- Medical Devices

- Positron Emission Tomography Imaging Market

Positron Emission Tomography Imaging Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Positron Emission Tomography Imaging Market by Product (Full-Ring PET Scanners, and Partial Ring PET Scanners), by Application (Oncology, Neurology, Cardiology, and Others) by End-user (Hospitals, Ambulatory Surgery Centers, Diagnostic Imaging Centers, and Others), and Regional Analysis from 2026 to 2033

Positron Emission Tomography Imaging Market Share and Trends Analysis

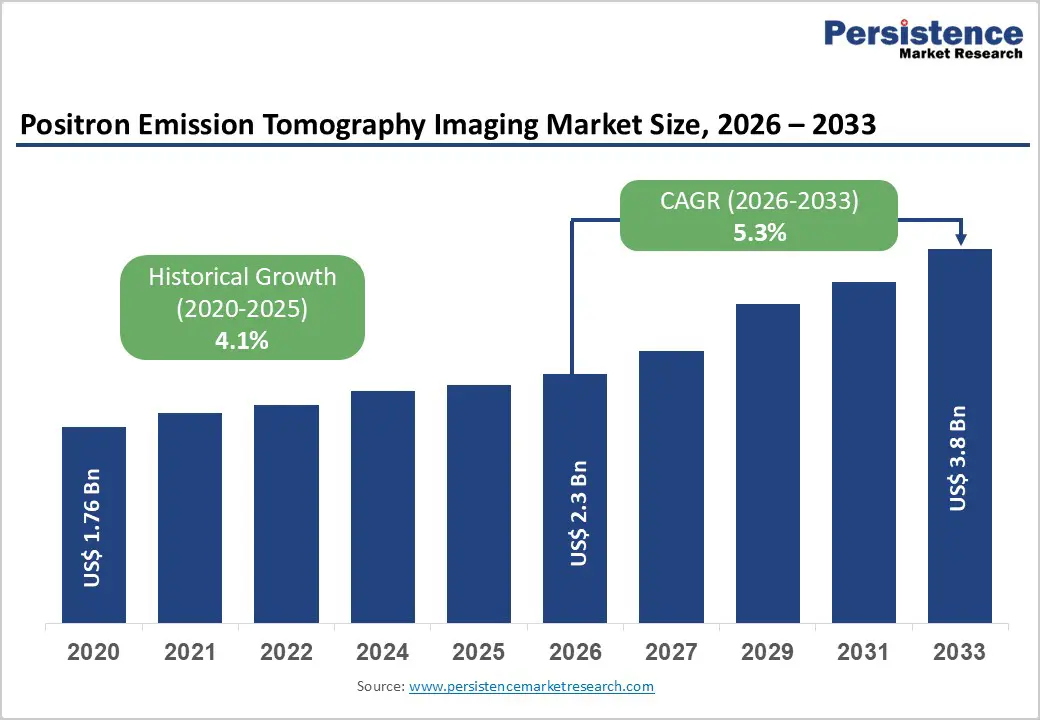

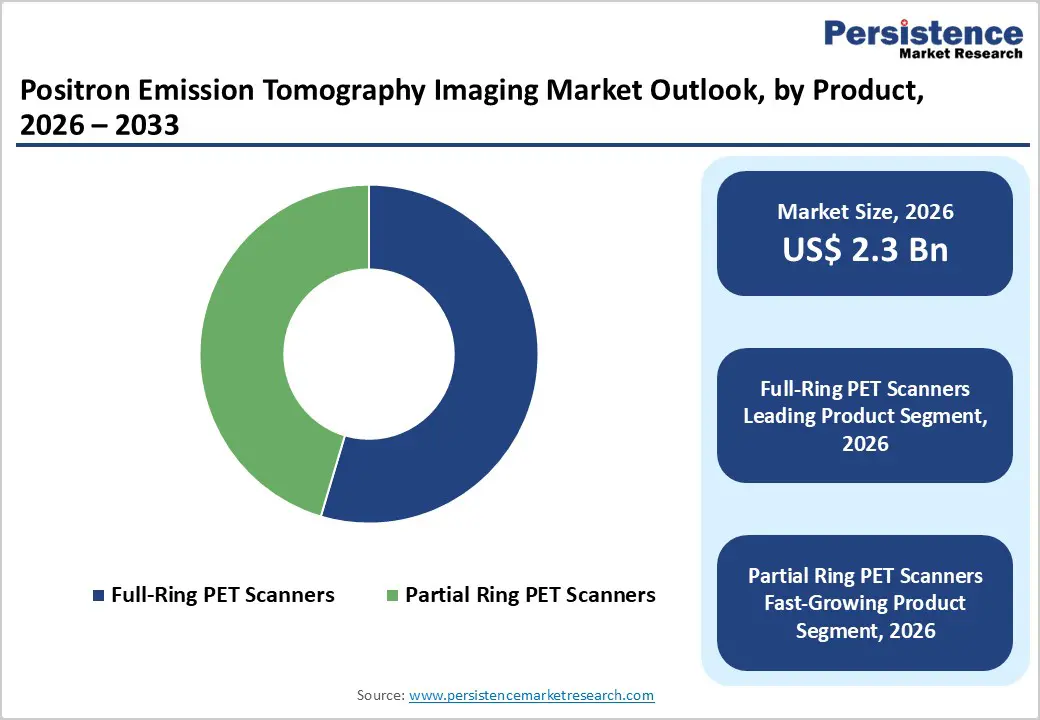

The global positron emission tomography imaging market size is estimated to grow from US$ 2.3 billion in 2026 to US$ 3.8 billion by 2033. The market is projected to grow at a CAGR of 5.3% from 2026 to 2033.

Global demand for positron emission tomography (PET) imaging is increasing steadily, driven by the rising prevalence of cancer, neurological disorders, and cardiovascular diseases, along with growing demand for early and accurate disease diagnosis. The increasing adoption of minimally invasive diagnostic procedures, the expanding clinical applications of molecular imaging, and greater awareness among clinicians regarding precision diagnostics are supporting sustained market growth. Higher volumes of oncology diagnostics, treatment monitoring, and therapy response assessments, coupled with rising healthcare expenditure and improved reimbursement frameworks in developed markets, are further accelerating PET adoption. The expansion of hospitals, diagnostic imaging centers, and academic research institutions is strengthening demand for advanced PET systems. Continuous innovation in detector technologies, time-of-flight imaging, AI-enabled reconstruction, and hybrid PET/CT and PET/MRI systems is improving image quality, reducing scan times, and enhancing diagnostic confidence. Additionally, the growing focus on personalized medicine, increasing availability of novel radiotracers, and broader acceptance of advanced imaging workflows are further propelling growth in the global market.

Key Industry Highlights:

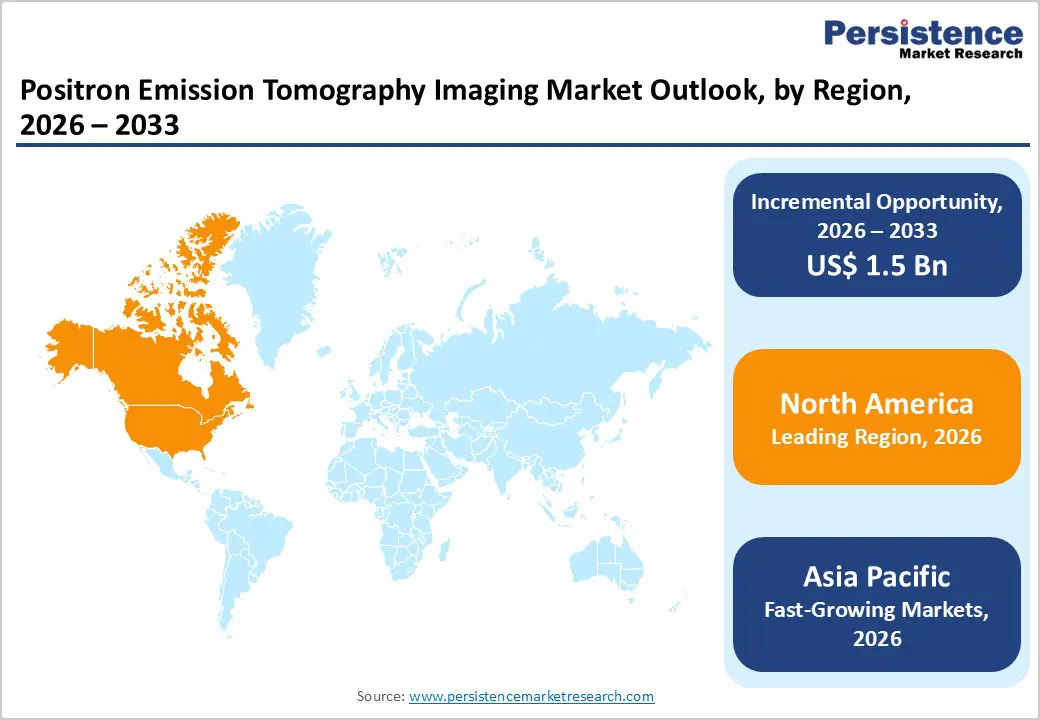

- Leading Region: North America accounts for the largest market share at approximately 47.5%, supported by advanced healthcare infrastructure, high diagnostic imaging volumes, favorable reimbursement policies, and early adoption of innovative PET technologies.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by a large patient population, rising cancer incidence, expanding diagnostic imaging infrastructure, increasing healthcare investments, and improving access to advanced imaging modalities.

- Leading Product Segment: Full-ring PET scanners dominate the market due to their superior sensitivity, whole-body imaging capability, higher image resolution, and widespread use in oncology and multi-disciplinary clinical settings.

- Fastest-Growing Product Segment: Partial-ring PET scanners are expanding rapidly as cost-effective alternatives, particularly in outpatient diagnostic centers and in emerging markets seeking compact systems with acceptable performance.

- Leading Application Segment: Oncology remains the largest application segment, supported by PET’s critical role in cancer detection, staging, treatment planning, and therapy monitoring.

- Fastest-Growing Application Segment: Neurology is witnessing the fastest growth, driven by the increasing prevalence of neurodegenerative disorders, the expanding use of PET in Alzheimer’s and Parkinson’s diagnostics, and the development of disease-specific radiotracers.

| Key Insights | Details |

|---|---|

| Positron Emission Tomography Imaging Market Size (2026E) | US$ 2.3 Bn |

| Market Value Forecast (2033F) | US$ 3.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver - Rising Disease Burden and Advancements in Precision Diagnostics

The global rise in chronic and life-threatening diseases, including cancer, neurological disorders such as Alzheimer’s and Parkinson’s disease, and cardiovascular conditions, is a major driver of demand for positron emission tomography (PET) imaging. For instance, in 2025, according to the Alzheimer’s Association, an estimated 7.2 million Americans aged 65 years and older are living with Alzheimer’s dementia, of whom approximately 74% are aged 75 years or above, highlighting the growing burden of neurodegenerative diseases in the aging population. PET plays a critical role in early disease detection, accurate staging, therapy selection, and treatment response monitoring, particularly in oncology where metabolic and molecular-level insights are essential for clinical decision-making. Increasing disease prevalence, aging populations, and higher diagnostic imaging volumes across both developed and emerging markets are reinforcing the clinical relevance of PET imaging. At the same time, growing awareness among clinicians and patients regarding the benefits of early and non-invasive diagnostics is accelerating PET adoption in precision medicine and personalized treatment pathways.

Technological advancements are further strengthening PET’s diagnostic value and expanding its clinical applications. Innovations such as hybrid PET/CT and PET/MRI systems, high-resolution digital detectors, time-of-flight technology, and AI-enabled image reconstruction are significantly improving image quality, scan speed, and diagnostic accuracy. In parallel, the development of novel radiotracers is enabling more targeted disease characterization across oncology, neurology, and cardiology. These advancements enhance workflow efficiency, reduce scan times, and improve patient throughput, making PET imaging more accessible and clinically impactful. Together, the convergence of rising disease burden, demand for early and accurate diagnostics, and continuous technological innovation is driving sustained growth in the global PET imaging market.

Restraints - High Capital Investment and Regulatory Barriers

The adoption of positron emission tomography (PET) imaging systems is significantly constrained by high capital and operational costs. PET scanners require substantial upfront investment, including the cost of the imaging system, specialized infrastructure such as radiation shielding, cooling systems, and facility modifications, as well as ongoing expenses related to maintenance, software upgrades, and system calibration. In addition, operational costs associated with radiopharmaceutical procurement, cyclotron access, cold-chain logistics, and the need for highly trained technologists and nuclear medicine physicians further elevate the total cost of ownership. These financial barriers limit PET adoption, particularly among smaller hospitals, outpatient imaging centers, and healthcare providers in cost-sensitive or emerging markets.

Regulatory complexity presents an additional challenge, especially for radiotracer development and system approvals. Radiopharmaceuticals are subject to stringent regulatory oversight due to their radioactive nature, requiring extensive clinical validation, safety assessments, and compliance with country-specific nuclear and pharmaceutical regulations. Lengthy approval timelines for new tracers and imaging technologies can delay commercialization and restrict clinical access to innovative diagnostic tools. Variability in regulatory frameworks across regions further complicates global market expansion, increasing development costs and slowing technology diffusion. Together, high capital requirements and regulatory hurdles continue to restrain broader PET imaging adoption and limit the pace of innovation across the market.

Opportunity - Technological Innovation, Radiotracer Development, and Theranostic Expansion

The integration of artificial intelligence (AI) and digital platforms represents a major growth opportunity for the positron emission tomography (PET) imaging market. AI-enabled image reconstruction, automated lesion detection, predictive analytics, and workflow optimization tools are enhancing scanning efficiency, improving diagnostic accuracy, and reducing interpretation variability. Cloud-based diagnostics and advanced data analytics further support remote image review, faster reporting, and multi-site collaboration, particularly within large hospital networks and diagnostic imaging chains. These digital advancements enable higher patient throughput, better clinical decision support, and more efficient utilization of PET systems, making advanced imaging more accessible and cost-effective across healthcare settings.

Furthermore, the development of novel radiotracers and the rapid growth of theranostics and personalized medicine are expanding PET’s clinical relevance beyond traditional oncology applications. Disease-specific tracers targeting neurological disorders, immuno-oncology pathways, and cardiac biomarkers are enabling more precise disease characterization and earlier diagnosis. PET’s growing role in theranostic workflows-where imaging is used to identify patients most likely to benefit from targeted radioligand therapies-creates strong synergies between diagnostics and treatment planning. This convergence is driving increased adoption of PET imaging in precision medicine programs, clinical research, and advanced therapeutic monitoring, unlocking new diagnostic and commercial opportunities across the global PET imaging market.

Category-wise Analysis

By Product, Full-Ring PET Scanners Dominate Globally Due to Superior Image Quality and Broad Clinical Utility

The full-ring PET scanners segment is projected to dominate the global positron emission tomography imaging market in 2026, accounting for a revenue share of 54.6%. This dominance is primarily attributed to their superior sensitivity, higher spatial resolution, and ability to perform whole-body imaging with greater diagnostic accuracy compared to partial-ring systems. Full-ring PET scanners are widely preferred in high-throughput clinical environments for oncology, neurology, and cardiology applications, where precise lesion detection, staging, and therapy response monitoring are critical. These systems are extensively deployed in tertiary hospitals and large diagnostic imaging centers due to their compatibility with advanced hybrid configurations such as PET/CT and PET/MRI. The growing emphasis on precision diagnostics, molecular imaging, and quantitative analysis has further strengthened adoption. Continuous advancements in detector technologies, time-of-flight imaging, digital photon counting, and AI-enabled reconstruction algorithms are enhancing scan speed, image clarity, and workflow efficiency. Additionally, rising investments in comprehensive cancer centers and academic research institutions globally continue to reinforce the sustained dominance of full-ring PET scanners.

By Application, Oncology Leads the Market Due to High Diagnostic Volumes and Clinical Reliance on PET

The oncology segment is projected to dominate the global positron emission tomography (PET) imaging market in 2026, accounting for 42.6% of revenue. This leadership is driven by PET’s indispensable role in cancer diagnosis, staging, treatment planning, and post-therapy monitoring across a wide range of malignancies. PET imaging enables functional and metabolic assessment of tumors, offering clinicians critical insights beyond conventional anatomical imaging modalities. Rising global cancer incidence, increasing use of targeted therapies, and the growing adoption of personalized treatment protocols are significantly boosting PET utilization in oncology. PET is routinely used to assess tumor aggressiveness, detect metastases, evaluate treatment response, and identify early-stage disease recurrence. Furthermore, expanding the availability of oncology-specific radiotracers and integrating PET into multidisciplinary cancer care pathways are strengthening its clinical relevance. Continuous improvements in image resolution, quantitative accuracy, and reduced scan times further support oncology's dominance as the leading application segment.

By End-user, Hospitals Dominate Globally Due to High Patient Volumes and Advanced Imaging Infrastructure

The hospitals segment is projected to dominate the global positron emission tomography imaging market in 2026, accounting for 48.2% of revenue. Hospitals serve as primary centers for complex diagnostic evaluations, cancer care, and advanced neurological and cardiac assessments, driving high utilization of PET imaging systems. Their ability to invest in capital-intensive imaging technologies and maintain in-house radiopharmacy capabilities further strengthens their market position. Large hospitals benefit from integrated diagnostic departments, multidisciplinary clinical teams, and access to specialized nuclear medicine professionals, enabling efficient PET deployment across multiple indications. High patient footfall, rising demand for advanced diagnostics, and the growing emphasis on early disease detection are driving sustained PET scan volumes. Additionally, hospitals are often early adopters of next-generation PET technologies, including PET/CT, PET/MRI, and AI-enabled imaging platforms, reinforcing their dominance as the leading end-user segment.

Region-wise Insights

North America Positron Emission Tomography Imaging Market Trends

North America is expected to dominate the global positron emission tomography (PET) imaging market, with a 47.5% share in 2026, led by the United States. Market leadership is supported by advanced healthcare infrastructure, high utilization of diagnostic imaging, and strong reimbursement coverage for PET procedures, particularly in oncology. The region benefits from early adoption of innovative imaging technologies and widespread availability of hybrid PET systems across hospitals and diagnostic imaging centers.

High prevalence of cancer and neurodegenerative disorders, strong emphasis on precision medicine, and active clinical research ecosystems are further driving PET demand. The presence of leading imaging manufacturers, well-established radiopharmaceutical supply chains, and robust clinician training programs supports sustained technology uptake. Additionally, increasing investments in AI-driven imaging analytics and theranostic applications are strengthening North America’s position as the largest PET imaging market globally.

Europe Positron Emission Tomography Imaging Market Trends

The European positron emission tomography imaging market is expected to grow steadily, supported by expanding access to advanced diagnostic imaging, an aging population, and the increasing burden of chronic diseases. Key markets such as Germany, the U.K., France, Italy, and the Nordic countries exhibit strong adoption of PET due to well-developed healthcare systems and established nuclear medicine practices.

The growing integration of PET into oncology and neurology care pathways, along with the rising use of PET in clinical research and drug development, is supporting market expansion. Regulatory support for advanced imaging technologies, improving reimbursement frameworks in select countries, and increased investments in hybrid PET systems are enhancing adoption. Continuous innovation by regional and global manufacturers, combined with strong academic and research collaborations, is sustaining long-term growth across Europe.

Asia Pacific Positron Emission Tomography Imaging Market Trends

The Asia Pacific positron emission tomography (PET) imaging market is expected to register a relatively high CAGR of around 7.2% between 2026 and 2033, driven by expanding healthcare infrastructure, rising disease prevalence, and increased access to advanced diagnostic technologies. Countries such as China, India, Japan, and South Korea are witnessing rapid growth in PET installations driven by rising cancer incidence and improved diagnostic capabilities.

Government initiatives to strengthen healthcare systems, growing investments in tertiary hospitals, and increasing penetration of private diagnostic imaging centers are accelerating PET adoption. Cost-effective system offerings, expanding radiopharmaceutical production capabilities, and growing awareness of early disease detection are further supporting market growth. Strategic partnerships between global manufacturers and regional healthcare providers are also enhancing access to technology across emerging Asia Pacific markets.

Competitive Landscape

The global positron emission tomography imaging market is highly competitive, with strong participation from companies such as United Imaging Healthcare Co., Ltd., Siemens Healthineers AG, GE HealthCare, Bruker, and MinFound Medical Systems Co., Ltd. These players leverage strong brand recognition, broad distribution networks, and continuous technological innovation to address diverse clinical requirements across oncology, neurology, cardiology, and research applications.

Manufacturers are increasingly focusing on advanced detector technologies, AI-enabled image reconstruction, improved system sensitivity, and workflow optimization to enhance clinical performance and operational efficiency. Strategic priorities include portfolio expansion, geographic penetration in emerging markets, partnerships with radiopharmaceutical developers, and clinician training initiatives. Ongoing innovation and competitive differentiation remain central to strengthening market positioning and driving sustained growth in the global PET imaging market.

Key Industry Developments:

- In October 2025, Sirona Medical obtained U.S. Food and Drug Administration (FDA) 510(k) clearance for its Sirona Advanced Imaging Suite, representing a key regulatory milestone and the company’s first authorization for a Class II medical device.

- In October 2024, United Imaging launched its uMI Panvivo and uMI Panorama GS PET/CT systems and showcased the uMI AI Solution at the EANM 2024 Congress in Hamburg, underscoring its commitment to innovation in molecular imaging.

- In July 2024, Positron Corporation introduced its NeuSight PET-CT 3D 64-slice scanner for the U.S. and North American markets, offering enhanced imaging precision, patient comfort, and operational efficiency for nuclear cardiology practices and hospitals.

- In October 2023, the Medicines Discovery Catapult (MDC), the Medical Research Council (MRC), and Innovate UK launched the UK’s first national total-body Positron Emission Tomography (PET) Imaging Platform (NPIP), funded with £32 million and equipped with Siemens Healthineers’ Biograph Vision Quadra PET/CT systems to advance drug discovery and improve patient outcomes.

Companies Covered in Positron Emission Tomography Imaging Market

- Shanghai United Imaging Healthcare Co., LTD.

- Siemens Healthineers AG

- GE HealthCare

- Bruker

- MinFound Medical Systems Co., Ltd

- CANON MEDICAL SYSTEMS CORPORATION

- Koninklijke Philips N.V.

- Mediso Ltd.

- Kindsway Biotech

- Neusoft Medical Systems Co., Ltd.

- Shimadzu Corporation

- Positrigo AG

- SynchroPET, Inc.

- Others

Frequently Asked Questions

The global positron emission tomography imaging market is projected to be valued at US$ 2.3 Bn in 2026.

Rising prevalence of cancer and neurological disorders, growing demand for early and precise diagnosis, and continuous advancements in PET imaging technologies are driving global market growth.

The global positron emission tomography imaging market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Key opportunities include expanding adoption in emerging markets, integration of AI-enabled imaging platforms, development of novel radiotracers, and growth of theranostics and personalized medicine.

United Imaging Healthcare Co., Ltd., Siemens Healthineers AG, GE HealthCare, Bruker, MinFound Medical Systems Co., Ltd., are some of the key players in the positron emission tomography imaging market.