- Medical Devices

- Scleral Lens Market

Scleral Lens Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Scleral Lens Market By Lens Type (Mini-scleral, Full Scleral), Material (Rigid Gas Permeable Scleral Lens, High-Dk Polymers), Application, Distribution Channel, and Regional Analysis for 2025 - 2032

Scleral Lens Market Size and Trends Analysis

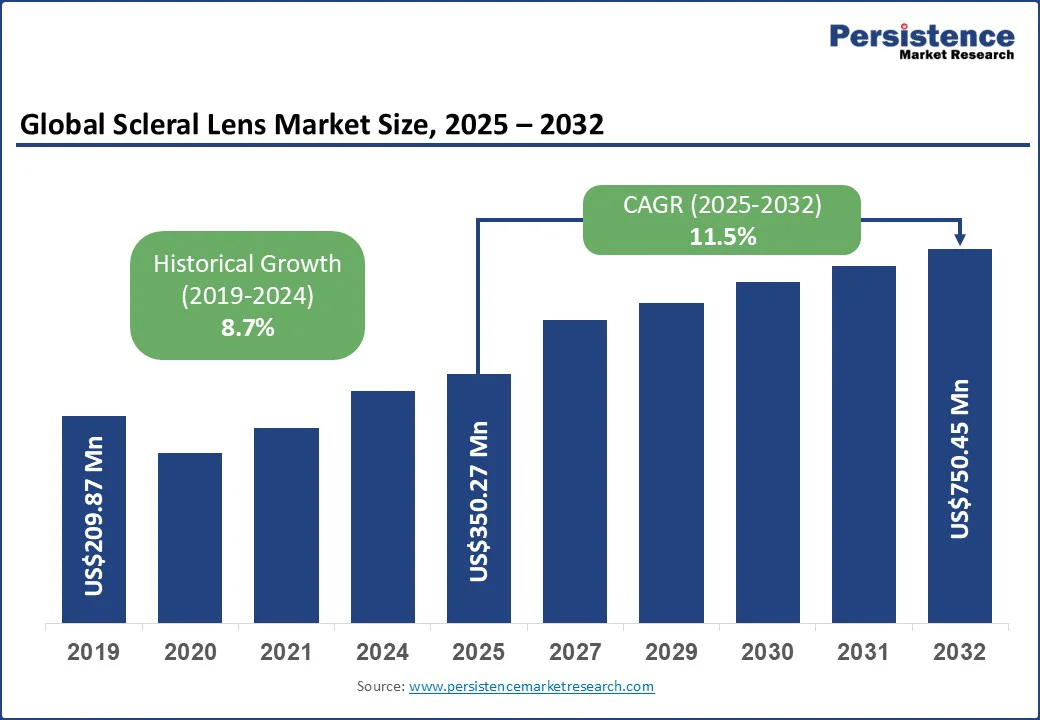

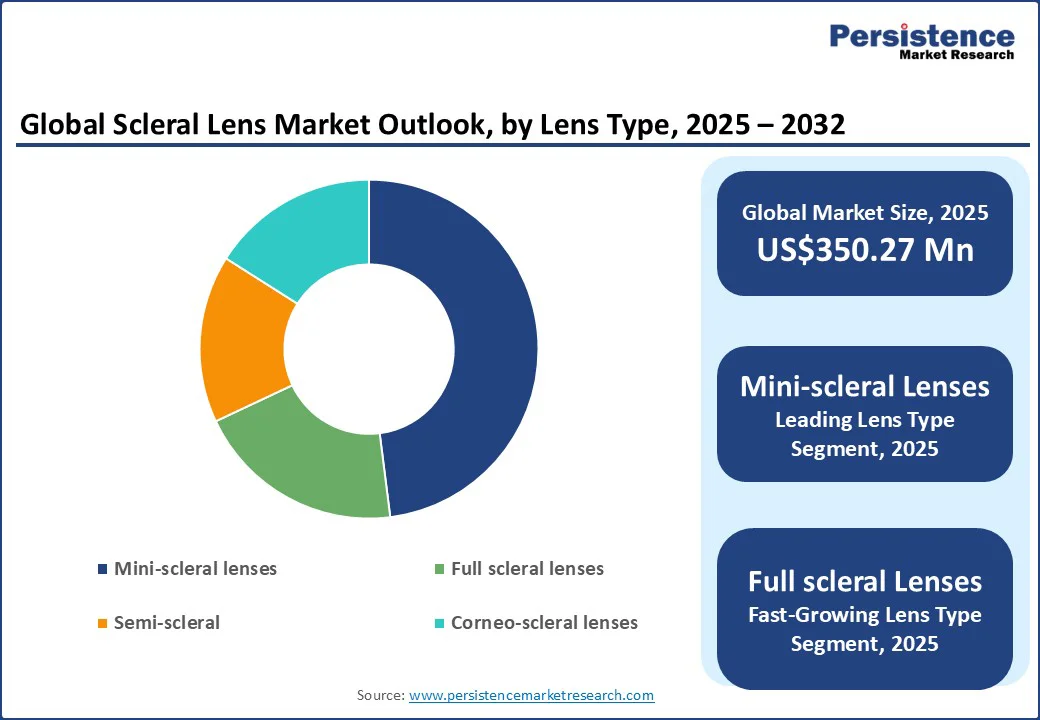

The global scleral lens market size is likely to be valued at US$350.27 Mn in 2025 and is expected to reach US$750.45 Mn by 2032, growing at a CAGR of 11.5% during the forecast period from 2025 to 2032.

The scleral lens market is gaining strong traction as a specialized segment within the contact lens industry, driven by the prevalence of corneal disorders, keratoconus, and ocular surface diseases that require advanced vision correction solutions.

Key Industry Highlights

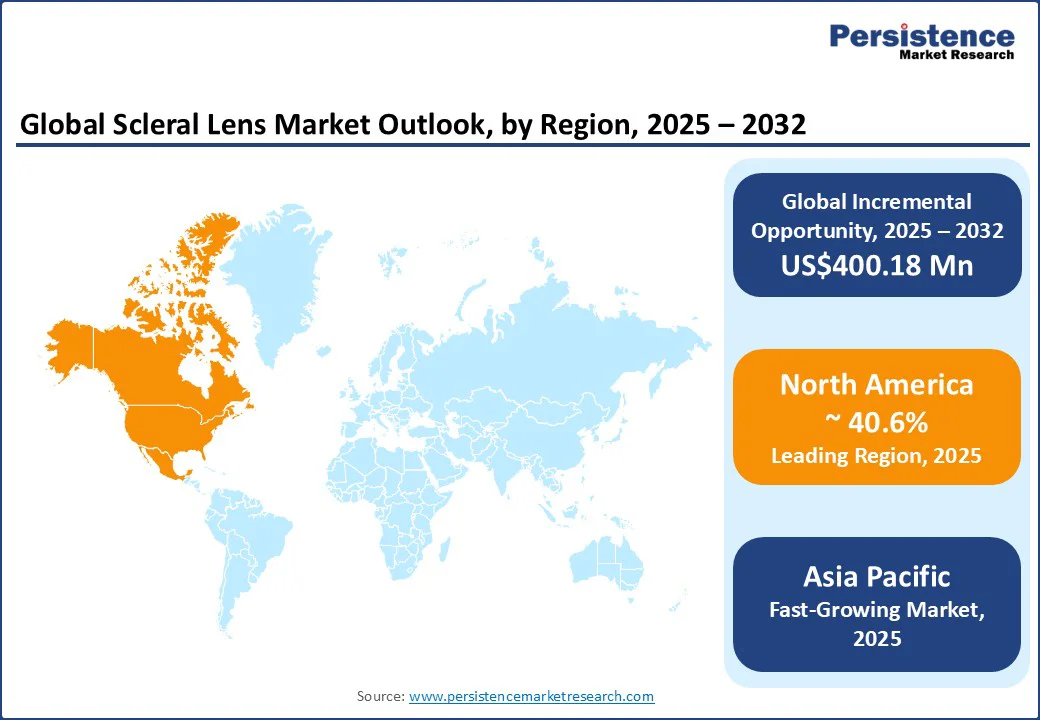

- Leading Region: North America is expected to lead the market with a 40.6% share, driven by its advanced healthcare infrastructure, a well-established network of eye-care professionals, and high patient awareness.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing region in 2025, driven by rapid urbanization, rising disposable incomes, and growing awareness of advanced eye care options.

- Dominant Lens Type: Mini-scleral lenses are expected to lead the market with a 48.4% share in 2025, driven by their optimal balance of performance and user-friendliness.

- Leading Material: Rigid gas permeable (RGP) silicone-acrylate lenses are expected to lead the material segment with approximately 42% of the market share, owing to their long-standing clinical use, excellent optical clarity, and dependable oxygen permeability at a cost-effective price.

|

Global Market Attribute |

Key Insights |

|

Scleral Lens Market Size (2025E) |

US$350.27 Mn |

|

Market Value Forecast (2032F) |

US$750.45 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

11.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.7% |

Unlike conventional lenses, scleral lenses arch over the cornea and rest on the sclera, offering greater comfort and optical performance for patients with irregular corneal conditions. The market growth is further driven by rising adoption among patients who are intolerant to standard contact lenses, along with innovations in lens design and materials. More eye care professionals offering scleral lenses are helping them become an important part of the specialty eye care market.

Market Dynamics

Driver - Precision Imaging and Therapeutic Benefits Drive Scleral Lens Use in Complex Eye Conditions

Scleral lenses are increasingly used in complex cases such as post-corneal transplant recovery, severe dry eye, and ocular surface diseases, including Stevens-Johnson syndrome and graft-versus-host disease. Their unique vaulting design allows the lens to create a fluid reservoir between the lens and cornea, which helps maintain constant hydration while protecting delicate tissue. This therapeutic effect not only improves comfort and vision quality but also reduces complications linked with epithelial disruption, making scleral lenses a preferred option in advanced clinical settings.

Recent adoption of anterior-segment optical coherence tomography (OCT) and corneoscleral topography has transformed the way scleral lenses are fitted. These imaging technologies allow eye care professionals to map the ocular surface with high precision and design lenses that align perfectly with the sclera and corneal vault. This digital approach minimizes the need for repeated trial fittings, ensures greater first-fit success, and provides tailored solutions for patients with irregular corneas.

Restraint - Limited Specialist Access and Usability Issues Hinder Wider Scleral Lens Adoption

Scleral lenses often face limited market reach due to the scarcity of expert practitioners proficient in high-precision free-form fitting techniques, especially in rural or emerging regions. Fewer than 15 % of optometrists possess the requisite profilometer-aided scleral vault mapping, leading to significant access disparities.

Due to insufficient clinic equipment, patients recount being stuck with poorly fitting lenses or having doctors abandon the fitting process after prolonged attempts. This supply-side bottleneck of qualified scleral-fitting specialists creates a constraint that cannot be solved merely by product innovation and needs sustained practitioner training and infrastructure.

Another restraint lies in the manual dexterity required for self-insertion and hygiene, which becomes especially challenging for patients with motor limitations. The larger diameter lenses, while being clinically advantageous, demand precise handling using plungers or “tripod” finger techniques, which can be frustrating and discourage continued use.

Strict cleaning protocols, including specialized disinfectants and meticulous rinsing routines, create a barrier to broader adoption. Many users cite the lens care regimen as cumbersome, noting that long-term compliance issues pose risk factors such as microbial keratitis. These everyday usability trials define a distinct, patient-centric restraint unrelated to cost or regulation.

Opportunity - Digital Customization and Tele-Optometry Drive Scalable Growth of Scleral Lenses Worldwide

Advances in 3D printing and digital design are creating new opportunities for truly personalized scleral lenses. Technologies such as free-form impression-based scleral designs and precision-manufactured customized scleral vaults allow lenses to conform to even the most complex corneal and scleral shapes.

This is particularly valuable for patients with irregular surfaces due to conditions such as keratoconus or post-surgical ectasias. By improving fit accuracy, reducing trial-and-error sessions, and shortening production timelines, these innovations are enabling eye care providers to deliver faster, more reliable solutions that enhance patient satisfaction.

The growth of tele-optometry follow-ups and e-commerce-based scleral lens refills is creating new opportunities, particularly in Asia Pacific and other underserved regions. Patients can now receive their initial clinical fitting in specialized centers and continue with virtual check-ups, remote monitoring, and seamless digital re-ordering of lenses.

This hybrid approach reduces barriers to specialty eye care while improving convenience for patients who might otherwise face long travel times or limited access to trained practitioners. As distribution networks strengthen in emerging economies, this model is well-positioned to expand the adoption of scleral lenses.

Category-wise analysis

Lens Type Insights

Mini-scleral lenses are likely to lead, accounting for around 48.4% of the market share in 2025. Their dominance is due to a balance between performance and ease of use. With diameters ranging from 15 to 18 mm, they provide sufficient corneal vaulting and a tear reservoir while remaining relatively easy to insert, remove, and fit compared to full-sized scleral lenses.

This makes them highly appealing to both practitioners and patients, especially for managing irregular corneas and moderate ocular surface conditions. Strong adoption in optometry practices and positive patient experiences further drive their demand.

Full scleral lenses currently represent a smaller market share but are projected to be the fastest-growing segment, with a high CAGR expected through 2032. These larger lenses, typically 18-24 mm in diameter, are indispensable in complex cases such as severe keratoconus, post-corneal transplant care, and advanced ocular surface diseases.

Their ability to provide a large, stable tear reservoir makes them critical for patients with significant corneal irregularities. Recent improvements in high-Dk materials have helped overcome concerns about oxygen permeability, supporting wider adoption in hospital ophthalmology departments and tertiary care centers.

Material Insights

Rigid gas permeable (RGP) silicone-acrylate lenses are anticipated to dominate, contributing around 42% of the global market share in 2025. Their leadership is driven by decades of clinical familiarity, proven optical clarity, and reliable oxygen permeability at a relatively affordable cost.

These lenses are widely available, easy to manufacture at scale, and trusted by practitioners for a broad range of indications. This combination of performance, cost-effectiveness, and practitioner confidence has established RGP materials as the backbone of the scleral lens industry.

Looking ahead, the fastest-growing material segment is high-Dk fluoro-silicone-acrylate polymers, which are projected to grow at a CAGR of nearly 12.7%. These advanced materials offer significantly higher oxygen permeability, making them particularly valuable for larger-diameter full scleral lenses and extended wear applications.

Many of these lenses also feature hydrophilic surface treatments that reduce fogging and deposit build-up, improving patient comfort and long-term wearability. Although more expensive than traditional RGP materials, they are increasingly preferred in specialty practices where ocular physiology and premium performance take priority.

Regional Insights

North America Scleral Lens Market Trends - Technological Advancements and Strong Clinical Infrastructure

North America is expected to lead the market with a 40.6% share, driven by its advanced healthcare infrastructure, a well-established network of eye-care professionals, and high patient awareness. The region benefits from favorable reimbursement policies that make specialty lenses more accessible to patients with corneal disorders.

Over the past two years, new product launches and technological advancements have further reinforced the market's leadership position. For instance, Bausch + Lomb introduced Zenlens ECHO in the U.S., a custom scleral lens designed for patients with advanced corneal conditions. Similarly, Visionary Optics released the Europa Tangent design in 2023, based on data from over 10,000 fittings, offering greater customization and comfort for wearers.

The U.S. holds a significant position in the North American market, accounting for about half of all scleral lens prescriptions. Its advanced infrastructure, research focus, and specialized training programs for practitioners have created an environment where new lens technologies can be adopted quickly.

Canada also represents a strong market, but access is more fragmented due to provincial differences in insurance coverage. While practitioner awareness is high, patients often face significant out-of-pocket costs because scleral lenses are frequently classified as elective or non-covered products. Despite this, Canada’s market continues to expand steadily, particularly in urban centers where advanced fitting clinics are concentrated.

Asia Pacific Scleral Lens Market Trends - Rapid Urbanization and Rising Practitioner Training Fuel

Asia Pacific is emerging as the fastest-growing market for scleral lenses. The region is being shaped by rapid urbanization, rising disposable incomes, and a growing awareness of advanced eye-care solutions. Governments and healthcare providers are increasingly investing in practitioner training and pediatric keratoconus screening programs, particularly in countries such as India and China.

Local manufacturing hubs in Southeast Asia are also strengthening supply chains, reducing lead times, and ensuring wider availability of lenses. The LV Prasad Eye Institute in India became a key partner of BostonSight in offering PROSE scleral lenses, marking an important step toward expanding treatment access across South and Southeast Asia.

India has become the largest market in South Asia, representing nearly 60% of the regional share. The growth is largely fueled by a combination of high unmet need for keratoconus management and the increasing number of skilled practitioners trained in scleral lens fitting.

Centers such as LVPEI in Hyderabad are seen as pioneers in this field and have become referral hubs for complex cases. China is also experiencing robust growth, driven by higher diagnosis rates of corneal disorders in urban hospitals and increasing demand from the rising middle class.

However, access remains uneven, as some regions still lack scleral lens fitting services and rely on rigid gas-permeable lenses instead. Despite these gaps, both India and China are expected to play pivotal roles in driving global market expansion over the next decade.

Europe Scleral Lens Market Trends - Precision Fitting Technologies and Expanding Reimbursement Bolster Regional Adoption

Europe is witnessing strong growth, supported by strong healthcare systems, widespread clinical adoption, and emerging reimbursement frameworks. Germany, the U.K., and France are among the leading markets, with each country playing a distinct role in shaping regional demand.

BostonSight partnered with Spanish company Conóptica to expand manufacturing and distribution of its PROSE scleral lenses across Southern Europe. Alongside this, Germany has become a hub of technological innovation, with widespread use of computer-assisted corneal topography and digital vault designs, enabling highly precise fittings.

Germany stands out as Europe’s largest market, capturing nearly 45% of the region’s scleral lens demand. Growth in this region is driven by robust healthcare systems, widespread clinical adoption, and the emergence of supportive reimbursement frameworks.

The U.K. is another important growth driver. Its combination of academic-industry collaborations, training programs for optometrists, and early diagnosis initiatives under the NHS has made scleral lenses more widely accessible. Private clinics are also reporting a steady increase in demand, particularly among patients with keratoconus and dry eye disease, solidifying the UK’s position in the regional market.

Competitive Landscape

The global scleral lens market is moderately consolidated, with a mix of global players and specialized niche manufacturers competing through product innovation and customization capabilities. Leading companies such as Bausch + Lomb, Visionary Optics, BostonSight, and Blanchard Lab dominate the market with advanced designs, high-Dk materials, and strong practitioner training programs.

Their competitive strength lies in offering highly customizable lens geometries and expanding distribution networks across North America and Europe. Strategic partnerships, such as BostonSight’s collaboration with Conóptica in Spain, are also helping companies expand reach in underserved geographies.

At the same time, smaller independent laboratories and regional manufacturers are capturing market share by catering to local fitting needs and offering cost-effective alternatives. In the Asia Pacific region, collaborations with eye institutes such as LV Prasad in India are creating growth opportunities for both local and international players.

The competition is increasingly being driven by technological integration in scleral lens fitting, including digital corneal mapping and AI-assisted fitting software, which are becoming key differentiators for market leaders.

Key Industry Developments

- In May 2025, Bausch + Lomb launched the Zenlens Chroma HOA, a wavefront-guided scleral lens featuring SmartCurve and Bi-Elevation technologies. Designed to correct higher-order aberrations (HOA) such as halos and glare, this lens offers enhanced visual clarity for patients with complex corneal irregularities.

- In February 2025, ABB Optical Group unveiled the DELTA Scleral lens, a next-generation design aimed at simplifying and enhancing the fitting process for eye care professionals.

Companies Covered in Scleral Lens Market

- Bausch + Lomb

- Visionary Optics

- BostonSight

- ABB Optical Group

- Blanchard Lab (part of CooperVision Specialty EyeCare)

- Art Optical Contact Lens, Inc.

- AccuLens

- EssilorLuxottica

- Menicon Co., Ltd.

- SynergEyes, Inc.

- TruForm Optics, Inc.

- Innovative Sclerals (ISC)

- ALDEN Optical

- Optikal Contact Lens Inc.

- SEED Co., Ltd. (Japan)

- Cantor & Nissel Ltd. (UK)

- Paragon Vision Sciences

- Medmont International

- Contamac Ltd.

- Lagado Corp.

Frequently Asked Questions

The scleral lens market is expected to be valued at US$350.27 Mn in 2025.

By 2032, the scleral lens market is projected to reach US$750.45 Mn.

Key trends include the adoption of profilometry-based scleral lens fitting, growing use of high-Dk polymer lenses for enhanced oxygen transmission, expansion of mini-scleral lenses for broader patient groups, and increasing investments in wavefront-guided customization for improved visual outcomes.

By lens type, full scleral lenses hold the largest market share due to their stability and widespread use in advanced corneal conditions. By material, rigid gas permeable scleral lenses (RGP) dominate owing to their durability and proven clinical effectiveness.

The scleral lens market is forecasted to grow at a CAGR of 11.5% from 2025 to 2032.

Key players include Bausch + Lomb, Visionary Optics, ABB Optical Group, BostonSight, and Art Optical Contact Lens, Inc.