- Specialty & Fine Chemicals

- Pyruvic Acid Market

Pyruvic Acid Market Size, Trends, Share, and Growth Forecast, 2026 – 2033

Pyruvic Acid Market by Product Type (Food Grade, Pharmaceutical Grade, Industrial Grade), Application (Food & Beverages, Pharmaceuticals, Cosmetics, Chemicals, Others), End-User (Food Industry, Pharmaceutical Industry, Cosmetic Industry, Chemical Industry, Others), and Regional Analysis for 2026-2033

Pyruvic Acid Market Share and Trends Analysis

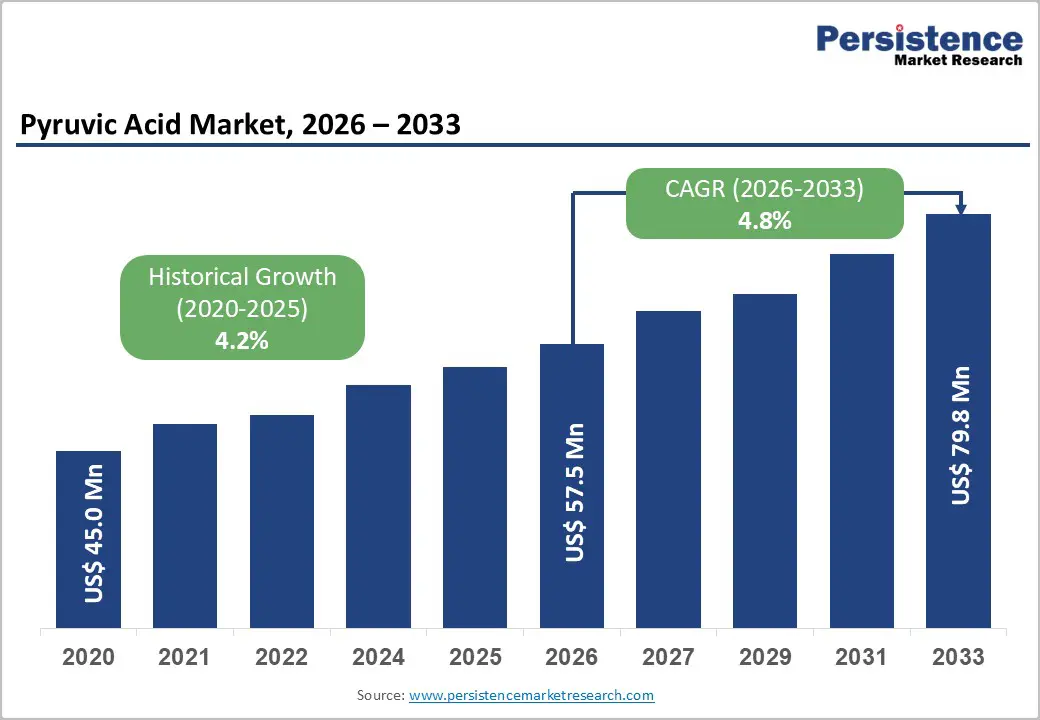

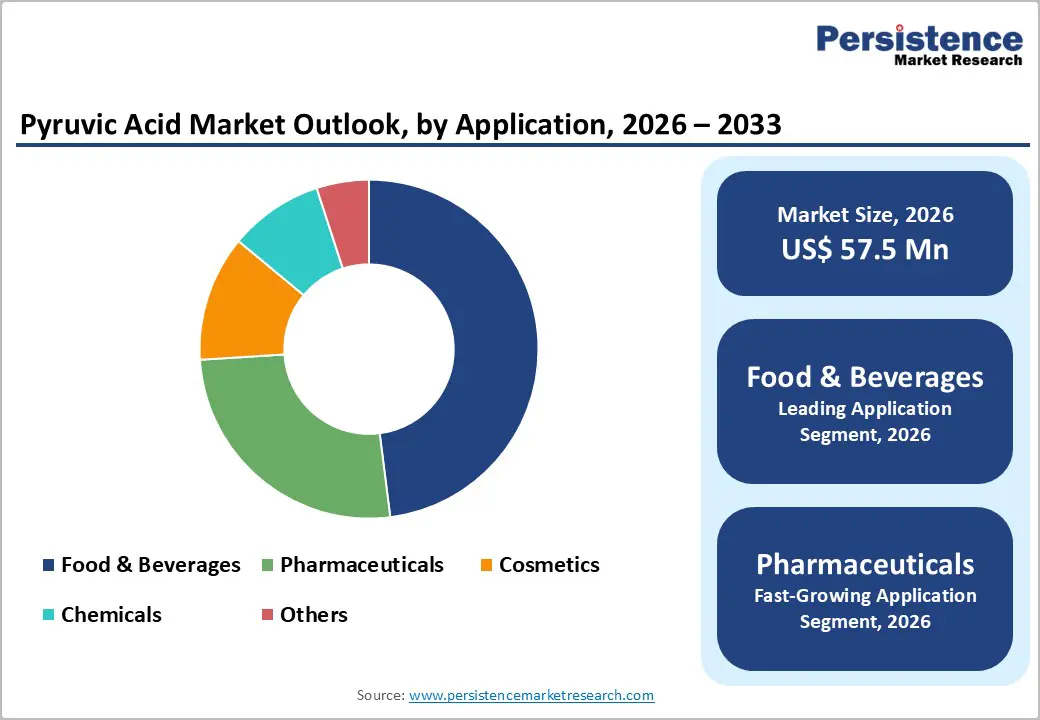

The global pyruvic acid market size is likely to be valued at US$ 57.5 million in 2026, and is projected to reach US$ 79.8 million by 2033, growing at a CAGR of 4.8% during the forecast period 2026−2033.

This expansion is being driven by increased adoption in food processing, pharmaceutical formulations, cosmetics manufacturing, and specialty chemical synthesis, where pyruvic acid acts as a biochemical intermediate and acidity regulator. The market has benefited from steady demand for processed foods, heightened pharmaceutical research, and the rising popularity of organic acids in cosmetic products, all of which have contributed to a stable growth trajectory.

Regulatory authorities have consistently recognized pyruvic acid as a safe ingredient for use in both food and pharmaceutical products, thereby strengthening market stability and encouraging broader application. Ongoing advances in fermentation-based production technologies have improved yield efficiency and enhanced product purity, making pyruvic acid more cost-competitive for manufacturers. Emerging economies are also supporting incremental growth by expanding their manufacturing capabilities and increasing downstream industrial activity, brightening the market outlook through 2033.

Key Industry Highlights

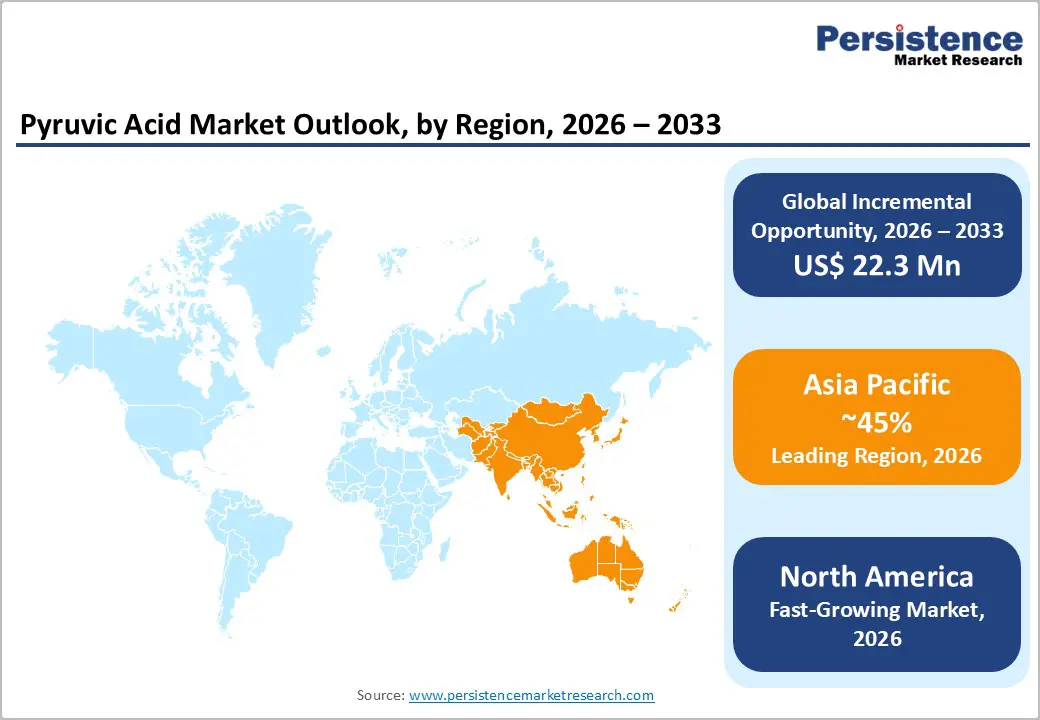

- Dominant Region: Asia Pacific is predicted to hold a 45% market share in 2026, driven by the abundant availability of renewable feedstock sources.

- Fastest-growing Market: North America is forecast to be the fastest-growing market from 2026 to 2033, driven by expanding pharmaceutical and specialty chemical applications.

- Leading Application: Food & beverages are likely to lead with about 48% revenue share in 2026 due to widespread use of pyruvic acid in bakery, beverages, and functional nutrition products.

- Fastest-growing Application: Pharmaceutical applications are projected to grow the fastest through 2033, driven by rising investment in drug development and high-purity intermediates.

| Key Insights | Details |

|---|---|

| Pyruvic Acid Market Size (2026E) | US$ 57.5 Mn |

| Market Value Forecast (2033F) | US$ 79.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Applications in Pharmaceuticals and Health Supplements

The pharmaceutical and health supplement sectors have experienced steady growth in pyruvic acid adoption due to its established role in cellular energy metabolism. Pyruvic acid serves as a key biochemical intermediate in glycolysis and the citric acid cycle, supporting therapies for metabolic disorders, recovery protocols, and endurance enhancement. Pharmaceutical companies leverage its compatibility with existing synthesis and formulation processes, enabling efficient integration into drug development pipelines.

This functional alignment with metabolic efficiency and clinical relevance has elevated pyruvic acid’s profile among manufacturers seeking reliable and scientifically validated ingredients. The momentum in these sectors is further strengthened by a strategic shift toward evidence-based product development. Pharmaceutical and nutraceutical firms increasingly favor ingredients with clear metabolic pathways and documented clinical utility, as these attributes facilitate regulatory approval and enable transparent consumer claims.

Pyruvic acid’s well-documented role in fundamental metabolic cycles reduces formulation uncertainty and accelerates product development cycles. Continuous investment in high-purity manufacturing and quality assurance standards ensures a consistent supply, supporting broader adoption in regulated healthcare and wellness markets. This combination of scientific credibility and operational efficiency positions pyruvic acid as a preferred ingredient for future growth in these segments.

Technical Challenges and Raw Material Volatility

Technical constraints have limited pyruvic acid economics because manufacturers have managed multi-step synthesis and tight operating windows simultaneously. Commercial output has relied on chemical oxidation routes and fermentation pathways, and both have required consistent, high-purity inputs and disciplined control of temperature, residence time, and catalyst behavior. Operators have seen that small parameter drift has created more off-spec material, lowered yields, and increased purification load, thereby pushing unit costs upward.

Teams are also facing scale-up friction because reaction kinetics and microbial robustness have not behaved uniformly as volumes have increased, while corrosion exposure, solvent recovery losses, and energy-intensive distillation continue to compress margins. Input volatility has compounded these hurdles because procurement has remained exposed to agricultural cycles and petrochemical pricing. Producers have sourced key precursors from feedstock such as tartaric acid and carbohydrate-based substrates, so supply shocks and seasonal variability have weakened cost predictability and planning discipline.

This instability has disrupted longer-term supply agreements and forced downstream pricing conversations to remain reactive, diluting competitiveness in contract bids. To gain firmer ground in the market, suppliers can benefit from dual-sourcing feedstock, qualifying alternates early, and tightening specifications to reduce sensitivity to swings in any single input stream.

Sustainable Bio-Synthesis Expansion

Bio-based production pathways have emerged as the primary strategic opportunity because chemical manufacturers have responded to decarbonization mandates and stricter procurement criteria across global value chains. Fermentation-driven synthesis has delivered measurable reductions in lifecycle emissions and decreased reliance on petrochemical feedstocks, while agricultural residues and renewable sugars have provided flexible input options that insulate producers from fossil-fuel price swings.

Regulatory frameworks governing carbon intensity and traceability have accelerated this transition, and organizations that have invested early in microbial strain engineering and biocatalysis have secured first-mover advantages in quality consistency and cost competitiveness. This shift is reinforcing supply chain resilience because bio-routes have supported diversified sourcing and have reduced exposure to single-commodity volatility. Commercial differentiation through bio-synthesis has extended beyond compliance into premium positioning and investor appeal.

Companies that have integrated circular economy principles, such as waste valorization and resource recovery, are attracting capital from environmental, social, & governance (ESG)-focused portfolios and are commanding higher pricing in pharmaceutical and cosmetics applications where sustainability credentials matter. Strategic alliances with biotechnology firms and agricultural cooperatives have shortened innovation cycles and enabled faster capacity scale-up, thereby improving time-to-market for new formulations. Manufacturers that prioritize continuous bioprocess optimization and transparent lifecycle reporting will be well positioned to expand their market presence in high-value segments where end users demand verified low-carbon inputs.

Category-wise Analysis

Product Type Insights

Food-grade pyruvic acid is predicted to occupy a commanding market position, projected to capture 45% of the market revenue share in 2026. This leadership reflects extensive deployment across processed foods, beverages, and preservation systems where manufacturers prioritize functional reliability and volume consistency above all else. Regulatory bodies have maintained stable approval frameworks, while producers have delivered predictable batch-to-batch performance that ensures seamless production continuity.

Recurring consumption patterns have generated steady replenishment demand, and the scarcity of cost-effective alternatives has minimized substitution threats. Deep integration with existing processing infrastructure has further cemented this segment's dominance, making it a stable foundation for portfolio planning.

The pharmaceutical-grade segment is are positioned to become the fastest-growing from 2026 to 2033. Clinical development pipelines have expanded significantly, and manufacturing output has increased across global facilities. Research focus on metabolic pathways has intensified, collectively creating strong momentum. Rising demand for high-purity intermediates in specialized formulations and laboratory settings has reinforced this growth trajectory. Stringent quality standards have erected high entry barriers that have facilitated supplier consolidation and supported premium pricing models, offering attractive margins for qualified producers.

Application Insights

Food and beverage applications are expected to account for about 48% of total pyruvic acid demand in 2026, as producers continue to incorporate it into bakery items, beverages, and functional nutrition products. High-volume, recurring consumption patterns are supporting scale efficiencies, while urban lifestyle shifts and stronger preference for packaged and convenience formats are sustaining frequent repurchase cycles. Standardized formulation requirements, clear regulatory treatment, and integration with existing processing assets have allowed procurement teams to source pyruvic acid efficiently and maintain consistent quality across global manufacturing networks.

Pharmaceutical applications are expected to have been the fastest-growing use area between 2026 and 2033, driven by higher investment in drug development programs, biochemical research initiatives, and dermatology-oriented treatments such as chemical peels and controlled-release systems. Demand has been increasing for high-purity intermediates that support studies of metabolic pathways and enable specialized formulations, while capacity expansion in Asia Pacific and Europe has been improving access to supply and shortening project timelines for originators and contract manufacturers. As regulatory expectations have remained stringent, specialized producers that can demonstrate robust quality systems and data packages are expected to have sustained premium pricing, creating a differentiated position in this segment by the end of the forecast period.

End-User Insights

The food industry is poised to account for about 50% of market revenue share by 2026, supported by the sustained use of pyruvic acid in processed foods, beverages, and functional nutrition products that require consistent functional performance at scale. Large processors have established long-term supply contracts that secure volume visibility for producers and stabilize capacity planning across multiple facilities. Recurring consumption patterns and low substitution risk have maintained a dependable baseline demand, while standardized sourcing protocols, clear regulatory approvals, and close integration with production and distribution networks have improved operational efficiency for buyers and suppliers. As a result, the food industry has remained the anchor customer base and will continue to set the context for pricing, quality, and service expectations in major markets.

The pharmaceutical industry is set to emerge as the fastest-growing end-user during the 2026-2033 forecast period, as investment in personalized medicine, biopharmaceutical research, and advanced formulations has been increasing across key regions. Companies have been expanding clinical trial pipelines and drug development projects, which has raised demand for high-purity intermediates that support sophisticated delivery systems and metabolic pathway studies.

Regulators have maintained strict expectations around quality and traceability, so customers have relied more heavily on specialized suppliers that can document robust controls, enabling premium pricing and stronger differentiation. Rising prevalence of chronic and metabolic disorders has been reinforcing this trajectory, and by the end of the forecast period, the pharmaceutical industry will have become a major contributor to overall market expansion, particularly in high-value, margin-accretive applications.

Regional Insights

North America Pyruvic Acid Market Trends

North America is forecasted to be the fastest-growing regional market for pyruvic acid between 2026 and 2033, supported by increasing adoption of bio-based production methods and rising demand for high-purity pyruvic acid in pharmaceutical, specialty chemical, and functional food applications. Strong investment in research and development within biotechnology and chemical sectors is enabling production of high-purity pyruvic acid at scale, catering to demanding pharmaceutical formulations and clinical-grade intermediates. Rising focus on metabolic disorder research and development of advanced therapeutics stimulates demand for bioactive compounds derived from pyruvic acid. Regulatory emphasis on sustainable manufacturing practices and stringent quality standards encourages manufacturers to adopt green synthesis routes, further accelerating growth.

Growth momentum is further supported by technological innovation and strategic industrial integration across North America. Developments in microbial strain engineering, biocatalysis optimization, and continuous flow production techniques enhance yields and reduce processing time, improving operational efficiency for both pharmaceutical and food-grade applications. Expansion of contract manufacturing organizations (CMOs) and contract research organizations (CROs) ensures faster scale-up and adoption of pyruvic acid in emerging therapies and nutraceutical products. Proximity to major research hubs, coupled with robust funding for biotechnology startups, strengthens the innovation pipeline, creating differentiated product grades with premium pricing potential.

Europe Pyruvic Acid Market Trends

Europe is predicted to hold a significant position in the market through 2033, reinforced by increasing adoption of bio-based pyruvic acid in sustainable industrial applications and a strong focus on regulatory compliance. The area emphasizes green chemistry practices across food, pharmaceutical, and specialty chemical sectors, encouraging manufacturers to use pyruvic acid produced via fermentation and enzymatic processes. Investments in clean technology and circular economy initiatives enhance production efficiency while reducing environmental impact. Growing demand for functional foods, nutraceuticals, and high-purity intermediates for clinical research further sustains a consistent market presence.

Market strength is supported by technological advancements and cross-industry collaboration. Improvements in microbial strain development, enzyme catalysis, and process optimization enable higher yields and lower production costs, supporting scalable production for both food-grade and pharmaceutical-grade pyruvic acid. Collaboration between research institutions, biotech startups, and established chemical manufacturers accelerates the development of differentiated pyruvic acid products for specialty pharmaceuticals, metabolic disorder therapies, and cosmetic applications. Regulatory emphasis on sustainability and clean-label sourcing increases adoption in functional foods.

Asia Pacific Pyruvic Acid Market Trends

By 2026, Asia Pacific is expected to command an estimated 45% of the pyruvic acid market share, propelled by strong integration of industrial biotechnology with food, pharmaceutical, and cosmetic sectors. High domestic demand from rapidly expanding processed food and beverage industries creates consistent off-take for pyruvic acid, particularly in flavor enhancers, acidity regulators, and preservation solutions. Strategic investments in large-scale fermentation and biocatalysis facilities improve production efficiency and lower per-unit costs, making Asia Pacific a preferred manufacturing hub. Abundant availability of low-cost, renewable feedstock such as corn, sugarcane, and agricultural residues strengthens raw material security and supports bio-based production methods. Urban population growth and rising consumption of functional foods and nutraceuticals drive demand, enabling manufacturers to achieve scale and optimize margins.

The region's dominance is further bolstered by technological advancements and strategic collaborations between local producers and global players. Investments in microbial strain optimization, enzyme engineering, and process intensification allow higher yields, reduced waste, and faster product turnover. The Asia Pacific market also benefits from logistical advantages, including proximity to raw material sources and export markets, reducing supply chain disruptions and enhancing responsiveness to industrial demand. Growth of skilled workforce in biochemical engineering and industrial biotechnology facilitates rapid deployment of innovative production techniques. Collaborations between research institutions and industrial entities can foster continuous innovation, creating differentiated pyruvic acid grades for high-value applications in pharmaceuticals and specialty chemicals.

Competitive Landscape

The global pyruvic acid market structure demonstrates moderate fragmentation, with leading companies such as Merck, Thermo Fisher Scientific, Tokyo Chemical Industry, Musashino Chemical Laboratory, and Santa Cruz Biotechnology holding substantial market shares and shaping industry dynamics. Smaller manufacturers and specialized chemical producers continue to compete in niche segments, resulting in a competitive landscape where established global suppliers enjoy advantages in scale, compliance, and distribution, while smaller players focus on regional or specialty applications.

Strategic differentiation is most evident among innovation-driven firms such as Thermo Fisher, which have prioritized advanced synthesis methods and high-purity product development for pharmaceutical and research markets, thereby enhancing their functional value proposition. Established players such as Merck and Tokyo Chemical have leveraged their operational scale, regulatory expertise, and global supply chains to maintain premium positioning, ensuring reliable supply and consistent quality for large-scale customers. This dynamic supports ongoing consolidation among top-tier suppliers, while niche competitors continue to serve specialized and regional needs.

Key Industry Developments

- In October 2025, researchers including E.MichiBurrow, Javier Carmona García, Connor J.Clarke, Basile F.E.Curchod, and Jan R.R.Verlet reported precise measurement of the singlet–triplet energy gap of pyruvic acid in the gas phase, offering key insight into its photochemical behavior and advancing understanding of its atmospheric chemistry.

- In July 2025, a study in Genes & Diseases found that oral pyruvate effectively treats ulcerative colitis in mice by reducing inflammation, cytokines, and symptoms while restoring gut barrier integrity. Pyruvate's oral bioavailability, safety, and dual anti-inflammatory/barrier-protective effects position it as a promising candidate for inflammatory bowel disease therapy and beyond, such as rheumatoid arthritis.

- In May 2025, Agios Pharmaceuticals presented new preclinical data on its pyruvate kinase activation portfolio, including mitapivat for sickle cell disease and thalassemia, and AG-946 for PK deficiency, demonstrating improved red blood cell function, energy metabolism, and anemia correction in models. The company is advancing mitapivat into Phase 3 trials for sickle cell disease, with positive topline results from prior hemoglobinopathy studies reinforcing its potential as an oral therapy.

Companies Covered in Pyruvic Acid Market

- Merck KGaA

- Thermo Fisher Scientific Inc.

- Tokyo Chemical Industry (India) Pvt. Ltd.

- Musashino Chemical Laboratory, Ltd.

- Santa Cruz Biotechnology Inc.

- TORAY FINE CHEMICALS CO., LTD.

- Central Drug House.

- MP Biomedicals.

- LobaChemie Pvt. Ltd.

- FUJIFILM Wako Pure Chemical Corporation

Frequently Asked Questions

The global pyruvic acid market is projected to reach US$ 57.5 million in 2026.

Rising demand from pharmaceutical, food, and cosmetic applications, coupled with growing adoption of bio-based and high-purity production methods, drives the market.

The market is poised to witness a CAGR of 4.8% from 2026 to 2033.

Expansion of bio-based synthesis, high-purity pharmaceutical intermediates, and functional cosmetic and food applications represent key market opportunities.

Key players in the market include Merck KGaA, Thermo Fisher Scientific Inc., Tokyo Chemical Industry (India) Pvt. Ltd., and Musashino Chemical Laboratory Ltd.