- Food Packaging

- Shrink Bags Market

Shrink Bags Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Shrink Bags Market by Material Type (Polyethylene, Polyolefin, PVC, Polypropylene, Other), Product Type (Round Bottom, Straight Bottom, Side Sealed), Barrier Type (Low, Medium, High, Ultra-High), Application (Food & Beverage, Healthcare & Pharmaceutical, Consumer Goods, Industrial, Other), and Regional Analysis for 2026 - 2033

Shrink Bags Market Size and Trend Analysis

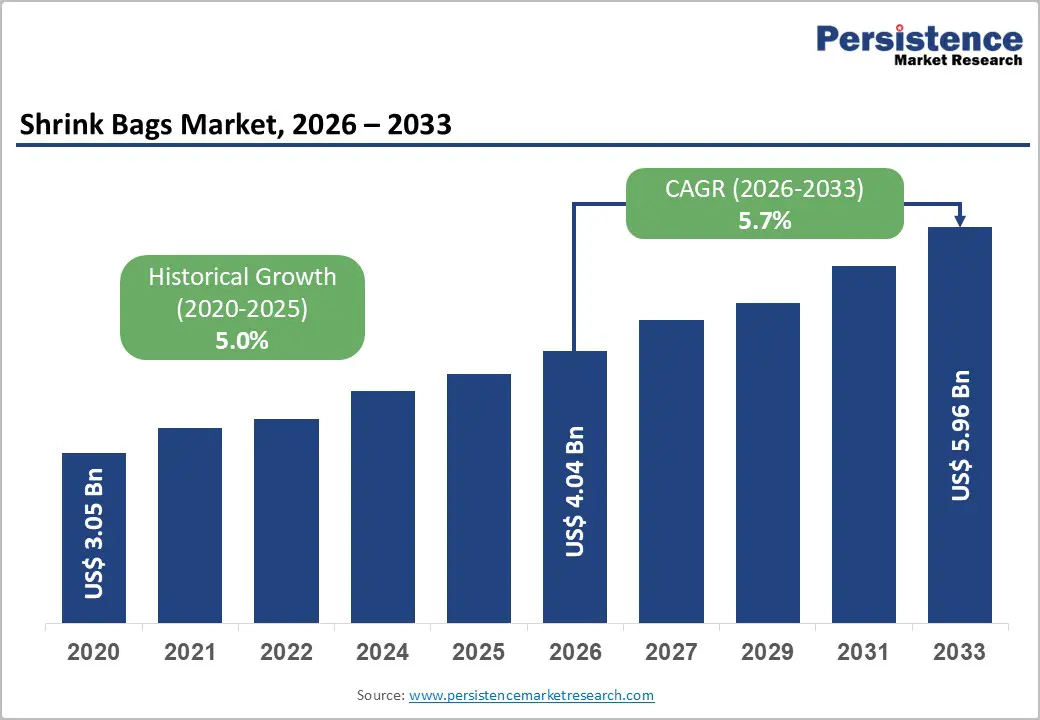

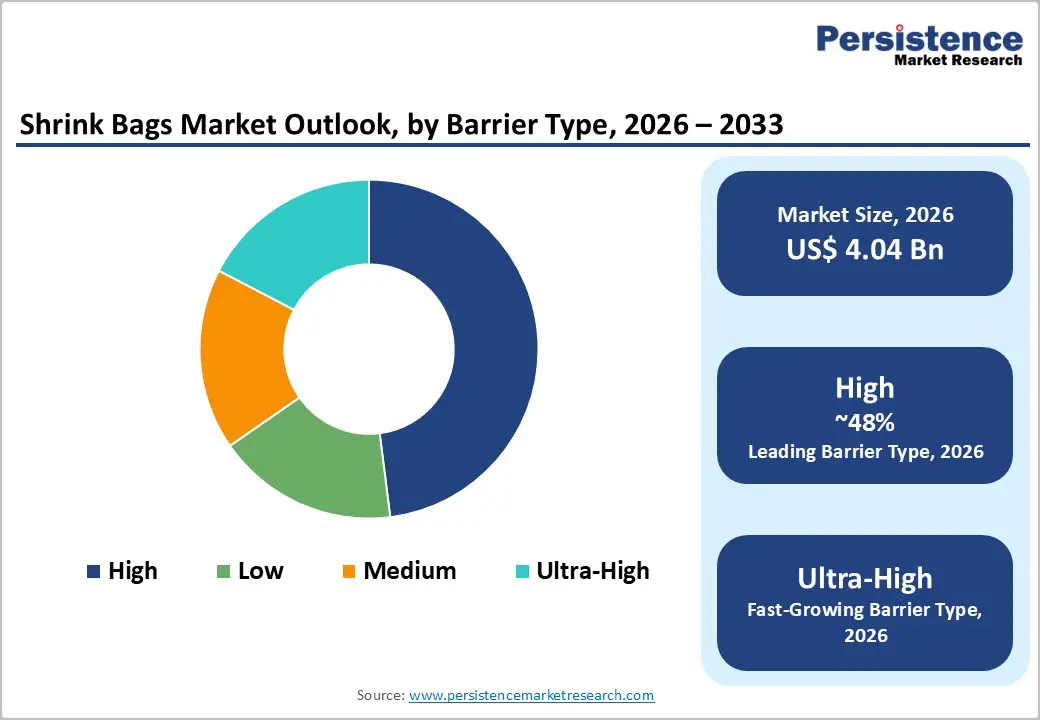

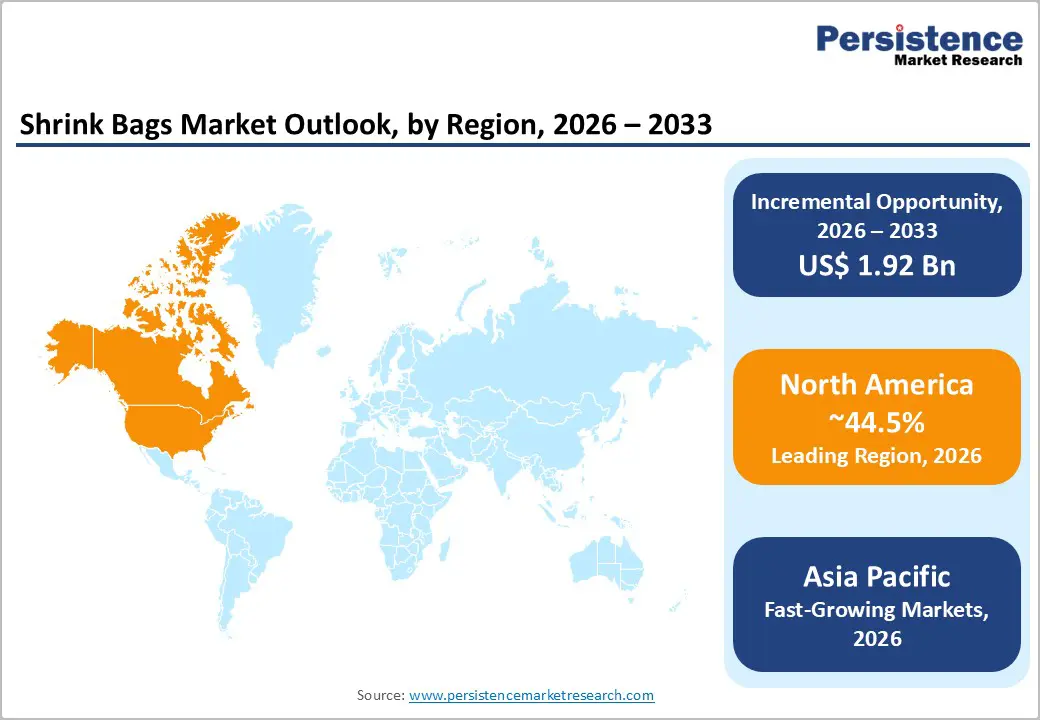

The global shrink bags market size is likely to be valued at US$ 4.04 billion in 2026 and is projected to reach US$ 5.96 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

The market expansion is driven primarily by rising demand for efficient food-preservation solutions and stringent regulatory requirements for pharmaceutical packaging safety. Shrink bags provide exceptional barrier properties against oxygen, moisture, and bacterial contamination, making them indispensable for vacuum-sealed applications across multiple industries. The growth trajectory is further reinforced by innovations in multi-layer high-barrier technologies, recyclable formulations, and antimicrobial coatings that enhance product efficiency while addressing sustainability mandates.

Key Market Highlights

- Regional Leader: North America maintains a dominant market position with 44.5% market share in 2025, driven by the mature food and beverage industry, established cold chain infrastructure, and strong demand from the meat processing and pharmaceutical sectors.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market, driven by rapid industrialization, rising protein consumption in China and India, increased investment in cold chain infrastructure, and rising adoption of vacuum-packed and extended-shelf-life packaging solutions.

- Dominant Segment: Polyethylene-based materials dominate the market, with approximately 58% share, driven by superior barrier properties, regulatory compliance, and cost-effectiveness across food, pharmaceutical, and industrial applications.

- Fastest Growing Segment: High-barrier shrink bags represent the fastest-growing segment, driven by increasing requirements for extended shelf life in meat packaging applications and pharmaceutical sterile barrier systems.

- Key Market Opportunity: Development of biodegradable shrink bags using PHAs, plant proteins, and algae-based plastics presents significant opportunities, addressing sustainability mandates and premium market segments willing to adopt eco-friendly alternatives.

| Key Insights | Details |

|---|---|

| Shrink Bags Market Size (2026E) | US$ 4.04 Bn |

| Market Value Forecast (2033F) | US$ 5.96 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.7% |

| Historical Market Growth (2020 - 2025) | 5.0% |

Market Dynamics

Drivers - Increasing Demand in Food and Beverage Packaging

The proliferation of ready-to-eat and processed food consumption is fundamentally transforming packaging requirements, with shrink bags emerging as a critical solution for maintaining product freshness and extending shelf life. 97% of participants reported daily consumption of ready-made meals, underscoring the massive scale of packaged-food dependence. Shrink bags offer superior barrier properties that protect against moisture, oxygen, and light penetration, thereby preventing spoilage and degradation of packaged food products.

The FDA and USDA have established stringent compliance standards for food contact materials, with polyethylene-based shrink bags meeting these guidelines through their demonstrated safety in direct food contact applications. LDPE, HDPE, and LLDPE variants provide excellent moisture resistance and chemical stability, with migration levels maintained below the 50 parts per billion (ppb) threshold for most foods and 10 ppb for milk and soft drinks. The expanding meat packaging market is driving the adoption of shrink bags, as vacuum-sealed applications ensure contamination-free transport and storage of perishable protein products.

Pharmaceutical Industry Adoption for Sterile Barrier Systems

Healthcare and pharmaceutical sectors are increasingly adopting shrink film packaging solutions to ensure product integrity, sterility, and tamper-evident protection throughout the supply chain. Shrink bags provide airtight seals that form seamless shields against moisture, dust, and other environmental contaminants, which is critical for sensitive medications that can be compromised by humidity. The high-quality polymers utilized in pharmaceutical-grade shrink bags are impermeable to both liquids and particulates, ensuring extended shelf life and maintaining the efficacy of medications during transportation and storage under varying conditions.

Automated application machinery enables efficient packaging of plastic bottles, glass vials, cartons, and high-count brick packs, with perforated shrink film providing tamper-evident seals while maintaining ease of access. The lightweight nature of shrink film minimizes the need for additional packing material, reducing waste and costs while conforming to any product shape, thereby optimizing space utilization during shipping and storage. Clear shrink film enhances shelf appeal by allowing product visibility while providing a professional appearance and space for branding, instructional information, and marketing materials that enhance consumer engagement.

Restraints - Regulatory Pressure and Recycling Compliance Challenges

Government policies targeting plastic waste reduction and increased recycling mandates are imposing significant compliance burdens on shrink bag manufacturers across global markets. Regulations in most countries are establishing stringent requirements for plastic packaging waste management, compelling producers to develop recyclable or biodegradable alternatives to shrink bags.

The European Union Packaging and Packaging Waste Regulation (PPWR), adopted in December 2024 and published in January 2025, mandates that all packaging must be recyclable by 2030, with specific requirements that packaging cannot fall below recyclability Class C. From 2030, flexible packaging must contain at least 35% recycled plastic content, creating substantial sourcing and cost challenges for manufacturers. Multi-layer films that cannot be recycled using existing technologies will be banned from the EU market, requiring significant reformulation and investment in new technologies. These regulatory pressures are driving innovation toward sustainable materials but simultaneously increasing production costs and complexity for market participants.

Price Volatility of Petroleum-Based Raw Materials

The shrink bags market faces persistent challenges from fluctuating prices of petroleum-derived polymers, including polyethylene, polypropylene, and PVC, which constitute the primary raw material base. Price instability in crude oil markets directly impacts polyethylene production costs, creating margin pressures for shrink bag manufacturers and pricing unpredictability for end-users. The transition toward bio-based and recycled content materials, while environmentally beneficial, often entails higher production costs than virgin petroleum-based polymers, creating a competitive disadvantage in price-sensitive market segments.

Manufacturers must balance sustainability commitments with economic viability, particularly as regulatory mandates for recycled content implementation approach 2030 deadlines across major markets. Small and medium-sized enterprises face particular difficulties in absorbing raw material cost fluctuations while simultaneously investing in recycling infrastructure and sustainable material development.

Opportunity - Development of Sustainable and Recyclable Materials

The development of biodegradable shrink bags presents a substantial growth opportunity as sustainability becomes a priority for both consumers and regulatory bodies. Advancements in lightweight, high-barrier, and moisture-resistant materials derived from renewable resources are expected to drive innovation and broaden applications across industries. Polyhydroxyalkanoates (PHAs), produced through microbial fermentation, emerges as viable alternatives to conventional plastics, offering complete biodegradation in soil within 28 days while maintaining strength and flexibility comparable to low-density polyethylene.

Furthermore, plant-based proteins from peas and soy are being engineered into biodegradable films using advanced solubility techniques, yielding structures suitable for flexible packaging. Nano-cellulose sourced from plant fibers provides excellent strength-to-weight ratios and transparency, coupled with superior barrier properties against moisture and gases. Algae-based plastics further reduce carbon footprints while delivering the flexibility and durability required for shrink bag applications. Companies investing in these innovative materials are well-positioned to capture premium market segments that prioritize sustainable packaging aligned with corporate environmental objectives.

Expansion in E-commerce and Convenience Packaging Segments

The explosive growth of e-commerce retail channels is creating substantial demand for protective shrink bag packaging that ensures product integrity during direct-to-consumer shipping. Germany’s shrink bag market demonstrates strong growth driven by expanding e-commerce sectors and increasing consumer demand for convenient packaging formats, with companies like RKW Group and Südpack developing sustainable solutions aligned with environmental goals. Custom-sized shrink packaging is gaining adoption as businesses optimize packaging-to-product ratios to reduce material waste and shipping costs while maintaining protection standards.

The Asia Pacific region is witnessing rapid e-commerce penetration, with emerging middle classes in China, India, and Southeast Asia driving demand for branded, convenience-oriented, and ready-to-eat food products utilizing shrink packaging technologies. Global converters and film suppliers are expanding their manufacturing footprints in the Asia-Pacific to meet local demand and reduce logistics costs, creating infrastructure for sustained regional market growth.

Category-wise Analysis

Material Type Insights

Polyethylene-based shrink bags dominate the material type category, accounting for approximately 58% of the global market share, driven by their exceptional balance of barrier properties, cost-effectiveness, and regulatory compliance. LDPE shrink bags meet FDA/USDA food-handling guidelines while offering flexibility, transparency, and high resistance to moisture, making them particularly suitable for fresh-vegetable and fruit-storage applications. HDPE shrink bags offer superior chemical resistance and durability for industrial applications, with excellent barrier properties that maintain product freshness and extend shelf life.

The polyethylene segments' leadership is reinforced by extensive manufacturing infrastructure, established supply chains, and proven safety profiles, facilitating regulatory approvals across diverse applications, including the food & beverage, pharmaceutical, and consumer goods sectors. Ongoing innovations in polyethylene film technology, including metallocene catalysts and multi-layer coextrusion techniques, are further enhancing performance characteristics while maintaining economic competitiveness against alternative materials.

Product Type Insights

Side sealed shrink bags represent the leading product type segment, capturing approximately 42% of market share due to their superior seal integrity, versatility across diverse product geometries, and efficient manufacturing processes. This product type demonstrates particular strength in pharmaceutical applications where tamper-evident features and sterile barrier maintenance are critical requirements, with automated filling and sealing equipment optimizing production efficiency.

Round bottom shrink bags serve specialized applications in bulk food packaging and industrial components, offering enhanced load distribution for heavier products. Straight-bottom variants provide stable standing for retail display applications, facilitating shelf presentation while maintaining barrier protection.

Barrier Type Insights

High-barrier shrink bags command the largest market share, at approximately 48%, reflecting growing requirements for extended shelf life in food and pharmaceutical applications. High-barrier formulations typically incorporate multiple polymer layers with EVOH cores to reduce oxygen transmission rate, which is critical for maintaining product quality in meat packaging applications. The meat packaging market is driving demand for high-barrier solutions, as vacuum-sealed protein products require stringent protection against oxygen infiltration, which can cause discoloration and bacterial growth.

Ultra-high-barrier shrink bags are experiencing rapid adoption in specialized pharmaceutical and medical device packaging, where moisture vapor transmission rates below 0.5 g/m²/day are required for product stability. Medium-barrier variants serve broad applications in cheese, processed foods, and consumer goods, where moderate protection suffices for the intended shelf life.

Application Insights

Food & beverage applications dominate the shrink bags market with approximately 52% share, driven by fundamental requirements for contamination prevention, freshness maintenance, and regulatory compliance. The segment encompasses diverse product categories, including fresh meat, poultry, seafood, cheese, processed foods, and ready-to-eat meals, each of which demands specific barrier properties and seal-integrity characteristics. Shrink bags' ability to extend product shelf life is particularly valued among the 97% of consumers who report daily ready-made meal consumption, creating massive demand for reliable packaging solutions.

Healthcare & pharmaceutical applications represent the fastest-growing segment, with robust expansion driven by increasing requirements for sterile barrier systems, tamper-evident packaging, and moisture-resistant protection. Pharmaceutical shrink bags provide airtight seals that prevent contamination of sensitive medications, with clear film that allows product visibility while maintaining a professional appearance and space for regulatory labeling.

Regional Insights

North America Shrink Bags Market Trends

The U.S. maintains market leadership in North America, driven by advanced cold chain infrastructure, stringent FDA and USDA regulatory frameworks, and sophisticated food processing industries. Regulatory compliance requirements mandate that shrink films meet safety standards for direct food contact, with migration thresholds strictly enforced at 50 ppb for most foods and 10 ppb for dairy products. The FDA's functional barrier exemption criteria have shaped material innovation strategies, encouraging manufacturers to develop packaging solutions that prevent substance migration while maintaining cost-effectiveness.

North American pharmaceutical companies are increasingly adopting shrink film packaging for small bottles, vials, and carton bundling applications, with tamper-evident features addressing safety concerns and regulatory requirements. The region's innovation ecosystem supports ongoing research into lightweight, high-barrier materials and automated packaging equipment that enhances production efficiency. E-commerce growth is driving demand for protective shrink-packaging solutions that ensure product integrity during direct-to-consumer shipping, particularly for perishable food categories.

Europe Shrink Bags Market Trends

Germany, the U.K., France, and Spain are leading European markets characterized by strong sustainability emphasis and progressive regulatory harmonization under the Packaging and Packaging Waste Regulation (PPWR). The PPWR, adopted in December 2024 and published in January 2025, mandates that all packaging be recyclable by 2030, with minimum thresholds requiring recyclability Class A or B (>80%) for many applications. From 2030, flexible packaging must incorporate at least 35% recycled plastic content, calculated as annual averages per manufacturing plant, fundamentally reshaping raw material sourcing strategies.

German companies, including RKW Group and Südpack, are pioneering the development of biodegradable and recyclable shrink bag solutions aligned with the country's environmental protection goals. Stringent regulations on packaging waste and consumer preferences for eco-friendly solutions are accelerating the adoption of sustainable alternatives. The PPWR introduces packaging-to-product ratio restrictions that prohibit excessive layering, compelling manufacturers to optimize material usage while maintaining protection standards.

Asia Pacific Shrink Bags Market Trends

Asia Pacific is emerging as the fastest-growing region, propelled by rising processed food consumption, urbanization, and rapid adoption of modern retail and e-commerce channels. Emerging middle classes in China, India, and Southeast Asia are increasing demand for branded, convenience-oriented, and ready-to-eat food products that utilize shrink packaging technologies. The region's manufacturing advantages, including lower labor costs and growing polymer production capacity, are attracting global converters and film suppliers to establish production footprints in the region to serve local markets while reducing logistics costs.

China and India are experiencing substantial investments in cold chain infrastructure, enabling expanded distribution of perishable foods requiring vacuum-sealed shrink bag packaging. Japan's advanced packaging technology sector is driving innovations in high-barrier formulations and automated equipment systems that enhance production efficiency. ASEAN countries are witnessing rapid growth in processed food manufacturing and export-oriented industries that depend on protective shrink packaging for international shipping.

Competitive Landscape

The global shrink bags market exhibits moderate consolidation, with leading multinational corporations holding significant market shares alongside numerous regional and specialized manufacturers serving niche applications. Market leaders are pursuing expansion strategies through technological innovation, capacity additions, and strategic partnerships that enhance geographic reach and product portfolio breadth. Emerging business model trends include collaborative development partnerships with end-users, circular economy initiatives incorporating post-consumer recycled content, and service-based offerings that bundle packaging design expertise with material supply.

Key Market Developments

- March 2024: Sealed Air Corporation launched a new eco-friendly EVOH shrink bag to enhance its sustainable packaging offerings, incorporating recycled content and improved barrier performance for meat packaging applications.

- April, 2025: Amcor completed its merger with Berry Global, creating a packaging powerhouse with expanded capabilities in flexible, rigid, and healthcare packaging, aiming for greater innovation and sustainability in consumer goods.

- August 2023: Winpak Ltd. announced the expansion of its shrink bag production capacity to meet growing demand from pharmaceutical and food processing customers across North America.

Top Companies in Shrink Bags Market

- Sealed Air Corp. (U.S.) maintains global leadership through its diversified portfolio of protective packaging solutions, including Cryovac-branded shrink bags that serve food, pharmaceutical, and industrial applications. The company's vertical integration, spanning polymer formulation through converting operations, enables rapid innovation cycles and customized solutions for multinational customers.

Amcor (Zurich, Switzerland) delivers comprehensive shrink bag solutions leveraging advanced multi-layer film technologies and a global manufacturing footprint. The company's technical expertise in barrier optimization and seal integrity serves demanding applications in meat packaging, cheese, and the pharmaceutical sectors. - Winpak Ltd. (Canada) specializes in high-quality shrink bags for food and healthcare applications, with particular strength in North American markets. The company's focus on customer service, technical support, and consistent quality standards has established strong relationships with major food processors and pharmaceutical manufacturers.

Companies Covered in Shrink Bags Market

- PREMIUMPACK GmbH

- Winpak Ltd.

- Spektar d.o.o.

- Flexopack SA

- Coveris Holdings S.A

- Bemis Company Inc.

- Schur Flexibles Group

- Atlantis-Pak Co. Ltd.

- Sealed Air Corp.

- Kureha Corporation

- Duropac

- Supralon International AG

- Amcor plc

- Berry Global Group Inc.

Frequently Asked Questions

The global shrink bags market is projected to reach US$ 5.96 Bn by 2033, growing from US$ 4.04 Bn in 2026 at a CAGR of 5.7% during the forecast period.

Increasing demand for food preservation solutions, stringent FDA and USDA regulatory requirements for packaging safety, pharmaceutical industry adoption for sterile barrier systems, and 97% of consumers reporting daily ready-made meal consumption are primary growth drivers.

Polyethylene-based materials, including LDPE, HDPE, and LLDPE, dominate with approximately 58% market share due to superior barrier properties, regulatory compliance, and cost-effectiveness across multiple applications.

North America leads the market driven by advanced cold chain infrastructure, stringent FDA and USDA regulatory frameworks, and sophisticated food processing industries requiring compliant packaging solutions.

Development of biodegradable shrink bags using PHAs, plant proteins, and algae-based plastics presents significant opportunities, addressing EU PPWR mandates requiring 35% recycled content by 2030 and capturing premium sustainability-focused market segments.