- Healthcare Services

- Septoplasty Market

Septoplasty Market Size, Share and Growth Forecast, for 2026-2033

Septoplasty Market by Indication (Deviated Nasal Septum, Correction of Cleft Defects, Enlarged Turbinates, Others), Procedure (Open Septoplasty, Endoscopic Septoplasty, Image-Guided Septoplasty, Laser-Assisted Septoplasty, Radiofrequency-Assisted Septoplasty), End‑Use (Hospitals, Ambulatory Surgical Centers (ASCs), ENT Specialists, Others), and Regional Analysis for 2026-2033

Septoplasty Market Share and Trends Analysis

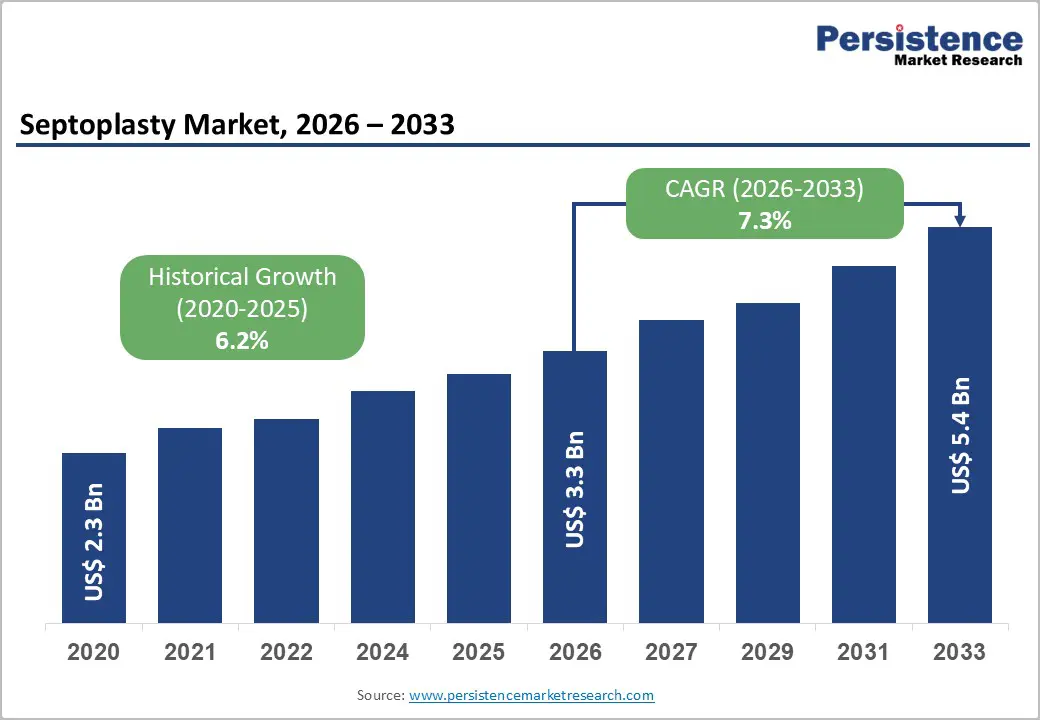

The global septoplasty market size is likely to be valued at US$ 3.3 billion in 2026, and is projected to reach US$ 5.4 billion by 2033, growing at a CAGR of 7.3% during the forecast period 2026-2033.

Market growth is being driven by demographic aging and the rising prevalence of deviated nasal septum conditions, particularly among middle-aged and elderly populations. Increasing diagnosis rates are resulting from improved awareness of chronic nasal obstruction and sleep-related breathing disorders. At the same time, continuous advancements in endoscopic septoplasty and image-guided surgical technologies are improving procedural accuracy, reducing complication rates, and shortening recovery timelines.

These clinical improvements are encouraging higher procedure volumes across hospital and ambulatory care settings. Long-term demand is being reinforced by favorable reimbursement frameworks for medically necessary septoplasty procedures in developed healthcare systems. Public and private payers are continuing to recognize septoplasty as a functional intervention rather than an elective procedure when linked to airway obstruction or sinus disease. In parallel, expanding access to ear, nose, & throat (ENT) care in emerging economies is increasing procedure uptake through improved hospital infrastructure and specialist availability. Competitive positioning is increasingly being shaped by innovation-led differentiation, including minimally invasive techniques, enhanced visualization tools, and precision instrumentation.

Key Industry Highlights

- Dominant Indication: Deviated nasal septum is set to command around 65% of the revenue share in 2026, while enlarged turbinate correction is likely to grow the fastest at 8% CAGR through 2033, supported by rising diagnostic recognition.

- Leading Procedure: Endoscopic septoplasty is expected to hold approximately 45% of the revenue share in 2026, while image-guided septoplasty is projected to grow the fastest through 2033, driven by a high demand for precision in complex and revision surgeries.

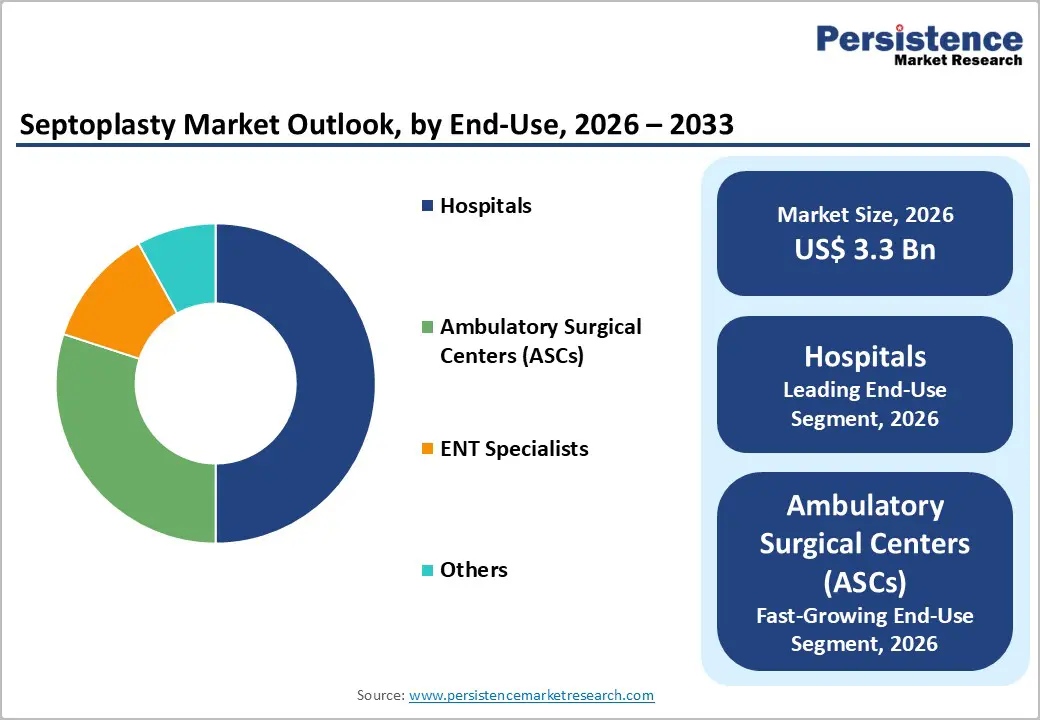

- End-Use Dynamics: Hospitals are anticipated to account for around 50% of market revenue in 2026, while ASCs are likely to expand at the fastest pace at about 8.6% CAGR through 2033, reflecting the shift toward outpatient ENT procedures.

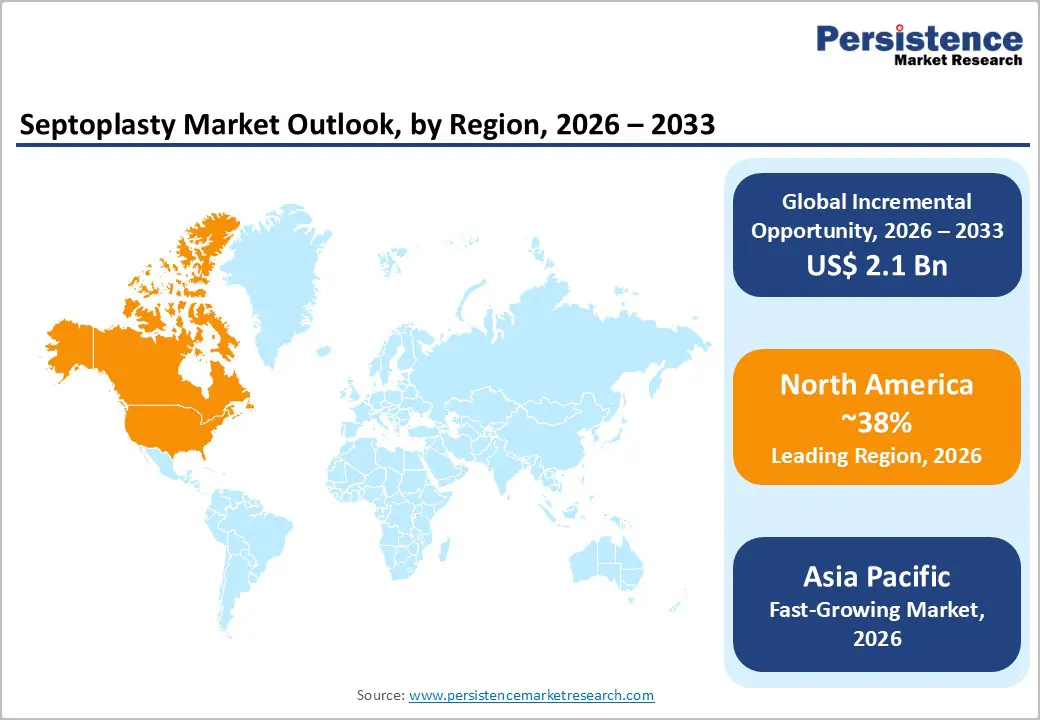

- Regional Leadership: North America is poised to lead with about 38% revenue share in 2026, while Asia Pacific is expected to register the fastest growth at 8.4% CAGR through 2033, led by expanding ENT infrastructure in China, India, and Southeast Asia.

- Competitive Environment: Market competition is shaped by technology-driven differentiation, with leading players focusing on image-guided and advanced endoscopic platforms.

| Key Insights | Details |

|---|---|

| Septoplasty Market Size (2026E) | US$ 3.3 Bn |

| Market Value Forecast (2033F) | US$ 5.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Clinical Burden of Nasal Airway Disorders and Expanding Surgical Capability

The increasing prevalence of deviated nasal septum is a primary growth driver for the global septoplasty market. According to data from the U.S. National Institutes of Health (NIH), structural nasal septal deviation affects over 60–70% of the adult population, with a significant subset experiencing symptomatic obstruction. The Laryngoscope and Otolaryngology–Head and Neck Surgery journals confirm a steady rise in clinically indicated septoplasty procedures over the past decade. Aging populations are more susceptible to chronic sinusitis and sleep-disordered breathing. These conditions frequently require surgical correction to restore nasal airflow. As a result, procedure volumes continue to increase across care settings.

Advances in surgical technology and broader healthcare access further strengthen market growth. According to the American Academy of Otolaryngology–Head and Neck Surgery (AAO-HNS), endoscopic techniques have reduced complications and shortened recovery times by up to 25–30%. Improved outcomes are encouraging both surgeon and patient adoption. Minimally invasive approaches also improve operating room efficiency. At the same time, data from the World Health Organization (WHO) and national ministries of health show rising specialist physician density in Asia Pacific. Countries including India, China, Indonesia, and Vietnam are expanding ambulatory surgical centers. This infrastructure growth is improving access to functional septoplasty procedures. These factors are converting unmet clinical need into sustained market demand.

Cost and Reimbursement Barriers Limiting Uniform Market Adoption

Despite favorable demand fundamentals, high procedural and technology-related costs remain a key restraint for the septoplasty market growth. Technology-assisted procedures require substantial capital investment in image-guided systems, powered surgical instruments, and laser platforms, increasing the overall cost of care. According to OECD healthcare expenditure data, advanced ENT surgical technologies can raise per-procedure costs by 20–35%, making adoption challenging in cost-sensitive healthcare environments. These elevated costs limit access for smaller hospitals and outpatient centers. Budget constraints further restrict procurement in publicly funded systems. As a result, technology penetration remains uneven across regions. This dynamic slows broader diffusion of advanced septoplasty solutions.

The regulatory and reimbursement variability continues to constrain market expansion. In several healthcare systems, reimbursement coverage is limited strictly to functionally indicated septoplasty procedures. Combined or borderline cosmetic cases are often excluded, reducing the addressable patient pool. In Europe, health technology assessment agencies apply stringent medical-necessity criteria that can delay approvals. These processes increase administrative burden for providers. Reimbursement inconsistency also affects investment planning for device manufacturers, augmenting revenue risk and limiting uniform market growth.

Expansion of Outpatient Care, Emerging Market Access, and Smart Surgical Technologies

The growing shift toward minimally invasive septoplasty in ASCs represents a significant market opportunity. Data from the Centers for Medicare & Medicaid Services (CMS) indicate a steady migration of ENT procedures from inpatient hospitals to outpatient settings, driven by cost efficiency, shorter recovery times, and patient preference. This transition supports higher procedure throughput while lowering system-level costs. ASCs are increasingly equipped to handle functional septoplasty cases. As a result, demand for compact, outpatient-optimized surgical technologies is rising. This creates scalable growth opportunities for device manufacturers. The outpatient trend also improves overall market accessibility.

The substantial untapped demand in high-population emerging markets, combined with rapid technological convergence, is unlocking long-term growth potential. WHO data suggests that less than 40% of patients with clinically significant nasal obstruction in South and Southeast Asia currently receive surgical intervention, highlighting a large unmet need. Improving healthcare access could unlock multi-billion-dollar incremental value over the forecast period. Convergence of digital imaging, navigation systems, and AI-enabled planning tools is also reshaping septoplasty workflows, with integrated surgical platforms enabling better outcomes and operational efficiency. These innovations support premium positioning and long-term customer retention, expanding smart technology adoption and redefining growth pathways.

Category-wise Analysis

Indication Insights

Deviated nasal septum is projected to remain the dominant indication, accounting for around 65% of septoplasty procedures in 2026 due to its high prevalence and clear functional impairment. Structural deviations are widely recognized as a primary cause of nasal airway obstruction, prompting consistent surgical referrals and established clinical pathways. Functional guidelines and medical necessity criteria support routine procedural volumes in hospitals and ENT clinics. A retrospective analysis from SVIMS?Sri Padmavathi Medical College reported that septoplasty is the most common procedure performed for symptomatic deviated nasal septum with chronic sinonasal conditions, reinforcing its role as a procedural staple. Clinical outcomes confirm consistent symptom improvement, validating operator preference and procedural volume. Routine integration of deviated nasal septum correction makes it central to indication?based market forecasts.

Enlarged turbinates is anticipated to be the fastest growing indication, expected to expand at roughly 8% CAGR from 2026 to 2033 as diagnostic standards evolve. Growing recognition of turbinate hypertrophy’s role in chronic nasal obstruction is expanding intervention volumes beyond isolated septal correction. A 2025 prospective clinical study comparing septoplasty alone versus septoplasty plus inferior turbinoplasty showed significantly better symptomatic and airflow outcomes in combined treatment cases, making the latter increasingly preferred in complex airway management. Enhanced imaging and ENT assessment protocols have improved early identification of turbinate issues, increasing surgeon confidence in integrated procedural planning. This dynamic reinforces the rapid growth trajectory of enlarged turbinate indications.

Procedure Insights

Endoscopic septoplasty is expected to lead the procedural landscape with an estimated 45% revenue share in 2026, driven by its minimally invasive profile, superior visualization, and broad clinical acceptance. Endoscopic techniques reduce tissue trauma, improve recovery times, and support integration with concurrent functional airway procedures. The AAO HNSF Global Grand Rounds webinar on advanced endoscopic sinus surgery highlighted evolving endoscopic approaches, including live demonstrations that reinforce global clinician engagement with minimally invasive septoplasty techniques. These events reflect widespread international adoption of endoscopic methods across developed and emerging ENT care settings. Real?world outcomes from clinical practice support high patient satisfaction and safety profiles, increasing surgeon preference. The global trend toward outpatient and same day surgery strengthens endoscopic septoplasty’s procedural leadership.

Image-guided septoplasty is projected to grow at approximately 9.2% CAGR through 2033, driven by increasing integration of navigation and planning technologies into ENT surgical workflows. A clear global example comes from Scarborough Health Network (SHN) in Canada, successfully completed its first surgery using the Medtronic StealthStation™ FlexENT Navigation System, providing real?time anatomical guidance for sinus and skull?base procedures with enhanced precision and safety. This implementation demonstrates how advanced image?guided systems are being adopted beyond traditional settings to improve outcomes in complex ENT surgeries. Navigation technologies help surgeons navigate delicate sinonasal anatomy, reducing operative risk. Their use for challenging sinus and nasal procedures reinforces the growing clinician preference for image?guided approaches. As navigation becomes more widely available in tertiary centers across regions, it strengthens the case for rapid procedural adoption.

End Use Insights

Hospitals are anticipated to remain the largest end?use segment with roughly 50% of the septoplasty market revenue share in 2026, supported by high procedural volumes and advanced surgical infrastructure. Hospitals serve as the primary sites for complex septoplasty cases and combined airway corrections that require multidisciplinary care and extended perioperative support. ENT device utilization data show hospitals accounted for more than 50% of total device usage, reflecting their central role in high?acuity procedures and advanced clinical workflows. Hospitals are equipped with specialized operating rooms, imaging systems, and diagnostic tools necessary for both routine and complex ENT surgeries, reinforcing their leadership. Their ability to integrate cutting?edge technologies and comprehensive care pathways enables efficient management of complications and revision cases. Hospitals also remain key centers for procedural training and dissemination of best practices.

Ambulatory Surgical Centers are projected to expand at the highest 2026-2033 CAGR, driven by cost efficiency, convenience, and broader outpatient reimbursement coverage. Industry data from ASC News and healthcare market analyses indicate a continuing shift of surgical volumes from hospitals to ASCs, highlighted by CMS expanding the list of procedures eligible for ASC reimbursement, making a wider range of surgeries viable in outpatient settings. These trends reflect a broader healthcare movement toward outpatient care and patient preference for shorter stays and lower costs. Procedural migration is supported by expanded payer and regulatory frameworks that encourage same?day surgery in dedicated outpatient facilities and value?based care models. The growing acceptance of higher acuity procedures in the ASC setting further illustrates this evolution. Financial and operational analyses show that ASCs are investing in infrastructure to accommodate expanded procedural types and patient volumes, reinforcing their position as the fastest growing end?use segment.

Regional Insights

North America Septoplasty Market Trends

North America is expected to remain the largest market for septoplasty procedures, contributing roughly 38% of the revenue in 2026, bolstered by the presence of advanced hospital infrastructure, strong reimbursement frameworks, and high procedural volumes. Adoption of minimally invasive and image-guided techniques has increased surgical precision, reduced complications, and improved recovery times. Hospitals integrate advanced surgical systems into routine workflows, efficiently managing both routine and complex septal corrections. Surgeon training programs enhance technology adoption while maintaining quality outcomes. Hospitals also serve as centers for clinical research and best-practice dissemination, reinforcing procedural consistency. The region’s innovation ecosystem fosters rapid commercialization of new devices. Procedural efficiency and technology uptake continue to drive market leadership.

Market growth in the region is reinforced by Stryker’s expansion of its microdebrider systems in multiple U.S. and Canadian hospitals, improving workflow efficiency and procedural accuracy. Integration of these devices allows higher case volumes without compromising outcomes. Combined with outpatient procedural expansion, this has strengthened North America’s market dominance. Advanced ENT systems support both complex and routine procedures seamlessly. Hospitals leverage these technologies for precision surgery and operational efficiency. Adoption of high-tech platforms increases patient throughput. Technology-driven adoption and clinical capability maintain North America’s leadership.

Europe Septoplasty Market Trends

Europe is likely to host a stable market for septoplasty during the 2026-2033 forecast period, with Germany, the U.K., France, and Spain driving procedure volumes and revenue. Structured clinical pathways and universal healthcare access support broad availability of functionally indicated septoplasty procedures. Harmonized EU regulations ensure high-quality care and safety standards while guiding device adoption. Hospitals and specialty centers increasingly implement endoscopic and minimally invasive techniques, improving outcomes and reducing recovery. Aging demographics and rising ENT disorder prevalence maintain consistent procedural demand. Training programs ensure surgical quality is preserved across institutions. Hospitals remain central to technology adoption and clinical innovation.

Clinical precision has improved with Olympus’ 4K rhinolaryngoscope with AI-assisted lesion detection, are deployed across European ENT centers. This enhances visualization during complex septoplasty and sinus procedures, integrating into workflows without disruption. Adoption supports procedural efficiency, safety, and high-quality outcomes. Incremental technology upgrades strengthen hospitals’ capability to handle both routine and revision cases. Regulatory-compliant deployment ensures broad applicability. Hospital adoption reinforces stable market performance. European ENT centers balance clinical quality with technological progress effectively.

Asia Pacific Septoplasty Market Trends

Asia Pacific is projected to be the fastest-growing septoplasty market at about 8.4% CAGR through 2033 driven by large populations, rising healthcare investment, and expanding ENT infrastructure. China, Japan, and South Korea lead in volumes, while Southeast Asia develops capacity and training programs. Urbanization and increasing disorder awareness increase procedure rates. Hospitals and outpatient centers upgrade suites to accommodate minimally invasive and image-guided septoplasty, supporting efficiency. Rising procedural volumes are matched by improved technology integration. Hospitals implement complex procedures while maintaining high safety standards. Market growth is strengthened by expanding access and clinical capability.

Brainlab’s ENT surgical navigation platform, deployed in Japan and South Korea, integrates real-time imaging and guidance for complex septoplasty. Surgeons achieve higher precision and reduced variability, embedding advanced tools into everyday practice. Increased adoption supports patient throughput and operational efficiency. These systems facilitate complex and revision procedures seamlessly. Regional hospitals leverage advanced technology to expand capacity. Clinical adoption aligns with rising patient demand. Asia Pacific’s investment in surgical technology reinforces its fastest-growing status.

Competitive Landscape

The global septoplasty market structure is moderately consolidated, with leading players such as Medtronic, Stryker, Olympus, and Brainlab together accounting for over 50% of revenue. These companies leverage strong hospital and ENT networks, validated clinical outcomes, and integrated platforms combining visualization, powered instruments, and navigation. Heavy R&D investment drives innovations in image-guided navigation, minimally invasive tools, and AI-assisted surgical planning. Adoption of advanced systems improves procedural accuracy, efficiency, and patient outcomes. Training programs and clinical support strengthen brand loyalty. Their comprehensive portfolios reinforce market dominance globally.

Regional and niche players like Karl Storz, Smith & Nephew, and CONMED focus on specialized procedures or geographic strongholds, providing targeted or cost-efficient solutions. Barriers such as regulatory approvals, clinical adoption cycles, and high capital requirements limit new entrants. However, demand for outpatient and minimally invasive procedures enables startups with workflow-focused innovations. Leading players pursue acquisitions, partnerships, and technology collaborations to expand. Smaller firms integrate advanced imaging and navigation to compete. Overall, innovation and strategic partnerships define competitive dynamics.

Key Industry Developments

- In September 2025, Brainlab officially launched its Spine Mixed Reality (MR) Navigation system in the U.S. following FDA 510(k) clearance, integrating advanced AR/MR overlays directly into the sterile field. This technology enables surgeons to visualize critical anatomy in 3D, improving procedural precision and reducing intraoperative risk. The system supports complex ENT and septoplasty procedures by enhancing navigation and real-time anatomical guidance.

- In June 2025, Medtronic received the Outstanding Company Award at the 2025 Surgical Robotics Industry Awards for its Hugo™ RAS system, Touch Surgery™ ecosystem, and Mazor™ robotic guidance technology. Hugo™ RAS and Mazor™ systems enhance procedural efficiency, accuracy, and safety in minimally invasive interventions. This milestone strengthens their market position in advanced ENT and septoplasty-relevant technologies.

- In June 2025, Spirair reported positive results from its Zephyr Study evaluating the SeptAlign™ bioabsorbable implant for deviated septum correction. Patients experienced 71.8% median improvement in NOSE scores and 60.3% improvement in SNOT-22 scores within a year. The implant allows a minimally invasive, cartilage-preserving approach that can be performed in-office under local anesthesia.

Companies Covered in Septoplasty Market

- Medtronic

- Stryker

- Olympus Corporation

- Karl Storz

- Johnson & Johnson

- Smith & Nephew

- B. Braun

- Integra LifeSciences

- Conmed Corporation

- Zimmer Biomet

- Cook Medical

- Medicon eG

Frequently Asked Questions

The global septoplasty market is projected to reach US$ 3.3 billion in 2026.

Rising prevalence of nasal airway disorders, adoption of minimally invasive and image-guided procedures, and expanding ENT infrastructure worldwide are driving the market.

The market is poised to witness a CAGR of 7.3% between 2026 and 2033.

Key opportunities include the shift to outpatient procedures, expansion of ENT services in emerging economies, and adoption of advanced surgical navigation platforms.

Medtronic, Stryker, Olympus, Brainlab, Karl Storz, Smith & Nephew, and CONMED are some of the key players in the market.