- Pharmaceuticals

- Radioembolization Therapy Market

Radioembolization Therapy Market Size, Share, and Growth Forecast 2026 – 2033

Radioembolization Therapy Market by Product Type (Yttrium-90 Microspheres, Others), Procedure Type (Selective Internal Radiation Therapy, Others), Technology, Application, and Regional Analysis 2026 – 2033

Radioembolization Therapy Market Size and Trends Analysis

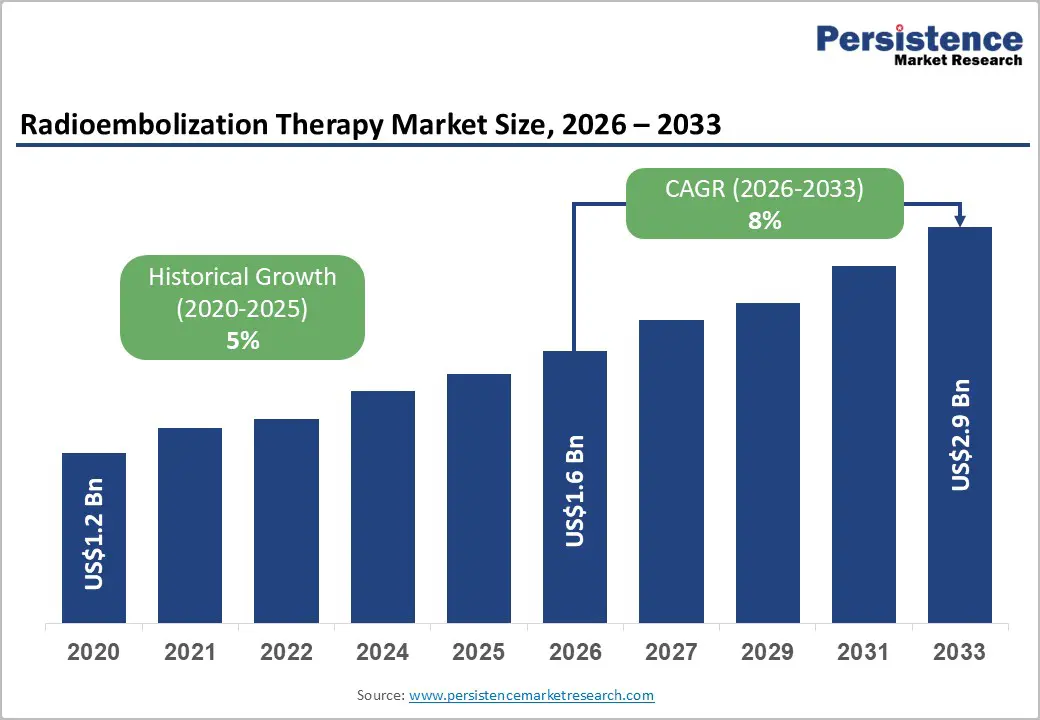

The global radioembolization therapy market size is likely to be valued at US$1.6 billion in 2026 and is expected to reach US$2.9 billion by 2033, growing at a CAGR of 8% during the forecast period from 2026 to 2033, driven by the clinical validation of combination therapies where radioembolization is paired with immunotherapy and the introduction of personalized dosimetry software that enhances treatment precision.

The market’s acceleration reflects a significant shift in interventional oncology, particularly due to the expansion of indications for Hepato-Cellular Carcinoma (HCC) and Metastatic Colorectal Cancer (mCRC). Advancements in microsphere delivery and imaging technologies are enhancing treatment accuracy and outcomes, while favorable reimbursement policies in key regions are further promoting adoption.

Key Industry Highlights:

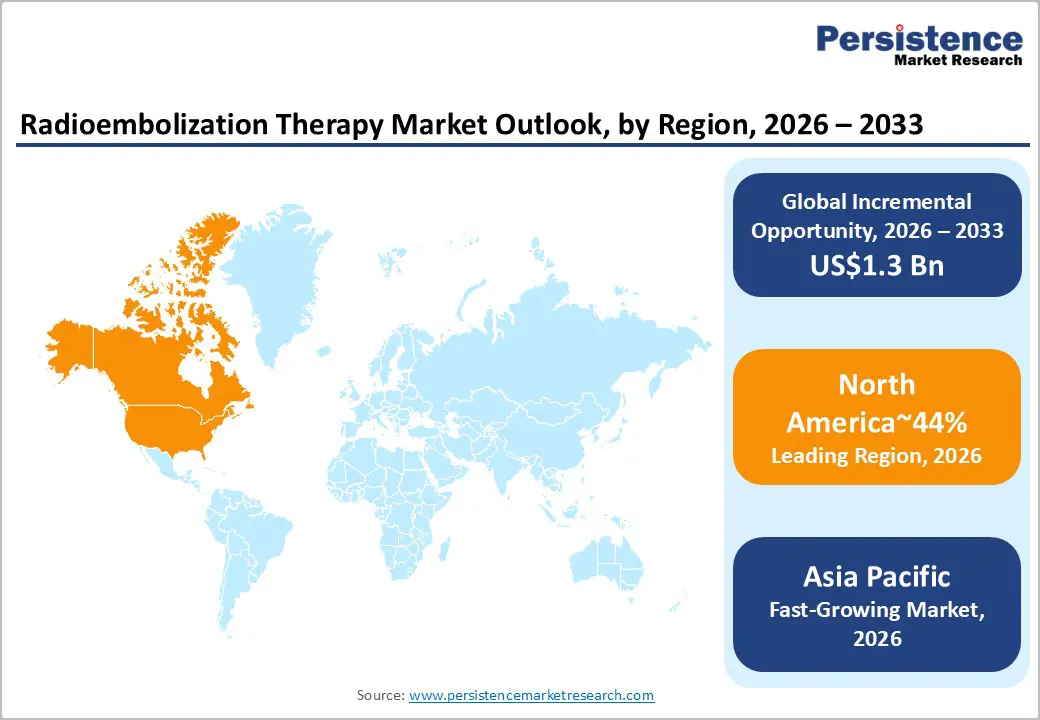

- Leading Region: North America is expected to lead with approximately 44% share in 2026, anchored by a high burden of hepatocellular carcinoma and colorectal liver metastases.

- Fastest-growing Region: Asia Pacific is expected to emerge as the fastest-growing region, driven by high liver cancer prevalence, infrastructure expansion in China, India, and Southeast Asia, and tiered pricing strategies enabling broader access.

- Leading Product Type: The Yttrium-90 (Y-90) microspheres segment is projected to dominate the market with 92% share in 2026, reinforced by established clinical use, FDA approvals, global distribution networks, and broad adoption across tertiary oncology centers.

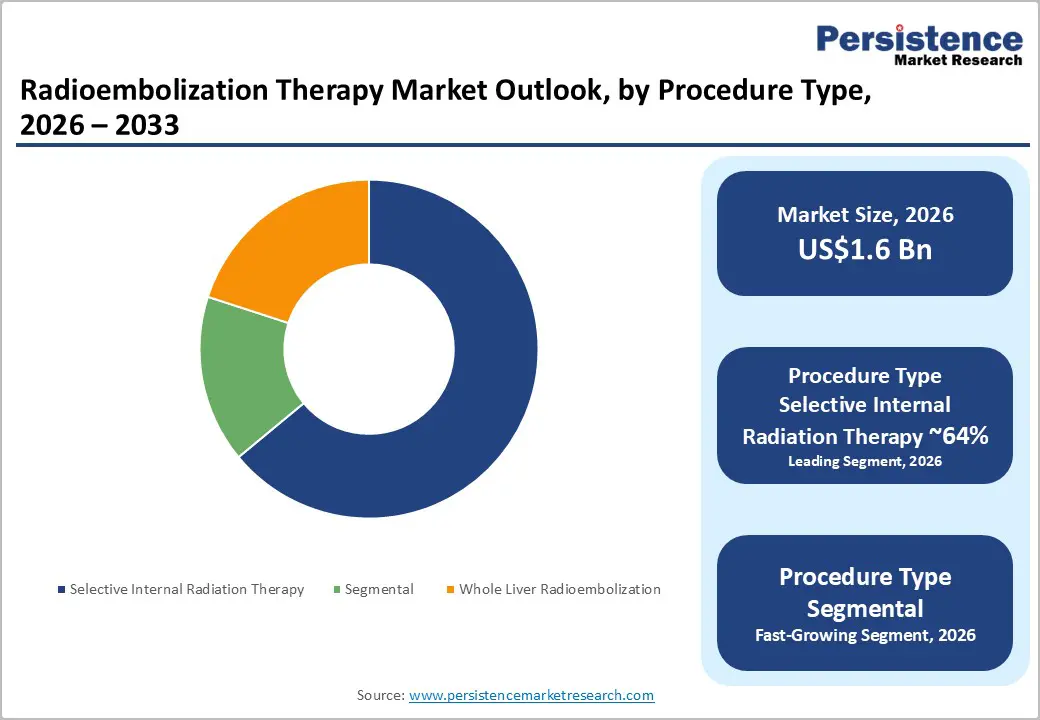

- Leading Procedure Type: Selective Internal Radiation Therapy (SIRT) is expected to maintain its leadership, comprising around 64% of procedural volume in 2026, as the established standard for transarterial radioembolization in hepatocellular carcinoma and metastatic liver disease.

- Industrial Development: In June 2025, Penumbra, Inc. launched the Ruby XL System for detachable embolization coils in the US, enhancing large-volume embolization with reduced radiation exposure and improved outcomes for oncology procedures such as radioembolization.

| Key Insights | Details |

|---|---|

|

Radioembolization Therapy Market Size (2026E) |

US$1.6 Bn |

|

Market Value Forecast (2033F) |

US$2.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Global Incidence of Hepatocellular Carcinoma (HCC)

The radioembolization market is primarily driven by the increasing global incidence of hepatocellular carcinoma (HCC), reflecting demographic changes and the growing disease burden. The World Health Organization (WHO) and the International Agency for Research on Cancer (IARC) report liver cancer as a leading cause of cancer-related deaths, with new cases surpassing 900,000 annually. Rising HCC prevalence in Asia, Africa, and sustained rates in North America have expanded the patient pool for minimally invasive treatments.

Transarterial radioembolization (TARE) using Yttrium-90 microspheres has evolved from a palliative procedure to a standard-of-care intervention for intermediate-stage HCC (BCLC Stage B), further endorsed by guidelines from the National Comprehensive Cancer Network (NCCN). This evolution fuels procedural growth, particularly for tumor downstaging before resection or liver transplantation.

Technological advancements in microsphere delivery, imaging guidance, catheter-based navigation, dosimetry planning, and real-time imaging have significantly enhanced the precision, safety, and outcomes of TARE, fostering broader adoption across tertiary oncology centers. These innovations also minimize complications, improve reimbursement alignment, and contribute to procedural consistency. Geographically, North America remains a leader due to advanced interventional oncology networks, while regions, including Asia Pacific and Africa, are poised for rapid market expansion as diagnostic capabilities and therapeutic access improve.

In July 2025, Sirtex Medical’s FDA approval for SIR-Spheres Y-90 resin microspheres for unresectable HCC marked a milestone, extending the treatment’s applicability to metastatic colorectal cancer, thus broadening its potential market and adoption as a targeted, minimally invasive alternative.

Operational Complexity and Supply Chain Fragility

The radioembolization market is materially constrained by the inherent operational complexity of the therapy, which requires coordinated engagement across interventional radiology, nuclear medicine, and medical physics disciplines. The procedural workflow is highly specialized, encompassing patient mapping, catheter-based delivery planning, and post-procedural dosimetry verification, all of which demand trained personnel and sophisticated infrastructure. This complexity elevates barriers to entry for smaller hospitals and regional clinics, effectively concentrating procedural volumes within tertiary and academic oncology centres equipped to manage the multi-step intervention safely.

Compounding these operational challenges, the supply chain for Yttrium-90 microspheres remains fragile due to the isotope’s short half-life and dependence on nuclear reactor output. "Just-in-time" logistics are essential to maintain clinical efficacy, with any disruption in production, transportation, or regulatory clearance leading to procedure delays or cancellations. Historical shortages between 2022 and 2024 illustrate the vulnerability of the supply network.

Collectively, these factors impose structural limitations on broader market penetration, moderating adoption rates despite robust clinical demand and guideline recognition. Multiple research reactors producing key medical isotopes faced simultaneous outages and planned shutdowns in late 2022, which led to significant global shortages of reactor-based isotopes.

AI-enabled Dosimetry and Precision Treatment Optimization

The integration of artificial intelligence into dosimetry planning constitutes a strategic growth driver for the radioembolization market by directly enhancing procedural accuracy and patient outcomes. AI algorithms analyze pre-procedural imaging to predict microsphere distribution with higher fidelity than conventional manual methods, reducing off-target radiation and safeguarding healthy hepatic tissue. By enabling personalized dosing that accounts for tumor vascularity and liver function variability, AI addresses the critical need for tailored interventions in heterogeneous patient populations, positioning radioembolization within precision oncology frameworks. This capability not only improves therapeutic efficacy but also mitigates post-procedural complications, thereby reinforcing clinical confidence and adoption rates across specialized centers.

North America currently spearheads this technological convergence, leveraging its robust network of academic hospitals, medical technology firms, and research consortia to accelerate AI-driven dosimetry deployment. The integration of predictive analytics into real-time workflow optimization simplifies complex procedural planning for interventional radiologists, shortens procedure duration, and enhances post-treatment monitoring.

Coupled with advanced imaging modalities, this convergence amplifies the potential for radioembolization to transition from a high-skill, center-specific therapy to a scalable, data-informed intervention with improved reproducibility and patient-centric outcomes. In October 2025, the Journal of Neurointerventional Surgery published a review on expanding applications of Y-90 radioembolization in endovascular neurosurgery. The review synthesizes rationale and potential for intra-arterial Y-90 in brain tumors, highlighting translational opportunities beyond liver cancer and sparking interest in new indications.

Category–wise Analysis

Product Type

Yttrium-90 (Y-90) microspheres are expected to dominate the product landscape with an estimated 92% market share in 2026, maintaining their leadership due to established clinical use in liver embolization procedures, FDA approvals, and widespread adoption by key providers such as Sirtex. Y-90 microspheres come in glass and resin variants, with glass microspheres preferred for curative-intent “radiation segmentectomy” due to their higher specific activity and reduced embolic effect. Resin microspheres, on the other hand, continue to offer broader coverage for managing multifocal disease, providing flexibility in treatment planning.

The segment’s dominance is supported by a robust global distribution network, physician familiarity, and consistent clinical outcomes that drive demand across oncology centers. As new competitors enter the market, Y-90 is expected to maintain its substantial market share due to its entrenched clinical role and long history of reliable supply.

Holmium-166 (Ho-166) microspheres are anticipated to be the fastest-growing segment, driven by their superior imaging compatibility via SPECT-based dosimetry, which addresses the verification limitations of Y-90 and enhances treatment planning precision. This segment is expected to gain traction in clinical trials and among early-adopter centers, thanks to its lower toxicity and improved workflow efficiency. Other radioactive microspheres, such as Rhenium-188 and radiopaque beads, currently account for about 2% of the market. These are expected to cater to cost-sensitive applications and specialized treatments, with their imageable properties improving procedural safety. Though their market volume remains small, innovation in niche isotopes is likely to support steady adoption in hospitals seeking targeted therapies and optimized workflows.

Procedure Type

Selective Internal Radiation Therapy (SIRT) is expected to remain the leading procedure type, accounting for approximately 64% of total procedural volume. Its leadership reflects its position as the established clinical standard for transarterial radioembolization, particularly in hepatocellular carcinoma and metastatic liver disease requiring lobar or multi-segment treatment. SIRT enables controlled, targeted delivery of radioactive microspheres via the hepatic artery, balancing tumor dose coverage with preservation of healthy parenchyma.

The procedure is widely embedded in interventional oncology workflows, supported by extensive physician familiarity, standardized protocols, and broad payer acceptance across key markets. Its adaptability across palliative and disease-control settings, including colorectal liver metastases, is expected to sustain high utilization. As treatment algorithms continue to favor minimally invasive options over systemic therapies alone, SIRT is forecast to anchor procedural volumes in routine clinical practice.

Segmental Radioembolization (Radiation Segmentectomy) is anticipated to be the fastest-growing segment, driven by its shift from palliative lobar therapy to curative-intent treatment for small unresectable tumors ≤3 cm. By delivering ablative doses (>190 Gy) to targeted liver segments, segmental therapy achieves outcomes comparable to surgery or thermal ablation while minimizing collateral tissue damage. Growth is reinforced by rising HCC incidence, preference for minimally invasive outpatient procedures, integration with immune checkpoint inhibitors, and adoption of Holmium-166 for MRI-visible treatment planning.

Key players, including Boston Scientific, Sirtex Medical, and Terumo, are expanding segmental offerings with AI-guided dosimetry and 3D modeling solutions. North America leads in revenue share due to early adoption and advanced clinical infrastructure, while Asia Pacific is the fastest-growing region, benefiting from high liver cancer prevalence in China and India and expanding interventional oncology capacity.

Regional Insights

North America Radioembolization Therapy Market

North America is expected to lead the radioembolization therapy market, accounting for approximately 44% share, supported by a high and rising burden of liver-related malignancies and strong clinical adoption. The U.S. anchors regional demand through an elevated incidence of hepatocellular carcinoma and a large pool of patients with colorectal cancer–related liver metastases. These disease dynamics sustain procedural volumes and reinforce the role of radioembolization as a core locoregional therapy.

The region benefits from a mature interventional oncology ecosystem, with widespread availability of advanced interventional radiology infrastructure and a highly trained specialist workforce capable of delivering complex Y-90 and Holmium-166 procedures.

The region is likely to maintain leadership as favorable reimbursement structures continue to support access to high-cost radiopharmaceutical therapies. Medicare payment policies and pass-through mechanisms enable predictable coverage, while the expansion of ambulatory surgery centers broadens procedural access beyond tertiary hospitals. North America also benefits from early adoption of AI-enabled dosimetry and procedural planning, improving precision and outcomes. Concentrated R&D activity and proximity to innovation hubs further reinforce the region’s leading position through continuous technological advancement and clinical integration.

Europe Radioembolization Therapy Market

Europe is expected to represent a mature and structurally stable region that trails North America in overall share. The region’s adoption is moderated by fragmented reimbursement frameworks, with countries, including Germany and France, providing defined pathways while others restrict access to TARE/SIRT as a last-line or budget-constrained therapy. Regulatory bottlenecks under the EU Medical Device Regulation (MDR) further limit the rapid introduction of next-generation devices, prioritizing maintenance of existing products over novel technology deployment.

Despite moderate growth, the Europe market is shifting toward precision and personalized care. AI-driven voxel-based dosimetry is increasingly implemented to optimize tumor targeting and spare healthy tissue. Centers are expanding the use of Alpha-emitting radionuclides, and TARE indications now include bridging to transplant or downstaging previously ineligible patients. Theranostic approaches pairing PET diagnostics with therapeutic microspheres are gaining traction, while EU sustainability initiatives promote biodegradable microspheres and eco-conscious isotope production. These developments reinforce Europe’s mature, innovation-focused profile, supporting incremental adoption rather than rapid market acceleration.

Asia Pacific Radioembolization Therapy Market

Asia Pacific is expected to emerge as the fastest-growing region, driven by a high disease burden and rapid infrastructure expansion. China anchors regional demand, representing nearly half of the world’s liver cancer cases, primarily Hepatitis B–related, while Japan maintains leadership in high-precision medical technologies. India and ASEAN nations are rapidly scaling access, with tiered pricing strategies supporting adoption in cost-sensitive markets. Urban centers in China and Japan provide world-class interventional oncology capabilities, but rural penetration remains limited, keeping overall regional market value below that of North America. These structural and epidemiological dynamics support rapid growth despite constraints in trained interventional oncologists and nuclear medicine facilities.

The region is likely to sustain accelerated expansion as governments continue greenfield hospital and radiotherapy center development, particularly in China, India, and Southeast Asia. Localized innovation, including cost-efficient microspheres and delivery systems, addresses price sensitivity while enabling broader patient access. Radioembolization increasingly serves as a bridge-to-transplant therapy in areas with limited deceased donor availability. Regulatory harmonization and cross-border approvals further facilitate market scaling. These factors collectively reinforce Asia Pacific’s position as the fastest growing market, combining high patient volume with emerging clinical and infrastructural capabilities.

Competitive Landscape

The global radioembolization therapy market is highly consolidated, with Boston Scientific Corporation and Sirtex Medical Limited together controlling over 85% of the total market share. Market dominance is reinforced by their leadership in Y-90 microsphere technology, extensive clinical validation, and strong reimbursement positioning across key regions. Emerging competitors and regional distributors account for the remaining share, primarily focusing on niche innovations such as radiopaque beads, advanced delivery systems, and localized market penetration strategies. Competitive dynamics are increasingly defined by product differentiation through bead composition, delivery precision, and integrated dosimetry software capabilities.

Market concentration metrics, including a Herfindahl-Hirschman Index indicating moderate concentration, reflect the limited number of major players and high barriers to entry. Strategic positioning emphasizes continuous clinical innovation, regulatory approvals, and payer alignment, while fragmented players attempt to gain traction through specialized regional solutions and incremental technological advancements. Overall, the market structure favors established players capable of sustaining R&D investments and navigating complex reimbursement environments.

Key Industry Developments:

- In January 2026, Plus Therapeutics, Inc. announced a business update highlighting advancements in its Alginate Microsphere Radioembolization Program for liver and solid tumors. This preclinical program explored alginate microspheres for intra-arterial delivery, aiming to enhance targeted radiation while minimizing systemic exposure, positioning it as a next-generation innovation in radioembolization.

- In December 2025, the Radiopharmaceuticals Market saw increased demand for Y-90 in therapeutic oncology applications. Driven by targeted therapies such as radioembolization, this growth expanded access in the Asia Pacific region and supported the integration of precision medicine, with Lutetium-177 and Y-90 leading the innovations.

- In September 2025, Sirtex Medical secured expanded CE Mark approval for SIR-Spheres Y-90 resin microspheres to treat additional liver cancer indications. The expanded indication included unresectable intrahepatic cholangiocarcinoma and other liver metastases, broadening European market access and supporting the global standardization of radioembolization protocols for diverse tumor types.

Companies Covered in Radioembolization Therapy Market

- Sirtex Medical

- Boston Scientific Corporation

- Terumo Corporation

- Merit Medical Systems, Inc.

- ABK Biomedical Inc.

- TriSalus Life Sciences

- Guerbet

- Nordion Inc.

- Varian Medical Systems

- China Grand Pharmaceutical and Healthcare Holdings

- Eckert & Ziegler BEBIG

- Cook Medical Inc.

- Becton Dickinson & Company

- Siemens Healthineers

- Fluidx Medical Technology

- IsoRay Medical, Inc.

Frequently Asked Questions

The global radioembolization therapy market is projected to be valued at US$1.6 billion in 2026 and is expected to reach US$2.9 billion by 2033, driven by expanding clinical indications and the integration of advanced dosimetry.

Growth is primarily driven by the rising incidence of hepatocellular carcinoma (HCC), the clinical validation of combination therapies with immunotherapy, the introduction of personalized AI-enabled dosimetry software, and favorable reimbursement policies in key regions.

The radioembolization therapy market is forecast to grow at a CAGR of 8.0% from 2026 to 2033, reflecting its pivotal role in modern interventional oncology.

Asia Pacific is the fastest-growing regional market, fueled by a high burden of liver cancer, rapid healthcare infrastructure expansion in China and India, and tiered pricing strategies that improve patient access.

The radioembolization therapy market is highly consolidated, with Boston Scientific Corporation and Sirtex Medical Limited holding over 85% of the market share, alongside key players such as Terumo Corporation, Merit Medical Systems, and Guerbet.