- Sensors & Controls

- Proximity Sensor Market

Proximity Sensor Market Size, Share, and Growth Forecast, 2026- 2033

Proximity Sensor Market by Technology (Magnetic, Infrared (IR), Capacitive Radiation, Force Sensor, and Other), by Product Type (Fixed Distance, Variable Distance), by Industry Vertical (Automotive, Industrial & Manufacturing, Aerospace & Defence, Building Automation, Consumer Electronics, Food & Beverage, and Others), and Regional Analysis for 2026 – 2033

Proximity Sensor Market Size and Trends Analysis

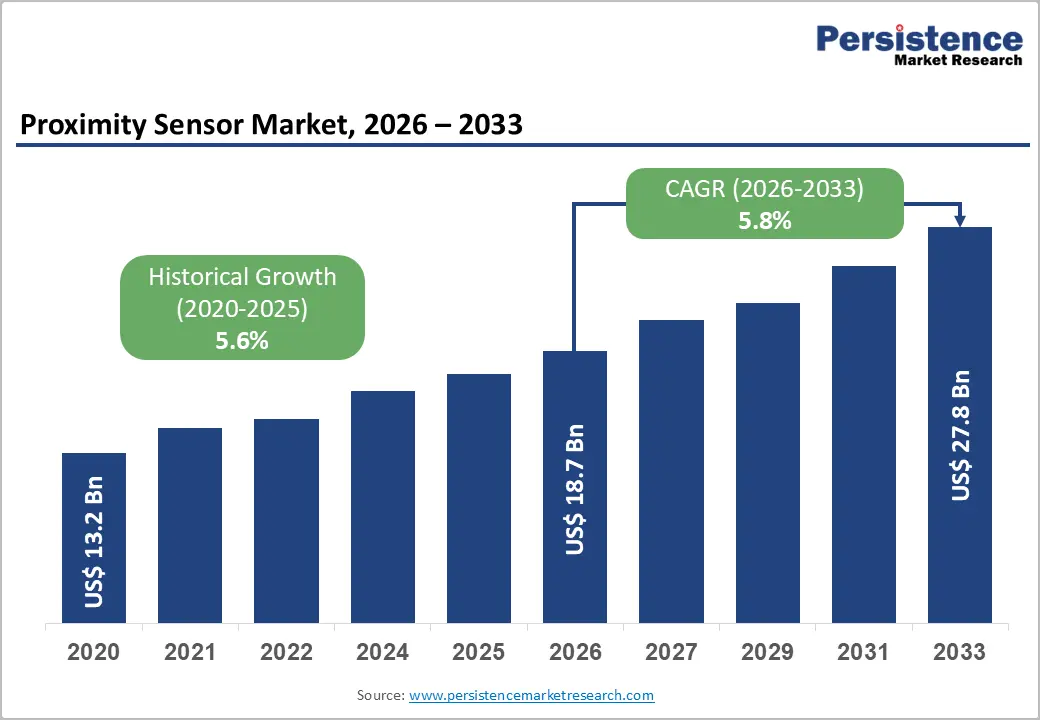

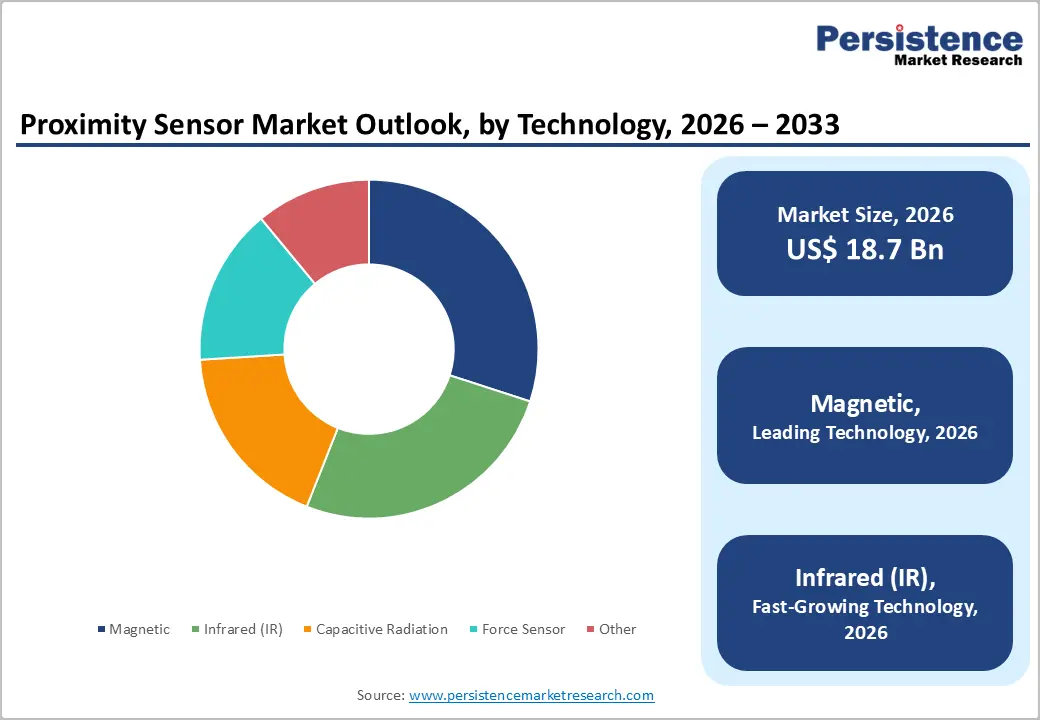

The global proximity sensor market size was valued at US$ 14.2 Billion in 2020 and reached US$ 18.7 Billion in 2026, with projections to expand to US$ 27.8 Billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

The market experienced a historical CAGR of 4.7% from 2020-2026, indicating accelerating growth momentum. The Proximity Sensors Market is driven by demand for non-contact object detection that eliminates physical wear, abrasion, and damage. Unlike mechanical switches, proximity sensors detect objects electrically, using semiconductor outputs that ensure longer service life and high-speed response. They perform reliably in harsh environments involving oil, water, dirt, chemicals, and extreme temperatures ranging from –40°C to 200°C, while remaining unaffected by object color. Inductive sensors detect metallic objects through eddy-current–based impedance changes, capacitive sensors sense variations in capacitance to detect metals, liquids, and resins, and magnetic sensors operate via reed switches activated by magnets. Their durability, precision, and versatility support widespread industrial adoption.

Key Industry Highlights:

- Technology Analysis: Magnetic proximity sensors maintain market leadership with 30%+ revenue share, while Infrared sensors represent fastest-growing technology at 7.2%+ CAGR, reflecting technology transition toward advanced applications

- Product Type Analysis: Fixed distance sensors command 65%+ revenue dominance; Variable distance sensors represent fastest-growing segment at 6.5% CAGR, reflecting structural shift toward intelligent automation platforms

- Industry Vertical: Automotive industry dominates with 40%+ market share; Industrial & Manufacturing vertical demonstrates fastest growth at 6.7% CAGR, driven by Industry 4.0 implementation and manufacturing automation acceleration

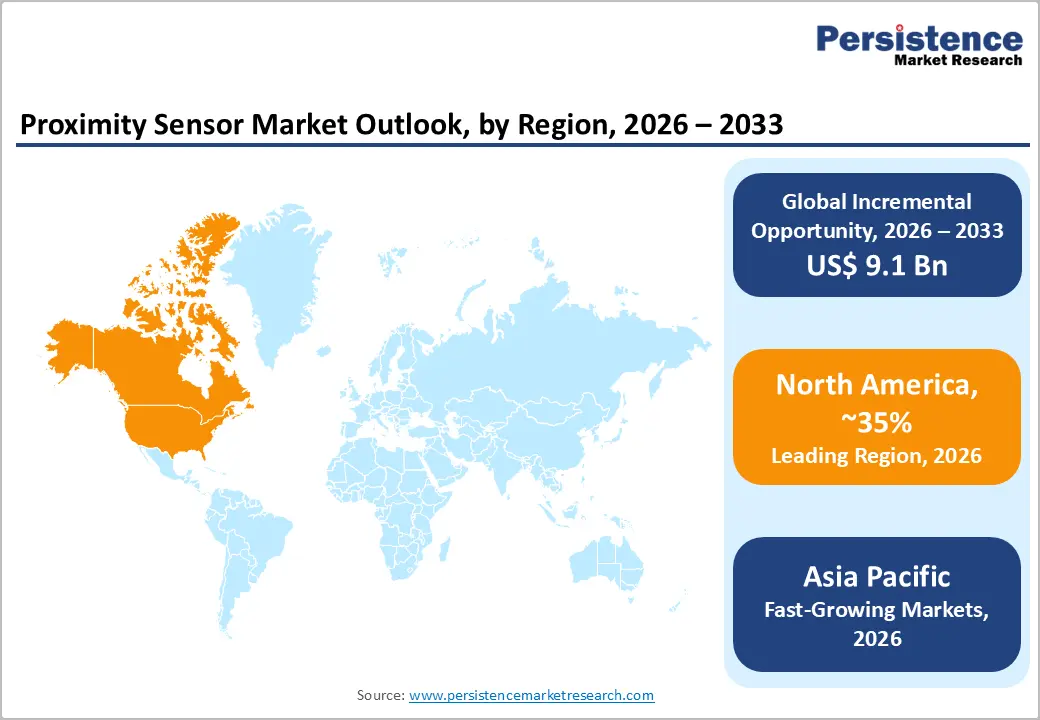

- Regional Analysis: Asia-Pacific region fastest-growing at 6.6% CAGR with North America maintaining market leadership at 35% revenue share, reflecting geographic divergence between mature and emerging market growth dynamics

- Competitive Analysis: Market consolidation ongoing through strategic acquisitions and manufacturing localization initiatives, with estimated 8-12 major transactions through 2026 reshaping competitive landscape toward integrated solution providers

- Vehicle electrification and building automation represent primary growth catalysts, with EV penetration expansion and smart building technology adoption creating structural demand multiplication drivers

| Report Attribute | Details |

|---|---|

|

Proximity Sensor Market Size (2026E) |

US$ 2.1 Bn |

|

Market Value Forecast (2033F) |

US$ 3.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.2% |

Market Dynamics

Key Growth Drivers

Accelerating Automotive Electrification and Autonomous Vehicle Development

The automotive industry's transition toward electric vehicles (EVs) and autonomous driving systems has become a fundamental growth driver for proximity sensor deployment. The automotive segment commands over 40% of the global proximity sensor market, reflecting the critical role these sensors play in vehicle safety systems, collision avoidance mechanisms, and automated parking features. EV manufacturers require proximity sensors for battery management systems, thermal monitoring, and advanced driver-assistance systems (ADAS).

According to industry data, global EV sales reached approximately 14 million units in 2023, with projections exceeding 35 million units by 2030, directly correlating with increased proximity sensor demand. The integration of proximity sensors in autonomous vehicles for obstacle detection, lane-keeping assistance, and adaptive cruise control represents a structural growth opportunity. This automotive-driven demand is projected to expand at approximately 6.0% CAGR through 2033, substantially above the historical 4.7% baseline, demonstrating the accelerating nature of this trend.

Market Restraining Factors

Technical Limitations and Environmental Interference Challenges

Proximity sensors' susceptibility to environmental interference factors including electromagnetic interference (EMI), temperature fluctuations, and material characteristics presents operational constraints in demanding industrial environments. Certain proximity sensor technologies (particularly capacitive sensors) demonstrate limited effectiveness in the presence of moisture, dust, or metallic contamination, requiring protective enclosures that elevate system costs and complexity.

Temperature sensitivity in extreme environments (automotive engines, industrial furnaces, outdoor building automation) necessitates specialized versions commanding premium pricing that limits market accessibility. These technical constraints restrict proximity sensor applicability in approximately 15-20% of potential industrial automation applications, representing identifiable market opportunity limitations. Environmental resilience requirements mandate comprehensive testing protocols and certification processes that extend product development timelines and increase go-to-market costs for manufacturers targeting harsh-environment applications

Proximity Sensor Market Trends and Opportunities

Technological Convergence and Multi-Sensor Integration Platforms

The evolution toward integrated sensor platforms combining proximity detection with temperature measurement, pressure sensing, and environmental monitoring creates premium product opportunities and system-level solutions addressing customer consolidation preferences. Variable Distance proximity sensors, while representing 35% of current market share, demonstrate the fastest growth at 6.5% CAGR, reflecting customer preference for adaptive sensing capabilities. Advanced sensor fusion technologies enabling simultaneous multi-parameter monitoring reduce system complexity, enhance reliability, and create value-added service opportunities through data analytics and predictive maintenance platforms.

The convergence of sensor technologies with edge computing, artificial intelligence, and cloud connectivity enables intelligent automation solutions commanding premium pricing and generating recurring revenue streams through software and service components. This opportunity addresses growing customer preference for systems-level integration rather than discrete component procurement, creating differentiation opportunities for technology leaders.

Proximity Sensor Market Insights and Trends

Technology Insights

Technology Segmentation Highlights in Global Proximity Sensor Market Dynamics

Magnetic proximity sensors continue to hold a dominant leadership position, accounting for over 30% of total market revenue due to their robustness, cost efficiency, and reliability in harsh operating environments. Their widespread adoption across industrial automation and automotive applications is supported by mature manufacturing ecosystems, extensive standardization, and strong compatibility with legacy systems. However, with a CAGR of around 5.0–5.5%, their growth slightly trails the overall market, signaling gradual share dilution as advanced sensing technologies gain traction.

Infrared (IR) proximity sensors represent the fastest-growing technology segment, expanding at over 7.2% CAGR. Growth is fueled by rising demand for touchless solutions in building automation, consumer electronics, and advanced automotive interiors. Accelerated adoption during the COVID-19 pandemic created long-term structural demand, while ongoing improvements in miniaturization and temperature stability further strengthen IR sensors’ competitive positioning.

Capacitive proximity sensors address specialized detection needs, including non-metallic materials and liquid level sensing, capturing roughly 18–20% market share. Despite moderate growth of 5.2–5.8% CAGR, environmental sensitivity limits broader adoption, confining capacitive sensors largely to niche industrial applications.

Product Type Insights

Fixed Dominance Meets Rapid Growth in Proximity Sensor Technologies

The proximity sensor market demonstrates a clear contrast between mature, volume-driven adoption and innovation-led growth trajectories across product types. Fixed distance proximity sensors currently dominate the market, accounting for over 65% of total revenue, supported by their extensive use in standardized industrial automation, automotive systems, and building infrastructure with predefined sensing requirements. Their ability to detect object presence at calibrated distances enables easy integration, high reliability, and cost efficiency, making them ideal for conveyor systems, assembly lines, and safety applications. Strong standardization and manufacturing simplicity have, however, resulted in market saturation, commoditization, and moderate historical growth in the range of 4.7–5.2% CAGR, with demand largely sustained by replacement cycles and retrofit installations.

In contrast, variable distance proximity sensors represent the fastest-growing segment, expanding at approximately 6.5% CAGR. Their ability to perform continuous distance measurement supports advanced automation, adaptive control logic, and IoT-enabled analytics. Growing adoption in smart buildings, industrial process control, and advanced automotive applications such as automated parking and obstacle detection is accelerating demand. Despite premium pricing, enhanced functionality and margin potential are driving market share expansion toward 42–45% by 2033, reflecting a structural shift toward intelligent sensing platforms.

Industry Vertical Insights

Automotive Dominance and Automation Propel Proximity Sensor Market Growth

The global proximity sensor market is shaped by strong demand across automotive, industrial, and aerospace verticals, each contributing distinct growth dynamics. The automotive sector leads with over 40% of global revenue, acting as the primary growth catalyst. Rising vehicle electrification, autonomous driving development, and advanced safety system integration significantly expand sensor requirements. Proximity sensors are critical in EV battery management, power distribution, charging interfaces, and autonomous functions such as obstacle detection and lane positioning. With global vehicle production nearing 85 million units annually and EV penetration projected to exceed 50% by 2033, sensor demand is set to multiply. Automotive growth of nearly 6% CAGR outpaces overall market expansion.

Industrial and manufacturing applications represent the second-largest vertical and the fastest-growing, at around 6.7% CAGR. Industry 4.0 adoption, factory automation, robotics, and predictive maintenance drive extensive sensor deployment. Global automation spending exceeding US$180 billion, particularly in Asia-Pacific manufacturing hubs, reinforces growth momentum, supported by reshoring initiatives in North America and Europe.

Aerospace and defence account for 8–10% of revenue, focused on high-reliability, premium applications. Although volume growth is moderate, superior margins and technical complexity ensure strong strategic importance.

End User Insights

Farms dominate Proximity Sensor demand while turf management grows fastest globally

Commercial farming operations represent the dominant end-user segment in the Proximity Sensor market, accounting for over 65% of total revenue. Large-scale farms cultivating cereals, oilseeds, and legumes form the backbone of demand, as soil pH management is critical for maximizing nutrient availability, crop yields, and long-term soil health. Proximity Sensor is widely integrated into structured soil management and productivity optimization programs, particularly in regions with intensive farming practices. High awareness among farmers, supported by agronomic advisory services and on-field demonstrations, reinforces consistent adoption across commercial farms. In addition, the scale of application in farming—covering large acreage—ensures stable, recurring demand, making farms the most commercially significant end-user segment.

In contrast, lawns and turf management represent the fastest-growing end-user category, projected to expand at a CAGR of 6.7% between 2026 and 2033. This segment includes residential lawns, golf courses, sports complexes, and public green spaces. Growth is driven by rising adoption of precision lime application to achieve optimal soil pH, improved turf density, and enhanced visual appeal. Premium turf applications, particularly golf courses and professional sports facilities, increasingly demand specialized lime formulations and professional application services. Moreover, expanding housing markets and higher consumer spending on landscaping and property aesthetics are accelerating residential lawn care demand, especially in developed economies with established lawn care industries.

Regional Insights and Trends

North America Leads Proximity Sensor Market Through Innovation Ecosystem

North America represents a dominant and technologically advanced region within the global proximity sensor market, accounting for approximately 35% of total revenue. The region benefits from a mature manufacturing base, strong industrial automation adoption, and a globally influential automotive sector. The United States leads regional performance, supported by major OEMs such as Tesla, General Motors, and Ford, alongside rapid deployment of smart building and industrial automation technologies. North America’s proximity sensor market exceeded US$ 6.5 billion in 2026 and is projected to approach US$ 9.0–9.5 billion by 2033, expanding at a CAGR of around 5.2–5.8%, slightly above the global average.

Key growth drivers include rising EV penetration, autonomous vehicle R&D programs, and expanding commercial building automation. Regulatory mandates such as vehicle safety standards, emission norms, and energy efficiency codes further reinforce sensor adoption. Federal incentives under EV infrastructure and manufacturing programs provide long-term structural demand. The competitive landscape is led by technology-focused players including Honeywell, Rockwell Automation, and TE Connectivity. Robust R&D investment, strong venture funding, and strategic acquisitions highlight North America’s innovation-driven market leadership.

Asia-Pacific Emerges As Fastest-Growing Proximity Sensor Manufacturing Hub

Asia-Pacific accounts for nearly 32–35% of global proximity sensor revenue and represents the fastest-growing regional market, expanding at around 6.6% CAGR. This growth is underpinned by rapid manufacturing expansion, accelerating urbanization, and strong momentum in automotive electrification. China dominates the region, contributing approximately 55–60% of regional revenue, driven by its position as the world’s largest automotive manufacturing base and aggressive adoption of industrial automation and smart building technologies. Electric vehicles already represent over half of China’s vehicle output, creating significant demand for proximity sensors across powertrain, safety, and thermal management systems.

India and key ASEAN economies such as Vietnam, Thailand, and Indonesia form secondary growth engines. India’s proximity sensor demand is supported by electric two-wheeler electrification, commercial vehicle manufacturing, and expanding electronics production, reinforced by government-led manufacturing incentives. Across the region, building automation adoption is accelerating due to sustainability mandates, commercial infrastructure upgrades, and smart city development.

The competitive landscape reflects a mix of global leaders such as Siemens, ABB, and Honeywell alongside fast-growing regional manufacturers offering cost-optimized sensor solutions. Strategic partnerships, localized manufacturing, and rising R&D investments continue to strengthen Asia-Pacific’s role as both a demand center and global production hub.

Proximity Sensor Market Competitive Landscape

The proximity sensor market demonstrates moderately consolidated competitive structure with leading global technology companies commanding 45-50% of combined market share through technological capabilities, manufacturing scale, and established OEM relationships. Honeywell International, Siemens AG, TE Connectivity, and Rockwell Automation represent established market leaders with diversified sensor portfolios, comprehensive geographic distribution networks, and significant R&D investment capabilities. Mid-tier competitors including Sick AG, Baumer, and Pepperl+Fuchs maintain strong regional positions and specialized product portfolios addressing niche applications.

Market fragmentation in emerging markets reflects entry of regional manufacturers offering cost-optimized solutions and localized support services, creating competitive dynamics favoring volume manufacturers in price-sensitive segments. Vertical integration by automotive OEMs (Tesla, Volkswagen Group) toward captive sensor component manufacturing creates competitive intensity in automotive applications. Overall market structure reflects transition toward premium technology leadership among advanced providers combined with emerging competitive pressure from cost-optimized regional competitors.

Key Industry Developments

- On December 23, 2025, Elliptic Labs announced the commercial launch of its AI Virtual Proximity Sensor™ on vivo S50 and S50 Pro Mini smartphones. The solution replaces physical sensors with software-based intelligence, enabling bezel-free designs, lower bill-of-material costs, and improved reliability in next-generation smartphones.

- In October 2024, SICK AG deployed a next-generation capacitive sensing module for food and beverage automation. The new module features IP69K-rated protection, self-calibrating algorithms, and enhanced detection accuracy for liquid and granular materials in harsh industrial environments.

- In October 2024, JonDeTech Sensors AB announced the development and upcoming market launch of a new proximity sensor, scheduled for 2024. Designed to expand its existing portfolio, the product has already attracted strong interest from global partners and distributors.

- In February 2024, Panasonic enhanced its miniature IR proximity sensor lineup with faster response times and reduced power consumption, targeting smartphones, wearables, and smart home devices.

- In January 2024, Panasonic introduced the LUMIX S-E100 medium-telephoto macro lens, incorporating a high-precision manual focus sensor, a Dual Phase linear motor, and advanced optical design to support high-resolution imaging and precise autofocus performance.

Companies Covered in Proximity Sensor Market

- Torque Fitness

- Technogym

- Shandong EM Health Industry Group Co., Ltd.

- Precor Incorporated

- Nautilus, Inc.

- Life Fitness (KPS Capital)

- Johnson Health Tech

- Impulse Health Technology Co., Ltd.

- Icon Health & Fitness

- Core Health & Fitness

- Other Market Players

Frequently Asked Questions

The Proximity Sensor market is estimated to be valued at US$ 18.7 Bn in 2026.

The primary demand driver for the proximity sensor market is the rapid expansion of automation and smart sensing across automotive, industrial, and consumer electronics applications.

In 2026, the North America Pacific region will dominate the market with an exceeding 35% revenue share in the global Proximity Sensor market.

Among industry verticals, automotive has the highest preference, capturing beyond 40% of the market revenue share in 2026, surpassing other industry vertical.

Technogym, Shandong EM Health Industry Group Co., Ltd., Precor Incorporated, Nautilus, Inc., Life Fitness (KPS Capital), Johnson Health Tech, Impulse Health Technology Co., Ltd. There are a few leading players in the Proximity Sensor market.