- Hardware & Software IT Services

- SCADA Market

SCADA Market Size, Share, and Growth Forecast, 2026 - 2033

SCADA Market by Component (Hardware, Software, Services), Deployment (On-Premises, Cloud-Based, Hybrid), Industry (Energy & Utilities, Food & Beverage, Manufacturing, Oil & Gas, Transportation & Infrastructure, Water & Wastewater, Others), and Regional Analysis for 2026 - 2033

SCADA Market Size and Trends

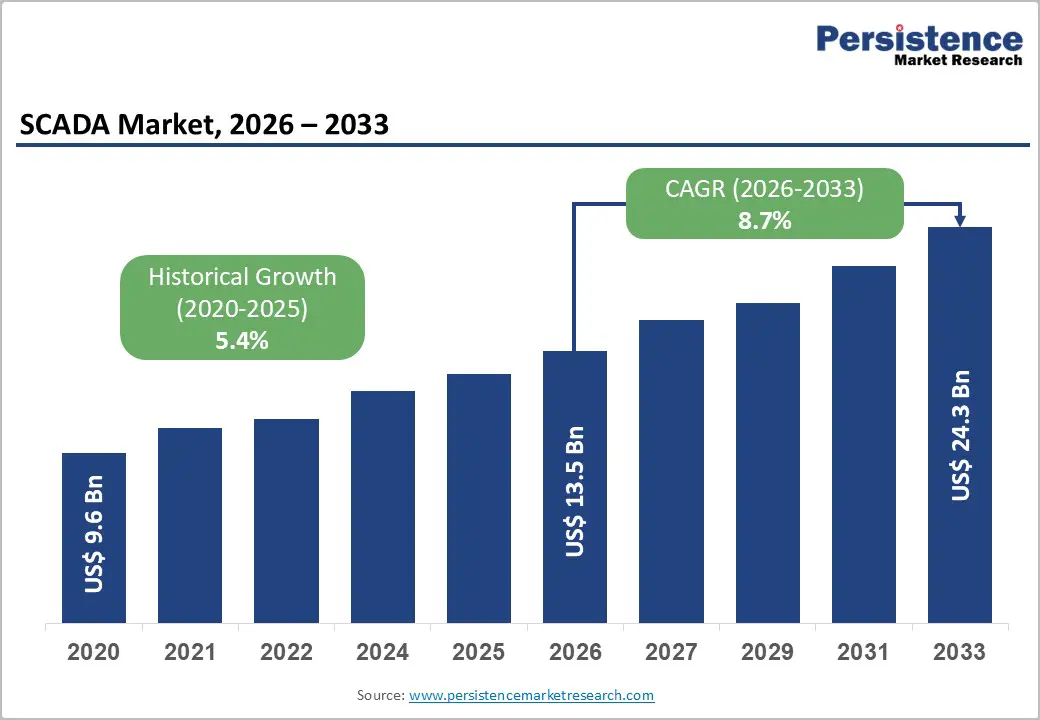

The global SCADA (Supervisory Control and Data Acquisition) market size is projected to rise from US$13.5 Bn in 2026 to US$24.3 Bn by 2033. It is anticipated to witness a CAGR of 8.7% during the forecast period from 2026 to 2033, driven by increasing industrial automation, critical infrastructure monitoring needs, and growing adoption of real-time data analytics across sectors.

Governments and industries are investing heavily in digital transformation and smart grid systems, which inherently rely on SCADA platforms for operational visibility. The rise in cybersecurity awareness and regulatory mandates for industrial control systems is accelerating adoption across both developed and emerging economies. The convergence of operational technology (OT) with information technology (IT) has further elevated the strategic importance, reinforcing robust long-term market expansion.

Key Industry Highlights:

- Leading Component: Hardware dominates with over 53% market share in 2026, valued at more than US$ 7.2 Bn, driven by demand for RTUs, PLCs, and field devices across industrial automation and grid modernization projects. Software is the fastest-growing due to the rising adoption of AI-powered analytics, cybersecurity solutions, and interoperable platforms.

- Leading Deployment: On-premises holds over 49% share in 2026, exceeding US$ 6.6 Bn, as critical industries prioritize control, reliability, and data security. Cloud-based SCADA is the fastest-growing deployment model, driven by lower capex, scalability, and increasing adoption of IoT-enabled remote monitoring solutions.

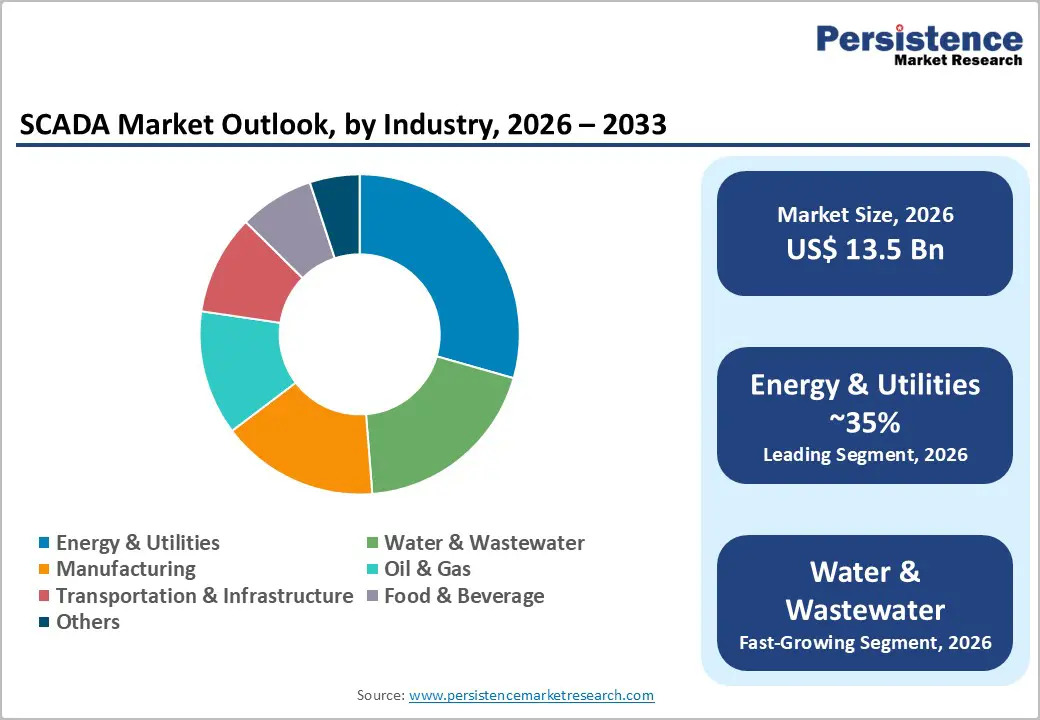

- Leading Industry: Energy & Utilities lead with over 35% share in 2026, valued at more than US$ 4.7 Bn, due to heavy reliance on SCADA for grid monitoring, renewable integration, and asset management. Water & Wastewater is the fastest-growing segment with a leading CAGR, driven by smart water management, regulatory compliance, and infrastructure modernization needs.

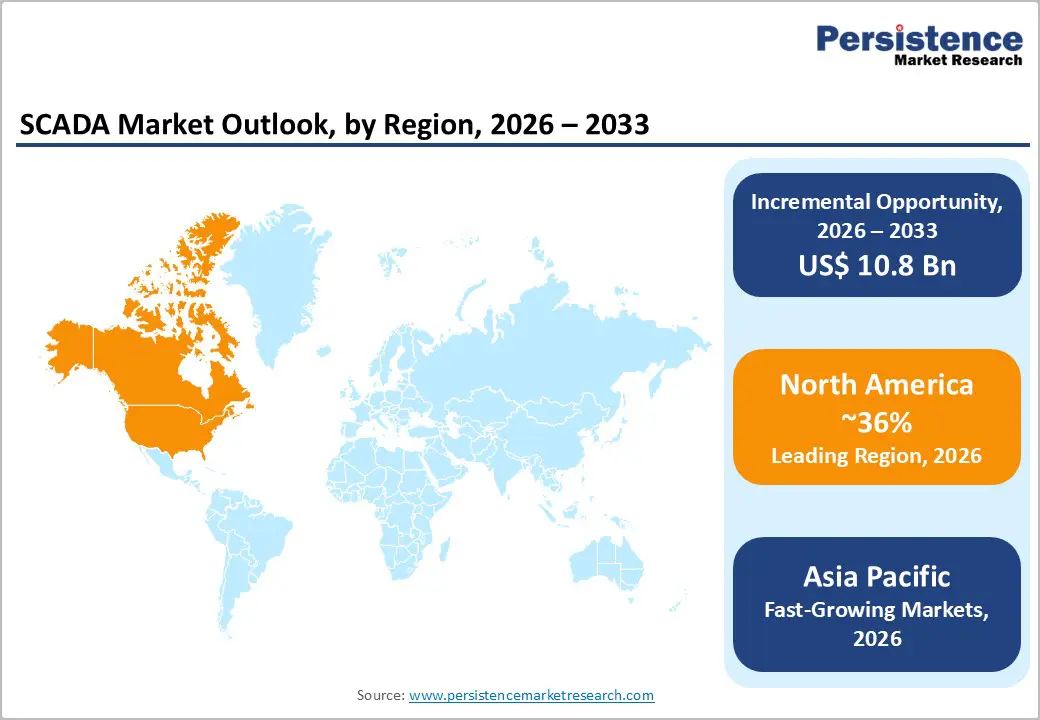

- Leading Region: North America is projected to lead with over 36% share in 2026, supported by strong regulatory frameworks and infrastructure investments such as the US$ 65 billion IIJA program. Asia Pacific is the fastest-growing region driven by industrialization, smart city initiatives, and large-scale grid modernization in China and India.

| Key Insights | Details |

|---|---|

| SCADA Market Size (2026E) | US$13.5 Bn |

| Market Value Forecast (2033F) | US$24.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Dynamics

Driver - Grid Modernization and Rising Energy Automation

National and regional utilities are investing heavily in transmission and distribution (T&D) automation, substation digitalization, and integration of distributed energy resources, all of which depend on SCADA for real-time telemetry, remote switching, and outage management. Global installed renewable energy capacity is projected to increase almost 4 600 GW between 2025 and 2030, significantly increasing the complexity of grid operations and the need for advanced supervisory control platforms. Programs such as the EU Green Deal, U.S. clean energy tax credits, and smart grid funding in various regions are catalyzing the deployment of SCADA for monitoring solar farms, wind parks, and energy storage assets, thereby structurally expanding the addressable market in power generation and T&D networks.

Industry 4.0, IoT, and Data-Driven Operations

Manufacturers are increasingly synchronizing SCADA with PLC, MES, and ERP systems to gain unified visibility over production lines, equipment health, and inventory flows, supporting higher overall equipment effectiveness (OEE) and lower downtime. The adoption of industrial IoT sensors and edge devices, combined with advanced analytics, allows SCADA systems to capture high-frequency process data and enable predictive maintenance, ultimately reducing unplanned outages and maintenance costs. Cloud-enabled SCADA and edge computing architectures now allow secure remote access, scalable data storage, and advanced AI-driven decision support, which are particularly attractive for multi-site enterprises and critical infrastructure operators aiming for centralized operations centers.

Restraint - Cybersecurity Vulnerabilities in Connected OT Environments

SCADA systems become more interconnected and IP-enabled, they expose industrial operations to a broader range of cyber threats. Critical infrastructure sectors are increasingly targeted, raising concerns over system integrity and operational safety. High-profile cyber incidents have intensified regulatory scrutiny and compliance requirements. Organizations are compelled to deploy advanced security measures such as OT-specific firewalls and intrusion detection systems. The resulting rise in cybersecurity investment creates a financial burden, particularly for cost-sensitive operators in developing regions.

High Integration Complexity and Legacy System Interoperability Challenges

Integrating modern SCADA platforms with legacy industrial systems remains a major challenge for many organizations. Older infrastructure often relies on proprietary communication protocols that are not easily compatible with current open-standard technologies. This lack of interoperability complicates system upgrades and modernization efforts. Migration projects tend to be time-consuming, requiring extensive customization and careful planning to avoid disruptions. The risk of downtime and operational inefficiencies discourages many industries from transitioning to advanced SCADA solutions.

Opportunity - Cloud-Based SCADA Adoption in Water and Wastewater Utilities

Water and wastewater utilities, historically among the most conservative adopters of digital technology, are increasingly embracing cloud SCADA due to shrinking IT budgets and decentralized infrastructure. The U.S. has over 50,000 community water systems, the majority of which are small utilities with limited automation and legacy supervisory processes. While agencies such as the EPA emphasize modernization and resilience for systems serving fewer than 50,000 people, the transition toward cloud-native and advanced digital operational technologies remains largely industry-driven rather than mandated. Vendors offering subscription-based, remotely hosted SCADA solutions with embedded cybersecurity and compliance reporting stand to capture disproportionate growth.

Expanding SCADA Demand in Renewable Energy and Microgrid Management

Solar, wind, and energy storage systems require continuous real-time monitoring to handle variability in power generation and ensure grid stability. SCADA solutions play a critical role in enabling remote operations, fault detection, and predictive maintenance across these decentralized assets. The rise of microgrids and smart grid infrastructure is increasing the need for advanced supervisory control capabilities. Major industry players are developing specialized SCADA platforms designed specifically for renewable applications. This is expected to create significant growth opportunities for SCADA providers.

Category-wise Analysis

Component Insights

Hardware dominates the market, capturing more than 53% of the market share in 2026 with a value exceeding US$ 7.2 Bn, as industries require reliable physical infrastructure such as RTUs, PLCs, sensors, and communication devices to ensure real-time monitoring and control. The growing need for modernization of aging industrial assets, especially in power grids and oil & gas facilities, continues to drive hardware demand. Expansion of industrial automation in developing economies increases the installation of field devices. Hardware investments are also essential for ensuring system redundancy and operational safety.

Software is expected to grow rapidly due to the rising need for advanced data analytics, predictive maintenance, and centralized monitoring platforms. Organizations are increasingly adopting SCADA software with AI and machine learning capabilities to enhance decision-making and operational efficiency. The shift toward open architecture and interoperability is enabling seamless integration across multiple industrial systems. Demand for cybersecurity solutions within SCADA software is also increasing due to rising cyber threats.

Deployment Insights

On-Premises holds over 49% market share in 2026, with a value exceeding US$ 6.6 Bn, due as critical industries prioritize full control over their infrastructure and data. Sectors such as energy, defense, and manufacturing require high system reliability, low latency, and strict regulatory compliance, which on-premises systems better ensure. These deployments also minimize exposure to external cyber risks by maintaining closed network environments. Legacy systems and existing infrastructure further support continued reliance on on-premises models. Industries with remote or low-connectivity environments prefer on-site systems for uninterrupted operations.

Cloud-Based is expected to grow significantly due to the need for scalability, remote accessibility, and reduced capital expenditure. Organizations are leveraging cloud platforms to monitor geographically dispersed assets in real time with greater flexibility. The growing adoption of IoT and edge computing is further accelerating cloud integration. Cloud solutions also enable faster updates, improved collaboration, and centralized data storage. Enhanced security frameworks and compliance standards are gradually addressing earlier concerns, encouraging wider adoption across industries.

Industry Insights

Energy & utilities command the largest market share at over 35% in 2026, with a value exceeding US$ 4.7 Bn, as the sector heavily depends on SCADA systems for grid monitoring, power distribution, and asset management across vast networks. Increasing electricity demand, renewable energy integration, and smart grid development are key drivers for adoption. Utilities require real-time visibility and control to ensure grid stability and prevent outages. Government regulations and infrastructure investments further support deployment in this sector. The transition toward decentralized energy systems increases the complexity of operations, strengthening the need for advanced SCADA solutions.

Water & Wastewater is expected to grow at a CAGR of 12.5% due to the need for efficient resource management and regulatory compliance. Urbanization and population growth are increasing pressure on water infrastructure, requiring automated monitoring and control systems. SCADA helps with leak detection, quality monitoring, and efficient distribution of water resources. Governments are investing in smart water management systems to reduce losses and improve sustainability. Remote monitoring capabilities are crucial for managing dispersed treatment facilities and ensuring operational efficiency.

Regional Insights

North America SCADA Market Trends

North America holds over 36% share in 2026, reaching US$ 4.9 Bn value, driven by its extensive critical infrastructure and strong regulatory ecosystem. The U.S. Department of Homeland Security classifies SCADA across multiple critical sectors, ensuring continuous modernization investments. The Infrastructure Investment and Jobs Act (IIJA), allocating US$ 65 billion, is accelerating deployment across grid, water, and broadband systems. The region hosts major vendors such as Rockwell Automation, Inc. and Honeywell International Inc., reinforcing innovation leadership. Advanced cybersecurity R&D from Idaho National Laboratory supports next-generation SCADA resilience. Canada complements growth through digital upgrades in oil sands and hydroelectric infrastructure.

Asia Pacific SCADA Market Trends

Asia Pacific is expected to grow at a significant rate with a CAGR of 13.2%, due to rapid industrialization and large-scale infrastructure investments. China dominates regional demand through initiatives led by the State Grid Corporation of China and its 14th Five-Year Plan, prioritizing grid modernization and industrial digitalization. India is witnessing strong adoption through programs like Smart Cities Mission and Jal Jeevan Mission. Japan continues innovation via companies such as Mitsubishi Electric Corporation. ASEAN countries are integrating SCADA in greenfield industrial parks, creating significant new deployment opportunities. Increasing cybersecurity focus is also shaping regional adoption.

Europe SCADA Market Trends

Europe is expected to hold more than 26% share by 2026, supported by strong industrial automation and regulatory-driven adoption. The NIS2 Directive has expanded compliance requirements, triggering widespread SCADA upgrades across energy, water, and transport sectors. Germany leads with its Industrie 4.0 framework, while the UK emphasizes cybersecurity through national guidelines. France and Spain are accelerating SCADA deployment in renewable energy, particularly wind and solar. Regional leaders such as Schneider Electric SE and ABB Ltd. strengthen technological capabilities. Cross-border grid projects under ENTSO-E further drive multi-country SCADA integration demand.

Competitive Landscape

The SCADA market is moderately consolidated, with key players dominating through technological expertise and global presence. Companies focus on innovation, cloud integration, and cybersecurity enhancements to differentiate their offerings. Strategic partnerships, acquisitions, and R&D investments are being adopted. Vendors are increasingly adopting subscription-based models and SaaS platforms to expand their customer base. Integration with IoT and AI technologies is a key trend, enabling predictive analytics and real-time monitoring capabilities across industries.

Key Industry Developments

- In February 2026, International Society of Automation released ANSI/ISA-112.00.01-2025, a new standard outlining a vendor-neutral framework for SCADA lifecycle management, diagrams, and terminology across industries. The standard supports both new and legacy SCADA systems, helping organizations design, operate, and modernize systems with standardized workflows, while additional parts on lifecycle review and architecture are planned.

- In February 2026, Siemens, in collaboration with Mescada, will deploy a large-scale AI-ready, cloud-based SCADA system for Global Power Generation Australia, connecting eight renewable assets across Australia with ~300,000 data tags for centralized monitoring.

Companies Covered in SCADA Market

- Siemens AG

- Schneider Electric SE

- Rockwell Automation, Inc.

- ABB Ltd.

- Emerson Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- Yokogawa Electric Corporation

- Inductive Automation

- GE Digital

- Hitachi Ltd.

- AVEVA Group

- Others

Frequently Asked Questions

The global market is projected to be valued at US$13.5 Bn in 2026.

The growing need for real-time monitoring, automation, and control of critical infrastructure such as energy, water, and manufacturing systems are key driver of the market.

The market is expected to witness a CAGR of 8.7% from 2026 to 2033.

The rapid adoption of cloud-based SCADA, AI-driven analytics, and remote operations is creating strong growth opportunities.

Siemens AG, Schneider Electric SE, Rockwell Automation, Inc., ABB Ltd., Emerson Electric Co., Honeywell International Inc., Mitsubishi Electric Corporation, and Yokogawa Electric Corporation are among the leading key players.