- Bulk Chemicals

- Rheology Modifiers Market

Rheology Modifiers Market Size, Share, and Growth Forecast 2026 - 2033

Rheology Modifiers Market by Product Type (Organic and Inorganic), Application (Cosmetics and Personal Care, Paints and Coatings, Adhesives and Sealants, Pharmaceuticals, Oil and Gas, Food and Beverages, and Others), and Regional Analysis for 2026 - 2033

Rheology Modifiers Market Size and Share Analysis

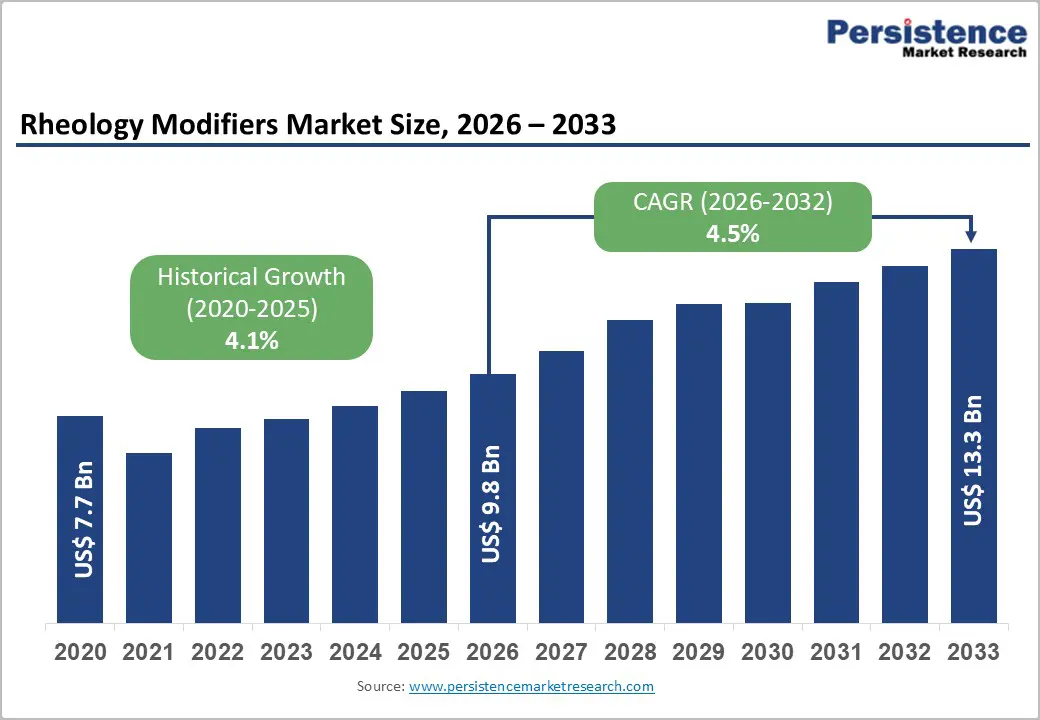

The global rheology modifiers market size is likely to be valued at US$ 9.8 billion in 2026 and is projected to reach US$ 13.3 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

Factors such as the escalating demand from the paints and coatings sector, the burgeoning personal care and cosmetics industry, environmental regulations promoting low volatile organic compound (VOC) formulations and the shift toward sustainable and bio-based products are accelerating the global rheology modifiers market. Robust infrastructure investment in Asia-Pacific regions, creating substantial demand for construction-related adhesives, sealants, and specialty coatings that require advanced rheology modifiers further drives market expansion.

Key Industry Highlights:

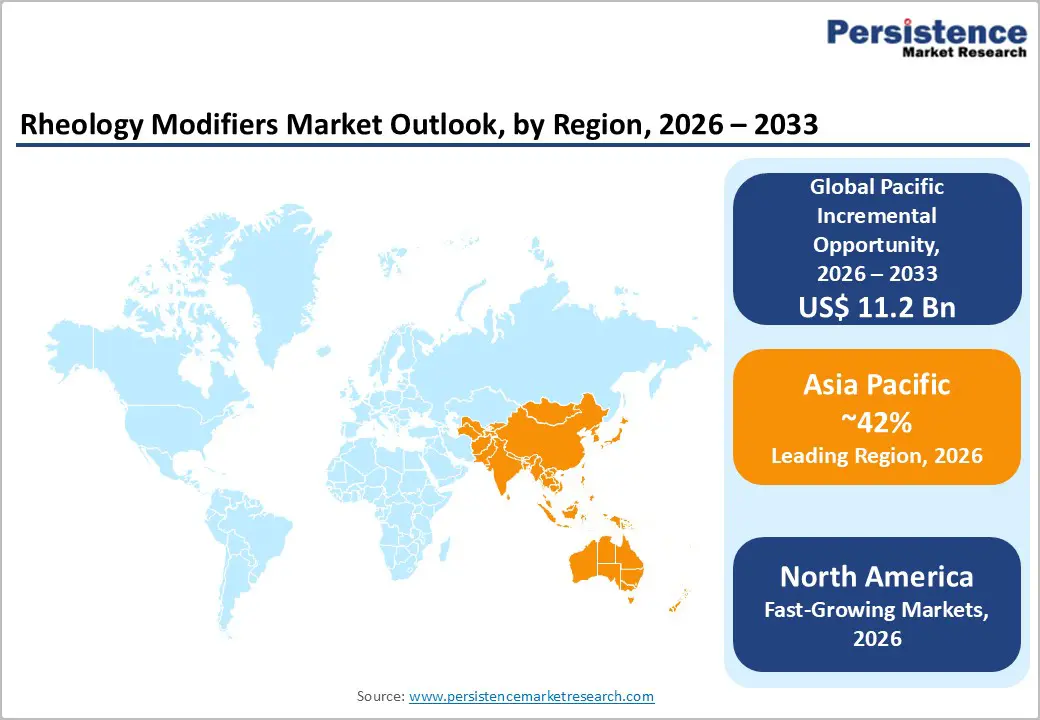

- Leading Region: Asia Pacific emerges as a leading regional market, commanding approximately 42% of global market share with rapid industrialization in China, infrastructure expansion in India, and manufacturing growth across Southeast Asia creating substantial opportunities for rheology modifier manufacturers.

- Fastest Growing Region: North America emerges as a significant regional market, commanding approximately 30% of global market share with mature industrial sectors, stringent regulatory standards promoting innovation, and robust personal care and construction industries driving sustained demand for advanced rheology modifier solutions across multiple applications.

- Dominant Product Type: Organic rheology modifiers dominate product segment, holding 64.7% market share driven by superior performance, versatility in both water-based and solvent-borne formulations, and increasing availability of sustainable alternatives aligning with regulatory and consumer preferences for eco-friendly products.

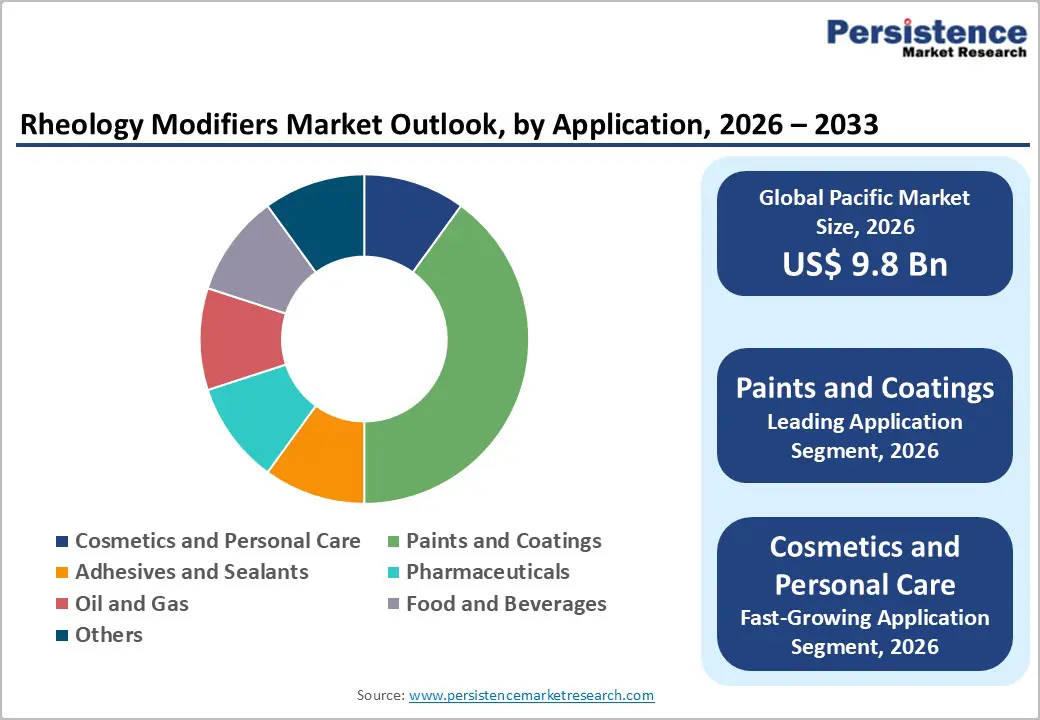

- Dominant Application: Paints and coatings, commanding 34.7% market share with accelerating demand from water-based formulations driven by environmental regulations, construction sector growth, and architectural demand for high-performance coating solutions across developed and emerging markets.

- Key Market Opportunity: Bio-based and natural rheology modifiers present the key growth opportunity, driven by stringent environmental regulations, consumer demand for clean-beauty and sustainable products, and regulatory incentives promoting renewable feedstock.

| Key Insights | Details |

|---|---|

| Global Rheology Modifiers Market Size (2026E) | US$ 9.8 Bn |

| Market Value Forecast (2033F) | US$ 13.3 Bn |

| Projected Growth CAGR(2026 - 2033) | 4.5% |

| Historical Market Growth (2020 - 2025) | 4.1% |

Market Dynamics

Drivers - Rapid Expansion in Paints, Coatings, and Construction Applications

Rheology modifiers are essential formulation components that control viscosity, flow behavior, stability, and application performance in architectural paints, industrial coatings, cementitious systems, adhesives, and sealants. Growth in residential and commercial construction, infrastructure development, and renovation activities directly increases consumption of architectural coatings, protective coatings, mortars, and concrete admixtures, all of which require precise rheological control. The global shift toward water-based, low-VOC, and environmentally compliant formulations has intensified the need for advanced rheology modifiers, particularly in paints and coatings, where maintaining performance while reducing emissions presents technical challenges.

Modern construction practices increasingly rely on ready-to-use materials such as self-leveling compounds, tile adhesives, and high-performance coatings that demand consistent flow, sag resistance, and long-term stability, further elevating the role of rheology modifiers. Urbanization and infrastructure investments, especially in emerging economies, are accelerating demand for durable, easy-to-apply, and energy-efficient building materials, reinforcing growth across the entire value chain. Rising expectations for surface aesthetics, durability, and application efficiency in both construction and decorative coatings are pushing manufacturers to adopt sophisticated rheology solutions.

Expansion into Personal Care, Cosmetics, and Clean Beauty Segments

The growing use of rheology modifiers in personal care, cosmetics, and clean beauty formulations has become a significant growth driver for the global market, driven by rising consumer demand for product performance, sensory appeal, and ingredient transparency. Rheology modifiers are essential in personal care products to control texture, viscosity, spreadability, and stability in creams, lotions, shampoos, conditioners, gels, serums, and color cosmetics. As consumers increasingly associate product quality with feel, consistency, and ease of application, manufacturers rely heavily on advanced rheology control to differentiate their offerings. This demand is further amplified by the rapid growth of the clean beauty movement, which emphasizes natural, bio-based, biodegradable, and non-toxic ingredients.

Clean-label formulations often remove traditional synthetic thickeners, creating a technical need for innovative rheology modifiers derived from cellulose, natural gums, or bio-engineered polymers that deliver performance while meeting regulatory and consumer expectations. Regulatory scrutiny over ingredient safety and sustainability is also encouraging formulators to adopt compliant and skin-friendly rheology solutions. As global cosmetic brands and indie beauty companies alike invest in product innovation and sustainable formulations, rheology modifiers are increasingly utilized as enablers of brand positioning and product value. This convergence of performance requirements, clean beauty trends, and consumer-driven innovation is establishing personal care and cosmetics as a fast-growing, high-margin application segment for rheology modifiers.

Restraint - Stringent Environmental and Chemical Regulations

The implementation of rigorous regulatory frameworks globally, including REACH, FDA regulations, and EPA guidelines, has elevated compliance costs and technical complexity in rheology modifier formulation and manufacturing. Restrictions on hazardous substances, including APEOs (alkylphenol ethoxylates) and volatile organic compounds, have necessitated costly reformulations and process modifications. The requirement for food-contact compliance in certain applications and restrictions on biocide usage have further constrained product development cycles.

European regulations promoting the phase-out of synthetic polymers in favor of natural alternatives create technical challenges, as natural ingredients often exhibit inferior performance characteristics. These regulatory pressures increase research and development expenditures and extended product commercialization timelines, which disproportionately affect smaller manufacturers and new market entrants, creating barriers to market participation.

Performance Limitations and Compatibility Issues in Diverse Formulations

Despite ongoing innovation, rheology modifiers can exhibit performance limitations and compatibility challenges when used across diverse formulations and application environments. Different systems, such as water-based, solvent-based, high-solid, or bio-based formulations, require precise rheological behavior, and not all modifiers perform consistently under varying shear, temperature, or pH conditions. Incompatibility with pigments, surfactants, or other additives can lead to issues such as phase separation, poor flow, or reduced stability. These technical risks discourage formulators from switching suppliers or adopting newer rheology technologies, particularly in high-performance applications where consistency and reliability are critical.

The need for extensive testing and formulation optimization increases development time and cost. This technical complexity, combined with the risk of inconsistent performance, acts as a barrier to widespread adoption and slows the penetration of advanced rheology modifiers in certain end-use segments.

Opportunity - Growing Demand for Sustainable, Bio-Based, and Natural Rheology Modifiers

The rising global demand for sustainable, bio-based, and natural rheology modifiers represents a significant growth opportunity for manufacturers, driven by tightening environmental regulations, corporate sustainability commitments, and changing consumer preferences. End-use industries such as paints and coatings, personal care, construction, and food processing are under increasing pressure to reduce environmental impact by lowering VOC emissions, improving biodegradability, and minimizing reliance on petrochemical-derived ingredients. This shift is accelerating the adoption of rheology modifiers derived from renewable sources such as cellulose, starch, natural gums, and bio-engineered polymers. Unlike conventional synthetic thickeners, these alternatives align with green formulation goals while supporting comparable viscosity control, stability, and performance.

In personal care and cosmetics, the rapid expansion of clean beauty and natural labeling trends is further strengthening demand, as brands seek transparent ingredient lists that resonate with environmentally conscious consumers. Similarly, green building standards and eco-certifications in the construction sector are encouraging the use of sustainable additives in coatings, mortars, and adhesives. This evolving landscape opens opportunities for innovation, premium pricing, and differentiation, as bio-based rheology modifiers often command higher margins due to their functional and sustainability benefits. As sustainability transitions from a compliance requirement to a strategic priority, companies that invest early in bio-based rheology technologies are well positioned to capture long-term demand, expand into regulated markets, and strengthen partnerships with environmentally focused formulators.

Emerging Applications in Food and Beverage Industry with Clean-Label Demand

The increasing adoption of rheology modifiers in the food and beverage industry, driven by the global shift toward clean-label and minimally processed products, is creating a compelling growth opportunity for market participants. Rheology modifiers play a crucial role in food formulations by controlling texture, viscosity, mouthfeel, suspension stability, and shelf-life performance in products such as sauces, dressings, dairy items, beverages, bakery fillings, and plant-based alternatives. As consumers become more health-conscious and ingredient-aware, demand is rising for products made with recognizable, natural, and non-synthetic ingredients. This trend is encouraging food manufacturers to replace conventional artificial thickeners and stabilizers with natural and bio-based rheology modifiers derived from sources such as starch, pectin, guar gum, xanthan gum, and cellulose. Clean-label positioning not only improves consumer trust but also enhances brand differentiation in highly competitive food categories.

The rapid growth of plant-based, low-fat, sugar-reduced, and functional foods has increased the technical need for effective rheology control to replicate traditional taste and texture profiles without compromising nutritional value. Beverage innovation, including protein drinks, dairy alternatives, and fortified beverages, further expands application potential, as these products require stable suspension and consistent flow behavior. Regulatory emphasis on food safety, transparency, and ingredient simplicity is reinforcing this shift, prompting manufacturers to reformulate using approved, label-friendly rheology solutions. This evolving demand landscape offers significant opportunities for suppliers that can deliver natural, high-performance, and cost-effective rheology modifiers tailored to modern food and beverage innovation trends.

Category-wise Analysis

Product Type Insights

The organic rheology modifiers segment, encompassing both synthetic and natural variants, maintains market dominance with approximately 64.7% market share in 2026, reflecting strong demand across paints, coatings, and personal care applications. Synthetic organic modifiers, including hydrophobically modified ethoxylated urethanes (HEURs) and associative thickeners, provide superior thickening efficiency, thermal stability, and viscosity control characteristics essential for high-performance industrial applications. Natural organic modifiers, derived from plant sources and biopolymers, are experiencing accelerating growth due to regulatory pressures and consumer preference for sustainable alternatives.

The segment's dominance is supported by its versatility, superior performance characteristics, and established manufacturing infrastructure. Organic modifiers demonstrate exceptional compatibility with both water-based and solvent-borne systems, enabling formulators to achieve desired rheological properties across diverse industrial applications without compromising environmental compliance or sensory attributes.

Application Insights

The paints and coatings application represents the largest demand segment, commanding approximately 34.7% of total market consumption. This dominance reflects the critical role of rheology modifiers in achieving desired viscosity control, anti-sag resistance, and application properties in architectural coatings, automotive finishes, and industrial protective coatings. Water-based coating formulations, constituting approximately 68.7% of total coating applications, have become the industry standard due to environmental regulations and low-VOC requirements.

The personal care and cosmetics segment is emerging as the fastest-growing application area for rheology modifiers, supported by evolving consumer expectations and premiumization trends. Consumers increasingly associate product quality with texture, stability, spreadability, and sensory feel, prompting manufacturers to invest in sophisticated rheology solutions for creams, lotions, gels, shampoos, and color cosmetics. Growth is further accelerated by clean beauty and natural formulation trends, which require innovative rheology modifiers capable of delivering performance while meeting safety and transparency standards.

Regional Insights

North America Rheology Modifiers Market Trends

North America maintains a significant market position, commanding approximately 30% of global rheology modifiers demand, with a market value of approximately US$ 2.9 billion in 2026. The United States dominates this region through its well-established personal care, paints and coatings, and construction industries, supported by robust research and development infrastructure and stringent regulatory standards promoting product innovation. Recent regulatory developments, including the FDA's 2024 amendments encouraging sustainable and safe ingredients in personal-care products, have accelerated the adoption of eco-friendly rheology modifiers.

The North American paints and coatings sector continues to drive demand, with emphasis on low-VOC and waterborne formulations complying with EPA and state-level environmental regulations. The personal care industry's expansion, reflecting rising consumer spending on premium cosmetic and skincare products with enhanced sensory attributes, creates sustained demand for advanced rheology modifiers. The region's construction sector, supported by infrastructure investment and residential property development, drives demand for adhesives and sealants with enhanced application properties.

Europe Rheology Modifiers Market Trends

Europe is projected to witness a stable growth from 2026 to 2033, driven by stringent environmental regulations and emphasis on sustainable chemistry. Germany emerges as the market leader within the region, leveraging its advanced manufacturing infrastructure and prominence in the automotive and chemical industries. The region's regulatory landscape, characterized by the REACH framework and EU Green Deal, has catalyzed a paradigm shift toward renewable and bio-based rheology modifiers, creating opportunities for innovation and product differentiation.

European manufacturers are increasingly adopting sustainable sourcing practices and renewable feedstock to align with regulatory requirements and consumer preferences for environmentally responsible products.

The personal care and cosmetics sectors in France, Germany, and the United Kingdom demonstrate strong growth, supported by consumer spending on premium beauty products and clean beauty trends. The region's paints and coatings industry is undergoing transformation toward waterborne and low-solvent formulations, driving demand for specialized rheology modifiers compatible with these advanced formulation systems.

Asia Pacific Rheology Modifiers Market Trends

Asia Pacific dominates the global rheology modifiers market, commanding approximately 42.6% of global market share and a market value of approximately US$ 4.2 billion in 2026, making it the largest regional market. China emerges as the dominant player, driven by its vast manufacturing base, rapid industrialization, and substantial infrastructure investment. The region's market growth is fueled by accelerating urbanization, construction development, and automotive manufacturing expansion, particularly in India, Vietnam, and Southeast Asia. China's investments in high-speed rail, urban development, and industrial manufacturing create substantial demand for paints, coatings, adhesives, and sealants requiring advanced rheology modifier solutions.

India represents a high-growth market opportunity, with rising infrastructure spending, expanding pharmaceutical manufacturing, and burgeoning personal care and cosmetics industry. The country's manufacturing advantages, including cost-competitive labor and emerging chemical manufacturing capabilities, are attracting investment from global rheology modifier manufacturers. Japan leads regional innovation in eco-friendly and high-performance rheology modifiers, with companies introducing bio-based additives addressing regional environmental concerns and stringent quality standards. The region's shift toward waterborne and environmentally compliant formulations is accelerating, driven by regulatory pressures and increasing consumer awareness of sustainability.

Competitive Landscape

The global rheology modifiers market exhibits a moderately consolidated structure, with market leadership concentrated among a small number of multinational chemical corporations. Major players, including BASF SE, Lubrizol Corporation, Evonik Industries AG, Elementis Plc., and Clariant, collectively control nearly 40% of the global market revenue through established product portfolios, extensive distribution networks, and significant research and development capabilities. The competitive landscape is characterized by ongoing consolidation through strategic acquisitions and mergers aimed at expanding product portfolios and geographic reach. Market leaders are investing heavily in sustainability initiatives, including renewable sourcing, green manufacturing processes, and circular economy principles, to strengthen market positioning and meet evolving stakeholder expectations.

Emerging market entrants and regional manufacturers are gaining competitive traction by focusing on niche applications, cost-competitive products, and regional customer relationships. The industry demonstrates increasing emphasis on research and development to develop bio-based alternatives, low-VOC formulations, and multifunctional additives addressing evolving regulatory requirements and consumer preferences. Strategic initiatives, including collaborative partnerships with research institutions, customer co-development programs, and expansion into emerging market segments such as personal care and food applications, are key competitive strategies.

Key Market Developments:

- In August 2025, Clariant unveiled Aristoflex SUN, an advanced rheology modifier specifically engineered for sunscreen formulations, combining superior stability, enhanced SPF performance, and luxurious sensory appeal while maintaining excellent compatibility with organic and inorganic UV filters.

- In April 2024, Lubrizol Corporation introduced Carbopol Fusion S-20 polymer, an inherently biodegradable rheology modifier addressing all 12 Principles of Green Chemistry, offering superior thickening and suspension capabilities with 30% reduction in environmental impact for premium shampoos and skin cleansers.

- In February 2023, Clariant launched Aristoflex Eco T, a next-generation rheology modifier naturally derived from Tara Gum with a renewable carbon index of 71%, combining synthetic polymer performance with biopolymer environmental benefits while delivering excellent thickening and stabilizing properties for skincare formulations.

Companies Covered in Rheology Modifiers Market

- Cabot Corporation

- Orion Engineered Carbons Holdings GmbH

- OMSK Carbon Group

- Phillips Carbon

- Tokai Carbon Co. Ltd.

- Asahi Carbon Co. Ltd.

- Ralson Goodluck Carbon

- Atlas Organic Pvt. Ltd.

- Continental Carbon Co.

- OCI Company Ltd.

- Birla Carbon

- Bridgestone Corp.

- Mitsubishi Chemicals

- China Synthetic Rubber Corporation (CSRC)

- Himadri Companies & Industries Ltd. (HCIL)

Frequently Asked Questions

The global Rheology Modifiers Market was valued at US$ 9.8 billion in 2026 and is projected to reach US$ 13.3 billion by 2033, expanding at a CAGR of 4.5% during the forecast period, driven by increasing demand from paints, coatings, and personal care industries alongside growing emphasis on sustainable formulations.

Accelerating demand from paints and coatings requiring advanced viscosity control and application properties, expansion of the personal care and cosmetics industry driven by rising consumer awareness of product texture and sensory experience, and environmental regulations promoting low-VOC and sustainable formulations

Organic rheology modifiers dominate the market with approximately 64.7% market share, comprising both synthetic and natural variants. Synthetic organic modifiers provide superior performance in industrial applications, while natural variants are experiencing accelerating growth driven by regulatory pressures, consumer demand for sustainability, and development of high-performance bio-based alternatives from renewable sources.

Asia Pacific is the largest regional market, commanding approximately 42.6% of global market share, driven by rapid industrialization in China, infrastructure expansion and manufacturing growth in India, and urbanization trends across Southeast Asia.

Bio-based and natural rheology modifiers present the most significant growth opportunity, driven by stringent environmental regulations, rising consumer demand for clean-beauty and sustainable products, and government incentives promoting renewable feedstocks.

Major market leaders include BASF SE (Germany), Lubrizol Corporation (US), Evonik Industries AG (Germany), Clariant (Switzerland), DuPont (US), Elementis Plc. (UK), The Dow Chemical Company (US), Cargill Incorporated (US), Croda International Plc. (UK), Ashland (US), Akzo Nobel N.V. (Netherlands), BYK Additives and Instruments (Germany), PPG Industries (US), and Arkema (France).