- Bulk Chemicals

- Sebacic Acid Market

Sebacic Acid Market Size, Share, and Growth Forecast, 2026 - 2033

Sebacic Acid Market by Derivative Type (Polyamides, Sebacic Acid (Base Form), and Sebacic Acid Ester), by End Use (Plasticizer, Lubricant & Greases, Corrosion Inhibitors, Cosmetics and Personal Care, Pharmaceuticals, Biopolymers) and Regional Analysis for 2026 - 2033

Sebacic Acid Market Size and Trends Analysis

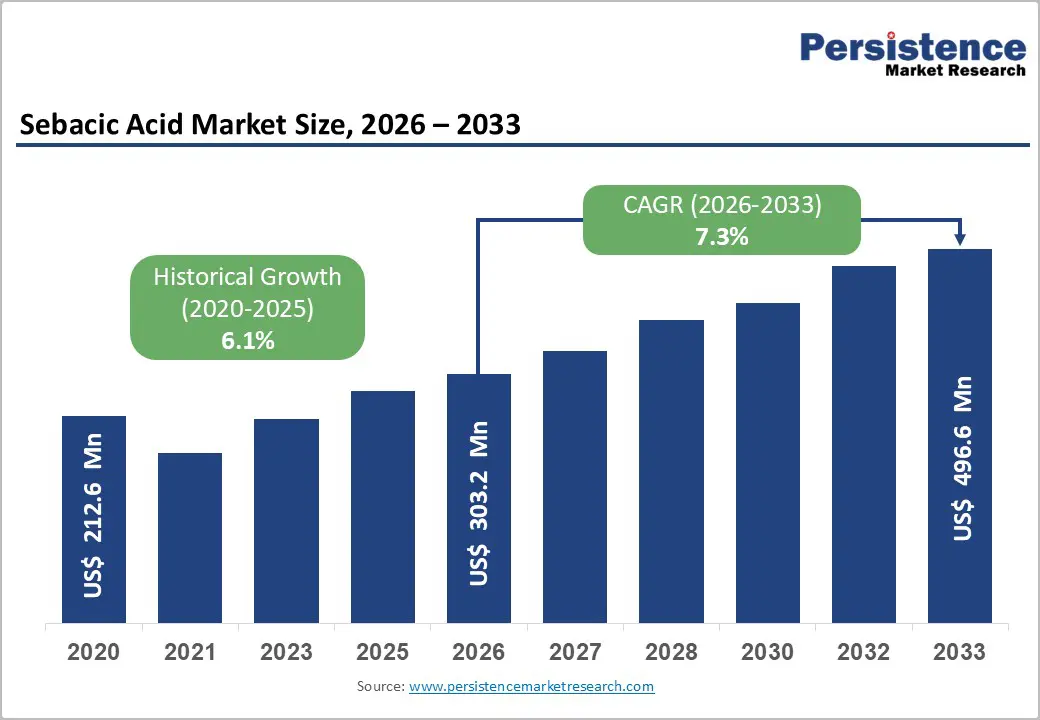

The global Sebacic Acid market size is likely to be valued at US$ 303.2 million in 2026 and is projected to reach US$ 496.6 million by 2033, registering a CAGR of 7.3%. This marks an acceleration compared to the 6.1% CAGR recorded during 2020–2026, reflecting intensifying downstream demand across bio-based polyamides, biopolymers, and specialty intermediates. Expanding bio-based polymer production, growing at double-digit rates and structurally outpacing conventional plastics, is significantly increasing sebacic acid consumption as a castor oil–derived platform chemical.

Strengthening sustainability mandates and tightening plastics regulations across Europe and Asia are further encouraging the substitution of fossil-based diacids with renewable alternatives, positioning sebacic acid as a preferred solution in green chemistry formulations. Asia Pacific continues to hold a structural advantage due to its dominance in castor cultivation and integrated polymer manufacturing, attracting new capacity additions and capital investments. According to Persistence Market Research, market growth is underpinned by rising adoption of bio-based and biodegradable materials in polymers, lubricants, cosmetics, and pharmaceuticals. Owing to its renewable origin, thermal stability, and multifunctional performance characteristics, sebacic acid is increasingly recognized as a strategic sustainable intermediate across diverse industrial value chains.

Key Industry-Highlights:

- Sebacic acid is primarily derived from castor oil, making it a sustainable and eco-friendly alternative to petrochemical-based acids.

- Bio-Based Demand Surge: Rising sustainability focus drives sebacic acid adoption in eco-friendly polyamides, lubricants, plasticizers; over 70% European automotive OEMs target 25% bio-based non-metallic content by 2030.

- Regulatory Decarbonization Push: EU plastic frameworks and carbon mandates accelerate bio-polyamides, growing 13–15% annually to 2035, embedding sebacic systems into mobility, consumer, and industrial value chains.

- China Supply Dominance: China leads global production; Hengshui Jinghua produced 35,000 tons in 2023, capturing 49% share, creating pricing power, volatility exposure, and geopolitical dependency risks.

- Renewable Nylon Leadership: PA610 and PA1010 offer 63–71% renewable carbon content, supporting lightweight automotive, electronics, and durable engineering applications worldwide.

- Cosmetics Fastest Growth: Over 120 cosmetic brands adopted bio-based ingredients in 2022/23; sebacic acid supports emollient, skin-conditioning formulations across premium personal care.

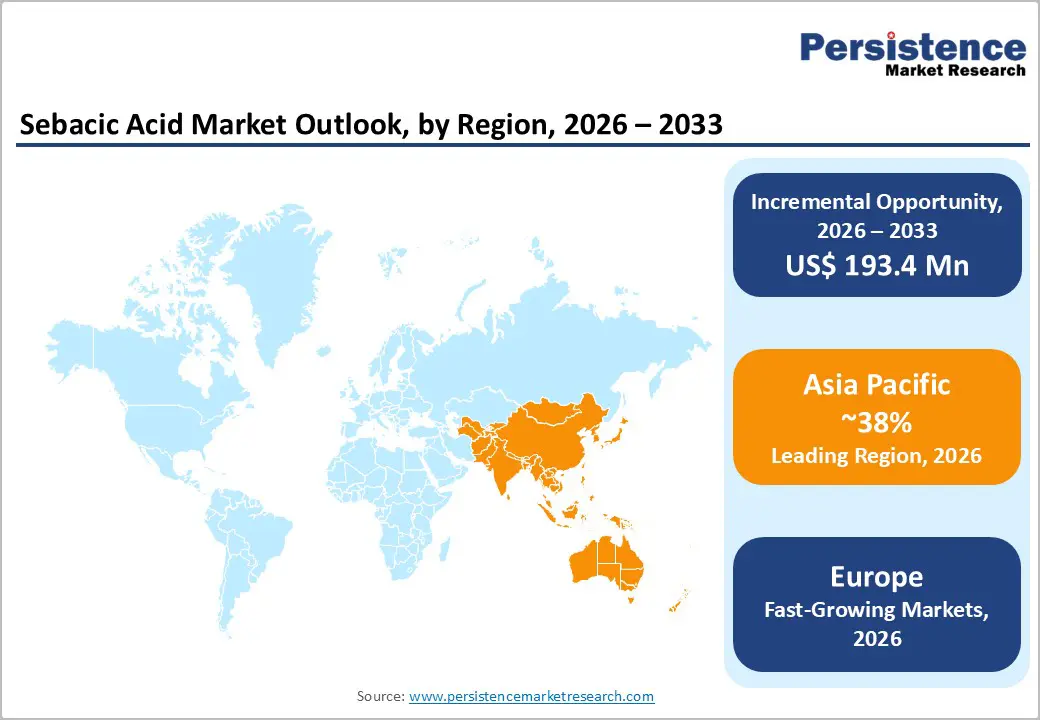

- Asia Pacific Dominance: The region accounts for over 38% demand in 2026; China produced 66,000 tons in 2023, supported by integrated castor-polymer value chains.

- Europe Fastest Growing: Europe projects 8.6% CAGR (2026–2033), producing 4.7 million tons of bio-chemicals annually, driven by circular economy mandates and automotive decarbonization targets.

- Rising use in bio-based polyamides (like PA 610 and PA 1010) boosts demand in automotive, electrical, and industrial sectors.

- Sebacic acid esters are increasingly used in high-performance, biodegradable lubricants and cold-resistant plasticizers.

- Adoption of personal care products as emollients and conditioning agents is growing, driven by consumer preference for natural ingredients.

| Key Insights | Details |

|---|---|

|

Sebacic Acid Market Size (2026E) |

US$ 303.2 Mn |

|

Market Value Forecast (2033F) |

US$ 496.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.1% |

Market Dynamics

Drivers - Growing Demand for Bio-Based and Sustainable Chemicals

The rising global focus on sustainability and environmental safety is a major driver for the sebacic acid market. Derived from renewable castor oil, sebacic acid offers a biodegradable and non-toxic alternative to petroleum-based dicarboxylic acids. Its increasing adoption in the production of eco-friendly polyamides, lubricants, and plasticizers aligns with stricter environmental regulations and growing consumer awareness.

Industries such as automotive, packaging, and personal care are actively shifting towards greener solutions, further boosting demand. More than 70% of European automotive OEMs have announced targets to incorporate bio-based materials in at least 25% of non-metallic vehicle parts by 2030.

As governments and organizations prioritize carbon-reduction and circular-economy initiatives, sebacic acid’s role as a sustainable chemical continues to expand.

Sustainability Regulation and Corporate Decarbonization Mandates

Regulatory initiatives such as the EU Single-Use Plastics framework and national carbon-reduction plans directly promote renewable, low-carbon chemistries, including bio-based sebacic acid and its derivatives. Bio-based polyamides already capture around 1% of global polymer output but are projected to grow by 13–15% annually through 2035, increasing their share in material selection for mobility, consumer, and industrial applications. Sebacic acid, produced mainly from castor oil, provides a ready-to-scale route to bio-content in high-performance polymers without compromising thermal or mechanical properties. As brand owners push toward 2030–2035 recycled and bio-content targets, sebacic-based systems become embedded in qualified platforms, raising switching costs and enabling contract-backed capacity expansions. Investors benefit from greater off-take visibility, longer contract tenors, and structurally lower demand risk relative to unregulated petrochemical chains.

Restraint - Market Concentration in China

China is the dominant global producer of sebacic acid, with production volumes significantly higher than those of any other country. Chinese manufacturers have integrated operations and produce a broad range of sebacic acid derivatives at scale. Hengshui Jinghua Chemical Co., Ltd. is one of the world's major producers of sebacic acid. In 2023, it produced and sold 35,000 tons of sebacic acid, accounting for 49% of the global market.

This concentration of production in China poses geopolitical risks and supply chain issues for global buyers. It also creates price volatility and dependency issues, especially for countries or companies looking to diversify sourcing or promote domestic manufacturing of bio-based chemicals.

Castor oil price volatility and supply concentration

Sebacic acid production depends heavily on castor oil, with a large share of global cultivation concentrated in India. Weather shocks, acreage shifts, and competing uses for castor derivatives drive multi-year swings in feedstock prices, which can exceed typical petrochemical cost volatility. When castor prices spike, unintegrated sebacic producers face margin compression as they cannot always pass through cost inflation to contract customers within a year, pressuring realised profitability even as market value grows at 7.3% CAGR. High feedstock risk raises hurdle rates for greenfield projects outside core castor-producing regions, limiting geographic diversification and reinforcing reliance on a narrow supplier base.

Opportunities - Rising Demand for Bio-Based Plasticizers in the Packaging Industry

The global shift toward safer, eco-friendly packaging materials is creating a strong opportunity for sebacic acid-based plasticizers. Traditional phthalates are increasingly restricted due to health and environmental concerns, prompting industries to adopt biodegradable, non-toxic alternatives. Over 40% of global packaging manufacturers have moved toward phthalate-free solutions in response to stricter environmental regulations, particularly in the EU and North America.

Sebacic acid esters such as dioctyl sebacate (DOS) and dibutyl sebacate (DBS) offer excellent flexibility, thermal stability, and compatibility with food-grade and medical packaging. With packaging materials accounting for over 32% of the bio-plasticizer market and mounting global regulatory pressure, the demand for sebacic acid in sustainable packaging solutions is poised to grow significantly. This presents manufacturers with a high-impact, future-forward market avenue.

Upgrading Into High-Margin Sebacic-Based Polyamides

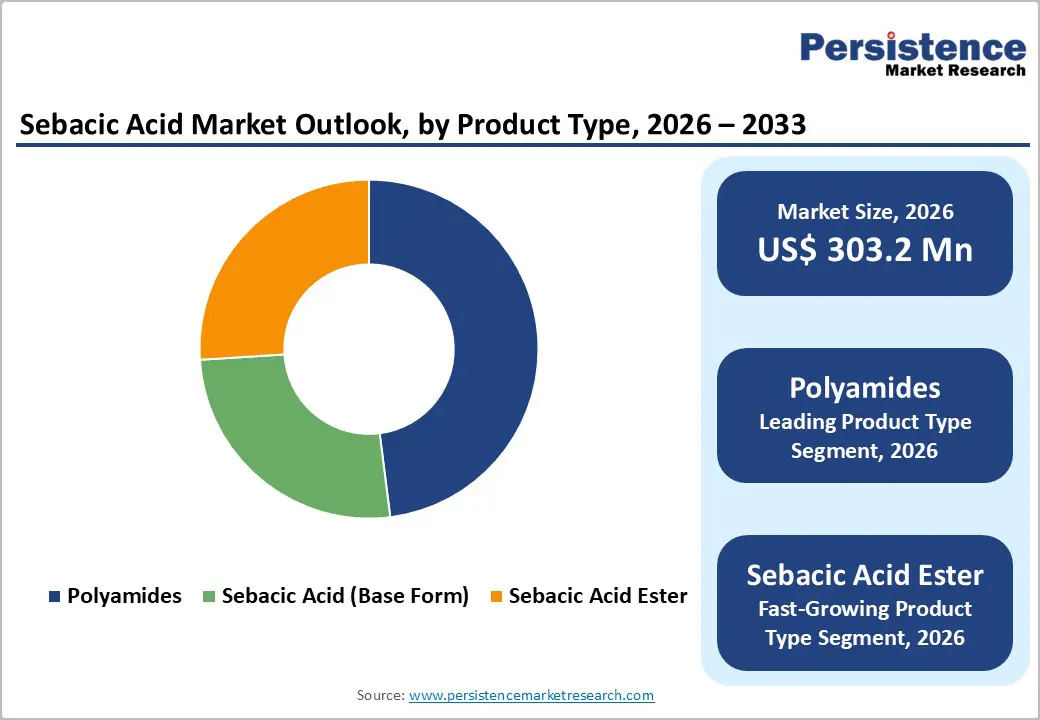

Polyamides already account for more than 40% of derivative-type demand in 2026 and sit at the top of the value chain in terms of price per tonne versus base sebacic acid. As bio-based polyamide markets expand around 8–12% annually, sebacic producers that forward-integrate into PA11, PA610, and related grades capture a disproportionate share of value growth and improve margin stability.

This shift reallocates revenue from commodity acid sales into engineered materials backed by application development, technical service, and co-innovation with automotive and electronics OEMs. For investors, integrated polyamide strategies convert the 7.3% sebacic market CAGR into higher blended revenue growth and enterprise value multiples more typical of specialty polymers than of basic chemicals.

Category-wise Analysis

Derivative Type Insights

Polyamides, particularly PA 610 and PA 1010, dominate due to their exceptional mechanical and thermal properties. These bio-based nylons offer a sustainable alternative to traditional petroleum-based polymers, making them highly attractive in industries like automotive, electronics, and consumer goods.

- PA 610 and PA 1010, derived from sebacic acid, exhibit renewable carbon content ranging from 63% to 71%.

They exhibit excellent chemical resistance, dimensional stability, and durability, which are critical in high-performance engineering applications. The increasing push for lightweight, eco-friendly materials in vehicle manufacturing and electrical components is further accelerating their adoption. As sustainability becomes central to industrial innovation, demand for sebacic acid-derived polyamides continues to surge globally.

End-user Insights

The cosmetics industry is rapidly adopting sebacic acid-based ingredients for their superior emollient and skin-conditioning properties.

- Over 120 global cosmetic brands reported using bio-based or biodegradable ingredients, including sebacic acid, in their 2022/23 product lines.

As consumers increasingly demand natural, eco-friendly products, sebacic acid's use in personal care formulations, such as moisturizers, lotions, and hair care products, is growing significantly. The shift towards plant-derived, biodegradable ingredients is driving this growth, as sebacic acid provides an alternative to petrochemical-based additives.

- Naturium Azelaic Acid Emulsion 10% is a lightweight, fragrance-free emulsion formulated with 10% azelaic acid, niacinamide, bio-retinol, and sebacic acid. Designed to brighten skin tone, reduce hyperpigmentation, and improve skin texture.

Regional Insights and Trends

Asia Pacific Leads Sebacic Acid Market Growth

Asia Pacific represents the most influential regional market for sebacic acid, driven by rapid industrialization, expanding manufacturing activity, and strong availability of bio-based feedstock. China and India are the primary contributors, with China emerging as a leading producer. In 2023, China’s bio-based sebacic acid production reached approximately 66,000 tons, reinforcing its global supply position. The region accounted for over 38% of global sebacic acid demand in 2026 and hosts a majority of large-scale production facilities.

A key structural advantage lies in Asia Pacific’s robust agricultural base, particularly castor cultivation in India, which supports a vertically integrated castor–sebacic acid–polymer value chain. This integration lowers production costs, enhances export competitiveness, and ensures feedstock security. Further expansion of the automotive, textile, packaging, and consumer goods industries further stimulates downstream demand for polyamides, plasticizers, lubricants, and personal care ingredients.

Rising consumer preference for sustainable and bio-based materials, especially in automotive and cosmetics applications, continues to strengthen regional demand. Although regulatory frameworks increasingly emphasize sustainability, policy support remains focused on industrial expansion and value-added chemical exports. High industry concentration among integrated producers enables economies of scale but also exposes the market to agricultural and climate-related risks affecting castor output.

Europe Sebacic Acid Market Driven by Sustainability

Europe is witnessing robust growth in the sebacic acid market, driven by rising demand across the automotive, cosmetics, specialty polymers, and performance chemicals industries. The region’s strong commitment to sustainability and bio-based chemical adoption remains a primary growth catalyst, with Europe producing nearly 4.7 million tons of bio-based chemicals annually, reflecting its significant contribution to global output. Countries such as Germany, France, and Italy are leading innovation, supported by heavy investments in research and development to expand sebacic acid applications in high-performance lubricants, bio-based polyamides, plasticizers, and eco-friendly personal care formulations.

Europe is projected to be the fastest-growing regional market, with demand expected to grow at a CAGR of 8.6% from 2026 to 2033, driven by stringent climate targets and circular-economy regulations. European Union policies aiming to reduce plastic waste by 55% by 2030 and accelerate automotive decarbonization are encouraging the shift toward recyclable and low-carbon bio-based intermediates. However, limited castor cultivation results in dependence on imports, pushing investments toward downstream processing, certification, and specialty compounding capabilities while exposing the market to policy-driven demand fluctuations.

Competitive Landscape

The sebacic acid market features a combination of large integrated manufacturers and specialized producers, creating a moderately concentrated competitive landscape. The top five companies-primarily established Asian and European players—control a significant portion of global production capacity. Market participants are actively expanding capacities and adopting advanced processing technologies to meet rising demand for bio-based chemicals. Strategic collaborations across automotive, packaging, polymer, pharmaceutical, and personal care industries are strengthening value-chain integration and customer alignment. Entry barriers remain notable due to reliance on castor oil feedstock supply chains, strict environmental regulations, and the need to deliver high-purity, application-specific grades. Vertically integrated producers benefit from stronger cost control and pricing power, while pricing dynamics fluctuate based on agricultural cycles and specialty-grade premiums across downstream derivatives.

Key Industry Developments:

- In January 2026, Arkema started up its new Rilsan® Clear transparent polyamide unit in Singapore, tripling its global production capacity. The US$20 million investment strengthens its Specialty Materials portfolio and supports rising demand for high-performance transparent polyamides across advanced industrial applications.

- In November 2025, Evonik announced the expansion of long-chain polyamide production at its Shanghai Multi-User Site in China, doubling capacity. The new production line, operational from December 2025, targets sports equipment and new energy vehicles to meet growing Asian demand.

- In October 2025, Syensqo launched Kalix LD-4850 BK000, a low-density high-performance polyamide developed for the consumer electronics sector, enhancing lightweight performance, durability, and processing efficiency to address evolving technological requirements.

- In September 2025, BASF introduced Ultramid® H33 L, the world’s first thermoplastic polyamide with high water permeability, combining mechanical strength with moisture transmission and enabling pure polyamide artificial sausage casings, showcased at the Düsseldorf plastics trade fair.

- In 2024, Arkema announced additional investments in high-performance bio-based polyamide capacity in Asia, building on its Rilsan and related platforms to serve the electric-vehicle and consumer-applications markets.

Companies Covered in Sebacic Acid Market

- HENGSHUI JINGHUA CHEMICAL CO., LTD.

- BASF SE

- Emery Oleochemicals

- Nanjing Chemical

- Tianxing Biotechnology Co., Ltd.

- JAYANT AGRO-ORGANICS LIMITED

- ITOH Oil Chemicals Co., Ltd.

- Hokoku Corporation

- Arkema

- Wincom Inc.

- Sigma Aldrich

- Mitsubishi Chemical

- Kraton Corporation

- Fujian Zhongke

- SABIC

- Oxea GmbH

Frequently Asked Questions

The Sebacic Acid market is estimated to be valued at US$ 335.4 Mn in 2026.

The primary demand driver for the Sebacic Acid market is accelerating adoption of bio-based polyamides and biodegradable polymers, driven by stringent sustainability regulations, circular economy targets, and rising preference for renewable feedstock-derived materials.

In 2026, the Asia Pacific region will dominate the market with an exceeding 38% revenue share in the global Sebacic Acid market.

Polyamides dominate the sebacic acid derivative landscape in 2026, accounting for over 40% of revenue, supported by robust demand from engineering plastics, automotive components, high-performance fibers, and specialty industrial applications.

The Sebacic Acid market is characterized by the presence of leading manufacturers and integrated oleochemical players such as HENGSHUI JINGHUA CHEMICAL CO., LTD., BASF SE, Emery Oleochemicals, Nanjing Chemical, Tianxing Biotechnology Co., Ltd., JAYANT AGRO-ORGANICS LIMITED, ITOH Oil Chemicals Co., Ltd., and Hokoku Corporation, collectively driving global supply, product innovation, and downstream integration strategies.