- Specialty & Fine Chemicals

- Pyridine Market

Pyridine Market Size, Share, and Growth Forecast 2026 - 2033

Pyridine Market by Product Type (Pyridine N-oxide, β-Picoline, α-Picoline, γ-Picoline, 2-Methyl-5-ethylpyridine (MEP), Others), End-user (Agriculture, Pharmaceutical & Healthcare, Chemical Manufacturing, Food & Beverage, Automotive & Rubber, Paints & Coatings, Electronics, Others), by Regional Analysis, 2026 - 2033

Pyridine Market Size and Trend Analysis

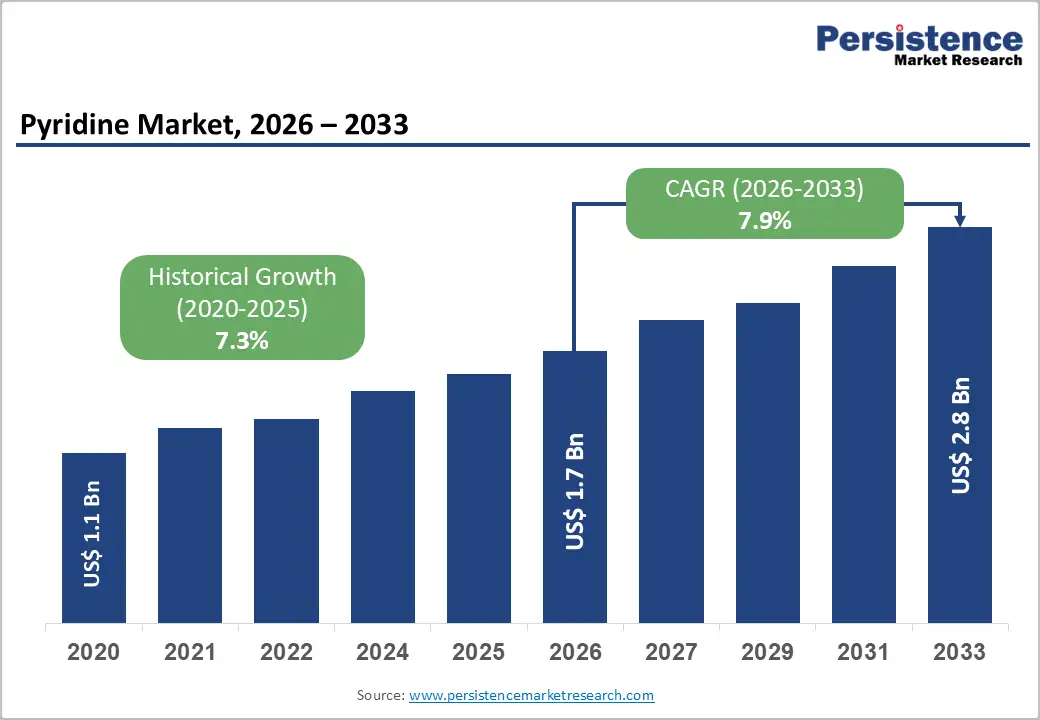

The global pyridine market size is likely to be valued at US$ 1.7 billion in 2026 and is projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033.

This expansion is primarily fueled by surging demand in the agrochemical and pharmaceutical sectors, where pyridine serves as a critical intermediate for pesticides, herbicides, and active pharmaceutical ingredients.

Key Industry Highlights:

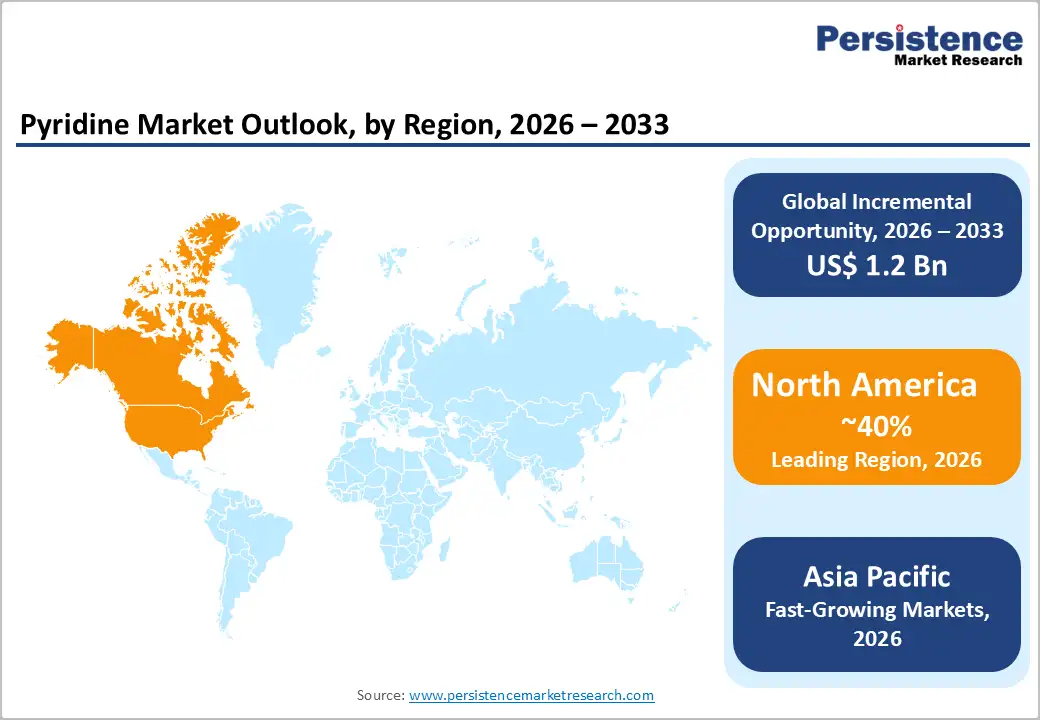

- Leading Region: North America holds a strong position in the pyridine market, with the U.S. leading demand through innovations in pharmaceuticals, agrochemicals, and chemical research, capturing over 40% share.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, fueled by a 10% annual industrial expansion and rising electronics demand in ASEAN countries.

- Leading Segment: The Agriculture segment dominates across end-users, holding 55% share due to essential roles in pesticides and herbicides for global food security.

- Fastest Growing Segment: Pharmaceutical & Healthcare is the fastest-growing end-user, propelled by 7% yearly drug innovation needs and pyridine's API synthesis applications.

- Key Opportunity: Sustainable production in electronics offers key opportunities, with bio-based pyridine derivatives aligning to 30% demand growth by 2030.

| Key Insights | Details |

|---|---|

| Global Pyridine Market Size (2026E) | US$ 1.7 Billion |

| Market Value Forecast (2033F) | US$ 2.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 7.9% |

| Historical Market Growth (2020 - 2025) | 7.3% |

Market Dynamics

Drivers - Growing Pyridine use in Agrochemicals is driven by Rising Pesticide Consumption and the Global Need for Improved Crop Yields

The global pyridine market is witnessing strong growth as demand rises across the agrochemical industry, where pyridine is widely used as a key precursor for herbicides, insecticides, and fungicides. According to the Food and Agriculture Organization (FAO), global pesticide consumption reached 4.1 million tonnes in 2023, highlighting the growing need for efficient crop protection solutions. Pyridine derivatives support improved yields, which is essential as the global population is expected to reach 9.7 billion by 2050.

This trend is particularly important for regions experiencing climate instability, where advanced pest management tools are becoming increasingly critical. Companies are developing modern pyridine-based formulations that offer better performance and reduced environmental impact, aligning with sustainability goals. As agriculture continues to prioritize higher productivity and consistent output, the agrochemical sector’s expansion ensures long-term demand and stable consumption for pyridine worldwide.

Pharmaceutical Expansion Boosts Pyridine Demand as it Remains Essential for Producing Key Apis and Advanced Drug Formulations

Pyridine plays a vital role in the pharmaceutical sector as a core ingredient in the production of essential drug intermediates, including analgesics, antivirals, and anti-inflammatory medications. The World Health Organization (WHO) reported a 6.5% increase in global pharmaceutical production in 2024, driven by rising chronic disease prevalence and growth in personalized medicine. Pyridine derivatives are also crucial in the manufacture of vitamin B3 and several active pharmaceutical ingredients that require high-purity chemicals.

As more countries expand healthcare budgets and improve drug accessibility, demand for pyridine-based intermediates is set to grow steadily. Additionally, increased regulatory approvals for innovative drug formulations encourage chemical manufacturers to enhance their production capabilities. Pyridine’s ability to support targeted chemical reactions makes it indispensable in complex drug synthesis. As a result, pharmaceuticals represent one of the most significant and steadily expanding end-user segments within the global pyridine market.

Restraint - Strict Environmental Regulations Increase Production Costs and Compliance Burdens for Pyridine Manufacturers Worldwide

Environmental regulations continue to be a major restraint for the pyridine market due to the compound’s toxic and volatile nature, which requires strict handling and emission control. The U.S. Environmental Protection Agency (EPA) enforces tight guidelines and has increased fines for non-compliance to up to $50,000 per day, significantly raising operational costs for chemical producers.

These regulations focus on reducing hazardous waste and limiting harmful emissions, thereby increasing investment in pollution-control technologies. Smaller manufacturers often struggle to meet these regulatory expectations, which reduces competition and slows overall industry innovation. In regions with particularly strict environmental standards, market entry becomes challenging, further limiting supply growth. As regulatory frameworks continue to evolve globally, companies must allocate more resources to compliance, which adds pressure to profit margins and impacts the pace of market expansion.

Volatile Petroleum-Based Raw Material Prices Disrupt Pyridine Production Costs and Hinder Market Stability

The pyridine market is also affected by fluctuations in raw material prices, particularly for ammonia and acetaldehyde, both derived from the petroleum sector. The International Energy Agency (IEA) recorded a 15% spike in crude oil prices in 2024 due to geopolitical conflicts and supply disruptions, directly increasing production costs for pyridine manufacturers. This price instability complicates long-term planning and disrupts procurement strategies, especially for companies dependent on imported feedstocks.

As raw material costs rise, manufacturers face shrinking margins and may delay expansions or reduce output to manage financial risks. Emerging economies, which already face infrastructure and supply chain constraints, feel these impacts more acutely. The combination of volatile pricing and uncertainty in the energy market restricts investment confidence and contributes to inconsistent market development across regions.

Opportunity - Sustainable and Bio-Based Pyridine Technologies Offer Strong Growth Opportunities amid Global Green Chemistry Trends

Sustainable production technologies present strong growth opportunities for the pyridine market, especially as industries shift toward environmentally friendly processes. The European Chemicals Agency (ECHA) estimates that green and bio-based pyridine alternatives could meet up to 30% of global demand by 2030. Companies are investing heavily in biomass-derived synthesis methods, which help reduce carbon emissions by nearly 40% compared to conventional production.

These innovations not only support regulatory compliance but also appeal to customers looking to incorporate eco-friendly materials into agrochemicals and pharmaceuticals. Global sustainability initiatives, including the United Nations Sustainable Development Goals, further push manufacturers to adopt cleaner production processes. As environmental policies strengthen worldwide, businesses that prioritize sustainable pyridine solutions are likely to attract more partnerships, funding, and market share, making this an attractive long-term opportunity for industry participants.

The Expanding Electronics Industry Creates High-Value Opportunities for Pyridine in Semiconductor and Specialty Material Applications

The electronics industry is emerging as a promising segment for pyridine applications, particularly in high-performance materials, semiconductor processing, and specialty solvents. According to the International Telecommunication Union (ITU), global electronics production is expected to grow at an annual rate of 8% through 2032, driven by rapid advancements in 5G networks, IoT devices, and advanced computing technologies.

Pyridine is increasingly used in coating materials and adhesive formulations essential for semiconductor manufacturing. Asia-Pacific remains a key growth hub, driven by strong manufacturing activity in China, India, Japan, and South Korea. Government initiatives such as India’s $10 billion semiconductor support scheme are further boosting demand for chemical intermediates like pyridine. With high-margin opportunities in specialized electronics-grade derivatives, this segment offers strong potential for producers focused on innovation and product customization.

Category-wise Analysis

By Product Type Insights

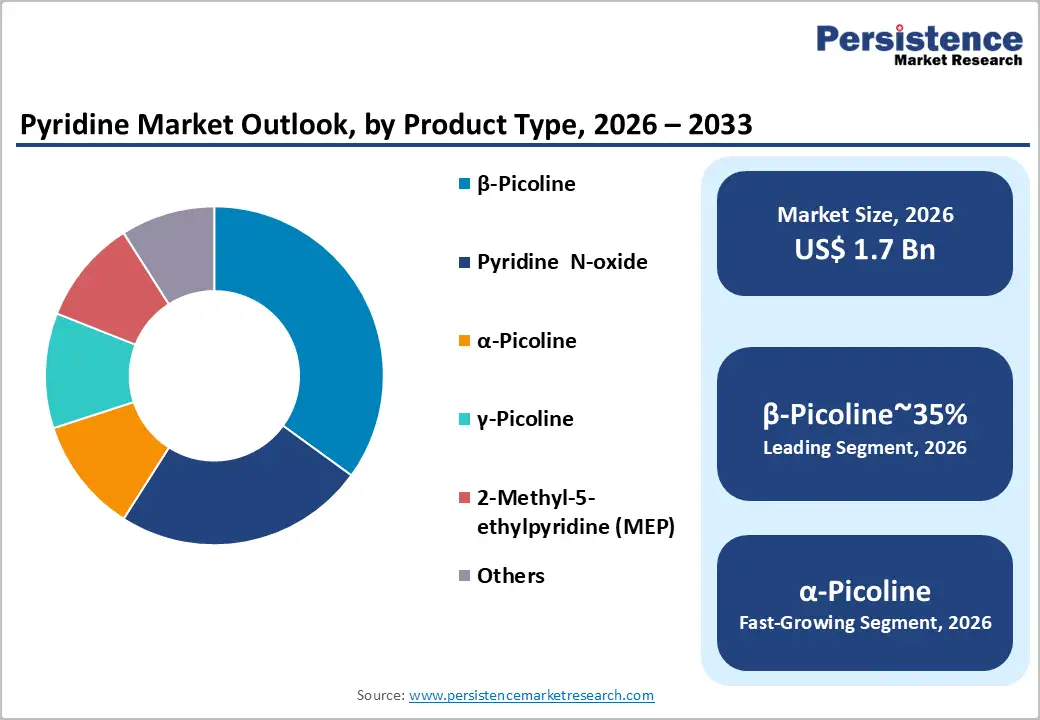

β-Picoline remains the top product type, holding nearly 35% market share due to its essential role in producing major agrochemicals, especially herbicides such as picloram. FAO data showing a 25% rise in herbicide use from 2020-2024 highlights its growing importance in crop protection. Its strong chemical stability and versatility make it a preferred choice for large-scale synthesis. The growing use of pharmaceutical intermediates further boosts demand, encouraging manufacturers to expand production capacity.

By End-user Insights

The Agriculture segment continues to lead the end-user market with about 55% share, driven by pyridine’s widespread use in pesticides, herbicides, and fungicides that protect crops from pests and diseases. UNEP data showing a 12% annual rise in agrochemical demand reinforces this trend. Pyridine-based solutions support higher yields and align with sustainable farming practices that reduce environmental impact. As global food security becomes a priority, the agriculture sector will maintain strong and consistent demand for pyridine derivatives.

Regional Insights

North America Pyridine Market Trends

North America holds a strong position in the pyridine market, with the U.S. leading demand through innovations in pharmaceuticals, agrochemicals, and chemical research. The U.S. Department of Agriculture (USDA) noted an 8% increase in pesticide use in 2024, reflecting continued reliance on pyridine-based formulations in modern precision farming. The region’s advanced regulatory environment, particularly EPA standards, encourages the development of safer, high-quality chemical products.

This motivates companies to invest in cutting-edge technology and purification processes to meet strict quality benchmarks. North America is also home to several major pharmaceutical manufacturers that consume large quantities of high-purity pyridine for drug synthesis. The combination of technological advancements, strong industrial infrastructure, and a focus on premium-quality materials ensures the region remains an important growth hub with stable long-term demand.

Europe Pyridine Market Trends

Europe’s pyridine market is largely shaped by regulatory frameworks such as REACH, which encourage cleaner, safer, and more sustainable chemical production. Countries including Germany, France, and the Netherlands are leading investments in green chemical technologies, supported by the European Commission's 2024 report of a 10% rise in sustainable chemical spending. Germany stands out with strong demand from agrochemicals, pharmaceuticals, and specialty chemical industries.

The U.K. and Spain are experiencing growth as local pharmaceutical manufacturing expands in the post-Brexit landscape, prompting higher pyridine consumption. European companies are increasingly prioritizing eco-friendly production methods, which aligns with broader EU environmental directives. As environmental policies tighten, the region continues to see increased innovation and market resilience, positioning Europe as a significant contributor to global pyridine demand.

Asia Pacific Pyridine Market Trends

Asia Pacific remains the dominant region in the global pyridine market, driven by extensive manufacturing capabilities, cost-effective production, and strong demand across agriculture, pharmaceuticals, and electronics. China and India lead regional growth, supported by large-scale chemical production facilities and strong export networks. The Asian Development Bank (ADB) reports that the region’s chemical output is expected to grow at a 15% CAGR through 2032, underscoring its importance in global supply chains.

Japan continues to influence demand through its advanced electronics sector, where pyridine is used in semiconductor materials. ASEAN countries, including Indonesia and Vietnam, are also expanding production capacity due to supportive government incentives and rising agricultural needs. With favorable economic conditions, large consumer bases, and industrial expansion, the Asia Pacific is set to maintain its leadership in pyridine production and consumption over the long term.

Competitive Landscape

The global pyridine market exhibits a consolidated structure, with the top three players—Vertellus Specialties Inc., Jubilant Life Sciences Limited, and Red Sun Group—controlling over 60% of the market share through integrated supply chains and R&D focus. Companies pursue expansion via capacity upgrades and partnerships, emphasizing sustainable technologies to differentiate. Key strategies include backward integration for raw materials and geographic diversification into Asia. Emerging models like bio-based production are gaining traction, enhancing competitiveness amid regulatory constraints.

Key Market Developments

- In October 2024, Lonza completed its acquisition of the Genentech large-scale biologics manufacturing facility in Vacaville, California, from Roche for USD 1.2 billion. This strategic move considerably enhances Lonza's position in the global biomanufacturing market and expands its footprint on the US West Coast.

- In May 2020, Trineso agreed to purchase Synthomer PLC's vinyl pyridine latex business, thereby expanding its product line.

- In June 2021, Vertellus reached an agreement to acquire ESIM Chemicals' intermediates and specialties business, a prominent supplier of specialized chemical products for the pharmaceutical, coatings, and fuel and lubricant industries.

Companies Covered in Pyridine Market

- Vertellus Specialties Inc.

- Jubilant Life Sciences Limited

- Lonza Group Ltd

- Red Sun Group

- Resonance Specialties Limited

- Shandong Luba Chemical Co., Ltd.

- Koei Chemical Co., Ltd.

- Weifang Sunwin Chemicals Co., Ltd.

- Bayer AG

- LOBA Feinchemie AG

- Merck KGaA

- The Dow Chemical Company

- Nippon Steel & Sumikin Chemical Co. Ltd.

- Labex Corporation

- Hubei Sanonda Co. Ltd.

Frequently Asked Questions

The global pyridine market is projected to reach US$ 2.8 Billion by 2033, growing from US$ 1.7 Billion in 2026 at a 7.9% CAGR, driven by agrochemical and pharmaceutical demands.

Rising agrochemical needs, with pyridine sessential for herbicides and pesticides, is a primary driver, supported by FAO projections for increased global food production.

The Agriculture segment leads with 55% share, due to its critical use in crop protection chemicals amid growing pest management requirements.

North America holds a strong position in the pyridine market, with the U.S. leading demand through innovations in pharmaceuticals, agrochemicals, and chemical research, capturing over 40% share.

Advancements in sustainable electronics applications offer significant opportunities, with pyridine derivatives supporting 8% annual sector growth.

Key players include Vertellus Specialties Inc., Jubilant Life Sciences Limited, and Bayer AG, focusing on R&D and capacity expansion for competitive edge.