- Specialty & Fine Chemicals

- Scratch Resistant Coating Market

Scratch Resistant Coating Market Size, Share, and Growth Forecast, 2026 – 2033

Scratch Resistant Coating Market by Product Type (Polyurethane Coatings, Epoxy Coatings, Acrylic Coatings, Ceramic Coatings, Others), Substrate type (Plastics, Glass, Metals, Wood, Others), Application (Automotive, Electronics, Construction, Optical, Industrial, Others), and Regional Analysis for 2026-2033

Scratch Resistant Coating Market Share and Trends Analysis

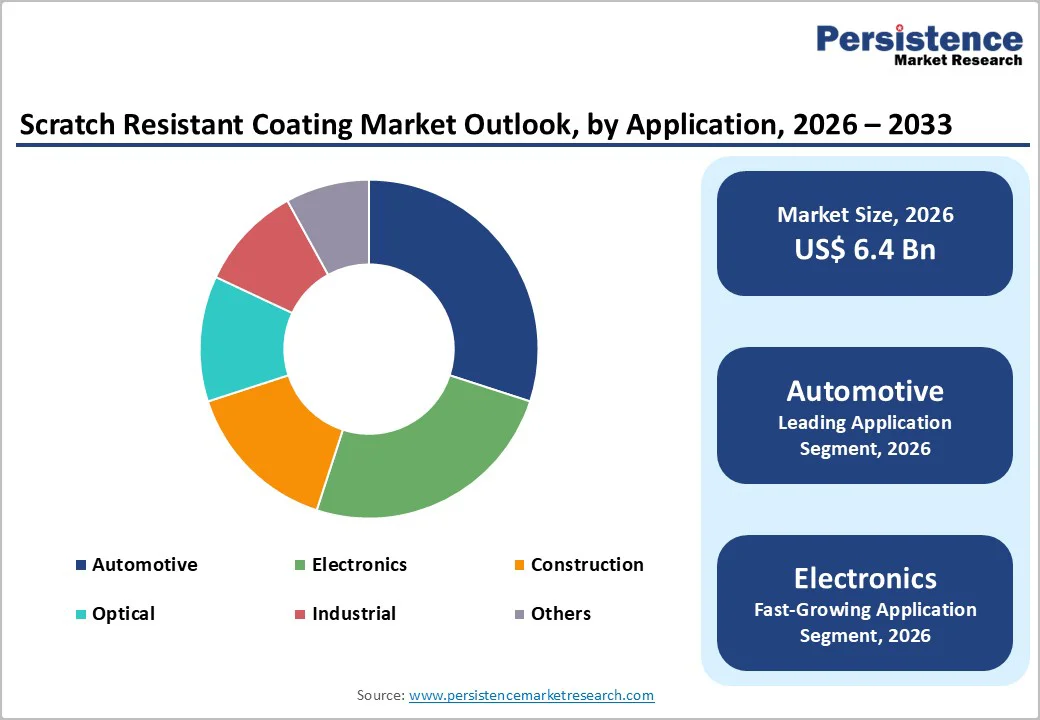

The global scratch resistant coating market size is likely to be valued at US$ 6.4 billion in 2026, and is projected to reach US$ 9.3 billion by 2033, growing at a CAGR of 5.5% during the forecast period 2026−2033. Rising demand for durable surface protection across automotive, electronics, construction, and optical applications, supported by steady advances in coating chemistry and substrate compatibility. Increasing penetration of lightweight plastics and high-value glass in end-use industries has structurally increased demand for abrasion-resistant solutions that extend product lifecycle and reduce maintenance costs. Regulatory pressure to improve product durability and reduce waste generation has further strengthened adoption, particularly in developed economies. From a technology standpoint, ceramic-based and hybrid polymer coatings have demonstrated improved hardness, transparency, and environmental compliance, enabling broader commercial scalability. Emerging manufacturing hubs in Asia Pacific are reinforcing supply availability while reducing unit costs.

Key Industry Highlights

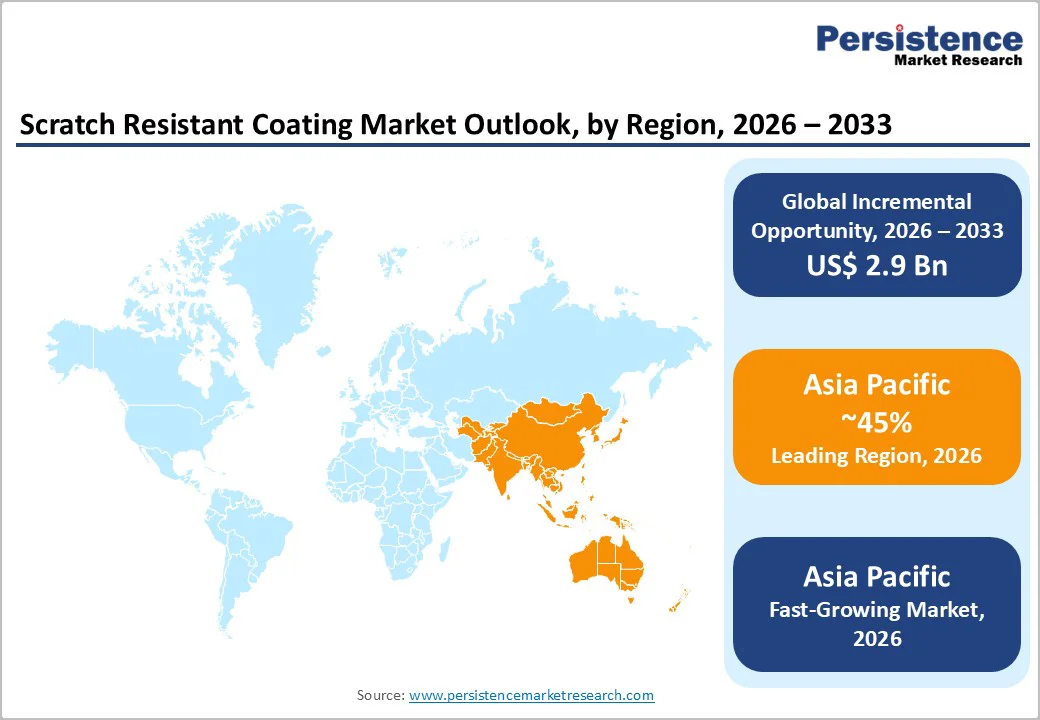

- Dominant Region: By 2026, Asia Pacific is projected to lead the market with about 45% share, driven by strong automotive and electronics manufacturing.

- Fastest-growing Regional Market: Asia Pacific is set to be the fastest-growing regional market from 2026 to 2033, fueled by rising electronics demand, urbanization, and adoption of advanced durable coatings.

- Application Leadership: Automotive applications are expected to hold an approximate 30% market share in 2026, supported by increasingly complex vehicle designs and a strong demand for durable, premium finishes.

- Fastest-growing Application: Electronics applications are set to be the fastest-growing segment through 2033, fueled by the widespread demand for scratch-free displays and integration of high-performance coatings.

- June 2025: SUNY Polytechnic researchers developed eco-friendly hydroxyapatite coatings from biowaste via pack cementation for enhancing the strength, biocompatibility, and wear resistance of dental implants.

| Key Insights | Details |

|---|---|

| Scratch Resistant Coating Market Size (2026E) | US$ 6.4 Bn |

| Market Value Forecast (2033F) | US$ 9.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Demand for Advanced Coating Solutions from Automotive and Electronics Sectors

Automotive manufacturers prioritize surface durability as vehicles integrate larger glass areas, painted plastics, and high-gloss interiors. Frequent touch points, environmental exposure, and long ownership cycles raise expectations for appearance retention. Scratch-resistant layers protect lightweight substrates used for efficiency targets, limiting rework and warranty claims while preserving brand perception. Electrified platforms amplify this need through expansive displays and piano-black trims that show defects quickly. Procurement teams favor solutions that stabilize quality across high-volume lines and reduce total lifecycle cost.

Electronics production centers on tactile interfaces where visual clarity signals product value. Screens, lenses, and casings face abrasion during assembly, logistics, and daily use. Coatings extend usable life and sustain optical performance without adding bulk, supporting slim form factors and yield discipline. According to International Data Corporation, global smartphone shipments reached about 1.17 billion units in 2023, evidence of scale that magnifies minor surface defects into major financial risk. Decision makers adopt protection technologies to safeguard margins, shorten refurbishment cycles, and maintain premium positioning.

Hardness–flexibility Balance to Limit Coating Versatility

Regulatory and compliance complexity restrains growth by forcing manufacturers to meet stringent environmental and safety standards that vary widely across regions. For example, coatings producers must comply with volatile organic compound (VOC) limits set by bodies such as the U.S. Environmental Protection Agency (EPA), where violations can lead to penalties of up to US$ 47,357 per day per violation under current federal VOC regulations. These requirements demand extensive testing, documentation, certification, and product reformulation, all of which increase development costs and delay market entry.

Different regional frameworks, such as European Union (EU)’s REACH, U.S. Clean Air Act, and other local standards, create fragmentation that complicates global supply chains. Manufacturers must tailor formulations to meet local limits and invest in compliance infrastructure, diverting resources from innovation and scaling operations effectively. Small and medium enterprises struggle most, as the cost and expertise required to navigate these varied regulations reduce competitive agility and slow growth.

Adoption of Eco-Friendly and Water-Based Coatings

The adoption of eco-friendly and water-based coatings offers a key opportunity as environmental regulations tighten and sustainability expectations rise among end-users. Water-based formulations minimize environmental impact and reduce workplace health hazards. Manufacturers adopting these coatings enhance brand credibility while ensuring compliance with global sustainability standards. End-users increasingly seek coatings that deliver high performance alongside ecological responsibility.

Advances in polymer chemistry enable water-based coatings to provide scratch resistance and durability comparable to traditional solvent-based options. For example, in February 2025, Cosmo Specialty Chemicals launched OGR 145B and OGR 145S water-based barrier coatings as sustainable alternatives to polyethylene, offering superior oil/grease resistance, FDA compliance, and heat-seal options for food packaging. This balance of performance and sustainability drives adoption across automotive, construction, and industrial sectors. Companies leveraging these coatings can differentiate themselves in the market, attract environmentally conscious clients, and foster long-term loyalty, positioning their offerings in line with the growing global emphasis on sustainable and responsible industrial practices.

Category-wise Analysis

Product Type Insights

Polyurethane coatings are poised to dominate, with a forecasted market share of 35% in 2026, supported by exceptional flexibility, impact resistance, and cost-performance balance. Their widespread application in automotive interiors, electronics housings, and industrial equipment ensures stable demand. Reliable raw material supply and established application methods further strengthen their leading position, making them the preferred choice across industries. Strong industry trust and long-standing performance track record continue to reinforce their market dominance.

Ceramic coatings are estimated to be the fastest-growing segment from 2026 to 2033, propelled by superior hardness, thermal stability, and optical clarity. Increasing adoption in automotive exteriors, displays, and optical lenses is supported by technological advancements and declining processing costs. Expansion beyond premium applications drives growth, positioning ceramic coatings as a key segment for high-performance and durable surface protection solutions. Rising demand for scratch-resistant and long-lasting coatings further accelerates their market uptake.

Substrate Type Insights

Plastics are projected to capture about 38% of the scratch resistant coating market revenue share in 2026 due to their light weight, flexibility, and replacement of heavier materials such as metals and glass in automotive parts, electronic housings, and consumer products. Scratch-resistant coatings boost surface toughness, which supports wider use in demanding environments. Mature production techniques and steady industrial needs solidify plastics as the top substrate option for manufacturers seeking cost-effective durability. Businesses should leverage this dominance by optimizing coating formulations for plastic substrates to secure reliable performance and competitive margins in high-volume applications. ?

Glass substrates will grow at the fastest rate from 2026 to 2033, fueled by rising applications in touchscreens, building facades, and precision optics. Superior coating adhesion combined with optical clarity drives commercial success in electronics and construction sectors that prioritize long-term resilience and aesthetic appeal. Ongoing innovations in surface treatments meet the demand for premium, abrasion-proof finishes in upscale products. Developers targeting this trajectory can prioritize glass-compatible solutions to tap into expanding markets where visual excellence and structural integrity command higher value.

Application Insights

Automotive applications are expected to account for roughly 30% of the market in 2026, supported by strict original equipment manufacturer (OEM) durability requirements and the rising complexity of modern vehicles. Scratch-resistant coatings improve the life of exterior trim and the robustness of interior surfaces, which lowers maintenance costs and reduces warranty claims. Growing consumer preference for premium finishes, lasting appearance, and high-quality materials is increasing demand across passenger cars, commercial fleets, and specialty vehicles. With mature production methods and expanding global vehicle output, automotive remains the leading segment, ensuring continued strength in this space. ?

Electronics applications are set to grow at the fastest pace through 2033, driven by rising global shipments of smartphones, tablets, laptops, and other consumer devices. Demand for scratch-free, visually attractive displays is pushing wider adoption of advanced protective coatings. Continuous product innovation, shorter replacement cycles, and a stronger focus on device durability and premium screen quality are creating strong growth momentum. Electronics manufacturers are increasingly using high-performance coatings to extend product life and improve user satisfaction, making this segment a key growth engine in the coming years.

Regional Insights

North America Scratch Resistant Coating Market Trends

North America is projected to emerge as the fastest-growing regional market for scratch resistant coatings during the 2026–2033 forecast period, supported by strong adoption across automotive, electronics, and industrial sectors. Stringent durability and safety standards from OEMs and regulatory authorities push manufacturers to integrate advanced coatings in vehicle exteriors and interiors. Research and development capabilities enable production of coatings with superior scratch resistance, chemical stability, and aesthetic appeal. Expansion of electric vehicles and autonomous technologies increases demand for durable polymer and glass components. Collaborations between coating manufacturers and OEMs accelerate innovation, reinforcing competitive edge and adoption rates.

The regional market also benefits from advanced industrial infrastructure and rapid technology adoption, creating favorable conditions for coating deployment. Growth in consumer electronics, including smartphones, tablets, and wearables, increases demand for scratch-resistant displays and housings. Focus on eco-friendly, water-based formulations reduces environmental impact. Increasing urbanization and construction activity boosts coating use for architectural glass and industrial equipment. Combined with strong investment in production facilities and advanced manufacturing, market growth is propelled by technological innovation, regulatory compliance, and demand for high-performance coatings.

Europe Scratch Resistant Coating Market Trends

Europe holds a significant position in the scratch resistant coating market landscape, underpinned by advanced manufacturing capabilities, strict regulatory standards, and high consumer focus on product quality and durability. The automotive and electronics sectors lead demand, as manufacturers prioritize surface protection for polymer and glass components to enhance longevity and aesthetic appeal. Expansion of electric vehicles, luxury automotive segments, and precision electronics drives adoption, while government initiatives promoting sustainable and low-VOC coatings encourage the use of eco-friendly formulations across industrial applications.

The market here is also witnessing steady growth due to increasing urbanization, construction projects, and demand for premium architectural finishes. Technological innovation in coating formulations enhances scratch resistance, chemical stability, and optical clarity, meeting rising expectations for high-performance surfaces. Electronics, industrial equipment, and automotive components increasingly integrate advanced coatings to improve service life and reduce maintenance. Strategic partnerships between manufacturers and end-users accelerate commercialization, enhancing market efficiency and expanding adoption of advanced scratch-resistant coating solutions across Europe.

Asia Pacific Scratch Resistant Coating Market Trends

By 2026, Asia Pacific is expected to lead with an estimated 45% of the scratch resistant coating market share, propelled by large-scale automotive and electronics manufacturing in China, Japan, South Korea, and India. The regional market stands to gain from integrated supply chains, cost-effective raw material availability, and widespread use of polymer and glass substrates that require high-performance coatings to enhance durability and visual appeal. Collaboration between coating manufacturers and OEMs enables localized innovation and faster commercialization of scratch-resistant technologies, strengthening market leadership. Government initiatives supporting advanced manufacturing and quality standards further consolidate the region.

Asia Pacific is also poised to be the fastest-growing market for scratch resistant coatings during the 2026–2033 forecast period, driven by rising demand for consumer electronics, expanding urban infrastructure, and increasing disposable income across emerging economies. Rapid adoption of advanced displays, automotive interiors, and optical devices accelerates coating application. Growing emphasis on long-lasting finishes, combined with lower production costs and flexible manufacturing, fuels investment and positions the region as both dominant and highly dynamic.

Competitive Landscape

The global scratch resistant coating market structure exhibits moderate fragmentation, with the top five players accounting for approximately 45% of global revenue. Leading companies maintain competitive positions through technology leadership, diversified end-use exposure, and global distribution networks. Key players driving market dynamics include PPG Industries, Inc., Akzo Nobel N.V., BASF, Sherwin-Williams, Nippon Paint (India) Private Limited, and Axalta Coating Systems, leveraging strong R&D capabilities and broad product portfolios to meet growing demand across automotive, electronics, and industrial sectors. Strategic collaborations and innovation pipelines further reinforce their positions globally.

These companies focus on developing coatings with superior scratch resistance, chemical stability, and eco-friendly formulations to capture evolving consumer and industrial requirements. Expansion into emerging markets and investment in advanced manufacturing facilities support scalability and rapid market penetration. By addressing high-performance demands across multiple end-use sectors, these players drive overall market growth. Continuous innovation, product differentiation, and global distribution strategies strengthen their competitive advantage in a moderately fragmented market landscape.

Key Industry Developments

- In November 2025, Diamond Quanta announced it will debut Adamantine Optics™, an engineered diamond-integrated antireflective coating, at CES 2026 Eureka Park to deliver superior scratch resistance, durability, and optical clarity for consumer electronics and precision optics. It has been co-developed with Heller Industries and ExtenD Co. Ltd. using hot-filament chemical vapor deposition (HFCVD), enabled with drop-in integration with existing manufacturing lines.

- In September 2025, PPG introduced PPG HI-GARD® Non-Methanol hard coating for 1.5 standard index ophthalmic lenses as a drop-in replacement for methanol-based solutions, maintaining equivalent scratch resistance while enhancing worker safety and regulatory compliance. The formulation integrates seamlessly with existing systems to reduce toxicity exposure under EU REACH and U.S. OSHA standards.

- In May 2025, AkzoNobel launched a "sunscreen" thermal insulation coating system in China featuring a radiative cooling topcoat and aerogel mid-coat that reduces building surface temperatures by up to 10% in summer. The low-VOC, water-based solution mitigates urban heat islands by reflecting solar heat and emitting infrared radiation to space, promoting energy-efficient sustainable buildings.

Companies Covered in Scratch Resistant Coating Market

- PPG Industries, Inc.

- Akzo Nobel N.V.

- BASF

- Sherwin-Williams

- Nippon Paint (India) Private Limited.

- Axalta Coating Systems

- Jotun

- Evonik

- DSM

Frequently Asked Questions

The global scratch resistant coating market is projected to reach US$ 6.4 billion in 2026.

Rising demand for durable, high-performance surfaces across automotive, electronics, and industrial applications is driving the market.

The market is poised to witness a CAGR of 5.5% from 2026 to 2033.

Growing preference for eco-friendly, water-based coatings and advanced technologies for high-performance, durable surfaces is opening novel opportunities for market players.

PPG Industries, Inc., Akzo Nobel N.V., BASF, Sherwin-Williams, Nippon Paint (India) Private Limited, and Axalta Coating Systems are few of the key players in the market.