- Home Care & Utilities

- Sandpaper Market

Sandpaper Market Size, Share, and Growth Forecast, 2026- 2033

Sandpaper Market by Product Type (Wheels, Rolls, Discs, and Others), By Abrasive Type (Aluminium Oxide, Ceramic, Silicon Carbide, and Garnet), By Application (Woodworking, Automotive Refinishing, Metalworking, Construction, and Others), and Regional Analysis for 2026 – 2033.

Sandpaper Market Size and Trends Analysis

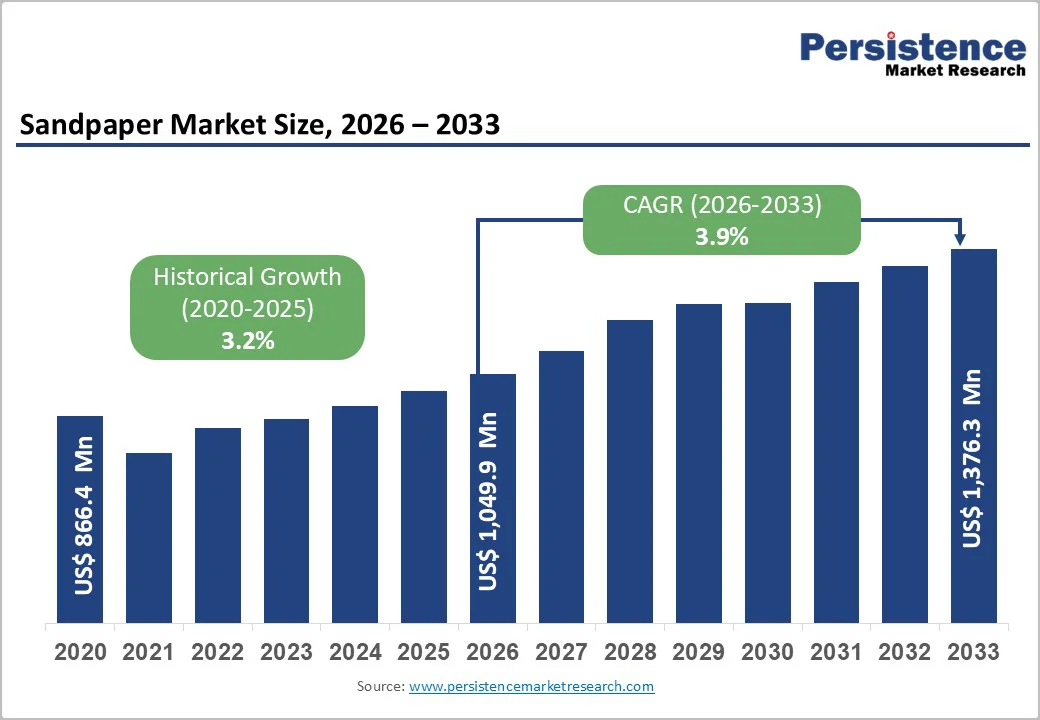

The global sandpaper market was valued at US$ 866.4 Million in 2020 and is projected to reach US$ 1,049.9 Million by 2026, expanding further to US$ 1,376.3 Million by 2033, growing at a CAGR of 3.2% (2020-2026) and 3.9% (2026-2033). The market expansion is driven by sustained demand from woodworking and automotive refinishing industries, recovery in construction activities post-pandemic, and technological advancements in abrasive manufacturing. Growth is moderately tempered by raw material cost volatility and increasing competition from synthetic alternatives, positioning the market for steady, value-driven expansion through 2033.

Key Industry Highlights:

- Product Segment Dynamics: Wheels segment dominates with 43%+ revenue share, while Rolls represents fastest-growing category at 4.4% CAGR; automation trends driving gradual product form evolution toward higher-margin, automation-compatible formats through 2033.

- Abrasive Material Evolution: Aluminum oxide maintains 45%+ market leadership, while Ceramic abrasives demonstrate fastest growth at 4.6% CAGR, reflecting manufacturing sector premium positioning and advanced coating adoption creating margin expansion opportunities.

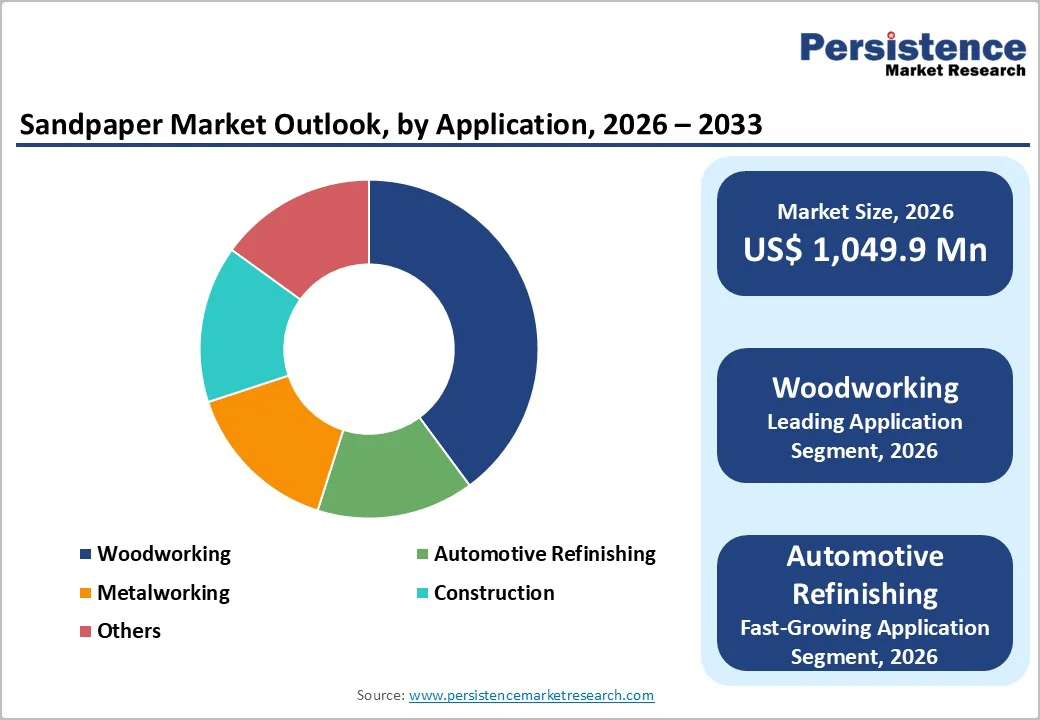

- Application Growth Acceleration: Automotive Refinishing leads growth at 4.7% CAGR versus Woodworking baseline at 40%+ share, indicating structural market shift toward higher-value aftermarket and OEM applications in developed economies.

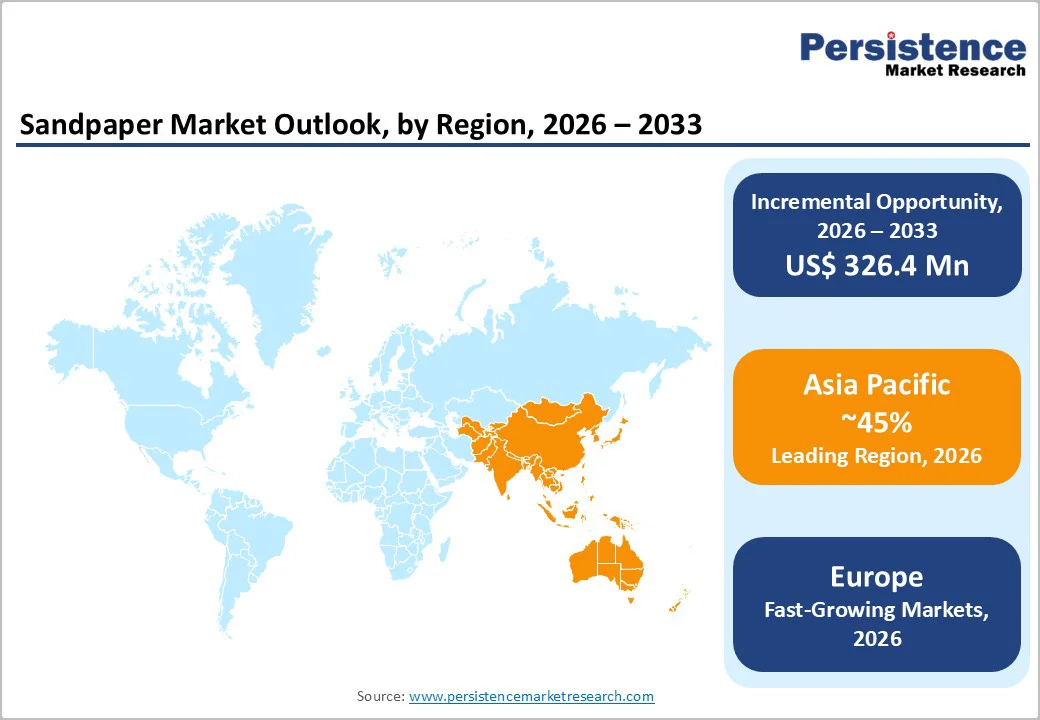

- Regional Growth Divergence: Asia Pacific dominates with 40%+ global share and 4.2-4.8% growth rates, while Europe emerges as fastest-growing developed region at 4.6% CAGR; North America shows maturity characteristics at 3.1% growth, creating geographic investment concentration opportunities in emerging markets.

- Competitive Consolidation and Innovation: Post-2023 strategic developments focus on regional manufacturing footprint establishment in Asia Pacific, sustainability-driven product innovation, and ceramic abrasive capacity expansion, indicating industry structural consolidation with accelerating multinational market penetration.

- Investment Implications: Market opportunities concentrate in emerging market expansion (India, Vietnam, ASEAN), specialty abrasive segment development, and sustainability-driven product innovation, collectively representing estimated USD 200-300 Million incremental market value through 2033 for well-positioned market participants.

| Global Market Attributes | Key Insights |

|---|---|

| Sandpaper Market Size (2026E) | US$ 1,049.9 Mn |

| Market Value Forecast (2033F) | US$ 1,376.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 3.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.2% |

Market Dynamics

Key Growth Drivers

Rising Construction and Renovation Activities Globally

Construction sector recovery post-pandemic has emerged as a primary growth catalyst for the sandpaper market. The global construction market is projected to reach USD 12-14 trillion annually by 2030, with significant expansion in residential and commercial segments requiring finishing materials. Surface preparation and refinishing operations—critical applications for sandpaper across concrete, wood, and metal substrates—are essential in modern construction protocols. Regional dynamics show particularly strong momentum in Asia Pacific, where urbanization rates exceed 45% in emerging economies, driving incremental demand for finishing materials. This driver directly correlates to the woodworking segment's 40%+ revenue share and supports the broader 3.9% CAGR trajectory through 2033.

Market Restraining Factors

Competition from Non-Abrasive Surface Preparation Technologies

Emerging alternatives including laser surface preparation, plasma cleaning, and chemical abrasion technologies present structural competitive threats. These methods offer superior precision, reduced material waste, and lower labor intensity in specific applications, particularly precision manufacturing. Adoption rates in automotive OEMs and aerospace industries create headwinds for traditional sandpaper in high-value segments. The technology substitution risk particularly impacts premium abrasive markets where value proposition is dependent on cost-performance economics rather than technological differentiation.

Sandpaper Market Trends and Opportunities

Emerging Market Expansion in Southeast Asia and India

Southeast Asia and India represent significant untapped markets with manufacturing GDP growth exceeding 6-7% annually. Rising middle-class consumer bases are driving residential construction and furniture manufacturing, core applications for sandpaper. Market penetration rates in India and Vietnam remain below 40% of developed market levels, indicating substantial expansion potential. The opportunity size is estimated at USD 150-200 Million incremental market value through 2033, achievable through localized manufacturing, distribution partnerships, and product adaptation for regional specifications.

Sandpaper Market Insights and Trends

Product Type Insights

Wheels Dominate Sandpaper Market While Rolls Accelerate Growth Through Industrial Automation

The global sandpaper market’s product type landscape is led decisively by the wheels segment, which accounts for over 43% of total revenue across all major regions. Wheels have emerged as the most widely adopted sandpaper format due to their versatility across grinding, finishing, and material removal operations. They are extensively used in woodworking, metalworking, and construction applications, where durability, consistency, and compatibility with standard industrial equipment are critical. Their strong market position is further reinforced by continuous-use manufacturing environments, where repetitive grinding and finishing are integral to production workflows. As a result, the wheels segment benefits from high repeat-purchase rates and standardized equipment usage across global manufacturing facilities. In 2026, the market size of the wheels segment is estimated to range between USD 470 million and USD 500 million, underscoring its entrenched role in industrial abrasive consumption.

In contrast, sandpaper rolls represent the fastest-growing product category, registering a projected CAGR of 4.4% between 2026 and 2033. This growth is closely linked to rising manufacturing automation, particularly in the automotive and woodworking industries. Roll-based abrasive systems are increasingly favored in automated and continuous finishing lines due to their efficiency, reduced material waste, lower labor dependency, and improved precision control. The accelerating adoption of rolls signals a gradual structural shift toward automation-compatible abrasive formats within advanced manufacturing environments.

Abrasive Type Insights

Aluminum Oxide Leads Abrasives Market While Ceramic Gains Momentum in Precision

The global abrasives market is currently led by aluminum oxide, which accounts for more than 45% of total revenue and remains the industry’s standard for general-purpose applications. Its leadership position is underpinned by a strong balance of cost-effectiveness, consistent performance, and broad material compatibility. Aluminum oxide is widely used across woodworking, metalworking, and general construction activities, where reliability and affordability are critical purchasing criteria. Its predictable cutting behavior and suitability for diverse substrates make it the default abrasive choice for high-volume and price-sensitive applications. By 2026, the aluminum oxide segment is estimated to reach a market value of approximately USD 480–520 million, reinforcing its status as the largest-volume abrasive category globally.

In contrast, ceramic abrasives represent the fastest-growing segment within the market, expanding at a projected CAGR of 4.6% between 2026 and 2033. Growth is driven by increasing adoption in precision manufacturing, aerospace components, automotive OEM operations, and advanced coating applications. Ceramic abrasives offer superior durability, longer service life, and reduced total cost of ownership compared to conventional materials. Although they command a price premium of 20–35% over aluminum oxide, manufacturers are increasingly willing to invest in higher-performance solutions where productivity gains and performance consistency justify the additional cost.

Application Insights

Woodworking Dominance and Automotive Refinishing Growth Reshape Global Abrasives Application Landscape

Woodworking remains the leading application segment, accounting for more than 40% of global revenue, supported by steady demand from furniture manufacturing, flooring production, and wood finishing activities. Its estimated market size of USD 420–460 million in 2026 reflects the sector’s structural stability as a mature, labor-intensive industry with continuous surface finishing requirements across residential, commercial, and industrial uses. Demand is closely tied to construction activity, interior refurbishment, and export-oriented furniture production. Regional dynamics further reinforce this dominance, with Asia Pacific emerging as the largest hub for wood-based manufacturing. Countries such as Vietnam, Indonesia, and India host dense clusters of furniture and panel producers, underpinning sustained volume consumption and long-term regional growth prospects.

In contrast, automotive refinishing represents the fastest-growing application segment, expanding at a CAGR of 4.7% between 2026 and 2033. Growth is driven by rising global vehicle fleets, increasing accident repair rates, and the growing adoption of premium coatings that require high-precision surface preparation. An estimated 800–900 million vehicle refinishing operations are conducted annually worldwide, each generating consistent abrasive demand. Growth in this segment outpaces the overall market by approximately 0.8%, highlighting a clear shift toward higher-value, performance-driven applications. By 2033, automotive refinishing abrasives represent a market opportunity of USD 280–320 million.

Regional Insights and Trends

Asia Pacific Sandpaper Market Leadership Driven by Construction Manufacturing Shifts and Regulations

Asia Pacific dominates the global sandpaper market, accounting for over 40% of total revenue, supported by dense manufacturing ecosystems, rapid construction activity, and sustained growth across emerging economies. The region is projected to represent approximately USD 430–470 million of global market value by 2026, expanding at a robust CAGR of 4.2–4.8%, well above the global average. China, India, and Southeast Asia together contribute more than 75% of regional demand, with India standing out as the fastest-growing market, advancing at a 5.1% CAGR through 2033.

China retains the largest absolute market share at around 35% of regional revenue; however, growth is moderating to nearly 3.1% CAGR due to industrial maturity. In contrast, India offers the strongest upside, driven by accelerating construction activity and expanding furniture and wood-processing industries. Vietnam and Indonesia are also emerging as high-growth markets, recording 4.5–4.8% growth rates, supported by export-oriented manufacturing and wood products expansion.

Construction recovery and rapid urbanization remain the primary demand drivers, with Asia Pacific construction investments expected to exceed USD 4.5 trillion through 2033. Ongoing manufacturing relocation from China to India and Southeast Asia is redistributing demand within the region. Additionally, rising automotive production and low vehicle penetration levels are stimulating aftermarket refinishing demand. Increasingly stringent environmental regulations, particularly in Japan, South Korea, and China, are accelerating adoption of low-dust, higher-quality abrasives, reinforcing long-term regional outperformance.

Asia Pacific Sandpaper Market Leadership Driven by Construction Manufacturing Shifts and Regulations

Asia Pacific dominates the global sandpaper market, accounting for over 40% of total revenue, supported by dense manufacturing ecosystems, rapid construction activity, and sustained growth across emerging economies. The region is projected to represent approximately USD 470 million of global market value by 2026, expanding at a robust CAGR of 4.8%, well above the global average. China, India, and Southeast Asia together contribute more than 75% of regional demand, with India standing out as the fastest-growing market, advancing at a 5.1% CAGR through 2033.

China retains the largest absolute market share at around 35% of regional revenue; however, growth is moderating to nearly 3.1% CAGR due to industrial maturity. In contrast, India offers the strongest upside, driven by accelerating construction activity and expanding furniture and wood-processing industries. Vietnam and Indonesia are also emerging as high-growth markets, recording 4.5–4.8% growth rates, supported by export-oriented manufacturing and wood products expansion.

Construction recovery and rapid urbanization remain the primary demand drivers, with Asia Pacific construction investments expected to exceed USD 4.5 trillion through 2033. Ongoing manufacturing relocation from China to India and Southeast Asia is redistributing demand within the region. Additionally, rising automotive production and low vehicle penetration levels are stimulating aftermarket refinishing demand. Increasingly stringent environmental regulations, particularly in Japan, South Korea, and China, are accelerating adoption of low-dust, higher-quality abrasives, reinforcing long-term regional outperformance.

Sandpaper Market Competitive Landscape

The global sandpaper market demonstrates a moderately consolidated competitive structure, clearly divided between multinational industrial manufacturers and regional specialists. The top five players collectively account for around 45–50% of global revenue, while mid-sized regional companies contribute roughly 25–30%, and smaller, fragmented participants make up the remaining 20–25%. This structure reflects substantial entry barriers created by capital-intensive manufacturing facilities, advanced abrasive technologies, and well-established distribution networks. Market concentration is notably higher in developed regions such as North America and Western Europe, whereas Asia Pacific remains more fragmented due to the strong presence of local manufacturers competing effectively on cost and regional familiarity. Multinational companies, typically limited to 8–10 firms with more than 3% individual market share, differentiate themselves through brand strength, product innovation, and supply chain reliability, while regional players emphasize pricing competitiveness and localized demand fulfillment.

Key Industry Developments

- In 2023, 3M expanded its premium abrasives portfolio by introducing finer grit grades ranging from 500+ to 1000+ under the 3M™ Cubitron™ line, extending availability across discs and sheet rolls to address high-precision finishing applications.

- In 2020, Asian Paints entered the abrasives segment with the launch of its sanding paper brand TruStar, supported by a quirky, mass-appeal marketing campaign aimed at building strong brand recall among painters and contractors while expanding its decorative solutions portfolio.

Companies Covered in Sandpaper Market

- Robert Bosch Tool Corporation

- 3M Company

- Saint-Gobain Abrasives

- SAIT Abrasivi S.p.A

- Keystone Abrasives

- Klingspor AG

- Mirka Ltd.

- Abrasiflex Pty Ltd

- Abcon industrial products Ltd

- Astro Pneumatic Tool Company

- GISON Machinery Co.,Ltd.

- Flexipads

- Jin Gwang Industries Co., Ltd. (ConfiAd)

- Other Market Players

Frequently Asked Questions

The Sandpaper market is estimated to be valued at US$ 1,049.9 Mn in 2026.

The key demand driver for the sandpaper market is the sustained growth in surface finishing requirements across construction, automotive, woodworking, and industrial manufacturing sectors.

In 2026, the Asia Pacific region will dominate the market with an exceeding 45% revenue share in the global Sandpaper market.

Among applications, woodworking has the highest preference, capturing beyond 40% of the market revenue share in 2026, surpassing other applications.

Robert Bosch Tool Corporation, 3M Company, Saint-Gobain Abrasives, SAIT Abrasivi S.p.A, Keystone Abrasives, and Klingspor AG. There are a few leading players in the Sandpaper market.