- Hardware & Software IT Services

- Privileged Access Management Market

Privileged Access Management Market Size, Share, and Growth Forecast 2026 - 2033

Privileged Access Management Market by Solution (Software, Services), by Deployment (Cloud-based, On-premise, Hybrid), Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs)), End-use Industry (BFSI, IT & Telecom, Government & Defense, Healthcare, Retail & E-commerce, Manufacturing, Energy & Utilities, Education, Others), and Regional Analysis, 2026 - 2033

Privileged Access Management (PAM) Market Size and Trend Analysis

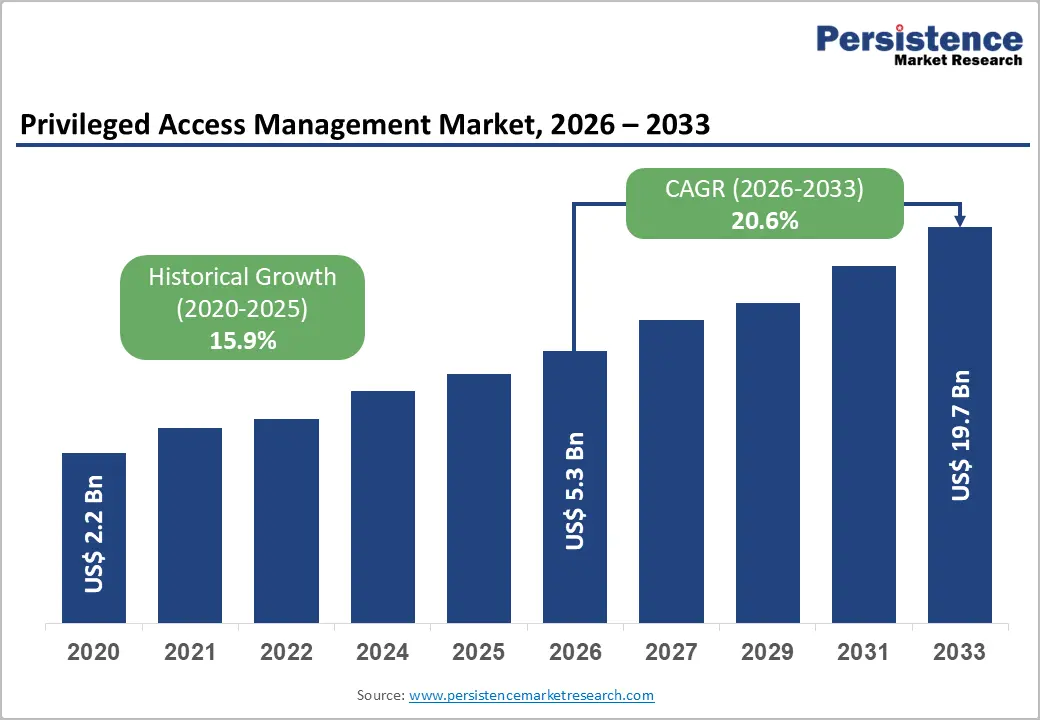

The global privileged access management market is expected to be valued at US$ 5.3 billion in 2026 and is projected to reach US$ 19.7 billion by 2033, growing at a CAGR of 20.6% between 2026 and 2033, driven by the growing need to secure critical IT infrastructure against increasing cyber threats, insider risks, and credential-based attacks in complex hybrid and cloud environments.

The convergence of mandatory zero-trust architecture adoption, accelerated by the U.S. National Cybersecurity Strategy and the European Union’s NIS2 Directive, has structurally elevated privileged access management from a discretionary IT investment to a compliance-driven and risk-mitigation necessity. As organizations face rising regulatory scrutiny and operational exposure, PAM has become an essential security control and a board-level imperative across every regulated sector globally.

Key Industry Highlights:

- Leading Solution: Software is likely to dominate with over 67% share in 2026, valued at more than US$ 3.55 Bn, driven by enterprise demand for centralized credential vaulting, privileged session monitoring, and least-privilege enforcement across regulated industries.

- Leading Deployment: On-premises deployment leads with over 36% share in 2026, valued at more than US$ 1.91 Bn, due to strict data sovereignty, regulatory compliance, and isolated infrastructure requirements across defence, banking, and critical infrastructure sectors.

- Leading Enterprise Size: Large enterprises are likely to account for above 70% share in 2026, valued at over US$ 3.71 Bn, supported by complex IT infrastructures, high regulatory exposure, and mandatory audit and compliance requirements across industries such as banking and pharmaceuticals.

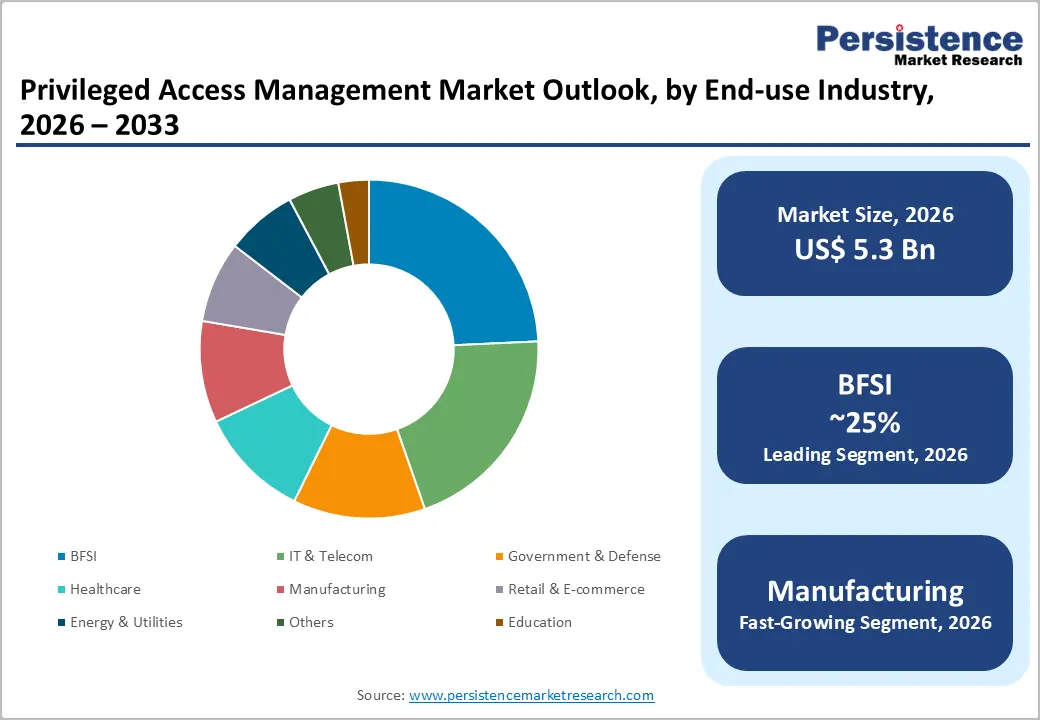

- Leading End-use Industry: BFSI leads with over 25.0% market share in 2026, valued at more than US$ 1.32 Bn, driven by the sector’s high concentration of privileged accounts, stringent regulatory obligations, and growing need for segregation-of-duties and insider threat protection.

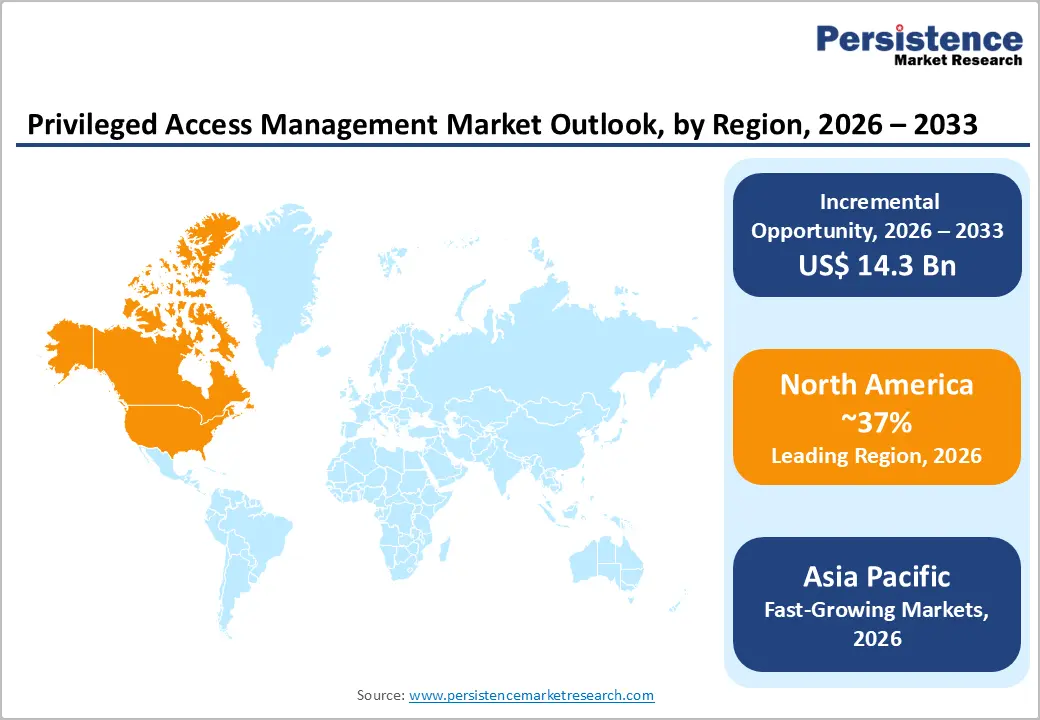

- Leading Region: North America dominates the market with over 37.0% share in 2026, valued at approximately US$ 1.96 Bn, supported by mature cybersecurity spending, strong federal zero-trust mandates, and the presence of major PAM vendors and enterprise customers.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a CAGR of 26.1%, driven by accelerating digital transformation, tightening cybersecurity regulations in China, India, and Japan, and increasing adoption of identity-centric security frameworks across critical infrastructure and enterprise cloud ecosystems.

Market Dynamics

Drivers - Proliferation of Zero-Trust Security Mandates Across Federal and Enterprise Ecosystems

Zero-trust architecture adoption is forcing organisations to replace implicit-trust network models with identity-centric access controls, making PAM software a non-negotiable infrastructure investment rather than a discretionary security spend. The U.S. Executive Order 14028 on Improving the Nation's Cybersecurity, subsequently reinforced by Office of Management and Budget Memorandum M-22-09 in 2022, set enforceable zero-trust maturity deadlines for all U.S. federal civilian agencies, compelling vendors such as CyberArk Software to expand their Federal Risk and Authorization Management Program (FedRAMP)-authorised PAM product lines through 2023 and 2024. Over the next two to three years, this federal precedent will cascade into state-level and allied-nation procurement frameworks, expanding the addressable market well beyond current enterprise boundaries.

Surge in Operational Technology and Critical Infrastructure Cyberattacks Drives Mandatory Controls

Manufacturing plants, power grids, and water treatment facilities are now primary targets for credential-based intrusions, as operational technology (OT) environments historically lacked the access governance controls standard in IT networks. The U.S. Transportation Security Administration's revised cybersecurity directives for pipeline and rail operators issued in 2022 and 2023 explicitly required multi-factor authentication and privileged session monitoring capabilities delivered exclusively by PAM platforms, compelling critical infrastructure operators to initiate large-scale deployments. As the European Union's NIS2 Directive, which entered force in October 2024, extends similar mandatory access controls to energy, transport, and water sectors across 27 member states, the OT-PAM addressable market will expand substantially, rewarding vendors with certified OT protocol support.

Restraints - High Implementation Complexity and Total Cost of Ownership Suppressing Mid-Market Adoption

Enterprise deployments require extensive credential discovery, vault integration, and session-recording infrastructure that routinely extends implementation timelines to six to eighteen months, creating substantial professional services costs that compress return-on-investment calculations for budget-constrained organisations. The National Institute of Standards and Technology (NIST) SP 800-207 framework, while providing architectural guidance, demands that organisations complete a comprehensive privileged account inventory before deploying a process it adds 15–25% to the total project cost in complex hybrid environments. For new entrants attempting to capture mid-market accounts, this friction is particularly acute because incumbents with established professional services networks hold a structural delivery advantage that is difficult to displace on price alone.

Talent Shortage in Identity and Access Management Constraining Deployment Velocity

A persistent deficit of certified identity security professionals’ throttles PAM deployment rates even when budget approval exists, as organisations cannot staff the internal teams required to configure, maintain, and audit privileged access environments. The ISC² 2023 Cybersecurity Workforce Study reported a global cybersecurity workforce gap of approximately 4.8 million professionals, with identity and access management roles among the hardest to fill, carrying salary premiums of 20–30% above general IT security positions according to SANS Institute compensation survey data. This constraint disproportionately disadvantages smaller managed security service providers attempting to scale PAM delivery practices, as they compete directly with hyperscalers for the same scarce talent pool.

Opportunities- Managed PAM-as-a-Service Addressing the Underserved Mid-Market Through Subscription Delivery

Vendors capable of packaging PAM capabilities into fully managed, subscription-based services unlock a mid-market segment that has historically been priced out of, and constrained by the complexity of, enterprise-grade privileged access controls. Delinea launched its Cloud Suite and extended managed PAM offerings in 2023, demonstrating the commercial validation of this delivery model. Vendors with mature cloud-native architectures and pre-built integrations with platforms such as Microsoft Azure Active Directory and AWS IAM are best positioned to capture this opportunity, provided they demonstrate compliance coverage aligned with frameworks like SOC 2 Type II that mid-market procurement teams already understand.

AI-Augmented Privileged Access Analytics Creating Premium Upsell and Differentiation Pathways

Embedding artificial intelligence and machine learning to detect anomalous privileged behaviour in real time represents a high-margin product expansion opportunity that buyers are actively willing to fund as a supplement to baseline vaulting and session management. IBM Corporation integrated its QRadar SIEM with privileged access analytics capabilities in 2024, enabling security operations centres to correlate privileged session data with broader threat intelligence feeds and reduce mean-time-to-detect for insider threats.

Solution providers that deliver demonstrable reductions in dwell time, a metric now tracked explicitly under the SEC's 2023 cybersecurity incident disclosure rules requiring material breach notification within four business days, will command meaningful pricing premiums over commodity vault-only competitors.

Category-wise Analysis

Solution Insights

Software is likely to command 67% of the global privileged access management market in 2026, reaching over to US$ 3.55 billion, driven by the enterprise need for centralized enforcement of identity security controls. Organizations increasingly require integrated platforms that unify credential vaulting, session monitoring, and least-privilege enforcement to mitigate risks associated with credential theft, insider threats, and unauthorized privileged escalation. In highly regulated environments such as financial services and government agencies, PAM software is critical for enforcing compliance with mandates, including SWIFT security controls and NIST SP 800-53 frameworks.

The services are emerging as the fast-growing category, due to the operational need to manage increasing PAM complexity across hybrid cloud and OT environments. Enterprises are facing internal capability gaps in deploying and maintaining privileged access frameworks, particularly in sectors such as healthcare, where HIPAA compliance requires continuous monitoring and policy enforcement. Organizations are shifting toward managed PAM services that provide ongoing implementation support, integration across identity ecosystems, and continuous compliance assurance, positioning services as a structurally higher-growth segment than standalone software licensing.

Deployment Insights

On-premises deployment leads the global privileged access management market at 36.0% share in 2026, due to non-negotiable compliance and sovereignty needs in highly regulated sectors such as defence, central banking, and nuclear energy. Organizations are required to maintain strict control over privileged credentials within isolated environments, ensuring that sensitive access data never leaves internal infrastructure. Frameworks such as CMMC 2.0 further reinforce this requirement by mandating stringent control over privileged access in defense supply chains.

Cloud-based PAM is the fast-growing deployment model, driven by the operational need to secure rapidly expanding cloud workloads and dynamic identity environments. As enterprises migrate applications to hyperscaler platforms, traditional static vault-based models cannot effectively manage ephemeral identities and distributed access points. The rise of Kubernetes and DevOps pipelines creates a need for cloud-native security controls that integrate directly into infrastructure-as-code environments. Cloud PAM is increasingly adopted to address the security needs of modern, scalable, and continuously changing IT architectures.

Enterprise Size Insights

Large enterprises are likely to account for more than 70% share in 2026, due to critical need for regulatory compliance, auditability, and control over vast privileged account environments. Industries such as pharmaceuticals and banking require strict adherence to frameworks like FDA 21 CFR Part 11 and PCI DSS v4.0, making PAM essential for meeting mandatory security and audit requirements. Their complex, multi-vendor IT infrastructures further necessitate centralized privileged access control to reduce cyber risk and ensure operational security.

Small & Medium Enterprises (SMEs) represent the fastest growing enterprise size due to improved accessibility of cloud-based solutions and lower deployment costs, rather than core operational necessity. Adoption is often triggered by external influences such as cyber insurance requirements and partner-driven security expectations. SMEs typically do not face intrinsic complexity that mandates PAM, but rather adopt it as security maturity improves. This makes SME growth more opportunity-enabled and pressure-influenced.

End-use Industry Analysis

BFSI leads with over 25.0% of market share in 2026, reaching over to US$ 1.32 Billion, driven by the sector's uniquely dense concentration of high-value privileged accounts governing core banking systems, trading platforms, and customer data vaults. Investment banks deploy to enforce segregation-of-duties controls on algorithmic trading infrastructure, ensuring no single administrator modify both execution logic and risk parameters a control explicitly mandated under the European Banking Authority's (EBA) Guidelines on ICT and Security Risk Management, finalised in 2019 and operationally enforced through 2022–2024 supervisory reviews. The Financial Industry Regulatory Authority (FINRA) reported that credential misuse remains the leading cause of reportable cybersecurity incidents among broker-dealers, cementing BFSI as the most structurally committed PAM vertical.

Manufacturing is the fast-growing industry as Industry 4.0 digitalisation connects previously isolated production networks to enterprise IT systems, exposing operational technology to credential-based attack vectors for the first time at scale. The EU Cyber Resilience Act, which entered into force in December 2024 and requires manufacturers of connected products to implement access control by design, will make PAM adoption a legal compliance requirement for manufacturers selling into European markets, driving structural demand.

Regional Insights

North America Privileged Access Management Market Trends and Insights

North America accounts for over 37.0% of the global privileged access management market in 2026, representing US$ 1.96 billion, establishing its position as the dominant region through a combination of mature enterprise security budgets, the world's highest density of Fortune 500 organisations, and an active regulatory environment that continuously creates new compliance mandates. North America's leadership position will be reinforced as Canadian Centre for Cyber Security frameworks extend PAM requirements to critical infrastructure operators across federal Crown corporations.

The United States privileged access management market is expected to reach over US$ 1.71 Billion in 2026, driven by the co-located presence of the world's largest PAM vendors and their most sophisticated enterprise customers across financial services, defence, and technology sectors. The Federal Zero Trust Strategy created a defined procurement roadmap for all 23 civilian federal departments, generating a concentrated pipeline of government PAM contracts. Rapid cloud migration and increasing API-driven infrastructure are expanding privileged access points, intensifying the need for continuous identity governance and real-time access monitoring across hybrid environments.

Europe Privileged Access Management Market Trends and Insights

Europe accounts for more than 28% of the global privileged access management market in 2026, representing US$ 1.48 billion, due to the growing need for regulatory compliance, identity governance, and protection against credential-based cyberattacks across critical industries. Germany privileged access management market is expected to surpass US$ 0.33 Billion, supported by rising cybersecurity investments from the automotive and industrial manufacturing sectors under the BSI IT-Grundschutz framework. The increasing convergence of IT and operational technology networks is further accelerating demand for advanced privileged credential monitoring and session management platforms.

The United Kingdom holds more than 20% of the Europe privileged access management market in 2026, accounting for over US$ 0.30 Billion, driven by rising cybersecurity compliance requirements and government-backed security initiatives. The UK’s evolving Data Protection and Digital Information Act is maintaining GDPR-equivalent access control obligations, creating sustained demand for identity-centric security solutions across BFSI, telecom, and public sector organizations. France privileged access management market is projected to witness the fastest growth rate in the region, fueled by increasing cybersecurity modernization across public administration, defence, and energy infrastructure. The country’s ANSSI qualification requirements and mandatory SecNumCloud framework are driving organizations toward locally certified PAM vendors, strengthening demand for sovereign and compliance-oriented privileged access management platforms.

Asia Pacific Privileged Access Management Market Trends and Insights

Asia Pacific accounts for 25% of the global share in 2026 and is projected to reach a CAGR of 26.1%. The growth is need-driven further accelerating digital transformation across China, India, and Southeast Asia, which is increasing enterprise exposure to identity-based cyber threats and privileged credential misuse. Governments across the region are tightening cybersecurity regulations to protect critical infrastructure, compelling organizations to implement privileged access governance frameworks.

China Privileged Access Management Market is expected to reach over US$ 0.46 Billion in 2026, while Japan accounts more than US$ 0.24 Billion value, driven by regulatory enforcement and the operational need to secure privileged identities in highly digitized sectors. In China, MLPS 2.0 audits, the Cybersecurity Law, and PIPL regulations are compelling state-owned enterprises and technology firms to deploy localized PAM solutions that meet data sovereignty requirements. Japan’s Financial Services Agency cybersecurity guidelines and the Economic Security Promotion Act are driving financial institutions and semiconductor companies to adopt privileged session recording and monitoring capabilities. India is expected to grow at highest rate due to rapidly expanding IT outsourcing ecosystem. The implementation of the Digital Personal Data Protection Act (DPDPA) is further accelerating PAM procurement among fintech, healthcare IT, and enterprise cloud service providers.

Competitive Landscape

The global privileged access management market operates as a concentrated oligopoly at the enterprise tier, with top players commanding an estimated 35–40% combined revenue share. Leading vendors are prioritizing cloud-native and hybrid deployment models to support multi-cloud infrastructures and remote workforce environments. Companies are also embedding AI-driven threat analytics and behavioral monitoring capabilities to improve privileged session detection and automated response. Companies are shifting toward subscription-based and managed PAM-as-a-Service models to penetrate the mid-market segment.

Key Developments:

- In March 2026, Securden announced updates and enhancements to its identity security and privileged access management platform through its latest press releases, highlighting continued innovation in unified security solutions. The company also emphasized advancements in password management, endpoint privilege controls, and expanded enterprise adoption across global industries.

- In April 2025, SITS Group launched Privileged Access Management (PAM) as a Service, a fully managed cloud-based solution built with CyberArk technology to secure and control privileged accounts. The service helps organizations reduce cyber risk by protecting high-value credentials, offering rapid deployment, scalability, and managed security without complex infrastructure setup or high upfront costs.

Global Privileged Access Management Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 2.2 Billion |

|

Current Market Value (2026) |

US$ 5.3 Billion |

|

Projected Market Value (2033) |

US$ 19.7 Billion |

|

CAGR (2026–2033) |

20.6% |

|

Leading Region |

North America, 37.0% Share |

|

Dominant Solution |

Software, 67.0% Share |

|

Top-ranking End-use Industry |

BFSI, 25.0% Share |

|

Incremental Opportunity |

US$ 14.3 Billion |

Companies Covered in Privileged Access Management Market

- CyberArk Software Ltd.

- BeyondTrust, Inc.

- Delinea

- IBM Corporation

- Oracle Corporation

- One Identity

- Broadcom

- ARCON

- Senhasegura

- Wallix

- Sectona

- ManageEngine

- HashiCorp

- Micro Focus NetIQ

- Others

Frequently Asked Questions

The global privileged access management market is valued at US$ 5.3 Billion in 2026 and is projected to reach US$ 19.7 Billion by 2033, registering a CAGR of 20.6% due to mandatory zero-trust architecture adoption enforced across enterprise and government sectors by frameworks including OMB M-22-09, driving non-discretionary PAM procurement globally.

Growing frequency of cyberattacks targeting privileged credentials, rapid cloud migration, remote work expansion, and the need to secure machine identities, APIs, and DevOps environments are accelerating enterprise demand for PAM solutions.

Software is likely to account for over 67% of the global market in 2026, as enterprise security operations centres require unified policy enforcement, credential vaulting, and session audit trails within a single administrative platform rather than disparate point tools.

North America dominates with more than 37.0% of global market share in 2026, underpinned by the co-location of the world's largest PAM vendors and the most active regulatory pipeline of any region, encompassing federal zero-trust mandates, SEC disclosure rules, and state-level cybersecurity frameworks.

The growing need to secure AI agents, machine identities, and automated workflows is creating major demand for intelligent PAM solutions with just-in-time access, behavioral analytics, and real-time threat detection.