- Hardware & Software IT Services

- Ransomware Protection Market

Ransomware Protection Market Size, Share, and Growth Forecast, 2026 – 2033

Ransomware Protection Market by Component (Solution [Endpoint Protection, Network & Email Protection, Backup & Recovery, Identity & Access Protection, Security Analytics & Threat Intelligence, Others], Services [Professional Services, Managed Services]), Deployment (On-Premises, Cloud / SaaS, Hybrid), Application, Industry, and Regional Analysis for 2026 – 2033

Ransomware Protection Market Size and Trends

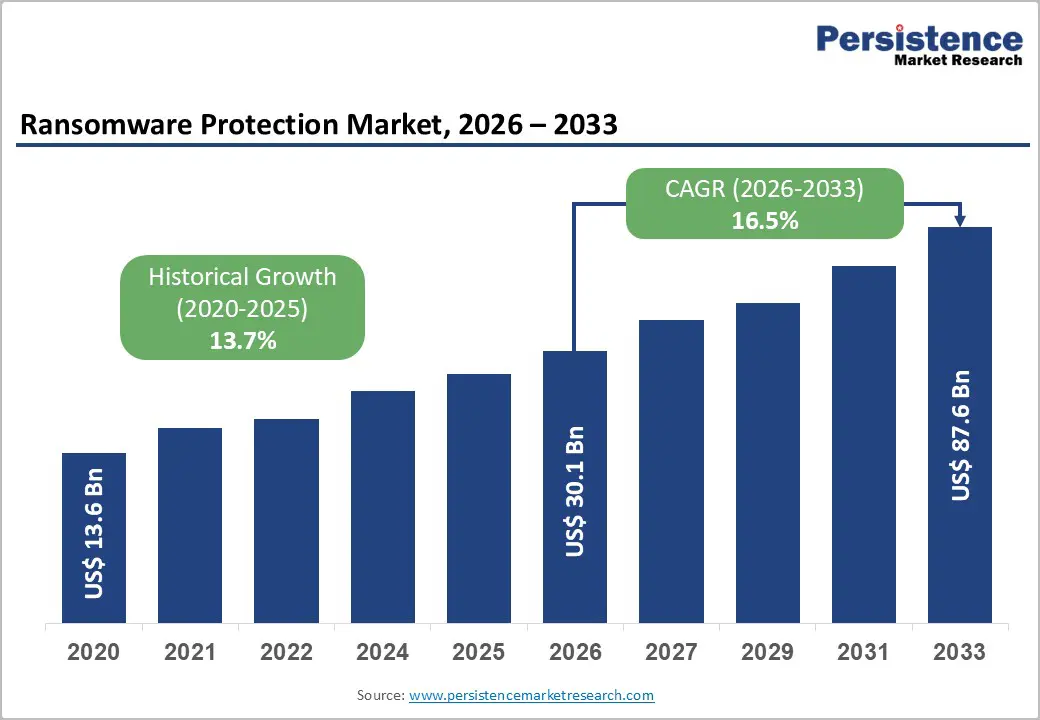

The global Ransomware Protection Market size is projected to rise from US$30.1 Bn in 2026 to US$87.6 Bn by 2033. It is anticipated to witness a CAGR of 16.5% during the forecast period from 2026 to 2033, driven by the escalating frequency and sophistication of ransomware attacks targeting critical infrastructure, combined with stringent regulatory compliance requirements such as the NIS2 Directive and GDPR. Organizations are increasingly recognizing that legacy security infrastructure cannot match the speed of AI-powered attacks, with 76% of organizations struggling to defend against adversary-controlled AI capabilities.

Key Industry Highlights:

- Leading Component: Solutions dominate the segment, capturing more than 67% market share in 2026 and valued at over US$ 20.2 Bn, as organizations urgently need scalable, always-on defense against evolving ransomware attacks. Services are the fastest-growing component, driven by the shortage of in-house cybersecurity expertise and the need for continuous monitoring, incident response, threat hunting, and rapid recovery support.

- Leading Deployment: On-Premises lead with over 38% market share in 2026, valued at more than US$ 11.4 Bn, due to strong preferences for direct control, data residency, compliance requirements, and integration with legacy infrastructure. Cloud/SaaS is the fastest-growing deployment, registering a 21.1% CAGR, supported by rapid deployment, continuous threat intelligence updates, and scalable protection for hybrid and remote environments.

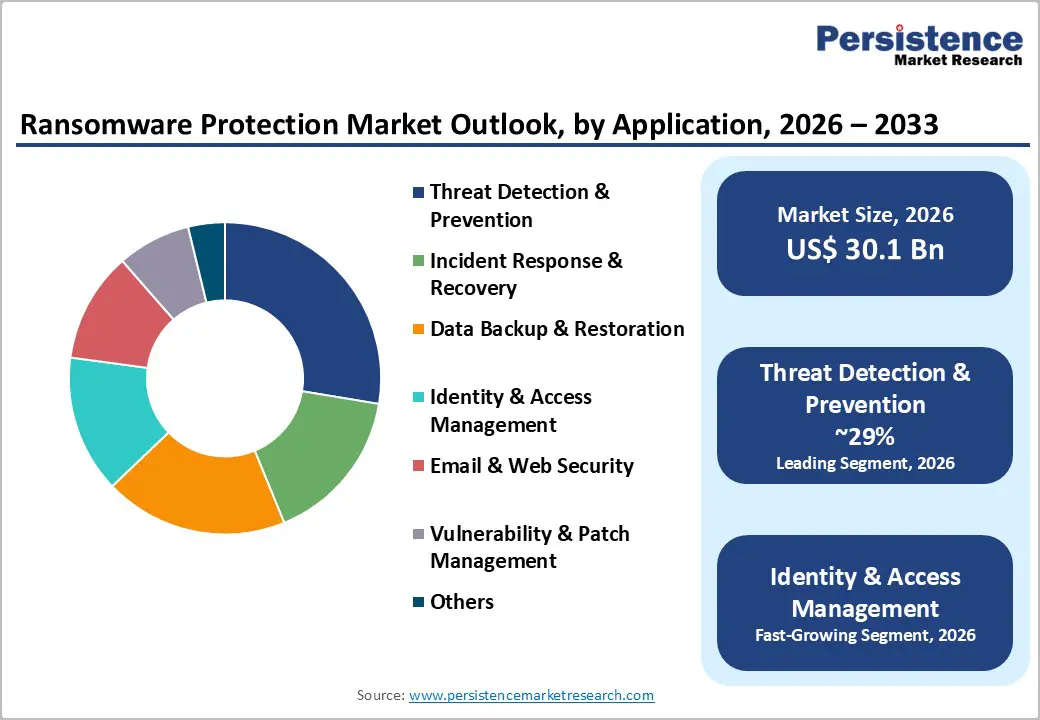

- Leading Application: Threat detection & prevention holds the share over 29% in 2026, valued at more than US$ 8.7 Bn, as organizations prioritize proactive defense to prevent ransomware attacks before encryption and lateral movement. Identity & Access Management (IAM) is the fastest-growing application, driven by increased credential theft, weak access controls, and the need for least-privilege access, adaptive policies, and real-time session monitoring.

- Leading Industry: BFSI holds the largest industry share at over 22% in 2026, valued at more than US$ 6.6 Bn, due to high-value customer data, strict compliance mandates, and the financial impact of operational disruptions. Manufacturing is among the fastest-growing industries, driven by Industry 4.0 adoption, OT/IoT vulnerabilities, legacy equipment, and the high cost of downtime and supply chain disruptions.

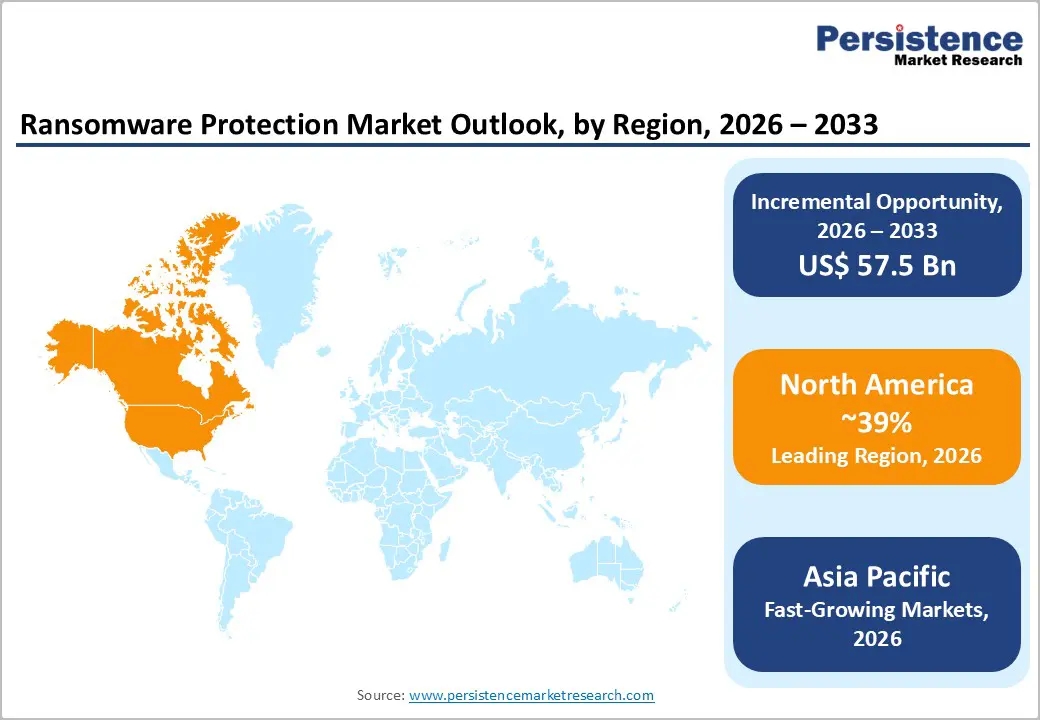

- Leading Region: North America leads the global ransomware protection market with over 39% share in 2026, valued at approximately US$ 11.7 Bn, supported by advanced infrastructure, high threat exposure, and strong regulatory enforcement. Asia Pacific is the fastest-growing region with a 22.3% CAGR, driven by rapid digital transformation, cloud adoption, and rising ransomware activity across large markets such as China and India, along with growing cybersecurity spending in ASEAN nations.

| Key Insights | Details |

|---|---|

| Ransomware Protection Market Size (2026E) | US$ 30.1 Bn |

| Market Value Forecast (2033F) | US$ 87.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 16.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 13.7% |

Market Dynamics

Driver

Rising Frequency and Sophistication of Attacks

Attackers are increasingly using advanced techniques such as double extortion, fileless malware, and AI-powered phishing to bypass traditional defenses, making organizations more vulnerable than ever. As ransomware incidents grow in volume and complexity, businesses are realizing that basic antivirus tools are no longer sufficient. This has led to a surge in the adoption of specialized ransomware protection solutions that provide real-time threat detection, behavior analysis, and rapid incident response. The expansion of remote work, cloud adoption, and IoT devices has widened the attack surface, creating more entry points for ransomware actors. High-profile breaches and significant financial losses have heightened awareness among enterprises, pushing them to invest proactively in stronger security measures.

Regulatory Mandates and Compliance-Driven Investments

The enforcement of the NIS2 Directive, effective October 18, 2024, and expanding GDPR requirements have forced organizations in regulated sectors to reprioritize cybersecurity spending. NIS2 requires mandatory cybersecurity standards, 24-hour incident reporting, tested backup and recovery plans, and supply chain security measures, driving investment in ransomware protection, incident response, and backup solutions. Non-compliance risks hefty penalties, especially for financial institutions, healthcare providers, and critical infrastructure operators, making ransomware protection a business imperative. Board-level accountability and cyber insurance conditions further pressure organizations to adopt certified solutions. Ransomware protection is shifting from discretionary spending to a mandatory operational expense.

Restraint

High Implementation Costs and ROI Uncertainty

High implementation costs and unclear ROI remain major restraints for the ransomware protection market, especially among SMEs. Deploying comprehensive solutions often requires substantial upfront capital for hardware, licenses, and skilled security staff, leading to a high total cost of ownership and difficult financial justification. Many SMEs hesitate to invest due to competing priorities and constrained security budgets, despite being the fastest-growing segment. Integration challenges with legacy systems and fragmented toolsets also cause delays and cost overruns. The value of ransomware protection is hard to quantify since prevented attacks cannot be easily measured, making budget allocation uncertain and limiting adoption in price-sensitive markets.

Evolving Threat Tactics and Defensive Obsolescence

Ransomware threat actors are rapidly evolving their tactics, increasingly shifting from traditional encryption-based attacks to data exfiltration and extortion without encryption, which speeds up attacks and bypasses many legacy detection controls. This creates a continuous arms race where security measures that were effective just months ago quickly become outdated, forcing organizations to constantly upgrade technologies and retrain staff. Companies relying on point solutions for specific attack vectors face significant risk as attackers adopt hybrid strategies that blend social engineering, data theft, and targeted encryption. The need for constant investment and operational effort limit adoption of ransomware protection solutions, especially for organizations with limited cybersecurity maturity or resources.

Opportunity

AI-Powered and Autonomous Threat Detection Solutions

Organizations are increasingly adopting AI and machine learning for superior threat detection through behavioral analytics, anomaly identification, and the ability to detect zero-day threat capabilities that traditional signature-based systems cannot match. Solutions with autonomous response features, such as automated rollback and self-healing infrastructure, are gaining strong traction, especially in industries where uptime is critical, like healthcare and manufacturing. The growing preference for AI-driven protection is driven by the need for faster threat identification, reduced response time, and minimized business disruption. High-value sectors such as BFSI, healthcare, and government are leading adoption due to their elevated risk profiles and larger security budgets, making this segment highly attractive for vendors and investors.

?Cloud-Based Security Solutions and Ransomware Recovery-as-a-Service

Organizations prefer cloud-based solutions for their lower upfront costs, faster deployment, continuous threat intelligence updates, and seamless integration with cloud-native security services. Data backup and recovery services are emerging as a crucial segment, as immutable and isolated backups are increasingly seen as essential for effective ransomware recovery. Ransomware Recovery-as-a-Service (RaaS) offerings, which combine detection, incident response, and data restoration, are gaining traction among organizations that want to outsource preparedness to specialized providers. This shift toward cloud delivery and managed services is also driving new revenue models, with subscription and outcome-based pricing increasing recurring revenue and attracting investment into ransomware-focused vendors.

Category-wise Analysis

Component Analysis

Solution dominates the solution segment, capturing more than 67% market share in 2026 with a value exceeding US$ 20.2 Bn, as organizations urgently need immediate, scalable, and always-on defense against rapidly evolving attacks. Enterprises prioritize integrated security platforms that combine prevention, detection, response, backup, and recovery in a single solution to minimize downtime and data loss. The surge in remote work, cloud workloads, and endpoint sprawl has increased demand for deployable software solutions rather than manpower-intensive services.

Services demonstrate significant growth due to the need for continuous, expert-led support to manage complex cyber threats. Many businesses lack in-house security talent, so they rely on managed services for real-time monitoring, incident response, and rapid recovery. The rise in hybrid work and cloud environments also creates more attack surfaces, driving demand for ongoing vulnerability assessments, threat hunting, and patch management. Ransomware incidents require fast, coordinated response and forensic analysis, which service providers are best equipped to deliver.

Deployment Analysis

On-Premises dominate the market, capturing over 38% market share in 2026 with a value exceeding US$ 11.4 Bn, due to many organizations still prioritizing direct control over their security environment, especially for sensitive systems and critical infrastructure. They prefer on-premises deployment to avoid reliance on external networks and third-party cloud providers, reducing exposure to internet-based attacks. These solutions also support compliance requirements and internal audit controls that demand strict data residency and access management. On-premises systems are optimized for performance in high-throughput environments and integrated tightly with legacy infrastructure, which is common in large enterprises.

Cloud / SaaS demonstrates the highest growth with a CAGR of 21.1% due to organizations' need for rapid deployment and continuous updates to defend against constantly evolving threats. SaaS solutions provide real-time threat intelligence and automated patching, reducing the burden on internal IT teams. They also support remote and hybrid workforces by securing endpoints and data across distributed environments. Cloud models offer scalable protection and predictable subscription costs, making advanced ransomware defenses accessible even for smaller businesses.

Application Analysis

Threat detection & prevention holds over 29% of the market share in 2026, with a value exceeding US$ 8.7 Bn, as organizations are increasingly prioritizing proactive security to stop attacks before they encrypt systems. With ransomware evolving rapidly, companies need real-time monitoring, behavior-based detection, and automated response to reduce dwell time and prevent lateral movement. This capability also helps maintain business continuity by minimizing downtime and avoiding costly recovery efforts. The growing regulatory pressure and reputational risk make prevention-focused tools a critical first line of defense.

Identity & access management are expected to grow at the highest rate due to attackers increasingly exploit stolen credentials and weak access controls to infiltrate networks. IAM helps enforce strong authentication, least-privilege access, and real-time session monitoring, which directly prevents unauthorized lateral movement after initial breach. Organizations need centralized control over user identities across multiple platforms to reduce exposure. IAM supports rapid detection and containment through access revocation and adaptive policies, making it a critical first line of defense against ransomware.

Industry Analysis

BFSI commands the largest market share at over 22% in 2026, with a value exceeding US$ 6.6 Bn, as financial institutions are prime targets due to the high value of customer data, transaction records, and the direct monetary impact of disruptions. They face constant, sophisticated ransomware campaigns that quickly shut down operations and damage trust. Strict regulatory and compliance requirements force banks and insurers to invest heavily in advanced protection and incident response. The rapid shift to digital banking and cloud-based services increases the attack surface, driving continuous demand for stronger ransomware defenses.

Manufacturing is expected to grow at a significant rate due to modern factories relying heavily on interconnected OT systems, making them prime targets for disruptive attacks that halt production and cause huge financial losses. The increasing adoption of Industry 4.0, IoT sensors, and automated control systems expands the attack surface, creating urgent demand for specialized ransomware defenses. Manufacturing plants often run legacy equipment with limited security, forcing companies to invest in advanced protection and rapid recovery solutions. The high cost of downtime and supply chain disruptions drives manufacturers to prioritize proactive ransomware protection to maintain continuous operations.

Regional Insights

North America Ransomware Protection Market Trends

North America accounts for over 39% of the Ransomware Protection market share in 2026, reaching approximately US$ 11.7 Bn, due to its large base of high-value digital targets and highly developed infrastructure, which attract sophisticated threat actors. The region’s dominant position is reinforced by strong regulatory pressure, with federal initiatives pushing organizations toward mandatory incident reporting and zero-trust adoption, driving increased compliance spending. The U.S. remains the primary focus for attackers, while Canada is seeing rising ransomware activity as threat actors expand into secondary markets with perceived weaker defenses. This evolving threat landscape is prompting organizations to accelerate investment in advanced ransomware protection solutions to reduce risk and demonstrate strong security practices.

Asia Pacific Ransomware Protection Market Trends

Asia Pacific is expected to grow at the highest rate with a CAGR of 22.3%, due to rapid digital transformation, growing cloud adoption, and rising cyber threat awareness. China and India offer huge addressable markets with large enterprise populations undergoing accelerated digitalization, while Japan represents a mature market for premium ransomware protection due to advanced cybersecurity infrastructure and strong regulatory requirements. The region’s manufacturing sector, especially in China, Japan, South Korea, and Vietnam, is a prime target for ransomware, driving investments in security across supply chains. ASEAN nations such as Singapore, Malaysia, and Thailand are expanding digital infrastructure and e-commerce, increasing attack surfaces and pushing cybersecurity spending from early stages to rapid growth.

Europe Ransomware Protection Market Trends

Europe is expected to hold more than 24% share by 2026, driven by rising incidents and stricter regulatory requirements that force organizations to strengthen their defenses. The NIS2 Directive and GDPR create mandatory security obligations and penalties, pushing essential service providers and digital infrastructure operators to invest heavily in ransomware protection. Germany, France, and the UK remain major markets, with mature security ecosystems and strong compliance demands. Regulatory harmonization across the EU simplifies security procurement for multinational firms, creating predictable buying patterns. European vendors such as Sophos remain competitive by offering localized compliance expertise and a deep understanding of the regional regulatory landscape.

Competitive Landscape

The ransomware protection market is moderately fragmented, with a mix of global cybersecurity giants and agile niche vendors competing for share rather than a highly consolidated few dominating the space. Companies focusing on continuous product innovation, especially integrating AI and machine-learning for proactive detection and automated response, and platform expansion to offer unified prevention, detection, response, and recovery capabilities that resonate with enterprise buyers. Many also pursue strategic partnerships and acquisitions to quickly broaden technology portfolios or penetrate new regions, while tailoring offerings to meet diverse customer needs.

Key Industry Developments

- In July 2025, Palo Alto Networks announced a definitive agreement to acquire identity and access management specialist CyberArk, strengthening Zero Trust capabilities and addressing AI agent machine identity security risks.

- In June 2025, Microsoft and CrowdStrike jointly announced a collaborative threat actor taxonomy standardization initiative, with Palo Alto Networks and Google/Mandiant joining to streamline ransomware group identification and intelligence sharing, representing industry maturation toward standardized threat intelligence frameworks.

Companies Covered in Ransomware Protection Market

- Microsoft Corporation

- Sophos Ltd.

- Trend Micro Incorporated

- Symantec Corporation

- Kaspersky Lab

- Malwarebytes Corp

- McAfee Inc.

- Avast Software s.r.o

- Cisco System Inc.

- Palo Alto Networks Inc.

- Zemana Ltd.

- Webroot Inc.

- Barracuda Networks Inc.

- Alien Vault Inc.

- Check Point Software Technologies Ltd.

- Bitdefender S.R.L.

- Others.

Frequently Asked Questions

The global market is projected to be valued at US$30.1 Bn in 2026.

The rapid rise in sophisticated ransomware attacks targeting critical infrastructure and enterprises, causing severe operational disruption and financial losses, is a key driver of the market.

The market is expected to witness a CAGR of 16.5% from 2026 to 2033.

Growing adoption of AI-driven threat detection and cloud-based ransomware protection as organizations seek scalable, real-time defenses across hybrid and remote IT environments is creating strong market expansion potential.

Broadcom Inc. , McAfee, LLC, Bitdefender SRL, FireEye, Inc., Malwarebytes Inc., SentinelOne, Inc., Sophos Ltd. are among the leading key players.