- Agrochemicals

- Rodenticide Market

Rodenticide Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Rodenticide Market by Form Type (Pellets, Blocks, Powder), Product Type (Anticoagulant, Non-anticoagulant), Application Type (Agriculture, Pest Control Companies, Warehouses, Urban Centers, Household), and Regional Analysis for 2025 - 2032.

Rodenticide Market Size and Forecast Analysis

Market Overview

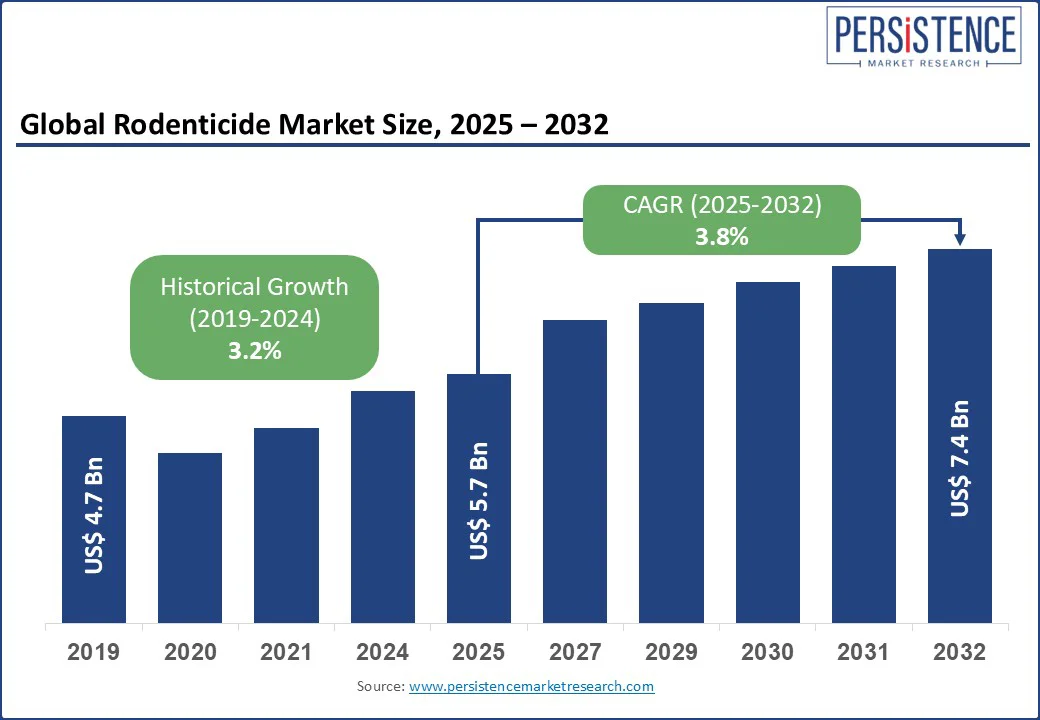

The global Rodenticide Market is likely to be valued at US$ 5.7 Bn in 2025 and reach US$ 7.4 Bn by 2032, achieving a CAGR of 3.8% from 2025 to 2032. This growth is fueled by increasing rodent populations, rising demand for pest management solutions, and advancements in rodenticide formulations.

The global rodenticide market is a critical component of the pest control industry, driven by the ongoing need to manage rodent infestations that threaten agriculture, urban centers, and public health. The sector’s expansion is supported by innovations in anticoagulant and non-anticoagulant rodenticides, growing awareness of rodent-related health risks, and increasing demand for effective rodent control in agricultural and urban settings. Rodenticides, available in forms such as pellets, blocks, and powder, are essential for mitigating crop losses, protecting stored goods, and preventing disease transmission.

North America leads the rodenticide market, followed by Europe and the rapidly expanding Asia Pacific, propelled by robust agricultural sectors, urbanization, and supportive regulatory frameworks. The industry is highly competitive, with key players focusing on eco-friendly formulations and strategic partnerships to enhance pest management solutions.

Market Dynamics

Drivers

The technology’s unique capabilities and expanding applications are boosting the market. The rodenticide market is experiencing robust growth driven by the technology’s exceptional capabilities in addressing rodent infestations that cause significant economic and health impacts. Rodenticides are critical for rodent population control, as they prevent damage to crops, contamination of food, and the spread of rodent-borne diseases such as Hantavirus and plague. For instance, the CDC advises controlling rodent populations to reduce transmission of plague, as infected fleas may seek new hosts if rodents are eliminated improperly. Their use is expanding in agriculture, pest control, warehouses, urban centers, and households. As industries pursue food security and public health, rodenticides offer significant advantages over traditional anti-rodent solutions. Continuous R&D enhances formulation safety and efficacy, reinforcing their role in integrated pest management (IPM) strategies.

Rising agricultural and urban demands fuel rodenticide adoption.

Rodenticides play a vital role in safeguarding global food security and urban infrastructure. In agricultural settings, rodents are responsible for 5-10% of crop losses annually in Asia, highlighting the urgent need for effective pest control to protect yields. Simultaneously, rapid urbanization over 50% of the global population now residing in urban areas, according to the World Bank, intensifying the demand for rodent control in cities, where infrastructure and hygiene are at risk. This dual pressure from agricultural and urban sectors is driving the rodenticide market forward, with growing interest in advanced, non-toxic, and environmentally safe rodent control solutions to meet evolving regulatory and safety standards.

Restraints

- Stringent Regulatory Restrictions: Stringent regulatory restrictions are a major restraint in the rodenticide market, particularly concerning the use of anticoagulant-based formulations. Regulatory bodies such as the U.S. Environmental Protection Agency (EPA) and the European Union’s Biocidal Products Regulation (BPR) have implemented strict guidelines to limit the environmental and health risks associated with rodenticide use. These regulations often restrict consumer access, mandate secure packaging, and limit concentrations of active ingredients, thereby complicating product development and distribution. Such compliance challenges increase operational costs for manufacturers and discourage innovation, while also reducing the availability of high-potency rodenticides in the rodenticide market, ultimately hindering overall growth potential.

Opportunities

- Advancements in Eco-Friendly Formulations: Innovations in eco-friendly rodenticide formulations, including bio-based alternatives and targeted delivery systems, present significant growth opportunities for the rodenticide market. Companies are increasingly focusing on developing non-toxic solutions that minimize environmental impact while maintaining effectiveness in pest control. For instance, firms such as EcoClear Products are pioneering safer options suited for residential and urban use. Additionally, ongoing research supported by institutions such as the U.S. Department of Agriculture is driving advancements in cost-efficient and scalable production methods. These developments support broader adoption of sustainable rodenticides, aligning with growing consumer demand for environmentally responsible pest control solutions.

- Public-Private Partnerships: Public-private partnerships are playing a critical role in advancing rodenticide market growth, particularly in emerging economies. Collaborations such as Bayer AG’s alliance with agricultural cooperatives exemplify how combining private sector innovation with public sector reach can enhance pest control infrastructure. These initiatives aim to improve farmer access to effective rodenticides, promote sustainable pest management practices, and reduce crop losses in agriculture-dependent regions. By leveraging shared resources and knowledge, such partnerships help scale distribution, ensure regulatory compliance, and drive awareness, ultimately supporting broader adoption of rodenticides and fostering long-term market expansion in high-need areas.

Category-wise Analysis

Form Type Insights

Among form types, pellets lead due to their ease of use, controlled release, and versatility in bait stations for agricultural and urban applications. In 2025, pellets accounted for a 45% market share. Blocks are the fastest-growing form, driven by their durability and suitability for outdoor environments, due to increased adoption in warehouses and urban centers.

Product Type Insights

Among product types, anticoagulant rodenticides lead due to their high efficacy, single-feed lethality, and widespread use in agriculture and pest control. In 2025, this segment held a Substantial market share by volume, driven by formulations such as bromadiolone and brodifacoum. Non-anticoagulant rodenticides, such as bromethalin and zinc phosphide, are the fastest-growing, fueled by demand for fast-acting solutions and regulatory restrictions on anticoagulants in regions such as North America and Europe.

Application Type Insights

Among application types, agriculture leads due to its critical role in protecting crops and stored grains, holding a 60% market share in 2025. Pest control companies are the fastest-growing segment, driven by the increasing outsourcing of rodent management in urban and commercial settings, due to rising demand for professional pest control services.

Regional Insights

North America Rodenticide Market Trends

North America holds the largest market share at 40% in 2024, with the U.S. contributing significantly due to its advanced agricultural sector and high pest control demand. The U.S. Rodenticide Market growth is highlighted based on:

- High Pest Control Demand: Rodent infestations remain a major concern in agriculture and urban areas. The U.S. Department of Agriculture identifies rodent-related crop damage as a key economic issue, prompting widespread adoption of rodenticides across farming operations and municipal pest control.

- Technological Innovation: Leading companies such as Bell Labs and Liphatech, Inc. are pioneering improved rodenticide delivery methods and active ingredients. These advancements enhance product effectiveness while meeting environmental and safety standards.

- Government Support: Regulatory frameworks established by the EPA support the responsible use of rodenticides. Continued approval of specific formulations for both agricultural and urban settings strengthens market confidence and encourages broader adoption.

Europe Rodenticide Market Trends

Europe is a fast-growing market for rodenticides and is projected to experience an upward trend in the forthcoming years, driven by rising pest management needs in both agricultural and urban environments. European countries are expected to see increasing adoption of eco-friendly and compliant rodent control solutions.

- Germany: Strong agricultural infrastructure and government-backed pest control initiatives are driving demand. Rodenticide use has risen due to persistent rodent-related crop threats, especially in grain-producing regions.

- U.K.: Urban pest management is a key focus, supported by the British Pest Control Association’s emphasis on integrated pest control and the shift toward safer rodenticide alternatives in cities.

- France: The country is advancing sustainable pest management, with companies promoting bio-based rodenticides. Regulatory support for low-toxicity products is reinforcing the transition to environmentally responsible pest control strategies.

Asia Pacific Rodenticide Market Trends

- India: Growing agricultural activities and national initiatives such as the Swachh Bharat Mission are driving strong demand for rodenticide pellets and blocks across both rural and urban regions. With increasing concern over crop losses and urban hygiene, the rodenticide market is seeing steady expansion through integrated pest control adoption.

- China: Rapid urbanization, coupled with an expanding agricultural base, is creating substantial demand for effective rodenticides. Multinational companies are increasing their regional footprint, and the shift toward more efficient pest control solutions is fueling consistent market growth.

- Japan: Government-led pest management campaigns are encouraging the use of advanced rodenticides, particularly non-anticoagulant formulations, in urban environments. These initiatives are reinforcing public health infrastructure and promoting eco-conscious pest control practices.

Competitive Landscape

The global rodenticide market is highly competitive, with companies dominating through extensive product portfolios and global distribution networks. Players such as BASF SE and Bayer AG invest heavily in R&D to develop eco-friendly rodenticide formulations, such as non-anticoagulant rodenticides. Collaborations with agricultural cooperatives, as seen with Rentokil Initial plc’s partnerships, enhance market penetration in high-demand regions. Companies such as Neogen Corporation are expanding in Asia Pacific through localized manufacturing and distribution.

Key Developments

- 2024: BASF SE launched a new eco-friendly rodenticide pellet, improving safety by 15% for non-target species.

- 2023: Bayer AG partnered with agricultural cooperatives to expand rodenticide access in India, reducing crop losses by 10%.

- 2022: Rentokil Initial plc introduced an advanced rodenticide block for urban pest control, enhancing durability by 20%.

Companies Covered in Rodenticide Market

- BASF SE

- Bayer AG

- Rentokil Initial plc

- Neogen Corporation

- Bell Labs

- Liphatech, Inc.

- Impex Europa S.L.

- EcoClear Products

Frequently Asked Questions

The Rodenticide market is projected to reach US$ 5.7 Bn in 2025.

Rising rodent populations, growth in agricultural and urbanization needs, and advancements in eco-friendly formulations are the key market drivers.

The Rodenticide market is poised to witness a CAGR of 3.8% from 2025 to 2032.

Advancements in eco-friendly formulations, public-private partnerships, and expansion in emerging markets are the key market opportunities.

BASF SE, Bayer AG, Rentokil Initial plc, Neogen Corporation, and Bell Labs are key market players.