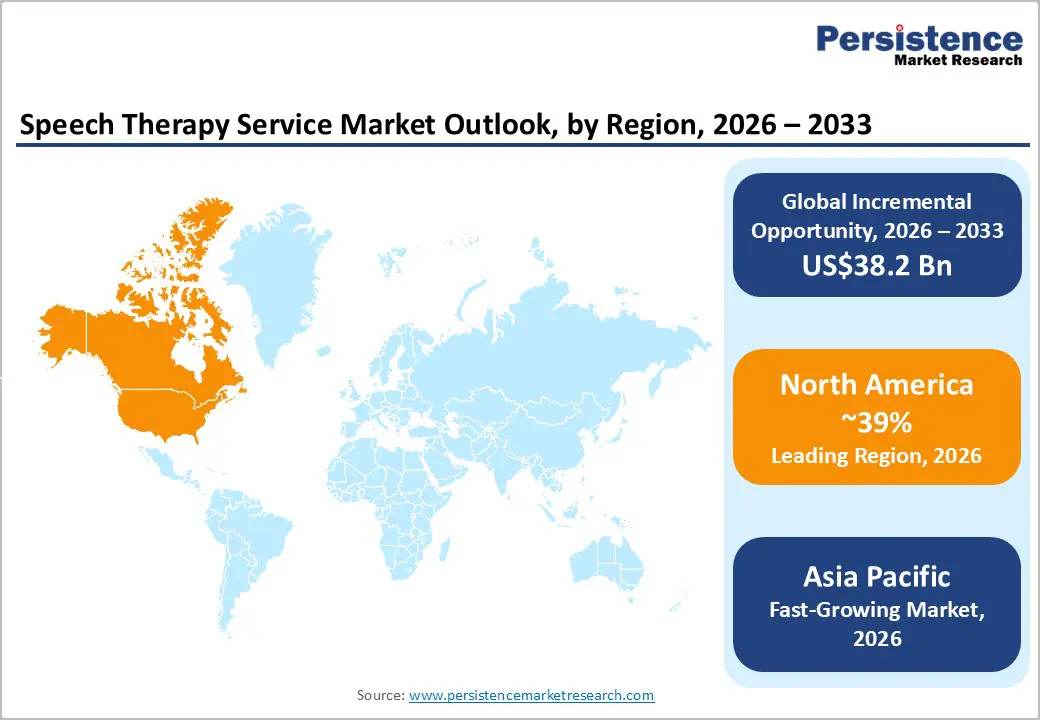

- Leading Region: North America is expected to dominate, accounting for a market share of 42% in 2026, supported by a strong healthcare infrastructure and established therapy networks.

- Fastest-growing Region: Asia Pacific is expected to become the fastest-growing regional market, driven by enhanced diagnostic capabilities and increasing availability of speech therapy services across China, India, and Southeast Asia.

- Fastest-Growing Age Group: The geriatric therapy segment is likely to grow rapidly, fueled by the increasing prevalence of neurological disorders, including post-stroke conditions and age-related communication impairments.

- Key Driver: The rising prevalence of speech and developmental disorders, heightened awareness of early interventions, and growing adoption of digital and telehealth platforms.

- Key Restraint: Limited availability of trained professionals and infrastructural gaps in emerging regions may constrain widespread service access.

- Key Opportunity: Telehealth and AI-enabled solutions present significant untapped potential, enabling broader access and operational efficiency across clinical and educational settings.

- Key Industry Developments: AI4ExceptionalEd is developing the AI Screener and AI Orchestrator to support SLPs by automating tasks and reducing burnout. Public rollout is expected around 2026, enabling more efficient, individualized interventions.

| Key Insights | Details |

|---|---|

| Speech Therapy Service Market Size (2026E) | US$44.9 Bn |

| Market Value Forecast (2033F) | US$83.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Aging Population and Chronic Conditions

The global geriatric population surpassed one billion in 2020, according to the WHO (October, 2025), and is expected to grow to 1.5 billion by 2050, significantly increasing demand for speech therapy services related to stroke rehabilitation and dementia care. In the U.S. alone, the CDC reports approximately 795,000 stroke cases each year, with nearly 30% of survivors developing aphasia that requires therapeutic intervention. Older adults face a higher incidence of neurological and chronic conditions, directly elevating the need for specialized communication and rehabilitation support. Improved post-stroke survival rates and rising life expectancy continue to expand the patient base, sustaining long-term demand for targeted speech and language therapies.

Increasing awareness among caregivers, healthcare professionals, and policy-makers is strengthening the emphasis on early diagnosis and timely intervention as essential factors in preserving and improving quality of life. This trend encourages the adoption of both clinical and home-based speech therapy solutions, while technological advances, including teletherapy and digital platforms, are expected to make services more accessible. Overall, demographic shifts and the rising burden of chronic neurological conditions remain key drivers for sustained market growth.

Shortage of Certified Speech-Language Pathologists (SLPs)

A critical structural challenge in the market is the widening gap between rising patient demand and the available supply of certified professionals. Regulatory bodies in North America and Europe report significant vacancies across both educational and clinical settings, highlighting the difficulty of filling roles due to high burnout rates and the lengthy, rigorous training required for certification. This human capital constraint directly affects service delivery, limiting the capacity of rehabilitation centers, hospitals, and schools to meet the growing patient needs.

The shortage also slows down the adoption of specialized therapies in high-demand urban and aging population markets. With caseloads increasing and workforce expansion lagging, service quality may be impacted, particularly in regions with limited training infrastructure. This barrier underscores the need for alternative solutions such as teletherapy, digital platforms, and AI-powered tools to enhance efficiency and help offset the shortage of professionals, ultimately supporting long-term market growth.

Cross-Sector Integration into Corporate Wellness and Mental Health Platforms

The speech therapy market is undergoing a significant transformation through its integration with digital mental health platforms and corporate wellness initiatives. Organizations are increasingly emphasizing neurodiversity, inclusive communication, and employee well-being, creating demand for targeted support for adults facing social communication challenges, stuttering, or accent-related barriers. In response, speech therapy services are being incorporated into Employee Assistance Programs (EAPs) and broader cognitive wellness frameworks, allowing providers to engage professional populations that were previously underserved by traditional clinical models. This convergence positions speech therapy not only as a clinical service but also as a strategic tool for enhancing workplace productivity, engagement, and inclusivity.

Several organizational applications illustrate this shift. In multinational technology firms, structured speech therapy programs delivered virtually support employees in refining presentation skills, managing stuttering, and adapting speech patterns for international client interactions. Similarly, financial services institutions are integrating speech and communication modules into leadership development programs, equipping managers with enhanced clarity and confidence for high-stakes client negotiations. Customer service operations, including call centers and global support hubs, are embedding speech therapy within training programs to reduce communication-related stress, improve clarity, and elevate team performance. By embedding these services within holistic wellness and digital health programs, providers are expanding market reach, creating measurable value for employers, and addressing the unmet needs of adult professionals. This employer-driven segment is emerging as a significant growth vector, enabling speech therapy to establish a strategic presence across B2B ecosystems while reinforcing its role in promoting cognitive wellness, professional communication, and workplace inclusivity.

Category–wise Analysis

Therapy Type Insights

The articulation therapy segment is expected to hold a leading position in the market, accounting for approximately 40% of the total share in 2026, largely due to sustained demand for the treatment of speech sound disorders among children. This dominance is supported by early intervention requirements and broad acceptance within clinical practice, creating strong foundations for revenue stability and specialized practitioner expertise. Its proven effectiveness in correcting phonological impairments continues to drive preference across both educational and healthcare settings, ensuring consistent market presence and stable margins.

Oral motor therapy is emerging as the fastest-growing category, propelled by increasing recognition of dysphagia management and facial muscle rehabilitation in both pediatric and geriatric cohorts. Broader categories, including language intervention and cognitive therapy, address complex communication and developmental disorders such as autism and stuttering, reinforcing service breadth. Adoption of these therapies is likely to remain supported by evolving clinical protocols, regulatory emphasis on comprehensive care, and integration with multi-disciplinary rehabilitation programs, collectively enabling incremental market expansion and strategic diversification beyond the dominant articulation-focused segment.

Age Group Insights

Pediatric patients are expected to continue as the dominant market segment, accounting for approximately 55% of the total demand in 2026. This leadership is driven by the widespread implementation of early developmental screening programs, rising diagnosis rates of autism spectrum disorders, and the formal integration of speech therapy services within school systems. Pediatric care models are characterized by extended treatment durations and well-defined referral pathways, which support continuity of care and enhance revenue visibility. The use of standardized clinical and educational protocols further promotes consistent service utilization across settings. Strong alignment with public health and education priorities also facilitates broad adoption within clinics and therapy centers. Collectively, sustained clinical need, institutional support, and high patient engagement establish pediatric speech therapy as a stable and enduring source of market volume.

Geriatric patients are projected to be the fastest-growing segment, driven by the increasing prevalence of dementia, Parkinson’s disease, and age-related dysphagia. Increase in the need for specialized communication and swallowing interventions. Expanding awareness of geriatric rehabilitation and integrated multidisciplinary care models is further driving adoption in this cohort. As healthcare providers increasingly implement tailored programs for older adults, service delivery is gradually shifting toward outpatient, home-based, and assisted-living settings. This indicates significant potential for long-term expansion while complementing the established pediatric-dominated demand base. This segment is gradually prompting service models to shift toward integrated, multidisciplinary care tailored to older adults, including cognitive-communication and swallowing interventions.

End-user Insights

Hospitals and clinics are expected to lead the market, accounting for a share of 48% in 2026, functioning as the primary access point for acute diagnosis, structured assessment, and outpatient rehabilitation. Their dominance is reinforced by integrated diagnostic capabilities, multidisciplinary care pathways, and strong linkage with neurologists and pediatric specialists. This setting captures a substantial share of adult and pediatric cases due to its ability to initiate therapy immediately following diagnosis, ensuring continuity of care and predictable patient inflows. Hospitals also benefit from established referral networks, connecting patients seamlessly to long-term rehabilitation, homecare, or telehealth services. Their capacity to manage complex adult and pediatric cases makes them a preferred choice for families seeking comprehensive, evidence-based interventions. As a result, hospitals and clinics continue to serve as both the entry point and central hub for high-quality speech-language pathology services, driving overall market growth.

Rehabilitation centers are expected to register the fastest growth, driven by increasing demand for long-term neurological rehabilitation and post-stroke recovery programs that rely on intensive, outcomes-focused speech therapy. At the same time, educational institutions are expanding the integration of speech-language pathologists (SLPs) within school systems, strengthening early intervention coverage and enabling longer-term service agreements. By 2026, service delivery will have largely shifted from traditional “pull-out” therapy sessions to “push-in” models, with SLPs working directly within general education classrooms to support multimodal literacy across audio, visual, and text-based learning. This approach responds to the rising prevalence of Autism Spectrum Disorder, now affecting approximately 1 in 36 children, by embedding communication development into the core academic curriculum. Homecare and telehealth models continue to scale rapidly, supported by growing digital adoption, patient convenience, and the need to extend therapy access beyond institutional settings, gradually reshaping cost structures and care delivery models. Platforms such as Better Speech and Presence (formerly Presence Learning) illustrate the evolution from basic video consultations to fully integrated digital therapy ecosystems.

Regional Insights

North America Speech Therapy Service Market Trends

North America is expected to remain the largest and most mature regional market, underpinned by high awareness levels, broad insurance coverage, and advanced healthcare delivery systems. The region accounts for a share of 42% of the global demand in 2026, with the U.S. being the primary contributor due to strong pediatric prevalence and structurally embedded referral pathways across clinical and educational settings. Public reimbursement mechanisms, including expansions, continue to support sustained utilization, while widespread telehealth adoption strengthens access and continuity of care across state boundaries.

From an infrastructure and policy perspective, the region benefits from well-defined regulatory frameworks that facilitate the integration of digital and AI-enabled speech therapy tools. Regulatory clarity from agencies such as the FDA supports faster clinical validation, while a fragmented provider landscape sustains competitive intensity and innovation. Continued venture capital interest and platform-based expansion models are likely to reinforce North America’s leadership position, particularly through cross-state telepractice networks and scalable digital service delivery architectures.

Europe Speech Therapy Service Market Trends

Europe’s speech-language pathology market is expected to remain structurally robust, driven by demographic and clinical imperatives. The aging population is generating heightened demand for dysphagia and post-stroke aphasia management, while neurodegenerative conditions such as Parkinson’s and Alzheimer’s sustain long-term therapy requirements. Concurrently, policy mandates for early childhood screening in markets including France and Germany are reinforcing early intervention pathways, supporting predictable service contracts and extended therapy adoption. Technological integration, notably AI-driven voice analytics, is increasingly deployed for early detection and remote monitoring of neurological and developmental disorders, enhancing diagnostic precision and operational efficiency.

Europe’s market is underpinned by sustained public healthcare expenditure, rigorous regulatory frameworks including EU MDR and HTA compliance, and a concentration of global clinical and research leadership. These structural advantages ensure the adoption of validated digital therapy tools, facilitate outcome-linked reimbursement, and consolidate market dominance. Regulatory alignment and infrastructure maturity across the EU are enhancing reimbursement consistency and cross-border service standardization, contributing to steady market expansion. Rehabilitation services remain relatively concentrated, resulting in a more controlled competitive landscape, while ongoing consolidation continues to enhance provider scale and operational efficiency. Investment activity is increasingly directed toward digital health and teletherapy platforms, reflecting policy priorities around remote care delivery, workforce optimization, and cost containment within publicly funded healthcare systems.

Asia Pacific Speech Therapy Service Market Trends

Asia Pacific is projected to emerge as the fastest-expanding regional market, supported by improving diagnostic penetration and expanding access to speech therapy services across China, India, and Southeast Asia. Rapid urbanization, rising middle-class population, and increasing awareness of developmental and neurological disorders are reshaping demand structures, particularly in pediatric and early-intervention segments. China and India play a central role in driving regional momentum, with large population bases and increasing public and private healthcare investments contributing to volume-led demand expansion rather than immediate value concentration.

The region’s growth potential is reinforced by government-led initiatives and digital innovation. China’s 14th Five-Year Plan prioritizes rehabilitation medicine, while India’s Ayushman Bharat scheme expands reimbursement pathways to lower-income populations. Early pediatric screening programs, multilingual AI diagnostic tools, and tele-therapeutic solutions are increasing both accessibility and operational efficiency. Consequently, APAC is positioned to become the principal engine for incremental global revenue, with neurological disorders representing the most lucrative and rapidly expanding clinical segment. Tele-practice adoption, particularly in rural and underserved areas, is accelerating through AI-enabled platforms that facilitate personalized, cost-effective care, effectively addressing infrastructure gaps. Market structure remains fragmented, with domestic providers gaining prominence alongside rising foreign investments in telehealth infrastructure, positioning Asia Pacific as a key growth engine despite uneven reimbursement coverage and care standardization.

Competitive Landscape

The global speech therapy service market is characterized by a fragmented but increasingly competitive landscape, populated by a mix of specialized providers, therapy networks, and emerging digital health players. Major participants such as TinyEYE Therapy Services and EBS Healthcare exert significant influence through their established telepractice platforms and school-based contracts, driving market direction toward scalable digital delivery. Humanus Corporation and Benchmark Therapies leverage deep clinical networks and staffing solutions to address critical workforce shortages, while LinguiSystems maintains relevance through longstanding reputations in therapeutic resources and assessments. The competitive environment is intensifying as companies prioritize strategic acquisitions, such as The Stepping Stones Group’s expansion, and forge partnerships with tech firms and payers to integrate AI and telehealth solutions.

Key Industry Developments:

- In March 2025, The Stepping Stones Group acquired Gallagher Paediatric Therapy to expand its California footprint and strengthen paediatric therapy capacity amid workforce constraints.

- In July 2024, WellCare of North Carolina and Expressable expanded virtual, evidence-based speech therapy access to the underserved population to improve care equity.

- In April 2024, Elara Caring partnered with Constant Therapy to deploy AI-driven speech-language and cognitive therapy at scale across home health settings.

- In April 2024, Samsung Electronics launched the AI-powered Impulse app using wearable-based haptic feedback to support articulation and fluency improvement.

Companies Covered in Speech Therapy Service Market

- Cohesive Therapeutics

- Benchmark Therapies

- Talk Speech

- Speech Pathways

- John McGivney Centre

- Smart Speech Therapy

- Glenda Browne Pathology

- Therapy Solutions

- Speech Plus

- Say It Right

- LinguiSystems

- Super Duper

- EBS Healthcare

- Humanus Corporation

- TinyEYE Therapy Services

Frequently Asked Questions

The global speech therapy service market is valued at US$44.9 billion in 2026 and is projected to reach US$83.1 billion by 2033.

The speech therapy service market is driven by the rising prevalence of speech and communication disorders, an aging population, increased awareness of early intervention, and expanding adoption of teletherapy platforms.

The speech therapy service market is expected to grow at a CAGR of 9.2% between 2026 and 2033, supported by digital health integration and expanding pediatric demand.

Key opportunities include tele-practice expansion, AI-assisted screening and therapy tools, and integration of speech therapy into corporate wellness and mental health platforms.

Major players include TinyEYE Therapy Services, EBS Healthcare, Humanus Corporation, LinguiSystems, Super Duper, Say It Right, Speech Plus, Benchmark Therapies, and Therapy Solutions.