- Medical Devices

- Pulsed Field Ablation (PFA) Market

Pulsed Field Ablation (PFA) Market Size, Share, and Growth Forecast, 2026 – 2033

Pulsed Field Ablation (PFA) Market by Therapeutic Area (Cardiovascular Disorders, Oncological Disorders, Respiratory Disorders, Dermatological Disorders), Product (Catheter, Generator), End-User (Ablation, Ablation & Mapping), and Regional Analysis for 2026-2033

Pulsed Field Ablation (PFA) Market Share and Trends Analysis

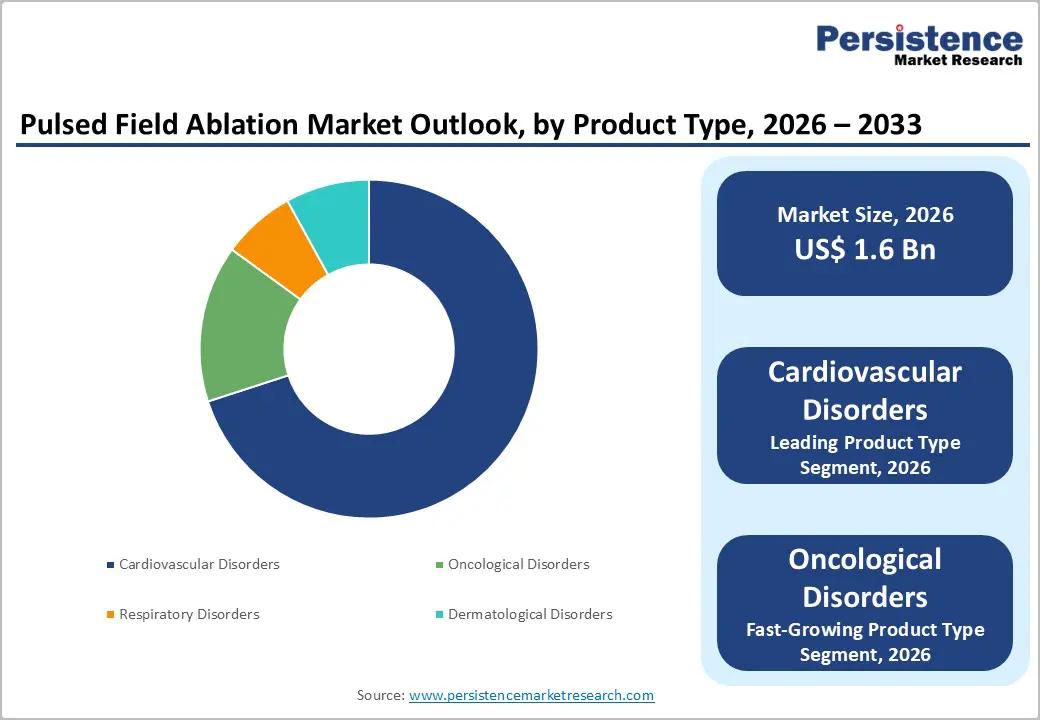

The global pulsed field ablation (PFA) market size is likely to be valued at US$ 1.6 billion in 2026, and is projected to reach US$ 11.9 billion by 2033, growing at a CAGR of 33.2% during the forecast period 2026−2033.

Rapid market expansion reflects a structural shift in interventional electrophysiology toward non-thermal ablation modalities that reduce collateral tissue injury and procedural risk. Aging population cohorts increase the prevalence of atrial fibrillation and other complex arrhythmias, which expands the clinically addressable patient base requiring safer and repeatable interventions.

Rising clinical awareness among cardiologists and electrophysiologists is accelerating adoption, supported by the growing dissemination of real-world evidence and procedural standardization across tertiary care centers. Treatment adoption strengthens as healthcare systems prioritize outcomes linked to shorter procedure duration, reduced complication profiles, and faster patient recovery, which align with value-based care frameworks. Technological integration of advanced generators, optimized catheter designs, and real-time mapping systems enhances procedural precision, reinforcing clinician confidence and institutional procurement decisions.

Key Industry Highlights

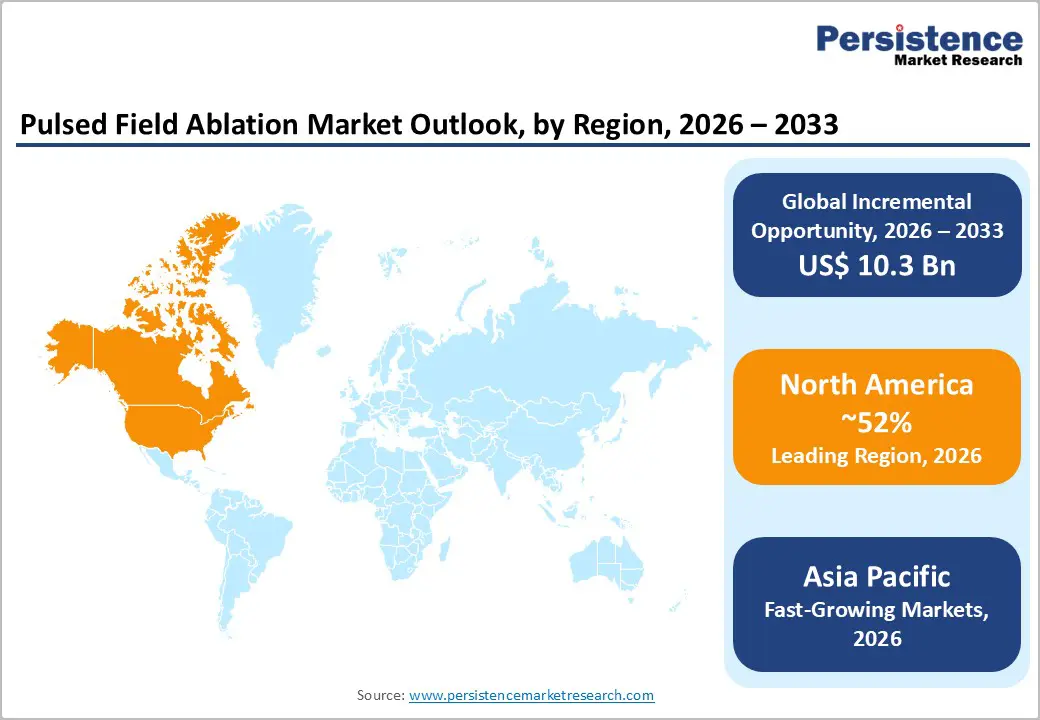

- Dominant Region: North America is projected to capture approximately 52% of the PFA market share in 2026, driven by atrial fibrillation (AF) protocols and high procedural density.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market through 2033, fueled by the rising incidence of cardiovascular disease and expanding hospital infrastructure.

- Leading Therapeutic Area: Cardiovascular disorders are anticipated to account for around 70% of revenue in 2026, supported by high arrhythmia prevalence and compatibility with mapping platforms.

- Fastest-growing Therapeutic Area: Oncological disorders are expected to be the fastest-growing during 2026–2033, driven by selective tissue targeting and the potential to elicit an immunogenic response.

- January 2026: U.S. Food and Drug Administration (FDA)-approved PFA technology from Kardium's Globe PF System achieved 77.8% freedom from atrial arrhythmias at 1 year in the PULSAR IDE study.

| Key Insights | Details |

|---|---|

| Pulsed Field Ablation (PFA) Market Size (2026E) | US$ 1.6 Bn |

| Market Value Forecast (2033F) | US$ 11.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 33.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 32.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Prevalence of Atrial Fibrillation and Demand for Safer Ablation Methods

Escalation in diagnosed cases of atrial fibrillation reflects demographic aging, higher survival from cardiovascular disease, and broader use of continuous rhythm monitoring across care settings. Rising AF incidence increases hospital admissions related to stroke risk, heart failure progression, and recurrent emergency visits, which elevates the priority placed on durable rhythm control strategies. Pharmacological management shows variable efficacy and tolerance across heterogeneous patient profiles, leading care pathways toward interventional solutions at earlier disease stages. Conventional thermal ablation techniques present variability in lesion formation and procedural risk across anatomies, which constrains scalability as case volumes rise.

Health systems face pressure to manage growing AF caseloads with predictable outcomes, shorter procedure times, and reduced downstream complications. These structural pressures position catheter-based ablation as a central therapeutic option, while exposing limitations of existing technologies under expanding clinical demand.

Preference for safer ablation approaches reflects heightened scrutiny from clinicians, providers, and payers focused on procedural risk, resource utilization, and long-term value. Pulsed field ablation uses non-thermal electroporation with tissue selectivity, favoring myocardial cells while sparing adjacent structures such as the esophagus and phrenic nerve. This safety profile aligns with institutional objectives centered on complication avoidance, standardized outcomes, and reproducibility across operator experience levels. Reduced dependence on precise thermal control simplifies workflows and supports consistent lesion quality, which strengthens confidence in broader adoption. Economic considerations further reinforce uptake, as lower complication rates translate into shorter hospital stays and fewer follow-up interventions.

Regulatory Clearance Timelines and Clinical Evidence Requirements

Extended approval pathways arise from the novelty of tissue-selective electrical energy delivery and limited long-term clinical familiarity. Regulatory bodies require multi-phase human studies, durability follow-up, and cross-population validation to confirm safety margins around cardiac conduction systems and adjacent structures. Evidence packages require statistically powered outcomes, standardized procedural protocols, and operator learning-curve assessment. These requirements elevate development costs, prolong submission cycles, and delay geographic expansion. Capital allocation decisions face pressure when return timelines extend, leading to cautious investment pacing. Startups encounter financing constraints during prolonged pre-revenue periods, while established manufacturers reprioritize portfolios toward platforms with predictable clearance pathways.

Clinical evidence expectations remain rigorous, as they must demonstrate sustained arrhythmia control, low complication rates, and reproducibility across care settings. Trial designs require comparative endpoints against established therapies, real-world registries, and post-approval surveillance commitments. Data heterogeneity across centers necessitates harmonized reporting, increasing coordination complexity. Physician adoption depends on peer-reviewed outcomes and guideline endorsement, both tied to robust evidence maturity. Hospitals and payers align procurement and reimbursement decisions with validated outcomes and health economic value, slowing uptake in the absence of definitive datasets.

Integration with Digital Health Platforms and Advanced Mapping Technologies

The convergence of digital health platforms with advanced mapping technologies creates a high-impact opportunity through transformation of procedural intelligence and clinical workflow efficiency. High-definition mapping systems translate electrophysiological signals into actionable visual insights, enabling precise localization of treatment targets during complex interventions. When connected with digital platforms, these insights integrate seamlessly with patient records, historical procedure data, and clinical decision frameworks. This unified environment supports standardized planning, real-time guidance, and outcome tracking within a single operational structure. Health systems increasingly evaluate technologies based on consistency, predictability, and data transparency, positioning digitally connected solutions as enablers of repeatable clinical performance and optimized resource utilization.

Strategic value further emerges from longitudinal data integration and system-wide interoperability. Digital platforms aggregate procedural metrics, follow-up data, and patient monitoring information into structured datasets that support performance benchmarking and continuous improvement. Advanced mapping alignment strengthens analytical depth, enabling trend identification, predictive modeling, and evidence-based protocol refinement. Hospital administrators and payer organizations prioritize technologies that demonstrate operational efficiency, traceable outcomes, and scalability across care networks. This integration supports standardization of training, reduces reliance on individual operator variability, and aligns clinical delivery with institutional governance requirements.

Category-wise Analysis

Therapeutic Area Insights

Cardiovascular disorders are anticipated to secure around 70% of the pulsed field ablation market revenue share in 2026, reflecting established clinical application in atrial fibrillation treatment. High prevalence of arrhythmias sustains consistent procedural demand across tertiary hospitals and specialized cardiac centers. Provider preference strengthens through tissue-selective, non-thermal mechanisms that preserve surrounding anatomical structures. Clinical acceptance advances through lower complication incidence, supporting confidence among electrophysiology teams. Treatment effectiveness is demonstrated through stable lesion formation and reliable rhythm normalization outcomes. Workflow efficiency improves through compatibility with electroanatomical mapping platforms.

Oncological disorders are expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by emerging applications in tumor ablation and margin accentuation. Expanding clinical evidence supports selective cellular disruption while limiting collateral tissue impact, aligning with precision oncology objectives. Treatment effectiveness addresses procedural gaps in managing complex solid tumors where thermal techniques show limitations. Provider preference increases through potential immunogenic responses associated with targeted cell destruction. Accessibility improves as protocols align with established oncology care pathways and interventional radiology practices.

Product Components Insights

Catheter components are poised to dominate, with a forecasted PFA market revenue share of over 75% in 2026, driven by their recurring use and procedural centrality. High procedural frequency across cardiac intervention centers sustains continuous replacement demand. Clinician trust remains anchored in predictable energy delivery, flexible shaft control, and ergonomic handling during complex workflows. Cultural alignment within electrophysiology practice supports the use of disposable, single-use formats that reinforce sterility and regulatory compliance.

Hospital procurement frameworks favor long-term supply agreements, ensuring consistent purchasing volumes. Preventive healthcare emphasis encourages earlier intervention, driving higher case throughput. Centralized digital procurement platforms improve inventory visibility, accelerate reorder cycles, and reduce supply chain variability.

Generator systems are estimated to be the fastest-growing segment from 2026 to 2033, fueled by technological upgrades and platform expansion. Advancements in energy modulation, software intelligence, and safety monitoring elevate system reliability and clinical confidence. Institutional acceptance grows through seamless interoperability with existing mapping and imaging infrastructure. Preventive healthcare strategies prioritize modernizing procedural suites, enabling accelerated generator replacement cycles.

Digital procurement models combined with service-based contracts strengthen lifecycle management efficiency. Recurring revenue potential expands through software updates, performance analytics, and long-term maintenance agreements, reinforcing strategic value for healthcare providers and manufacturers.

End-User Insights

Ablation is likely to be the leading application segment, with a projected 75% share of the pulsed-field ablation market in 2026, driven by established clinical protocols and widespread physician familiarity. Clinical credibility strengthens through repeatable outcomes, predictable lesion formation, and alignment with standardized electrophysiology guidelines. Provider referral momentum increases as care pathways formally position this approach as a frontline interventional option.

Digitalization of procedural planning improves case prioritization, scheduling efficiency, and resource coordination within catheterization laboratories. Economic performance benefits from lower complication incidence, reduced post-procedural monitoring intensity, and shorter inpatient durations.

Ablation and mapping applications are anticipated to be the fastest-growing application segment from 2026 to 2033, fueled by demand for integrated diagnostic and therapeutic workflows. Real-time mapping integration elevates clinical decision accuracy by correlating anatomical visualization with electrophysiological data during intervention. Technology-enabled service delivery supports management of complex arrhythmia cases while facilitating standardized training and procedural replication across institutions.

Operational efficiency improves through the consolidation of diagnostic and therapeutic steps into a unified workflow. Cost efficiency develops through reduced procedure times, lower variability in outcomes, and optimized utilization of clinical staff and infrastructure, supporting accelerated adoption across advanced care settings.

Regional Insights

North America Pulsed Field Ablation (PFA) Market Trends

North America is poised to capture around 52% of the market share in 2026, reflecting structural advantages embedded within cardiac intervention infrastructure. Dominance stems from established procedural protocols in atrial fibrillation treatment, where pulsed field ablation transitioned from experimental evaluation to standard practice. High procedural density across tertiary electrophysiology centers accelerates clinician expertise and validates consistent outcomes. Reimbursement systems favor technologies demonstrating improved safety profiles and operational efficiency, enabling faster adoption and capital deployment.

Collaboration among device manufacturers, hospitals, and physician networks ensures rapid translation of clinical evidence into procedural volume, creating a feedback loop that reinforces market strength.

Leadership is further strengthened through concentration of technology development, regulatory clarity, and data-driven clinical oversight. Early regulatory approvals enable commercial scaling, while comprehensive post-procedure datasets support protocol optimization and risk mitigation. Integration with advanced mapping, imaging, and digital workflow platforms improves procedural throughput and resource utilization, increasing economic value for providers. Procurement strategies emphasize long-term partnerships, ensuring recurring demand for consumables and system updates.

Workforce specialization within electrophysiology reduces operator variability, supporting predictable outcomes and consistent referral patterns.

Europe Pulsed Field Ablation (PFA) Market Trends

Europe demonstrates steady growth in the pulsed field ablation market, supported by advanced healthcare infrastructure and high procedural awareness among clinicians. Adoption of minimally invasive cardiac interventions is facilitated by established electrophysiology networks and widespread availability of mapping and imaging systems. Procedural standardization across hospitals improves outcome predictability, fostering clinician confidence and increasing referral consistency.

Regulatory clarity enables early market entry for innovative ablation technologies, while reimbursement structures prioritize therapies with demonstrated safety and efficiency advantages. Investment in high-volume cardiac centers and specialty clinics ensures sufficient procedural throughput to validate clinical benefits, supporting incremental adoption of pulsed field ablation in standard atrial fibrillation management pathways.

Clinical research initiatives and technological integration further reinforce market positioning. Collaborative studies between hospitals and device manufacturers generate robust evidence for safety, effectiveness, and long-term rhythm control outcomes. Integration with digital platforms for procedural planning and outcome tracking improves operational efficiency and resource allocation, enabling hospitals to expand adoption across multiple facilities. Cost optimization remains a key driver, as reduced complication rates and shorter inpatient durations align with institutional efficiency goals. Training programs for electrophysiologists enhance procedural expertise and reduce operator variability, strengthening consistent application across centers.

Asia Pacific Pulsed Field Ablation Market Trends

Asia Pacific is forecast to be the fastest-growing market for pulsed field ablation between 2026 and 2033, driven by rising cardiovascular disease prevalence and accelerated healthcare modernization. Rising incidence of atrial fibrillation and related arrhythmias drives procedural demand across metropolitan and emerging urban centers. Expansion of hospital infrastructure and establishment of specialized cardiac intervention units create opportunities for advanced therapy adoption. Structured clinician training programs and growing experience with minimally invasive procedures enhance procedural efficiency and safety outcomes.

Private hospital chains and high-volume cardiac centers actively prioritize innovative, tissue-selective technologies, while integration with mapping and imaging platforms enhances precision and procedural confidence, facilitating faster adoption across diverse healthcare settings.

Healthcare policy initiatives and economic factors further reinforce PFA market growth in the region. Government-backed infrastructure development and private investment increase accessibility of advanced ablation solutions to broader populations. Cost-sensitive institutions favor non-thermal, tissue-preserving approaches that reduce complication-related expenditures and shorten inpatient durations, improving overall procedural efficiency. Collaborations and technology transfer agreements with global manufacturers facilitate access to state-of-the-art systems, while long-term service and maintenance contracts support sustainable adoption. Integration of digital workflow management and data analytics enables operational optimization, procedural standardization, and scalability across multiple facilities.

Competitive Landscape

The global pulsed field ablation market demonstrates a moderately concentrated structure dominated by multinational medical device manufacturers with established electrophysiology portfolios. Leading players such as Medtronic, Boston Scientific Corporation, Abbott, Johnson & Johnson, Koninklijke Philips N.V., and Siemens Healthineers AG maintain substantial influence through proprietary platforms and integrated procedural solutions. Market share concentration reflects strong brand recognition, extensive clinical validation, and long-standing relationships with hospitals and specialty cardiac centers. Product differentiation, including tissue-selective energy delivery, advanced catheter designs, and compatibility with mapping and imaging systems, serves as a primary competitive lever. High procedural volumes across advanced healthcare facilities reinforce recurring demand for consumables and system upgrades, consolidating market leadership among top-tier companies.

Competitive dynamics focus on technology innovation, clinical evidence generation, and global distribution reach. Companies emphasize research collaborations, clinical trials, and post-market data collection to demonstrate safety, effectiveness, and procedural efficiency, enhancing adoption among electrophysiologists. Strategic initiatives such as partnerships with digital workflow providers and expansion of service and maintenance networks further strengthen market positioning. Marketing and training programs targeting hospitals and specialist clinicians reinforce brand loyalty and procedural standardization. Regional expansion and alignment with reimbursement frameworks ensure sustained access to high-volume intervention centers.

Key Industry Developments

- In January 2026, Abbott secured CE mark in the European Union (EU) for TactiFlex Duo, a dual-energy ablation catheter for treating AF, allowing seamless switching during procedures based on patient needs. It targets complex cases such as heart failure or prior failed ablations and integrates with EnSite X for 3D heart mapping.

- In December 2025, Abbott’s Volt pulsed field ablation system received U.S. FDA approval to treat atrial fibrillation, enabling imminent commercial procedures in the United States following strong clinical trial safety and effectiveness results and continued expansion from earlier European CE Mark authorization.

- In November 2025, Johnson & Johnson MedTech presented multiple clinical and real-world study results for its integrated VARIPULSE pulsed field ablation platform at the APHRS and JPHRS meetings, highlighting new safety, efficacy, and workflow data that reinforce procedural consistency and adoption across global electrophysiology practices.

Companies Covered in Pulsed Field Ablation (PFA) Market

- Medtronic

- Boston Scientific Corporation

- Abbott.

- Johnson & Johnson

- Koninklijke Philips N.V.

- Siemens Healthineers AG

- Kardium

- Japan Lifeline Co., Ltd.

- MicroPort Scientific Corporation.

Frequently Asked Questions

The global pulsed field ablation (PFA) market is projected to reach US$ 1.6 billion in 2026.

Rising prevalence of arrhythmias, demand for minimally invasive cardiac interventions, and adoption of tissue-selective, non-thermal ablation technologies are driving the market.

The market is poised to witness a CAGR of 33.2% from 2026 to 2033.

Integration with digital health platforms, advanced mapping technologies, and expanding applications in oncology present key market opportunities.

Some of the key market players include Medtronic, Boston Scientific Corporation, Abbott, Johnson & Johnson, and Koninklijke Philips N.V.