- Pharmaceuticals

- Seborrheic Dermatitis Market

Seborrheic Dermatitis Market Size, Share, and Growth Forecast, 2026 - 2033

Seborrheic Dermatitis Market by Treatment Type (Antifungal Products, Corticosteroid Lotions, Prescription-Strength Medicated Shampoos, Sulfur Products), Formulation (Tablet, Ointments, Injection, Shampoos, Creams, Gels, Others), and Regional Analysis for 2026 - 2033

Seborrheic Dermatitis Market Share and Trends Analysis

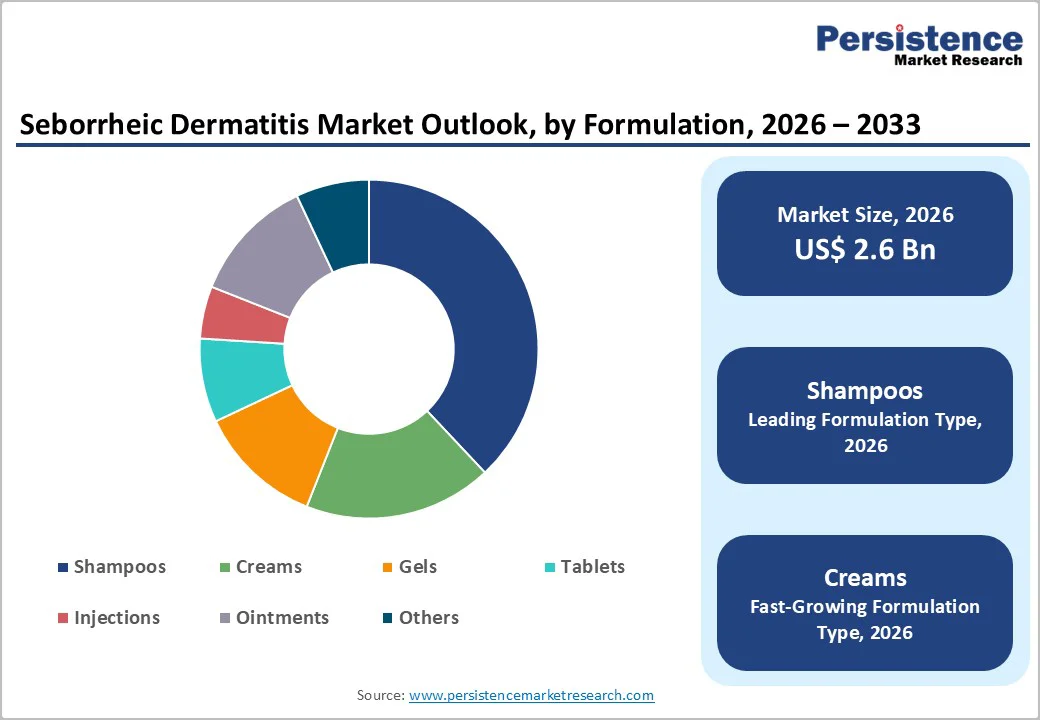

The global seborrheic dermatitis market size is likely to be valued at US$ 2.6 billion in 2026, and is projected to reach US$ 3.8 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026 - 2033.

The growing prevalence of chronic inflammatory skin conditions, expanding dermatologist-led treatment protocols, and rising demand for clinically validated scalp and facial care solutions across developed and emerging healthcare markets continue to shape the seborrheic dermatitis treatment landscape. However, the forecast period is expected to witness accelerated expansion as healthcare providers emphasize early intervention, maintenance-based treatment regimens, and broader access to prescription-strength and advanced topical therapies, supported by increasing awareness, digital dermatology platforms, and evolving clinical guidelines.

Key Industry Highlights

- Dominant Treatment Type: Antifungal products are expected to account for 42% of the market in 2026, due to their proven clinical efficacy and widespread dermatologist preference.

- Dominant Formulation: Shampoos are anticipated to lead with around 38% of the revenue share in 2026, owing to their ease of use, broad patient acceptance, and strong retail and e-commerce presence.

- Fastest-growing Formulation: Topical creams and gels are expected to record a CAGR of 6.5% through 2033, supported by targeted delivery for sensitive areas and improved skin penetration.

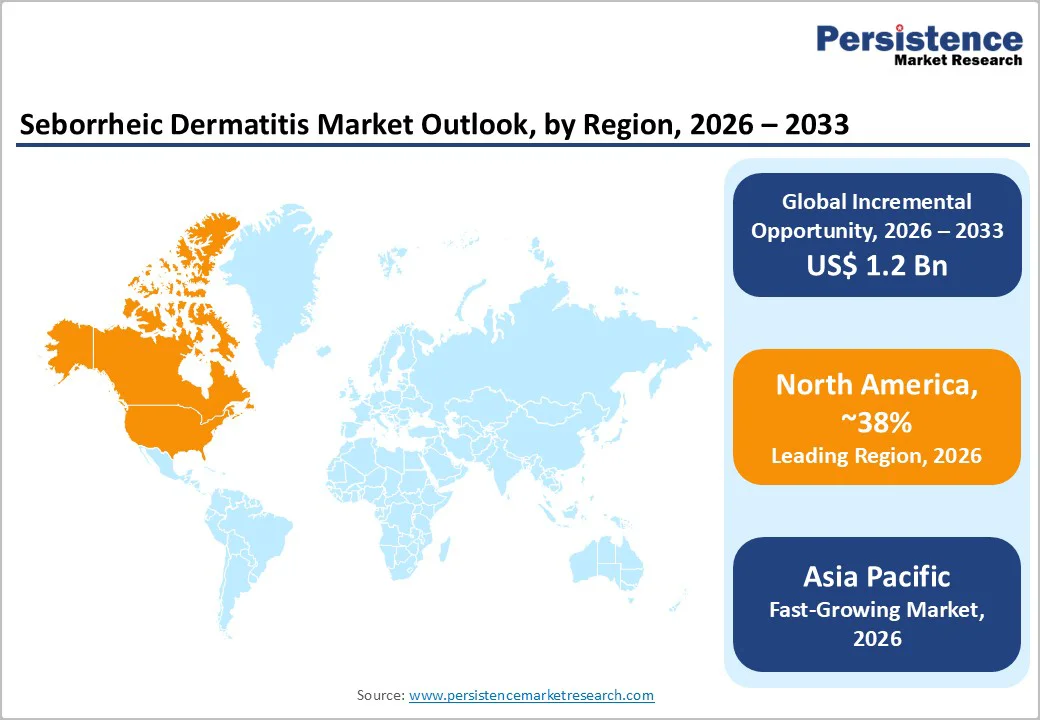

- Regional Leadership: North America is projected to hold the largest market share of 38% in 2026, driven by high diagnosis rates and advanced dermatology infrastructure.

- Clinical Guideline Endorsement: In June 2025, the American Academy of Dermatology (AAD) issued a strong evidence-based recommendation for ZORYVE® (roflumilast) cream 0.15% for adults with mild-to-moderate atopic dermatitis, citing sustained efficacy, favorable safety, and itch reduction.

| Key Insights | Details |

|---|---|

| Seborrheic Dermatitis Market Size (2026E) | US$ 2.6 Bn |

| Market Value Forecast (2033F) | US$ 3.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence and Evolving Treatment Landscape Driving Market Growth

Seborrheic dermatitis is a prevalent chronic skin condition, affecting populations around the world, with higher incidence among adults and elderly individuals. Growing awareness of skin health, improved diagnostic practices, and public education campaigns are contributing to earlier detection and higher treatment adoption rates. Urbanization, pollution exposure, and lifestyle-related stressors further elevate incidence, sustaining demand for effective therapeutic solutions. Patients increasingly seek treatments that address both symptoms and long-term skin health, creating opportunities across over-the-counter and prescription segments. The market is also supported by rising research and investment in inflammatory skin therapies and innovative clinical programs.

Simultaneously, advances in formulation, delivery, and real-world evidence are reshaping the treatment landscape. Advanced gels, creams, and medicated shampoos provide targeted antifungal, moisturizing, and anti-inflammatory therapy, improving adherence. Almirall S.A. presented 44 abstracts at EADV 2025, highlighting long-term efficacy, patient-reported outcomes, and real-world evidence across psoriasis and atopic dermatitis. Digital health platforms and teledermatology expand access to specialist care in underserved regions, while growing consumer preference for dermocosmetic and daily-care-compatible products reinforces adoption.

Treatment Costs and Long-Term Management Challenges

The high cost of prescription-strength therapies and advanced topical agents continues to limit patient access in the seborrheic dermatitis market, particularly in regions with limited healthcare coverage or inconsistent reimbursement frameworks. Out-of-pocket expenses can discourage patients from initiating or maintaining treatment, restricting the adoption of premium antifungal and steroid-sparing products. This financial barrier slows overall market growth, despite the increasing prevalence of seborrheic dermatitis and rising consumer awareness of scalp and skin health.

Moreover, the chronic and recurrent nature of seborrheic dermatitis presents ongoing management challenges. Long-term use of corticosteroid-based lotions or aggressive antifungal therapies may cause skin irritation, thinning, or discomfort, reducing patient adherence. Variability in individual response and tolerability further complicates treatment continuity. Together, these factors create structural hurdles to market expansion, affecting both the over-the-counter (OTC) and prescription segments and influencing strategic product positioning and commercial performance in key markets.

Expansion Potential through Emerging Markets and Innovative Care Solutions

The seborrheic dermatitis market offers strong expansion potential in emerging economies, particularly Asia Pacific and Latin America, where rising disposable incomes, urbanization, and growing awareness of scalp health are accelerating demand. In Asia Pacific, for example, innovations have been increasingly focused on scalp microbiome science, directly addressing Malassezia-associated conditions such as dandruff and seborrheic dermatitis. Dermocosmetic launches and ingredient innovations highlighted at industry events emphasize targeted yeast control and microbiome rebalancing, strengthening the OTC segment’s role alongside prescription therapies. These dynamics position emerging markets to deliver higher growth rates than mature markets, creating attractive entry points for both pharmaceutical and dermocosmetic players.

Concurrently, consumer demand is shifting toward science-backed, natural, and sensitive-skin-friendly formulations, including steroid-free and clean-label products. New OTC innovations, such as microbiome-targeted botanical actives and optimized antifungal ingredients such as piroctone olamine, are improving efficacy while enhancing tolerability. Digital engagement, teledermatology platforms, and online education further support adoption by bridging clinical credibility and consumer accessibility. Together, these trends enable broader reach, stronger brand trust, and premium product positioning, supporting long-term revenue growth and portfolio diversification across the seborrheic dermatitis treatment landscape.

Category-wise Analysis

Treatment Type Insights

Antifungal products are likely to remain the leading treatment segment, accounting for approximately 42% of the seborrheic dermatitis market revenue share in 2026, driven by their central role in managing yeast-driven inflammation. Ketoconazole-based therapies continue to serve as first-line treatments due to their proven efficacy and broad clinician adoption; however, the segment is gradually evolving beyond ketoconazole-only approaches. In 2025, the introduction of hypochlorous acid (HOCl)–based topical gels and advanced antiseborrheic formulations reflected growing diversification within antifungal and anti-inflammatory therapies. These innovations emphasize microbiome-friendly, steroid-free symptom control, expanding options across both prescription-adjacent and OTC categories and supporting long-term disease management.

Prescription-strength medicated shampoos are poised to be the fastest-growing treatment type, expected to register a CAGR of approximately 6.1% from 2026 to 2033. Their convenience, cost-effectiveness, and alignment with routine scalp care drive strong adoption, particularly for recurrent and maintenance-focused use. Corticosteroid lotions and combination therapies hold a smaller share due to safety considerations and short-duration use, while emerging natural and non-steroidal alternatives are gaining traction among patients seeking sensitive-skin-friendly solutions.

Formulation Insights

Shampoos are anticipated to dominate in 2026, accounting for approximately 38% of the market revenue, driven by their ease of use and alignment with routine scalp hygiene. In 2025, new clinical evidence released by Pierre Fabre confirmed that Ducray’s KELUAL DS Intensive shampoo is effective as a long-term maintenance therapy for seborrheic dermatitis, reinforcing the role of advanced antiseborrheic shampoos beyond short-term flare control. This validation has strengthened dermatologist confidence and sustained consumer adoption, particularly for recurrent scalp-focused cases. Broad availability through retail pharmacies and e-commerce platforms further supports high repeat usage and market leadership.

Topical creams, gels, and foams are set to represent the fastest-growing segment, projected to expand at a CAGR of approximately 6.5% from 2026 to 2033. Growth is driven by rising demand for non-steroidal, cosmetically elegant, and sensitive-skin-friendly options. Innovations introduced in 2025, including microbiome-conscious gels and lightweight foam delivery systems, have improved skin penetration and tolerability in hair-bearing and facial areas. These formats enhance patient adherence and are increasingly positioned as maintenance or adjunct therapies, supporting formulation diversification and incremental revenue growth across the seborrheic dermatitis market.

Regional Insights

North America Seborrheic Dermatitis Market Trends

North America is forecast to maintain its position as the dominant regional market, capturing approximately 38% of the seborrheic dermatitis market share in 2026. The United States anchors this leadership through elevated disease prevalence rates and sophisticated dermatology infrastructure. Broad insurance coverage ensures patients can access both innovative prescription medications and OTC therapies without prohibitive financial barriers. A critical competitive advantage lies in the region's rapid adoption of teledermatology platforms such as Teladoc Health, Amazon Clinic, and Hims & Hers Health. These digital providers are integrating AI-powered image triage and asynchronous consultations to enhance diagnostic accuracy. Clinician-led virtual care models improve treatment continuity for chronic inflammatory conditions, enabling patients to receive timely interventions without traditional office visits.

The regulatory framework significantly accelerates market expansion by offering streamlined approval pathways and robust intellectual property protections. This environment allows pharmaceutical developers to launch novel formulations rapidly while securing their competitive position. Digital health infrastructure further strengthens long-term disease management by connecting virtual diagnosis directly to prescription fulfillment and ongoing follow-up protocols. Forward-thinking organizations are adopting hybrid strategies that combine dual-mode portfolios with real-world clinical validation. Investments in digital therapeutics and specialty formulations are becoming essential to maintain differentiation, infusing the North America market with a steady growth momentum.

Europe Seborrheic Dermatitis Market Trends

Europe is expected to remain the second-largest regional market for seborrheic dermatitis in 2026, supported by high standards of dermatological care and broad insurance coverage. Key markets such as Germany, the U.K., France, and Spain benefit from well-established healthcare systems that enable early diagnosis and sustained treatment adoption. Growing public awareness of chronic inflammatory skin conditions and rising demand for both prescription and OTC solutions further reinforce market stability. Dermatology-specialized clinics and hospital networks play a critical role in supporting long-term disease management. The region also shows strong acceptance of dermocosmetic and sensitive-skin formulations.

The Europe market also benefits from harmonized European Union (EU) regulatory frameworks, enabling efficient cross-border product distribution while maintaining stringent safety and clinical evidence requirements. These standards enhance trust among clinicians and consumers, supporting steady uptake of approved therapies. Competitive activity includes multinational pharmaceutical companies and regional specialists focusing on localized medical education, real-world evidence generation, and formulation innovation. Incremental advancements in antifungal and anti-inflammatory treatments continue to refresh product portfolios. Digital engagement and pharmacy-based counseling further support patient adherence and elevate regional market prospects.

Asia Pacific Seborrheic Dermatitis Market Trends

Asia Pacific is expected to emerge as the fastest-growing regional market for seborrheic dermatitis, with a projected CAGR of 7.5% from 2026 to 2033. This expansion is fueled by increasing skin health awareness, rising disposable incomes, and substantial upgrades to healthcare infrastructure. Rapid urbanization across China, India, and ASEAN members is contributing to a higher incidence of seborrheic dermatitis. The demand for cost-effective, scalable treatment solutions is rising as patients seek accessible and reliable care for chronic dermatological conditions.

E-commerce and teledermatology platforms are significantly broadening access in Tier-2 and Tier-3 cities, particularly in China, where hospital–platform collaborations have enhanced store-and-forward dermatology services for chronic scalp and facial dermatitis. In Japan and South Korea, OTC and clinical product lines are converging, positioning sensitive-scalp and antifungal therapies as maintenance treatments following professional diagnosis. Regulatory alignment with global standards is lowering entry barriers for new products, encouraging both local and multinational manufacturers to invest in region-specific formulations. These developments support sustained adoption and long-term revenue growth in the Asia Pacific seborrheic dermatitis market.

Competitive Landscape

The global seborrheic dermatitis market structure is moderately consolidated, with leading players such as Johnson & Johnson, GlaxoSmithKline (GSK), Bayer, and Leo Pharma collectively controlling a substantial portion of market revenue. These companies leverage strong dermatology networks, established brand recognition, and diversified portfolios that span prescription-strength therapies, over-the-counter shampoos, and topical formulations. Heavy investment in R&D, clinical trials, and innovative formulations allows them to maintain leadership in antifungal, anti-inflammatory, and sensitive-skin-friendly product lines.

Smaller and regional players are focusing on niche segments, clean-label or steroid-free formulations, and local market penetration. Barriers such as regulatory approvals, clinical validation, and treatment safety requirements limit entry for new competitors. At the same time, digital health platforms and teledermatology solutions are enabling innovative distribution channels and improved patient adherence. Market consolidation is expected to gradually increase as leading firms acquire emerging brands or expand regionally, while strategic partnerships enhance product diversification and access to high-growth markets.

Key Industry Developments

- In October 2025, a large study conducted in the U.S. and published in Allergy revealed bidirectional links between seborrheic dermatitis and epithelial barrier diseases such as psoriasis, rosacea, and alopecia areata, supporting the epithelial barrier theory across skin, respiratory, and other systems.

- In September 2025, Arcutis Biotherapeutics’ ZORYVE® (roflumilast) won the Allure Best of Beauty Breakthrough Award, becoming the first prescription topical for atopic dermatitis, plaque psoriasis, and seborrheic dermatitis to receive this recognition. The award highlights its innovation and effectiveness in managing inflammatory skin conditions.

- In May 2025, roflumilast topical foam 0.3% (ZORYVE®) received supplemental FDA approval for the treatment of plaque psoriasis on the scalp and body in patients aged 12 years and older. This approval expands the therapeutic use of the roflumilast molecule beyond seborrheic dermatitis, providing a steroid-free, once-daily option suitable for hair-bearing areas.

Companies Covered in Seborrheic Dermatitis Market

- Johnson & Johnson

- GlaxoSmithKline plc

- Pfizer Inc.

- Bayer AG

- Merck & Co., Inc.

- Novartis AG

- Sun Pharmaceutical Industries Ltd.

- Leo Pharma A/S

- Almirall S.A.

- Arcutis Biotherapeutics, Inc.

Frequently Asked Questions

The global seborrheic dermatitis market is projected to reach US$ 2.6 billion in 2026.

Rising prevalence of seborrheic dermatitis, increasing awareness of skin health, urbanization, and expansion of dermatology access, along with innovation in antifungal and sensitive-skin-friendly formulations, are driving the market.

The market is poised to witness a CAGR of 5.6% from 2026 to 2033.

The development of hypoallergenic and clean-label products, and integration of teledermatology and digital health platforms to expand access and treatment adherence are key market opportunities.

Johnson & Johnson, GlaxoSmithKline (GSK), Bayer, Leo Pharma, Pfizer, Novartis, and Sun Pharmaceutical Industries are among the leading market players.