- Home Care & Utilities

- Pottery Ceramics Market

Pottery Ceramics Market Size, Share, and Growth Forecast, 2025 - 2032

Pottery Ceramics Market By Product Type (Tableware, Artware), Material Type (Earthenware, Stoneware), End-use, Distribution Channel, and Regional Analysis for 2025 - 2032

Pottery Ceramics Market Size and Trends Analysis

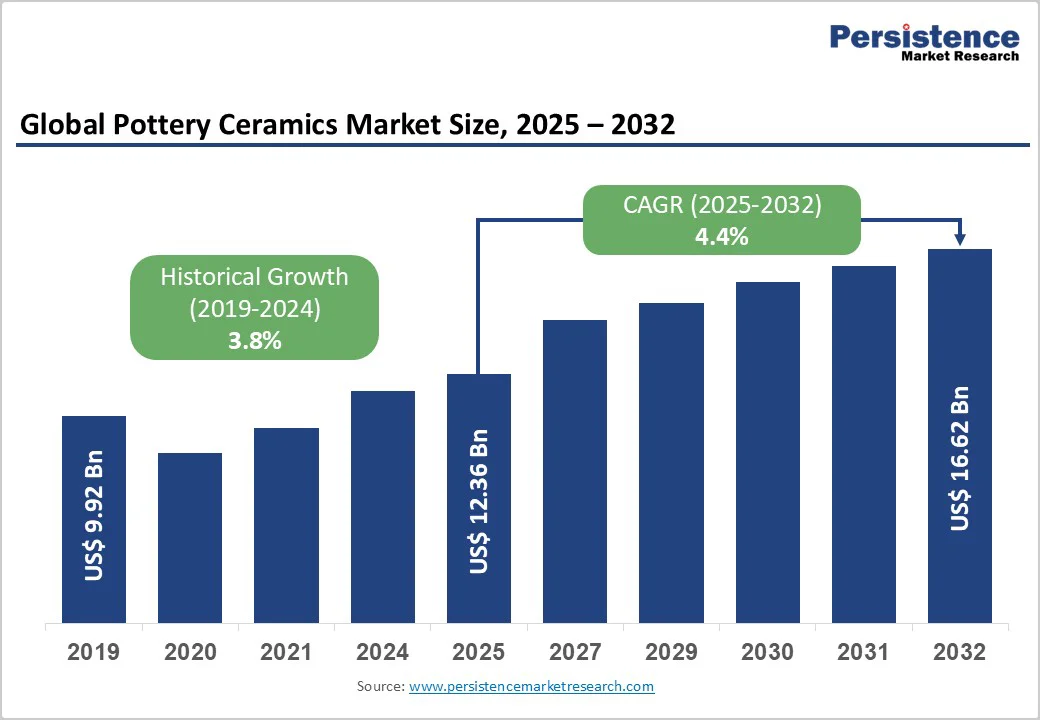

The global pottery ceramics market size was valued at US$12.36 Billion in 2025 and is projected to reach US$16.62 Billion by 2032, growing at a CAGR of 4.4% between 2025 and 2032, driven by strong demand from the hospitality industry, rising consumer spending on premium tableware, and the expansion of e-commerce channels.

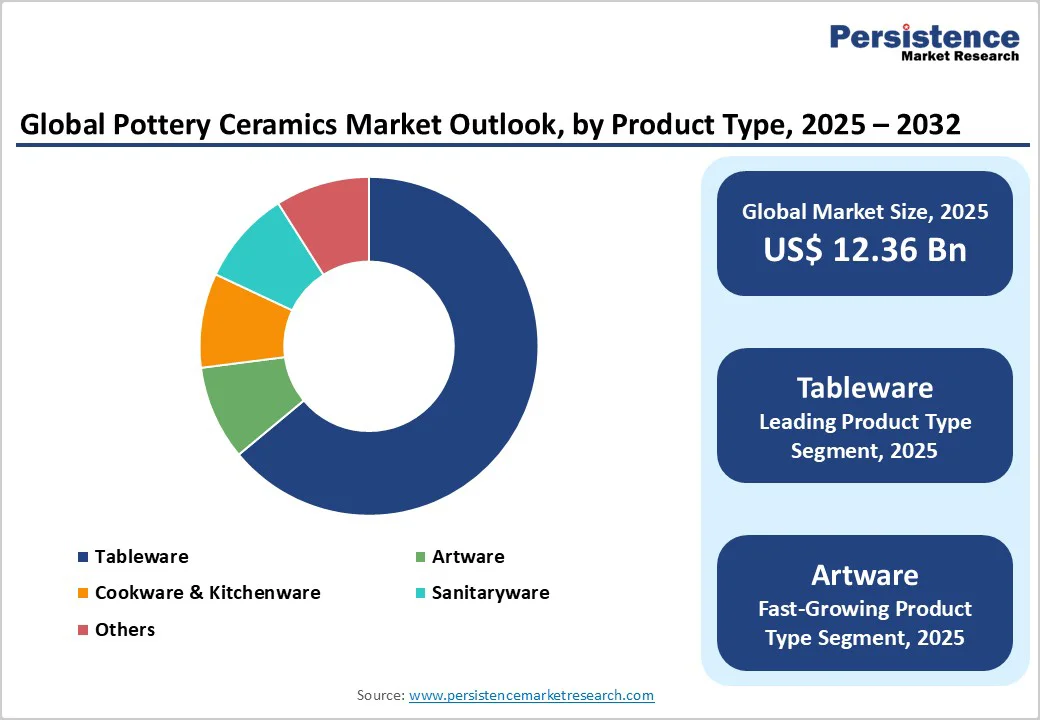

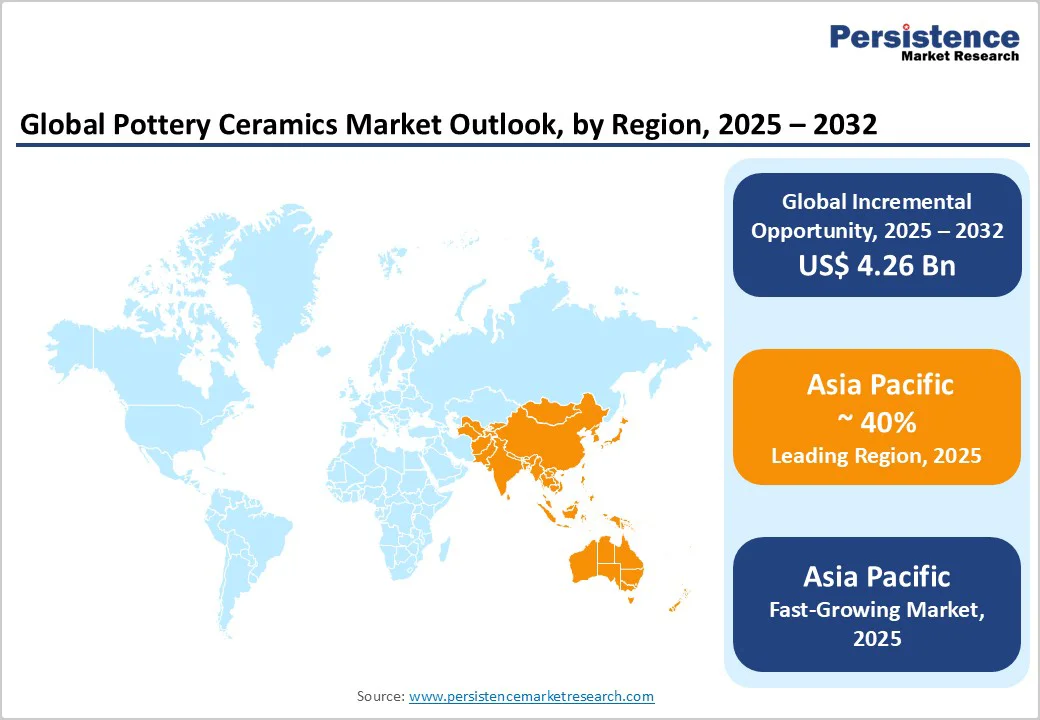

Tableware leads the market, capturing nearly 75% of sales in 2024, while artware gains traction in higher-margin segments. Asia Pacific dominates, accounting for over 40% of global revenue, driven by strong manufacturing and growing middle-class demand.

Key Industry Highlights

- Leading Region: Asia Pacific, accounting for over 40% of global revenues in 2025, supported by China’s large-scale production and rising domestic consumption.

- Fastest-growing Region: Asia Pacific, driven by India’s urbanization and export-oriented investments across China and ASEAN.

- Investment Plans: Significant investments are directed toward kiln modernization, eco-friendly production technologies, and e-commerce expansion, with companies such as RAK Ceramics and East Fork enhancing capacity and digital reach post-2023.

- Dominant Product Type: Tableware, representing about 71% of global revenues in 2025, driven by recurring household demand and large-scale procurement from the hospitality sector.

- Leading End-user Category: Residential, contributing 59% of global demand, fueled by household replacement cycles, festive gifting, and growing premium lifestyle adoption.

| Key Insights | Details |

|---|---|

| Pottery Ceramics Market Size (2025E) | US$12.36 Bn |

| Market Value Forecast (2032F) | US$16.62 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Hospitality and Refurbishment Cycle

Investments in hotels, restaurants, and residential renovations represent a major growth engine for pottery ceramics. Hospitality operators increasingly rely on premium ceramic tableware and artware to enhance dining aesthetics and guest experiences.

Large-scale procurement contracts for hotels and restaurants create bulk demand, providing manufacturers with recurring and stable revenue streams. Renovation cycles in the commercial sector also support high-volume orders, strengthening both demand stability and profitability.

E-commerce and Premiumization

The rise of online retail and direct-to-consumer brands has significantly expanded market reach. Digital channels make it easier for consumers to access artisanal and branded ceramics, boosting both product variety and premium positioning.

Manufacturers benefit from lower distribution costs and real-time customer data, enabling better pricing strategies and SKU optimization. This has encouraged higher average selling prices, especially in premium tableware and limited-edition artware.

Sustainability and Artisanal Revival

Consumers are increasingly drawn to sustainable, eco-friendly, and handcrafted ceramics. Products made with recycled clay, lead-free glazes, or energy-efficient kiln processes are gaining traction. Artisanal pottery with strong local or cultural identity resonates with design-conscious buyers in both residential and commercial segments. This trend supports differentiation, higher margins, and new growth niches, particularly in boutique hospitality and premium residential projects.

Barrier Analysis - Substitution from Alternative Materials

Plastic, metal, and tempered glass products pose a threat to pottery ceramics, particularly in cost-sensitive sectors such as institutional food services. These substitutes are valued for durability and lower replacement costs, reducing ceramics’ competitiveness in budget-conscious markets. This substitution risk limits the market’s ability to capture certain large-volume, low-margin procurement segments.

Raw Material and Energy Cost Volatility

Clay, feldspar, and kaolin, along with energy-intensive kiln firing, represent significant production costs. Volatility in raw material prices and energy supply can compress margins, especially for small-scale or artisanal producers. Regulatory tariffs on imports and exports further complicate cost structures. Larger manufacturers often mitigate these risks through vertical integration and investments in efficient kiln technologies.

Opportunity Analysis - Premium Hospitality and Contract Channels

Upscale hotels, luxury restaurants, and design-led commercial spaces are increasingly procuring custom tableware and artware. These contracts deliver high-value, repeat orders, with strong potential for brand exposure. The global expansion of premium hospitality chains offers manufacturers an opportunity to grow revenues through tailored, durable, and high-quality ceramic solutions.

Emerging Markets and Localized Manufacturing

Countries such as India, China, and those in Latin America are experiencing rising disposable incomes and a greater appetite for premium ceramics. Establishing localized manufacturing hubs reduces transportation costs and provides faster delivery times. These markets also serve as cost-effective bases for exports, helping manufacturers tap into both domestic growth and international opportunities.

Category-wise Analysis

Product Type Insights

Tableware continues to dominate the pottery ceramics market, accounting for roughly 71% of global revenues in 2025. The segment benefits from both everyday household consumption and bulk demand from the hospitality sector. Growing consumer inclination toward formal dining and premium kitchenware has fueled sales in developed economies, while gifting culture and festive purchases sustain volumes in Asia and the Middle East.

Replacement cycles for chipped or outdated sets ensure recurring purchases. Recent launches, such as Denby’s eco-friendly “Everyday Stoneware” range in 2024, illustrate how brands are combining sustainability with practicality to attract households and hospitality clients alike.

Artware, which includes decorative vases, sculptures, wall-mounted ceramics, and customized design-led products, is projected to record the fastest CAGR through 2032. Growing consumer interest in interior design, boutique hospitality aesthetics, and lifestyle-driven residential décor has increased demand for artisanal and high-value pieces.

Collaborations between manufacturers and designers are driving innovation; for instance, Rosenthal partnered with internationally renowned artists in 2024 to release limited-edition collectible pottery lines. These art-led collections command premium margins and appeal to niche but growing audiences in Europe, North America, and urban Asia. This trend positions artware as a dynamic growth frontier within the industry.

Material Type Insights

Earthenware remains the leading material type with a market share of 38% due to its affordability, versatility, and wide global availability. It is especially popular in emerging economies such as India, Indonesia, and Mexico, where consumer price sensitivity drives adoption. Its rustic finish also resonates with casual dining trends, farm-to-table restaurants, and mid-range households.

Localized production capabilities allow manufacturers to scale at lower costs, maintaining their dominance in mainstream markets. In 2023, India-based Clay Craft expanded its earthenware production lines to target mid-tier households, reflecting the material’s continued popularity in cost-conscious yet design-sensitive segments.

Porcelain and high-fired stoneware are registering the highest growth rates, particularly within premium and export-oriented markets. These materials are prized for their durability, translucence, and suitability for both fine dining and luxury hospitality. The adoption is rising in developed economies such as the U.S., Japan, and Germany, where hotels and households favor long-lasting, high-quality ceramics.

In 2024, Villeroy & Boch expanded its porcelain product line with a contemporary “Signature Dining Collection,” tailored to high-end restaurants and premium households. Their rising share reflects a shift toward premiumization, supported by consumers’ willingness to invest in long-lasting products that align with luxury dining experiences.

End-user Insights

Residential applications continue to account for the majority share, estimated at 59% of global demand in 2025. Rising disposable incomes in emerging markets, particularly in China, India, and Brazil, are fueling demand for quality ceramics in households. Consumers are increasingly replacing mass-market items with durable, design-oriented products.

The gifting culture around weddings and festive occasions, especially in Asia, also supports consistent volumes. A notable example includes Portmeirion Group’s 2024 launch of a premium “Festive Gifting Range,” which targeted holiday-season demand across the U.K. and North America. Such initiatives underline the resilience of residential demand across demographics.

The commercial segment, driven by hotels, restaurants, cafes, and institutional dining, is projected to grow at the fastest pace through 2032. Large-scale procurement contracts ensure high-volume orders, while regular refurbishment cycles in the hospitality sector provide recurring demand. This end-use also emphasizes compliance with durability standards, aesthetic appeal, and food safety regulations.

In 2024, RAK Porcelain secured a multi-year supply deal with a European luxury hotel chain, highlighting the strong growth potential of this channel. Commercial buyers increasingly favor branded, certified, and customizable products, making this segment a lucrative target for manufacturers focusing on premium ceramics.

Regional Insights

North America Pottery Ceramics Market Trends - Rising Demand for Artisanal Ceramics and Sustainable D2C Expansion

North America represents a mature yet lucrative market. The U.S. remains the largest consumer, driven by high household replacement cycles and rising premium hospitality projects. Consumers in this region exhibit strong demand for custom-designed and artisanal products, often favoring domestic brands such as Heath Ceramics and East Fork.

Regulatory oversight, particularly FDA restrictions on lead and cadmium levels in ceramics, makes certification an important competitive differentiator. Online distribution is highly penetrated, with brands increasingly selling directly via D2C channels. In 2024, East Fork Pottery announced the expansion of its e-commerce platform to Canada, strengthening regional accessibility. Investment flows are focused on sustainable production technologies and new collaborations with designers to align with changing lifestyle preferences.

Europe Pottery Ceramics Market Trends - Heritage-Driven Demand Meets Sustainability-Focused Innovation

Europe is supported by its reputation for craftsmanship and design sophistication. Germany, the U.K., France, Italy, and Spain remain key markets, with heritage brands such as Rosenthal, Wedgwood, and Royal Doulton driving demand. European consumers prioritize provenance, craftsmanship, and sustainable production, pushing manufacturers toward eco-friendly materials and energy-efficient kilns.

The European Union enforces strict regulations on migration limits for lead and cadmium in ceramics for food use, requiring supplier certifications and regular audits. Recent developments include Rosenthal’s 2024 launch of its “Designer Edition Series,” which combined modern artistry with traditional porcelain craftsmanship. Investments across Europe increasingly emphasize collaborations with artists and sustainability-driven production upgrades, strengthening its premium positioning in the global market.

Asia Pacific Pottery Ceramics Market Trends - Global Manufacturing Powerhouse with Growing Premium Demand

Asia Pacific dominates the global market with over 40% revenue share in 2025, supported by its strong manufacturing base and expanding middle-class consumption. China leads both as the largest producer and a key consumer, exporting large volumes globally while witnessing rising domestic demand for premium tableware. India is emerging as a growth hotspot, with increasing urbanization and gifting traditions boosting sales.

Japan continues to play a significant role in premium markets, with brands such as Noritake maintaining global prestige. Investments focus heavily on the modernization of kilns and export-oriented production. In 2024, RAK Ceramics expanded its production footprint in India to meet growing regional demand and serve as an export hub. The region’s competitive advantage lies in abundant raw material availability, cost-effective labor, and increasing domestic appetite for high-quality ceramics.

Competitive Landscape

The global pottery ceramics market is moderately fragmented, with global leaders competing alongside regional producers and artisanal studios. Large players such as RAK Ceramics, Villeroy & Boch, and Noritake maintain strong brand equity and economies of scale, while smaller firms thrive in niche and design-led markets.

Competition increasingly centers on product innovation, compliance certification, and digital distribution. Market leaders focus on premiumization, sustainability, and digital channel expansion. Key differentiators include design collaborations, product certifications, and vertically integrated production models.

Key Industry Highlights

- In February 2025, Villeroy & Boch introduced its Signature Dining Collection in Germany, blending contemporary aesthetics with durable porcelain to target the hospitality sector.

- In January 2024, Denby Pottery launched its Everyday Stoneware Collection made from recycled clay and low-energy firing processes, strengthening its sustainability positioning in Europe.

Companies Covered in Pottery Ceramics Market

- Villeroy & Boch

- RAK Ceramics

- Rosenthal GmbH

- Wedgwood

- Denby Pottery

- Royal Doulton

- Noritake Co., Ltd.

- Portmeirion Group

- Heath Ceramics

- East Fork Pottery

- Clay Craft India Pvt. Ltd.

- Fiesta Tableware Company

- Churchill China plc

- Meyer Corporation

- Lenox Corporation

- Narumi China Corporation

- Homer Laughlin China Company

- Apulum S.A.

- Guangxi Sanhuan Enterprise Group

- Herend Porcelain Manufactory

Frequently Asked Questions

The pottery ceramics market size is estimated at US$12.36 Billion in 2025.

The pottery ceramics market is projected to reach US$16.57 Billion by 2032, growing at a CAGR of 4.4% between 2025 and 2032.

The key trends are the rising demand for premium tableware and artware in residential and commercial sectors, and the growth of e-commerce and D2C channels, expanding market reach.

Tableware is the leading product segment, accounting for approximately 71% of global revenues in 2025, driven by household usage and hospitality procurement.

The market is projected to grow at a CAGR of 4.4% from 2025 to 2032.

Key players include Villeroy & Boch, RAK Ceramics, Rosenthal GmbH, Noritake Co., Ltd., and Wedgwood.