- Plastics, Polymers & Resins

- Rotomolding Resins Market

Rotomolding Resins Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Rotomolding Resins Market by Resin Type (Polyethylene (PE) - Low-Density (LDPE), Linear Low-Density (LLDPE), High-Density (HDPE), Cross-linked (XLPE), Others; Polypropylene (PP), Polycarbonate (PC), Polyvinyl Chloride (PVC), Others), Application (Tanks & Containers, Automotive Components, Toys, Industrial Products, Others), Regional Analysis, 2025 - 2032

Rotomolding Resins Market Size and Trend Analysis

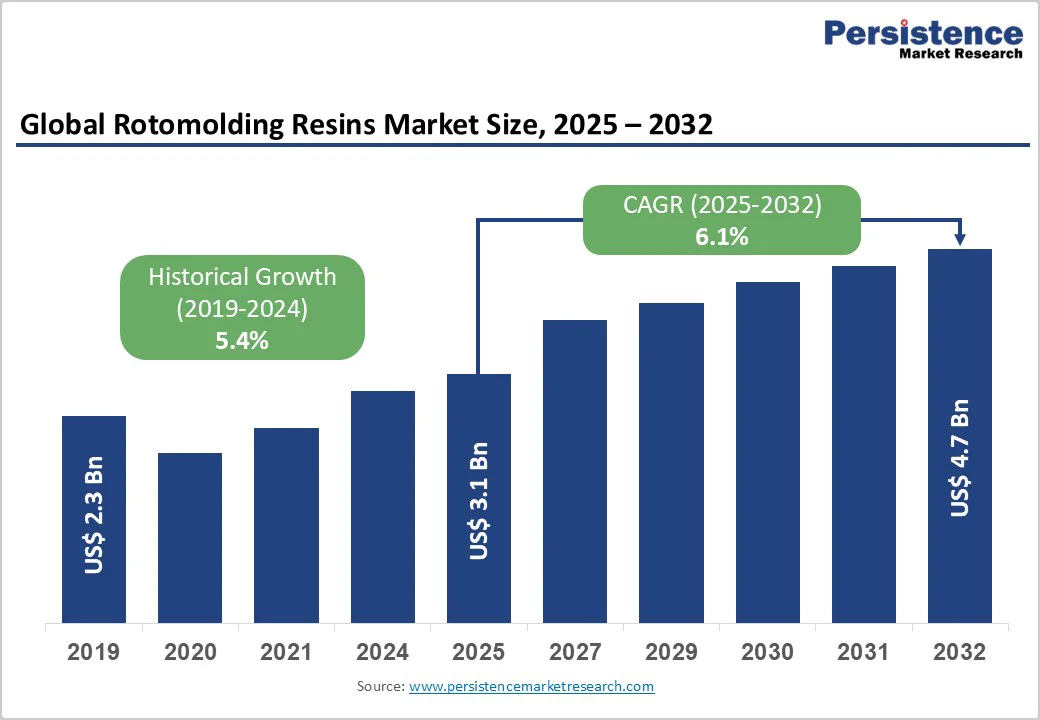

The global rotomolding resins market size was valued at US$3.1 billion in 2025 and is projected to reach US$4.7 billion, growing at a CAGR of 6.1% between 2025 and 2032.

The market expansion is primarily driven by the increasing demand for lightweight and durable plastic products across automotive, infrastructure, and agricultural sectors, coupled with the process advantages of rotational molding that enable the production of complex hollow parts with uniform wall thickness at competitive costs. The rising adoption of rotomolded components in water storage applications and the growing emphasis on sustainable manufacturing practices through recycled resin use are significantly driving market momentum.

Key Market Highlights

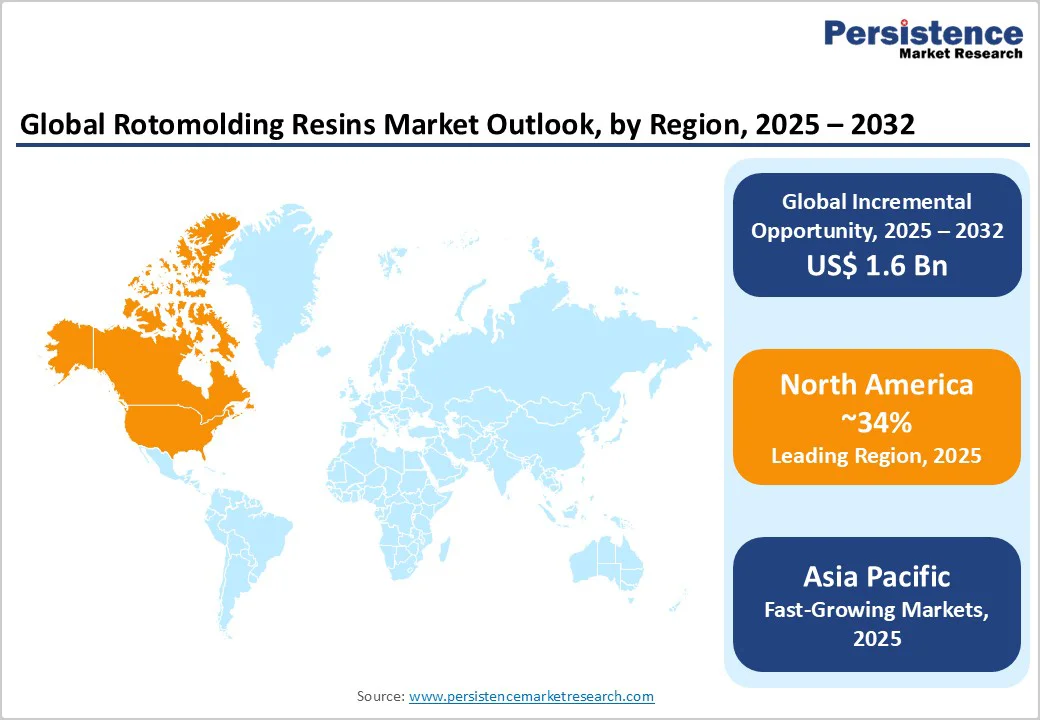

- Leading Region: North America leads the global rotomolding resins market with a 34% share, supported by abundant shale gas feedstock, strong petrochemical production, and innovation in sustainable resin technologies.

- Fastest-Growing Region: Asia Pacific holds around 31% share and is the fastest-growing region, driven by rapid industrialization, infrastructure expansion, and cost-efficient manufacturing in China and India.

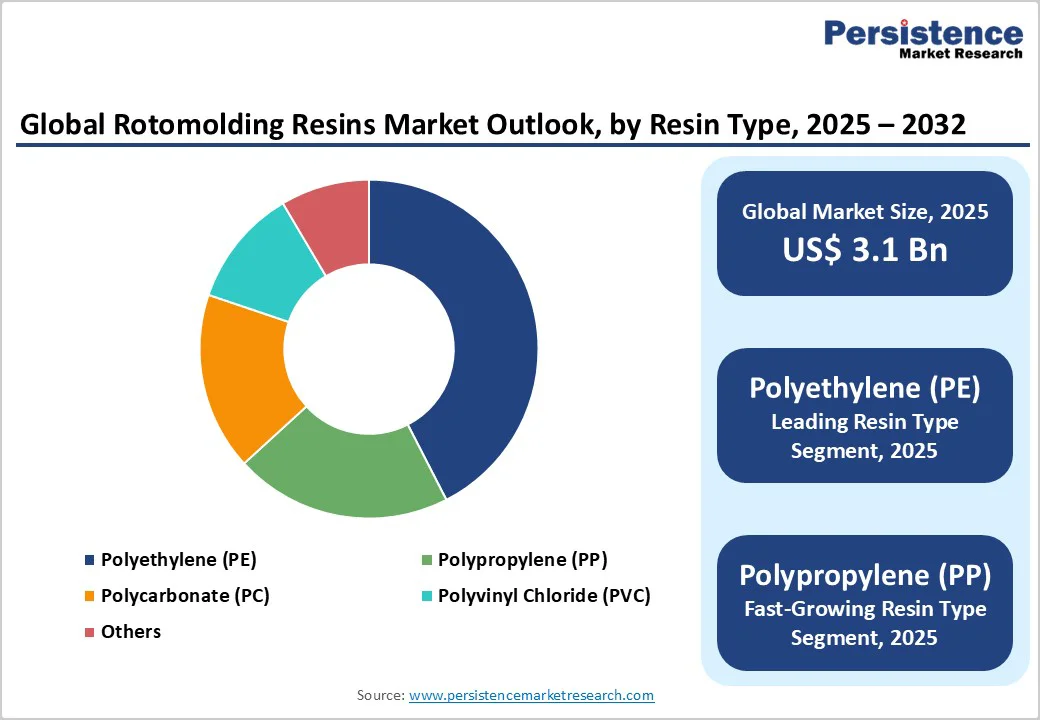

- Leading Category: High-Density Polyethylene (HDPE) dominates the resin type segment with ~52% share, owing to its superior strength, UV resistance, and versatility across multiple end-use sectors.

- Fastest-Growing Category: Linear Low-Density Polyethylene (LLDPE) is the fastest-growing resin, with a 6.8% CAGR, driven by its durability, flexibility, and improved processability.

- Key Market Opportunity: Rising adoption of bio-based and recycled resins with up to 50% renewable content and 91% post-impact strength retention underscores the market’s shift toward circular economy practices.

| Key Insights | Details |

|---|---|

|

Rotomolding Resins Market Size (2025E) |

US$3.1 Bn |

|

Market Value Forecast (2032F) |

US$4.7 Bn |

|

Projected Growth CAGR (2025-2032) |

6.1% |

|

Historical Market Growth (2019-2024) |

5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Surging Demand from Water Infrastructure and Agricultural Sectors Propelling Market Expansion

The rotomolding resins market is experiencing robust growth driven by escalating global demand for water storage and management solutions. According to UNICEF, half of the world's population could be living in areas facing water scarcity by as early as 2025, with some 700 million people potentially displaced by intense water shortages. This alarming trend has intensified investment in water infrastructure, particularly in emerging economies, where governments are prioritizing conservation and large-scale projects, including the widespread adoption of storage solutions. In China, the national plan prioritizes water conservation initiatives, while India's rural development programs are driving strong demand for affordable and durable plastic tanks for rainwater harvesting and storage.

The plastic water storage tank market size is likely to reach a positive CAGR by 2032. Polyethylene resins used in rotomolding offer excellent chemical resistance, durability, and cost-effectiveness, making them the preferred material choice for manufacturing water tanks ranging from 500 liters to 150,000 liters in capacity. The agricultural sector further amplifies demand as rotomolded products, including spray tanks, chemical storage containers, and feeding troughs, become essential equipment for modern farming operations globally.

Automotive Industry Lightweighting Initiatives Driving Rotomolding Resin Adoption

The automotive industry’s drive for vehicle lightweighting to improve fuel efficiency and meet emission norms is fueling rotomolding resin adoption. According to the U.S. Department of Energy, a 10% reduction in vehicle weight can enhance fuel economy by 6–8%, prompting manufacturers to replace metal parts with lightweight plastics. Rotomolded polyethylene components are increasingly used for fuel tanks, bumpers, interior parts, and battery enclosures owing to their high strength-to-weight ratio.

The shift toward electric vehicles has further expanded opportunities, with rotomolding used for battery housings and structural components that require both light weight and insulation. Advances in resin formulations that improve impact resistance, UV stability, and recyclability also align with circular-economy goals, strengthening the material’s role in sustainable automotive manufacturing.

Barrier Analysis - Volatility in Raw Material Prices Constraining Market Growth

The rotomolding resins market faces challenges due to fluctuations in polyethylene and polypropylene prices, which directly impact production costs and profitability. Polyethylene prices experienced notable movement through 2024, with July marking the highest monthly increase of $0.05/lb. These fluctuations stem largely from crude oil market volatility, as polyethylene is derived from petroleum-based feedstocks, making resin prices highly sensitive to energy market changes. Supply chain disruptions caused by geopolitical conflicts and drought-induced shipping delays have further worsened cost pressures.

During 2024, Gulf Coast warehouses reached capacity due to vessel backlogs, causing packaging delays and shipment restrictions. Although overall price volatility eased compared to previous years, unpredictable cost swings continue to challenge rotomolding manufacturers operating on tight margins. These fluctuations hinder stable pricing strategies and limit market expansion in cost-sensitive regions and applications.

High Energy Consumption in the Rotomolding Process Limits Cost Competitiveness

The rotational molding process requires substantial heating of molds in large ovens, resulting in high energy consumption and increased operational costs. The EU’s annual energy consumption from rotational molding is estimated at around 1.8 TWh, resulting in nearly 750,000 tonnes of CO2 emissions. With energy prices rising globally, particularly in Europe and North America, manufacturers face mounting pressure to enhance energy efficiency. According to the U.S. Energy Information Administration (EIA), energy costs have increased by 5–6% over the past year, adding to production expenses.

Heating cycles in the rotomolding process typically range between 220°C and 350°C, with nearly 73% of total energy used by auxiliary equipment. This high energy intensity makes rotomolding less competitive than injection or blow molding for large-scale production. Although Direct Tool Heating (DTH) technology offers improved efficiency and shorter cycles, high installation costs hinder adoption among small and medium-sized enterprises.

Opportunity Analysis - Growing Adoption of Sustainable and Bio-Based Resins Creating New Market Avenues

The rising global focus on environmental sustainability and circular economy practices is creating strong potential for rotomolding resin manufacturers to introduce bio-based and recycled resin alternatives. Braskem has pioneered green polyethylene derived from sugarcane ethanol, offering a 100% renewable and recyclable solution. Its collaboration with A. Schulman led to rotomolding compounds containing over 50% green plastic with at least 60% biobased content, as per ASTM D6866 standards. These eco-friendly materials lower greenhouse gas emissions while maintaining the same mechanical strength as virgin resins.

Advancements in chemical and mechanical recycling are also enabling higher use of recycled content in rotomolding applications. Studies show that reprocessed polyethylene retains 91% of post-impact residual strength compared to 93% in non-reprocessed materials, demonstrating their suitability for various uses, including food-contact packaging approved by regulatory agencies such as Brazil’s Anvisa.

Emerging Applications in Renewable Energy and Infrastructure Development

The shift toward renewable energy and large-scale infrastructure expansion across emerging economies is creating fresh opportunities for rotomolding resin applications. In solar and wind installations, rotomolded electrolyte storage tanks with UV20+ protection and up to 20 years of service life are becoming preferred for durability and efficiency. Matrix Polymers Australia, using BASF’s Irgastab IS 2520 P UV stabilization system, developed tanks offering superior outdoor performance while cutting production cycle time by up to 10% and reducing CO2 emissions by over 130 tons annually.

Government-led infrastructure programs in the Asia Pacific are also increasing demand for water management, chemical storage, and agricultural equipment. The rise in electric vehicle manufacturing further supports the use of lightweight, thermally stable, and cost-effective rotomolded components, while expanding waste and water treatment projects across developing cities continues to fuel resin consumption.

Category-wise Insights

Resin Type Analysis

High-Density Polyethylene (HDPE) dominates the rotomolding resins market with about 52% share in 2025, owing to its superior mechanical strength, chemical resistance, and cost-effectiveness. It is widely used for industrial containers, storage tanks, and automotive parts due to its tensile strength, impact resistance, and UV stability. HDPE grades such as Marlex HDPE and MDPE from Chevron Phillips Chemical exhibit excellent flow properties, broad processing windows, and outstanding low-temperature durability, making them ideal for high-performance rotational molding applications.

Linear Low-Density Polyethylene (LLDPE) represents the fastest-growing resin type, supported by its superior flexibility, stress-crack resistance, and excellent environmental performance. LLDPE resins are increasingly used for complex, thin-walled parts such as recreational equipment, toys, and small containers. Their ability to maintain toughness at low temperatures and compatibility with colorants enhances their appeal in consumer and outdoor product applications.

Application Analysis

Tanks & Containers leads the rotomolding resins market, holding around 45% share in 2025, driven by rising global demand for water storage, agricultural, and chemical-handling solutions. Rotomolding’s ability to produce large, seamless, and lightweight structures with uniform wall thickness ensures strong adoption in sectors emphasizing cost efficiency and durability.

The automotive components segment is the fastest-growing application, propelled by the industry’s push toward lightweighting and sustainability. Rotomolded parts such as fuel tanks, ducts, and protective housings replace heavier metal components, improving fuel efficiency and reducing emissions. As electric vehicle production scales up, the use of rotomolded polyethylene for battery housings and structural components is expanding rapidly, reinforcing its value in modern vehicle manufacturing.

Regional Insights

North America Rotomolding Resins Market Trends

North America holds a leading 34% share in the global rotomolding resins market, supported by strong manufacturing infrastructure, advanced petrochemical capacity, and continuous innovation. The U.S. benefits from abundant shale gas resources that provide low-cost ethane feedstock, making the region highly competitive in polyethylene production. Key players such as Dow Inc., ExxonMobil Chemical, Chevron Phillips Chemical, and LyondellBasell Industries ensure reliable resin supply through advanced Gulf Coast facilities.

Innovation continues to define the region’s market leadership. NOVA Chemicals’ collaboration with Amcor for recycled polyethylene, and LyondellBasell’s solvent-based LDPE recycling reflect growing sustainability efforts. Dow’s RESILITY resins offer 30% wider processing windows and superior UV protection. With North America producing 4.2 million tons of recycled plastic versus 30 million tons consumed, significant potential remains in recycled resin markets.

Europe Rotomolding Resins Market Trends

Europe rotomolding resin market is expected to achieve a CAGR of 6.5% from 2024 onward, driven by strong sustainability policies, advanced recycling systems, and material innovation capabilities. The region consumes roughly 1.8 TWh of energy annually for rotational molding, corresponding to about 750,000 tonnes of CO2 emissions, prompting investment in low-energy technologies and emission reduction. The EU’s circular economy plan mandates that all plastic packaging be reusable or recyclable by 2030, encouraging material innovation.

Germany, the U.K., France, and Spain remain leading markets, with Borealis advancing circular polymer initiatives through its acquisition of Rialti S.p.A. Borecene Compact PE grades enhance flow properties and processing economics. Projects such as ROTOFLEX have achieved 30% energy efficiency gains, cutting EU emissions by 150,000 tonnes annually. Europe’s harmonized standards further promote bio-based and recyclable resin adoption.

Asia Pacific Rotomolding Resins Market Trends

Asia Pacific holds nearly 31% share and is the fastest-growing region in the rotomolding resins market, fueled by industrialization, infrastructure development, and manufacturing expansion across China, India, Japan, and ASEAN countries. Rapid urbanization and population growth are boosting demand for affordable housing, water storage, and agricultural products. China dominates production capacity, while India’s infrastructure and water conservation projects strengthen regional demand.

Japan specializes in high-precision applications such as automotive and medical components, and Thailand’s PTT Global Chemical has expanded HDPE capacity to serve regional markets. Asia Pacific’s low labor costs, raw material availability, and proximity to global trade routes enhance competitiveness. Rising consumption of storage tanks, toys, and industrial products continues to accelerate the region’s dominance in rotomolding resins.

Competitive Landscape

The global rotomolding resins market is moderately consolidated, characterized by the presence of major petrochemical producers alongside regional manufacturers. Industry participants focus on leveraging large-scale polyethylene production capacities, technological advancements, and global distribution networks to strengthen their competitive positioning. Innovation in resin formulations and the development of sustainable product portfolios remain key differentiation strategies.

Companies are increasingly investing in circular economy initiatives, renewable energy integration, and recycling partnerships to enhance sustainability performance. Continuous expansion through capacity additions, strategic collaborations, and regional diversification supports their efforts to address rising demand and meet evolving regulatory and environmental standards.

Key Market Developments:

- In October 2024, Braskem completed South America's first commercial sale of circular polyethylene produced through chemical recycling to Copobras Group for flexible packaging applications in the pet food segment, marking a major milestone in advancing circular economy principles in the region.

- In April 2024, Braskem launched the HD4601U resin under its Maxio family, specifically designed for rotomolding applications requiring high strength and durability, enabling 7% to 10% reduction in production cycle time and delivering annual natural gas savings of approximately R$130,000 with CO2 emissions reductions exceeding 130 tons.

- In April 2024, Matrix Polymers Australia partnered with BASF to transition to Irgastab IS 2520 P UV stabilization system for rotomolded water storage tanks, achieving extended outdoor durability up to 20 years with UV20+ performance levels while improving manufacturing efficiency and sustainability metrics.

Companies Covered in Rotomolding Resins Market

- LyondellBasell Industries

- Dow Inc.

- SABIC

- Braskem

- Borealis

- PTT Global Chemical

- Matrix Polymers

- INEOS Olefins & Polymers

- ExxonMobil Chemical

- Chevron Phillips Chemical

- Mitsubishi Chemical Corporation

- DuPont de Nemours Inc.

- Lanxess AG

- Reliance Industries Ltd.

- Shaw Polymers

- A. Schulman

- NOVA Chemicals

- Formosa Plastics Corporation

- BASF SE

- Phychem Technologies

Frequently Asked Questions

The global rotomolding resins market is valued at US$ 3.1 billion in 2025 and projected to reach US$ 4.7 billion by 2032, growing at a 6.1% CAGR with rising use in water storage, automotive, and industrial sectors.

Growth is driven by water scarcity boosting storage infrastructure demand and automotive lightweighting improving fuel efficiency through rotomolded polyethylene parts.

HDPE leads with about 52% share due to its superior strength, UV resistance, cost-effectiveness, and wide industrial and automotive use.

North America dominates with a 34% share backed by shale gas feedstock, while Asia Pacific is the fastest-growing region through 2032.

Key opportunities lie in bio-based resins with renewable content and growing use in EVs, renewable energy, and water infrastructure.

Leading players include LyondellBasell, Dow, SABIC, Braskem, and Borealis.