- Smart Packaging

- Rotational Molding Machine Market

Rotational Molding Machine Market Size, Share, and Growth Forecast, 2026 - 2033

Rotational Molding Machine Market By Machine Type (Rock & Roll, Shuttle, Others), Application (Automotive, Material Handling, Others), Capacity, and Regional Analysis for 2026 - 2033

Rotational Molding Machine Market Size and Trends Analysis

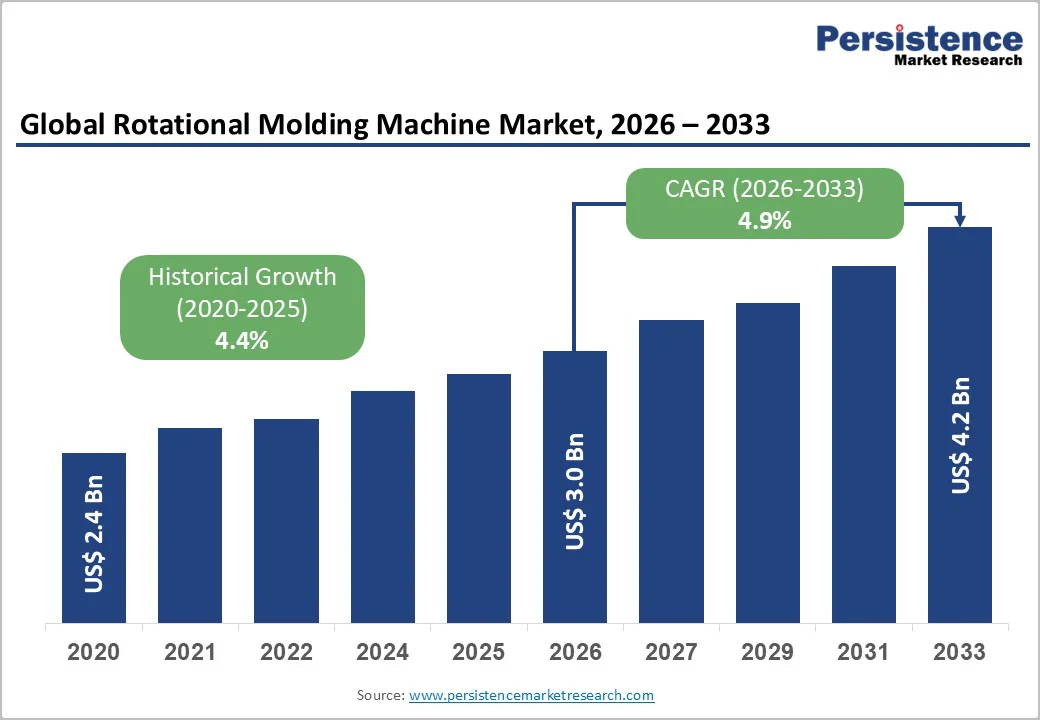

The global rotational molding machine market size is likely to be valued at US$3.0 billion in 2026 and is expected to reach US$4.2 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033, driven by rising demand for lightweight, large-volume hollow polymer components across automotive, tanks, containers, and industrial equipment.

Broader adoption of energy-efficient electric and direct-tool-heating (DTH) platforms is encouraging machine upgrades and improved process control. Contract molders are reinvesting in automation, multi-station capabilities, and retrofittable control architectures to lower energy intensity and meet ESG objectives.

Key Industry Highlights

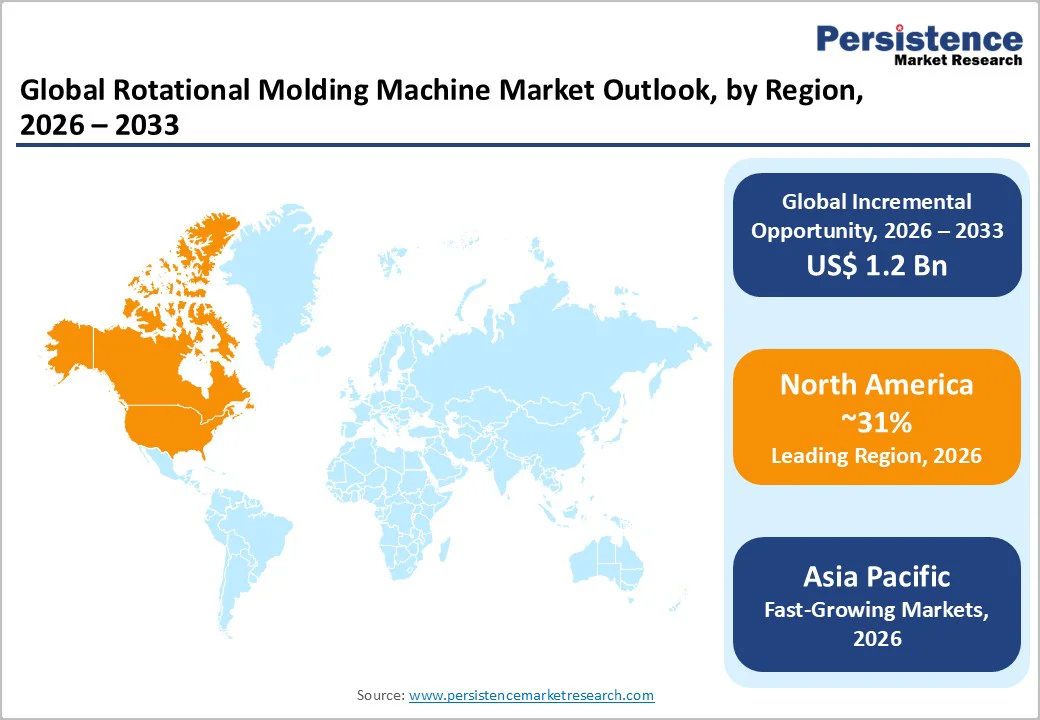

- Leading Region: North America, expected to contribute over 31% of global rotational molding machine revenues, driven by U.S. industrial capacity, advanced automation adoption, and strong demand from tank, automotive, and industrial goods manufacturers.

- Fastest-Growing Region: Asia Pacific, expanding at the highest rate due to rapid industrialization, large-scale water infrastructure development, and capacity additions in China, India, and ASEAN manufacturing clusters.

- Investment Plans: North American and European processors are accelerating investments in electrified heating systems, DTH-compatible platforms, robotic loading, and full-fleet modernization, while APAC processors are prioritizing new capacity build-outs, modular machines, and turnkey production lines.

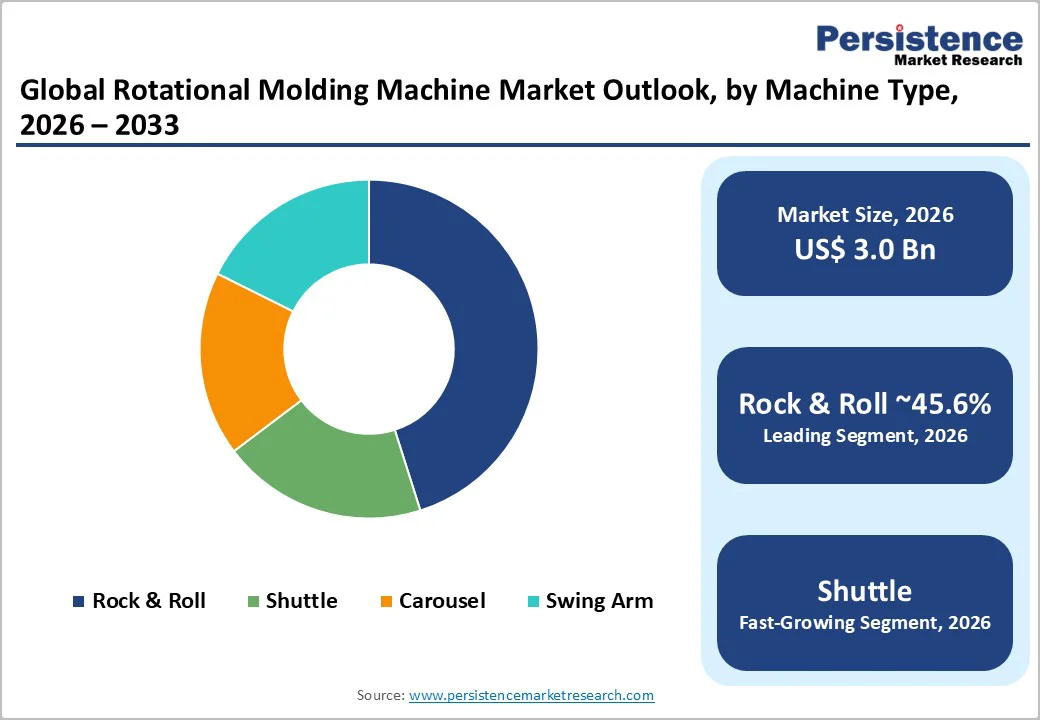

- Dominant Machine Type: Rock & roll machines, to hold approximately 45.6% of the market share in 2026, driven by strong global demand for large tanks, agricultural containers, and long-structure industrial applications.

- Leading Application: Automotive, to represent around 32.4% of total application demand in 2026, supported by growth in lightweighting, EV component housings, precision ducts, protective enclosures, and advanced polymer-based modules.

| Key Insights | Details |

|---|---|

| Rotational Molding Machine Market Size (2026E) | US$3.0 Bn |

| Market Value Forecast (2033F) | US$4.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Lightweighting & Electrification Boost Demand for Large Structural Rotomolded Parts

Automakers are accelerating lightweighting to boost fuel efficiency and EV range, increasing demand for large structural rotomolded parts. Rotational molding enables seamless housings, ducts, reservoirs, and protective structures with complex geometries, uniform wall thickness, and multi-layer construction- key for EV thermal systems, underbody shields, and high-strength components.

Tier-1 suppliers increasingly source multi-kilogram molded parts from contract molders, driving upgrades in high-throughput equipment. This growing demand aligns with OEM platform refreshes and capital expansions, fueling machine sales, higher-spec tooling needs, and modernization of production facilities to support next-generation automotive manufacturing.

Rising Adoption of Energy-Efficient Heating Technologies and Industry 4.0 Systems

Market adoption of electrically heated ovens, DTH tooling, and closed-loop thermal systems is accelerating as manufacturers aim to reduce total operating cost and improve sustainability metrics. These technologies lower cycle energy consumption and scrap rates, delivering operating-cost reductions of 5-15% based on documented plant trials.

Integration of smart sensors, PLC/SCADA systems, and predictive-maintenance algorithms improves overall equipment effectiveness (OEE) and minimizes unplanned downtime. Machine builders offering automation-ready platforms, robotic loading, programmable controls, and advanced monitoring are gaining competitive traction. The shift toward digital production ecosystems drives recurring investments in high-efficiency and data-driven machine fleets.

Expansion of Contract Molding Services and Industrialization in Emerging Markets

North America and Europe are seeing consolidation among contract molders, with larger processors expanding capacity to meet diverse market demand. This boosts average order sizes and favors flexible machine configurations such as carousel, independent-arm, and shuttle systems.

In the Asia Pacific, rapid industrialization in China, India, and key ASEAN countries drives growth in agricultural equipment, municipal water storage, and industrial containers, increasing demand for mid- and large-capacity machines. Expanding local OEM production, public-sector projects, and export-oriented manufacturing are fueling new machine installations and tooling purchases across the region.

Barrier Analysis - High Capital Intensity and Extended Payback Periods for Automated Production Cells

Advanced rotational molding systems that incorporate automated handling, multi-station independent arms, and DTH tooling require significant capital investment. Small and medium-sized processors often struggle to justify these expenditures when production visibility or long-term contract security is limited.

Documented payback periods for fully automated lines typically range from 2 to 5 years, depending on production mix, utilization rates, and local energy costs. This financial barrier slows the adoption of next-generation systems in price-sensitive regions and restricts upgrades to larger processors with diversified product portfolios.

Supply-Chain Instability for Specialized Polymer Powders and Precision Tooling

Rotational molding relies on high-specification polymer powders, colorants, and aluminum tooling, all of which face occasional supply constraints. Fluctuations in resin availability increase material costs for processors, while long lead times for precision-machined molds can delay equipment commissioning.

These uncertainties create scheduling risks for machine buyers and may force production rescheduling or capacity deferral. The overall impact is a slowdown in investment momentum when supply-chain volatility is elevated, particularly for companies operating with thin margins or limited inventory buffers.

Opportunity Analysis - Retrofitting and electrification of existing machine fleets

A substantial portion of the global installed base still relies on gas-heated ovens and legacy control systems, presenting a sizable retrofit opportunity. Electrification kits, DTH-compatible tooling retrofits, and modernized PLC control packages are increasingly being adopted to reduce energy intensity and meet corporate sustainability mandates.

If only one-third of existing equipment qualifies for retrofit and retrofit pricing averages 10-20% of a new machine, the addressable aftermarket represents a significant multi-year revenue pool for machine builders and service providers. Retrofit potential is especially high in North America and Europe, where energy-efficiency upgrades are strongly incentivized.

Expansion into emerging markets with modular, cost-efficient machine platforms

Demand for cost-effective machines is rising in APAC and Latin America as domestic molders expand production capacity for tanks, containers, agricultural components, and industrial equipment. Manufacturers offering modular, easily serviceable carousel and shuttle machines can capture substantial growth by aligning with local price points and operational preferences.

Even modest penetration gains in these fast-growing, high-volume regions can yield meaningful increases in shipments. Flexible financing packages, on-site training, and local spare-parts networks further strengthen opportunities for global machine producers seeking to build long-term market presence.

Integrated sustainability-oriented solutions

Sustainability mandates are reshaping procurement decisions among OEMs and public-sector buyers. Machines designed to handle recycled polymer powders, achieve consistent wall thickness with variable materials, and support multi-layer or foam-core construction unlock new value streams.

Early adopters have shown measurable material savings and emissions reductions, strengthening the business case for sustainability-oriented machinery. Integrated solutions that package machines, tooling, process control systems, and powder-handling equipment position suppliers to win high-value contracts, especially in sectors pursuing closed-loop material programs or designing components for extended lifecycles.

Category-wise Analysis

Machine Type Insights

Rock & roll machines are likely to dominate the market in 2026, accounting for 45.6% of installations, due to their suitability for large, elongated, or cylindrical components such as water storage tanks, chemical containers, septic tanks, and marine pontoons. Their dual-axis oscillating motion ensures efficient resin distribution over long mold surfaces, making them the preferred choice in the U.S., India, and Southeast Asia.

Companies such as Sintex (India) and regional tank manufacturers in Texas and Florida expanded rock & roll capacity in 2024 - 2025 to meet municipal and agricultural water-storage demand. Investments in advanced thermal controls, reinforced ovens, and energy-efficient or electrified heating enhance part consistency and energy efficiency.

Shuttle machines are likely to be the fastest-growing segment, valued for their flexibility, cost-efficiency, and compatibility with small- to medium-sized components. Their two-arm shuttle motion enables asynchronous operation, allowing processors to manage molds with different heating and cooling needs.

Adoption is rising in automotive, material-handling, industrial packaging, and consumer-product sectors, where diverse product mixes and variable batch volumes demand versatility.

Automotive suppliers in the U.S., Mexico, and Germany use shuttle systems for air ducts, EV component housings, tool cases, and protective enclosures, benefiting from improved repeatability and shorter cycle times. Recent installations by Centro Inc. and ROTOTEC feature robotic loading, real-time temperature mapping, and integrated HMI analytics.

Application Insights

The automotive segment is expected to lead rotational molding demand in 2026, accounting for about 32.4% of global consumption. Growth is driven by lightweight structures, aerodynamic parts, modular subsystems, and EV-ready enclosures, encouraging adoption of precision rotomolding platforms.

Key components, including air ducts, DEF tanks, HVAC housings, battery-cooling enclosures, fluid reservoirs, fender liners, and battery-module covers, require uniform wall thickness and complex geometries achievable with modern systems.

Tier-1 suppliers in the U.S., Germany, and Japan, supporting OEMs such as GM, Ford, Stellantis, Toyota, and BMW, expanded capacity in 2024-2025 for electrification and light-vehicle upgrades. New plants in Mexico’s automotive corridor also added advanced shuttle and independent-arm systems for cross-border supply needs.

Material handling is estimated to be the fastest-growing application, driven by rising demand for durable pallets, IBCs, bins, dunnage systems, reusable packaging, and logistics containers. The expansion of e-commerce fulfillment, warehousing automation, and industrial logistics has increased the need for robust, customizable plastic-handling solutions.

Companies such as ORBIS (U.S.), Schoeller Allibert (Europe), and Supreme Industries (India) are investing in shuttle and carousel systems to meet higher orders for heavy-duty pallets and reusable modules. Rotational molding adoption is growing in automated warehouses, producing AGV-compatible pallets, RFID-enabled bins, and impact-resistant totes.

Sustainability initiatives further boost demand across manufacturing, food & beverage, retail, and automotive logistics.

Regional Insights

North America Rotational Molding Machine Market Trends - Electrification, Automation, and Nearshoring-Led Modernization

North America is anticipated to lead in 2026, accounting for over 31% of global rotational molding machine revenues, driven by its mature industrial ecosystem and strong manufacturing specialization. The U.S. leads regional demand, supported by a robust contract molding base, diverse industrial applications, and early adoption of advanced automated machinery.

Machine purchases are often influenced by replacement cycles and modernization programs, as processors transition from older gas-fired ovens to electric and digitally controlled systems. Companies such as Solar Plastics (Minnesota) and Norwesco (Texas) have recently invested in upgraded multi-arm carousel systems to meet growing demand for industrial tanks and agricultural products.

The U.S. market is bolstered by automotive Tier-1 suppliers and major industrial molders adopting high-capacity machines for technical products. Infrastructure projects, particularly municipal water management initiatives, drive demand for mid- and large-capacity water and chemical storage tanks.

Mexico is emerging as a key growth node due to nearshoring trends, with firms such as Grupo Rotoplas expanding rotomolding capacity between 2023 and 2025 to supply regional demand for storage tanks and consumer goods.

The adoption of energy-efficient and automated machinery further accelerates growth. Contract molders and OEMs increasingly invest in electrified heating systems, precision monitoring, and automation to boost productivity and meet ESG mandates.

Regulatory requirements and sustainability commitments are driving the replacement of legacy gas ovens with electric or hybrid systems. Companies such as Dutchland Plastics upgraded their fleets in 2024 with low-emission heating to reduce operating costs and comply with customer sustainability standards, reinforcing the shift toward modern, automated technologies.

Europe Rotational Molding Machine Market Trends - Energy-Efficient, Regulation-Driven Advanced Machinery Adoption

Europe is a leading region for technologically advanced rotational molding machinery, driven by strong engineering hubs in Germany, Italy, the UK, and France.

The region emphasizes energy efficiency, precision manufacturing, and regulatory compliance, fostering adoption of electrified or hybrid heating systems and DTH-compatible platforms. Italian suppliers such as Caccia Engineering, Persico, and Rotomachinery Group (Italy/Canada) provide high-automation systems widely used in industrial and automotive sectors.

Germany leads demand, with manufacturers adopting automated molding systems for technical parts and lightweight structural components. Since 2023, several German processors have implemented robotic loading and automated mold-handling systems to address labor shortages and improve cycle-time consistency.

Europe’s regulatory environment strongly influences equipment purchases. The EU’s Fit for 55 package, energy-efficiency directives, and circular-economy mandates encourage machinery that supports the use of recyclable materials, lower emissions, and smart thermal management.

Manufacturers in France and Germany are shifting to electric ovens and data-driven thermal profiling to meet sustainability targets and regulatory obligations. Buyers increasingly demand systems compatible with high levels of reclaimed or reprocessed powders, reflecting the EU’s recycling focus.

Investment trends include growing use of robotics for loading and unloading, collaborative R&D on advanced materials, and modernization of aging fleets across Central and Western Europe.

Asia Pacific Rotational Molding Machine Market Trends - High-Growth Industrial Expansion with Large-Capacity Machine Scaling

The Asia Pacific region is the fastest-growing market for rotational molding machinery, driven by industrialization, urban infrastructure expansion, and growing domestic manufacturing. Countries such as China, India, Japan, and ASEAN economies are scaling production of industrial containers, tanks, automotive parts, marine products, and consumer goods.

Growth is supported by modular machinery platforms meeting diverse capacity needs. Since 2023, China and India have significantly increased machine installations to expand capacity for water tank production, logistics equipment, and automotive components. China leads demand, with major processors such as Xiamen Dongfang, Jiangsu Wenhao, and Beijing Jingwei upgrading fleets with automated carousel systems for domestic and export markets.

India’s market is expanding rapidly, fueled by local machine builders and tooling manufacturers. Companies such as Sintex, Supreme Industries, and NILKamAL have modernized equipment with higher-efficiency ovens and multi-arm systems to meet rising demand for agricultural tanks, road-safety products, and industrial housings.

Mid- and large-capacity machines are particularly sought after for water tanks, agricultural containers, and logistics products. Automotive applications are gaining traction in Japan, South Korea, and China, where manufacturers require precision-controlled systems for technical components.

Government initiatives and industrial policies further support regional growth. China’s manufacturing-modernization strategies, India’s production-linked incentive (PLI) schemes, and ASEAN industrial investment programs encourage procurement of new or locally produced machinery.

Strong industrial expansion, rising consumption of tanks and containers, and the need for cost-effective, high-efficiency machinery continue to drive investments in rotational molding across APAC.

Competitive Landscape

The global rotational molding machine market is moderately fragmented, with global OEMs supplying high-end automated systems and regional manufacturers targeting cost-sensitive segments. Premium players lead in independent-arm and electrified machines due to engineering complexity and after-sales requirements, while APAC markets have many smaller builders offering affordable carousel and shuttle systems.

Market concentration is higher in advanced segments requiring process control, DTH tooling integration, and automation, creating barriers to entry. Leaders focus on electrification, DTH heating, and data-driven process control, leveraging service monetization, retrofits, and geographic expansion. Differentiation relies on automation, tooling compatibility, and comprehensive support, including training and lifecycle services.

Key Industry Developments

- In January 2025, Rotomachinery Group announced a new rotomolding machine design that reduces the required rear space for oven doors by using a split-door, double-motor configuration, enabling installation in tighter factory layouts and improving flexibility for customers.

Companies Covered in Rotational Molding Machine Market

- Ferry Industries

- Rotomachinery Group

- Persico Industrial

- Reinhardt Roto Machines

- Maka Machinery

- Ningbo Rotational Moulding Technology

- Rotoline

- Granger Plastics Machinery

- Crossfield Extru-Mould

- Polivinil Rotomachinery

- Roto Speed Manufacturing

- Orex Rotomoulding

- Bucher Emhart Glass (Roto Division)

- Nanjing Beite Plastic Machinery

- Wintec Machinery

- Pinette Emidecau Industries (PEI)

- Caccia Engineering

- Zhongda Machinery

- Rotoplast

- Sharma Engineering

Frequently Asked Questions

The global rotational molding machine market size is estimated to reach US$3.0 billion in 2026.

The market value is projected to reach US$4.2 billion by 2033, supported by the modernization of manufacturing fleets and rising demand across automotive, tanks & containers, and material-handling applications.

Key trends shaping the market include the electrification of heating systems and the adoption of Direct-Tool Heating (DTH) technologies for energy efficiency and increased installation of robotic automation for mold handling and process monitoring.

By machine type, rock & roll machines lead the market with approximately 45.6% share, mainly due to their dominance in tank and container production.

The rotational molding machine market is projected to grow at a CAGR of 4.9% between 2026 and 2033.

Key companies include Ferry Industries, Rotomachinery Group, Persico Industrial, NingBo Rotational Moulding Technology, and Sharma Engineering.