- Non-food Packaging

- Presswood Pallets Market

Presswood Pallets Market Size, Share, and Growth Forecast, 2026 - 2033

Presswood Pallets Market by Product Type (Nestable/Stackable, Rackable, Others), Size (Full-size, Half-size, Others), End-user, and Regional Analysis for 2026 - 2033

Presswood Pallets Market Size and Trends Analysis

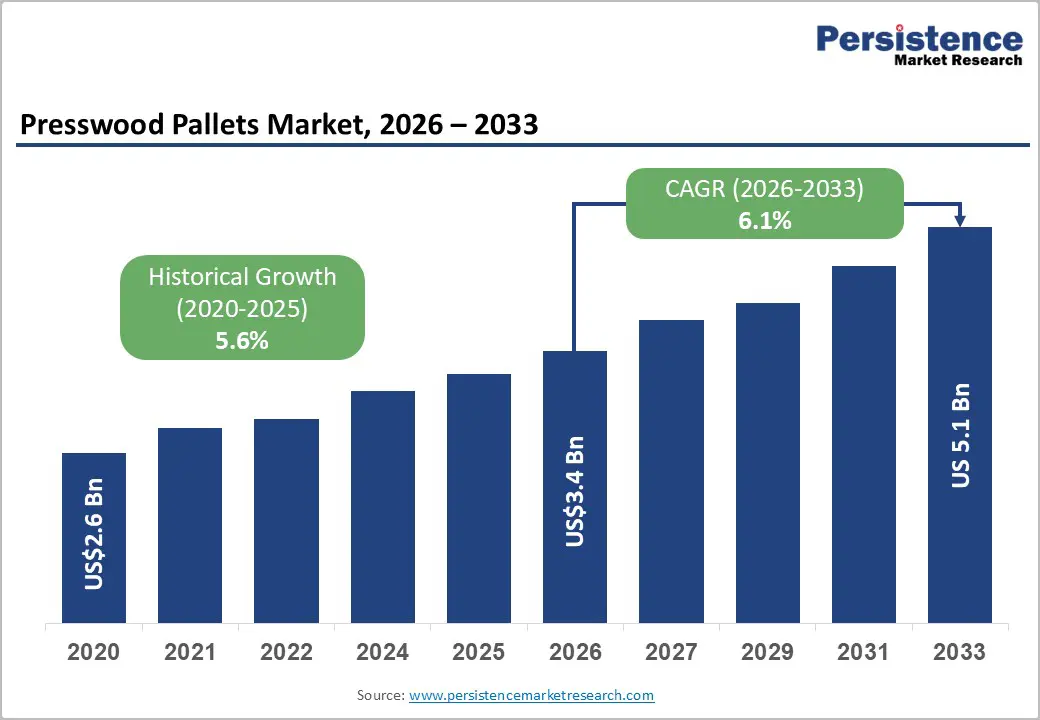

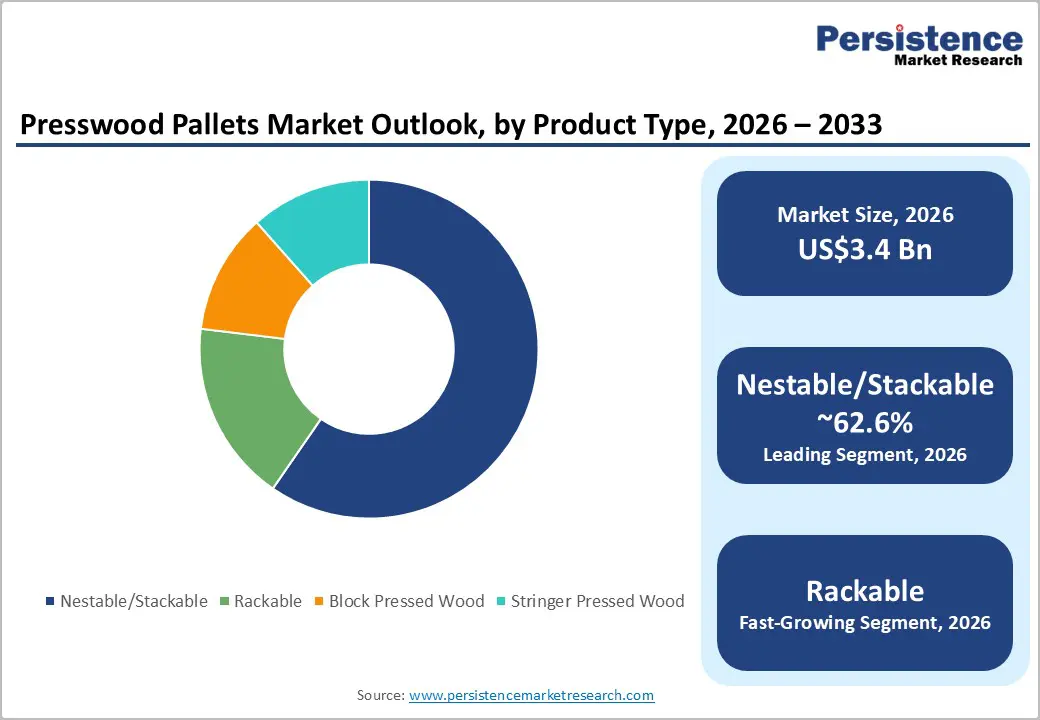

The global presswood pallets market size is likely to be valued at US$3.4 billion in 2026 and is expected to reach US$ 5.1 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033, driven by structural shifts in global logistics toward cost-optimized palletization, rising export activity requiring phytosanitary-compliant packaging, and corporate sustainability mandates favoring recycled wood fiber solutions.

Presswood pallets address these needs through nestable, lightweight designs manufactured from sawmill residues and recycled wood materials. While demand remains robust across export-intensive sectors, market performance is tempered by feedstock price volatility and competition from plastic and heat-treated solid-wood pallets.

Key Industry Highlights:

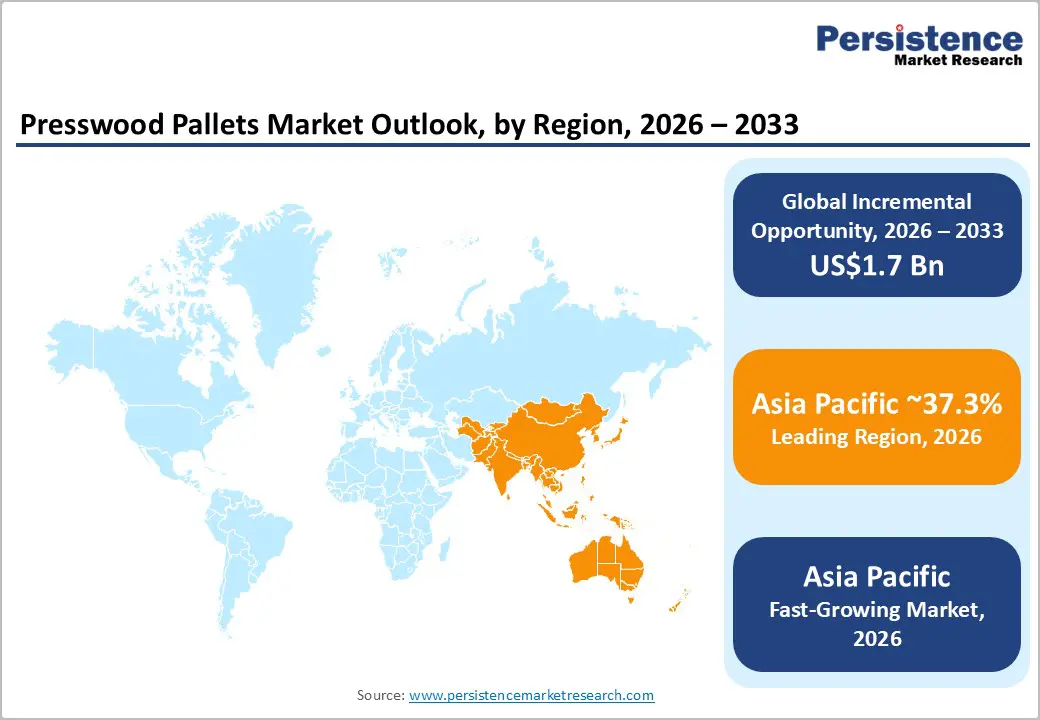

- Leading Region: Asia Pacific is projected to account for approximately 37.3% of the market, driven by strong export manufacturing bases in China and India, abundant feedstock availability, and rapid e-commerce-driven warehouse expansion.

- Fastest-growing Region: Asia Pacific is projected to register the highest CAGR, supported by automation investments, expanding fulfillment infrastructure, and rising palletization rates across organized retail and export sectors.

- Investment Plans: Ongoing capital allocation toward automated molding lines, reinforced rackable pallet development, feedstock supply partnerships, and recycling network expansion, particularly in North America and Europe, to meet ESG and circular economy targets.

- Dominant Product Type: Nestable/stackable presswood pallets are anticipated to hold 62.6% market share, supported by freight optimization benefits, lower reverse logistics costs, and strong adoption in one-way export applications.

- Leading Size: Full-size pallets are anticipated to account for 56.5% market share, aligned with ISO container standards, established warehouse racking systems, and high-volume retail distribution requirements.

| Key Insights | Details |

|---|---|

|

Presswood Pallets Market Size (2026E) |

US$3.4 Bn |

|

Market Value Forecast (2033F) |

US$5.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Cost & Logistics Economics

Presswood pallets offer measurable cost advantages in one-way and export logistics models. Their lighter weight and nestable configuration reduce freight volume, allowing more empty pallets to be transported per return load compared to conventional timber pallets. In high-turnover retail and FMCG distribution environments, logistics managers evaluate pallets based on “cost per trip,” freight optimization, and warehouse space efficiency. Nestable designs can reduce storage footprint requirements by more than half when empty, directly lowering transportation and warehousing costs. These operational efficiencies are particularly relevant for exporters shipping containerized cargo, where cubic optimization determines freight expense. As global trade flows continue expanding, procurement teams increasingly prioritize total landed cost over initial unit price, reinforcing steady adoption of presswood pallets.

Sustainability & Circular Feedstocks

Presswood pallets are manufactured from wood residues, shavings, and recycled fibers, and are compressed under heat and pressure. This production method aligns with circular economy objectives by diverting wood waste streams from disposal or low-value use. Large corporations in food & beverage, retail, and pharmaceuticals now incorporate sustainability performance into supplier scorecards, often weighting environmental criteria alongside cost and quality.

Presswood pallets typically utilize post-industrial wood fiber rather than virgin lumber; they help companies demonstrate reduced dependency on newly harvested timber. Their splinter-free design also reduces workplace hazards and contamination risks in hygienic environments. Sustainability-driven procurement policies increasingly favor such materials, contributing to incremental demand growth across multinational supply chains.

Export Compliance & Phytosanitary Advantage

International trade regulations governing wood packaging materials require phytosanitary treatment to prevent the spread of pests. Molded presswood pallets are manufactured under high heat and pressure, which eliminates pests during production. As a result, they are widely accepted as compliant with international phytosanitary requirements without the need for additional fumigation or heat-treatment stamping procedures. For exporters, avoiding additional compliance steps reduces paperwork, inspection delays, and associated port-of-entry costs.

In industries such as food processing, automotive components, and consumer electronics, shipment reliability and customs clearance efficiency are critical performance indicators. Presswood pallets offer a lower-friction compliance pathway, strengthening their value proposition in global trade corridors.

Barrier Analysis - Feedstock & Input Cost Volatility

Presswood production depends on consistent access to wood residues and fiber by-products. Competing industries such as biomass energy, particleboard, and wood pellet manufacturing can drive up raw material prices. In regions where sawmill activity declines or biomass demand rises, feedstock shortages may elevate production costs. Transportation distance between raw material sources and molding facilities also influences cost structure. When feedstock must be transported beyond economically viable radii, margins compress. Manufacturers mitigate this risk through regional sourcing agreements or vertical integration strategies, yet volatility remains a structural constraint.

Performance Limitations in Heavy-Duty Applications

Although presswood pallets are engineered to meet defined load specifications, they may not match the durability and repairability of solid hardwood or injection-molded plastic pallets in high-cycle pooling environments. Heavy static loads in deep racking systems or extreme cold-storage conditions can exceed the performance thresholds of standard presswood models. In industries requiring multi-year reuse cycles or very high load-bearing capacity, customers may prefer rackable hardwood or reinforced plastic solutions. This limits presswood adoption primarily to export, light-to-medium-duty warehousing, and limited reuse scenarios unless reinforced designs justify the higher costs.

Opportunity Analysis - Automation-Compatible Product Innovation

Warehouse automation and automated storage and retrieval systems (AS/RS) require pallets with consistent dimensional tolerances. Presswood molding processes can produce standardized units with minimal variation, making them suitable for conveyor systems and robotic handling. Manufacturers that certify dimensional stability and load ratings for automated environments can secure long-term contracts with third-party logistics providers and e-commerce fulfillment centers. Automation-driven demand supports premium product tiers, particularly rackable presswood designs optimized for selective racking.

Regional Manufacturing Expansion in Emerging Markets

Establishing production facilities near sawmills and agro-residue sources in Southeast Asia, India, and parts of Latin America reduces transportation costs and improves feedstock security. These regions experience rising export volumes in consumer goods and industrial products, generating sustained pallet demand. Capturing even a modest share of pallet consumption in large emerging economies can create scalable revenue streams for domestic manufacturers. Regional capacity expansion also shortens delivery cycles and strengthens competitiveness against imported pallet alternatives.

Recovery & Recycling Service Models

Presswood pallets are less repairable than traditional timber pallets, creating an opportunity for structured recovery and recycling programs. Suppliers can offer take-back services that collect used pallets for grinding into biomass or board feedstock. Bundled service contracts lower disposal costs for customers and support sustainability reporting objectives. Managed recovery systems differentiate suppliers in competitive bids and enable recurring revenue beyond pallet sales. As environmental compliance expectations rise, integrated recycling solutions may become a standard procurement requirement.

Category-wise Analysis

Product Type Insights

Nestable/Stackable presswood pallets are expected to hold 62.6% market share in 2026, driven by their space-saving geometry and freight-optimization advantages. When empty, these pallets can be nested within one another, reducing storage volume by up to 60–70% compared to traditional block pallets. This capability directly lowers reverse logistics expenses and warehouse footprint requirements, particularly for export-oriented supply chains. Mass-market retailers, beverage distributors, and export manufacturers prefer nestable models for one-way or limited reuse applications.

Companies such as The Coca-Cola Company and Nestlé S.A. rely on lightweight pallet formats for high-volume cross-border distribution, where phytosanitary compliance and freight efficiency are critical. The lightweight structure simplifies manual handling in distribution centers and reduces injury risk. Their compatibility with automated stretch-wrapping and containerized shipping further strengthens their value proposition, sustaining segment leadership.

Rackable presswood pallets are projected to register the highest growth rate as warehouse infrastructure modernizes and automation adoption accelerates. Selective racking systems require pallets engineered to support defined beam spans and dynamic loads. Advances in reinforced ribbing, composite inserts, and structural density optimization have expanded rackable product offerings, enabling higher load-bearing performance comparable to conventional wooden block pallets.

The rapid expansion of e-commerce fulfillment networks operated by firms such as Amazon and third-party logistics providers such as DHL Supply Chain is increasing demand for pallets compatible with racking and conveyor-based automation systems. Rackable designs extend the applicability of presswood beyond one-way export flows into managed warehouse environments. This transition supports higher margins, repeat procurement contracts, and integration into closed-loop pallet management systems.

Size Insights

Full-size pallets remain the industry standard across global supply chains and are anticipated to account for 56.5% of market share in 2026. Standard dimensions, such as 1200 mm × 1000 mm and 48 in × 40 in, align with ISO container loading specifications, warehouse racking systems, and forklift equipment. Presswood pallets in full-size formats directly replace conventional wooden pallets in export and domestic distribution without requiring material-handling modifications.

High-volume sectors, including consumer packaged goods, electronics, and retail distribution, rely on standardized pallet footprints for operational continuity. Major global retailers such as Walmart and Carrefour maintain strict pallet dimension requirements to ensure compatibility with automated sorting and replenishment systems. The dominance of established logistics infrastructure and standardized handling protocols ensures continued preference for full-size pallets.

Half-size pallets are gaining momentum as last-mile logistics and retail-ready display solutions become more prominent. With footprints typically half that of standard pallets, they improve maneuverability in urban warehouses, compact retail outlets, and micro-fulfillment centers. Their lighter loads also reduce strain on manual handling operations. Convenience store chains and quick-commerce operators increasingly favor smaller load units that reduce replenishment time and minimize in-store restocking disruption.

The rise of urban distribution hubs and omnichannel retail models, supported by companies such as Reliance Retail, is accelerating adoption. As urbanization intensifies and e-commerce penetration deepens, half-size pallets are projected to record the strongest growth within the size segment, particularly in densely populated metropolitan markets.

Regional Insights

North America Presswood Pallets Market Trends - Export-Driven ISPM-15 Compliance and Automation-Compatible Recycled Fiber Pallet Adoption

North America represents a mature yet steadily expanding presswood pallets market, anchored by export-oriented industries and highly consolidated retail distribution networks. The U.S. leads regional demand due to its extensive warehousing infrastructure, advanced material-handling systems, and high pallet circulation volumes. Major logistics corridors linked to ports such as Los Angeles, Long Beach, and Savannah support strong demand for ISPM-15–compliant molded fiber pallets that eliminate heat-treatment requirements for export shipments.

Corporate sustainability commitments continue to accelerate the adoption of recycled-fiber pallet solutions. Retail giants, including Walmart, have expanded supplier sustainability scorecards, encouraging packaging and pallet optimization to reduce Scope 3 emissions. Similarly, Amazon has invested heavily in robotics-enabled fulfillment centers across the U.S., increasing demand for pallets compatible with automated storage and retrieval systems (AS/RS). This shift supports higher uptake of reinforced and rackable presswood designs engineered for dimensional consistency.

On the manufacturing side, Litco International continues to expand its Inca-brand molded wood pallet distribution network in North America, strengthening domestic supply capacity. Private equity participation in pallet pooling and recycling companies has also increased, reflecting predictable demand patterns and recurring procurement contracts tied to consumer goods distribution. Producers emphasize traceable sourcing of raw materials from sawmill residues and post-industrial wood fiber, aligning with ESG reporting requirements across food, beverage, and pharmaceutical supply chains.

Europe Presswood Pallets Market Trends - EU Circular Economy Mandates and Lightweight Nestable Pallet Standardization

Europe maintains strong demand for presswood pallets, supported by stringent environmental regulations and high export intensity across food processing, beverages, pharmaceuticals, and consumer goods. Core markets include Germany, the U.K., France, Spain, and Italy. The region’s emphasis on circular economy principles under EU Green Deal initiatives encourages the substitution of virgin timber pallets with recycled-molded-fiber alternatives.

Regulatory alignment with the EU Waste Framework Directive and packaging waste targets incentivizes manufacturers to integrate secondary wood residues into pallet production. Companies such as Palletower have expanded molded pallet offerings in response to retailer and exporter demand for lightweight, nestable solutions that reduce return freight costs. In Germany, automation-intensive distribution hubs operated by retailers such as Lidl and Aldi reinforce the need for standardized, dimensionally stable pallets compatible with high-bay racking systems.

Eastern Europe is emerging as a competitive production base. Poland and Romania, in particular, benefit from access to wood-processing residues and comparatively lower labor costs. Several Western European pallet suppliers have expanded manufacturing or sourcing partnerships in these markets to optimize cost structures while maintaining compliance with EU sustainability standards. Investment across the region focuses on upgrading molding presses, improving moisture control systems, and enhancing recovery logistics networks to strengthen circular material flows.

Asia Pacific Presswood Pallets Market Trends - Export Manufacturing Scale and E-Commerce-Led Warehouse Modernization Expansion

Asia Pacific is projected to account for approximately 37.3% of the market share in 2026 and represents the fastest-growing regional segment. The region’s growth trajectory is underpinned by expanding export manufacturing, rapid e-commerce penetration, and ongoing warehouse modernization across China, India, Japan, South Korea, and ASEAN economies. China remains the dominant production and consumption hub, supported by abundant sawmill residues and integrated wood-processing clusters.

Manufacturers supply both domestic exporters and multinational companies operating regional supply chains. E-commerce expansion led by Alibaba Group has significantly increased demand for standardized pallet solutions within automated fulfillment networks.

In India, logistics reforms linked to GST implementation and infrastructure investment have improved the efficiency of inter-state goods movement. Organized retail growth, driven by players such as Reliance Retail, supports rising palletization rates in consumer goods distribution. Japan and South Korea, characterized by high automation density in warehousing, are encouraging greater adoption of rackable molded pallets designed for precision handling systems.

Regional manufacturers continue to expand molding capacity and strengthen quality control systems to meet export specifications required by North American and European buyers. Competitive feedstock access, combined with export-oriented industrialization, positions the Asia Pacific as both a production powerhouse and a high-growth consumption market within the global presswood pallets industry.

Competitive Landscape

The global presswood pallets market is moderately fragmented, with numerous regional producers operating alongside established branded suppliers. Commodity pricing pressures characterize high-volume segments, while differentiation arises from certifications, automation compatibility, and recycling service offerings. Consolidation remains limited compared to plastic pallet pooling markets.

Market leaders emphasize cost-efficient feedstock sourcing, automation-ready product design, and integrated recycling programs. Regional expansion and selective reinforcement technologies support differentiation in competitive bids.

Key Industry Developments

- In April 2025, PalletsBiz completed delivery and commissioning of a fully automated presswood pallet production line, including robotic handling and automatic feeding systems, for a Southeast Asian logistics producer, enhancing productivity and enabling scalable output of diverse pallet types for global supply chains.

Companies Covered in Presswood Pallets Market

- Litco International

- Palletower

- Millwood Inc.

- Brambles Limited

- CABKA Group

- CHEP

- PECO Pallet

- Loscam

- Faber Halbertsma Group

- Craemer Group

- Presswood International B.V.

- ENNO Marketing Ltd.

- PalletOne

- UFP Packaging

- Scott Group

- Rehrig Pacific Company

- IPL Plastics

- ORBIS Corporation

Frequently Asked Questions

The global presswood pallets market is valued at US$3.4 billion in 2026.

The presswood pallets market is projected to reach US$5.1 billion by 2033.

The presswood pallets market is expected to grow at a CAGR of 6.1% between 2026 and 2033.

Nestable/stackable pallets lead by product type with an anticipated 62.6% market share. Full-size pallets dominate by size with an anticipated 56.5% share.

Major players include Litco International, Palletower, Millwood Inc., Brambles Limited, and CABKA Group.