- Plastics, Polymers & Resins

- Polytetrahydrofuran Market

Polytetrahydrofuran Market Size, Share, and Growth Forecast, 2025 - 2032

Polytetrahydrofuran Market By Source (Petro-Based Poly THF, Others), Application (Spandex Fibers, Others), End-user Industry (Paints & Coatings, Others), and Regional Analysis for 2025 - 2032

Polytetrahydrofuran Market Size and Trends Analysis

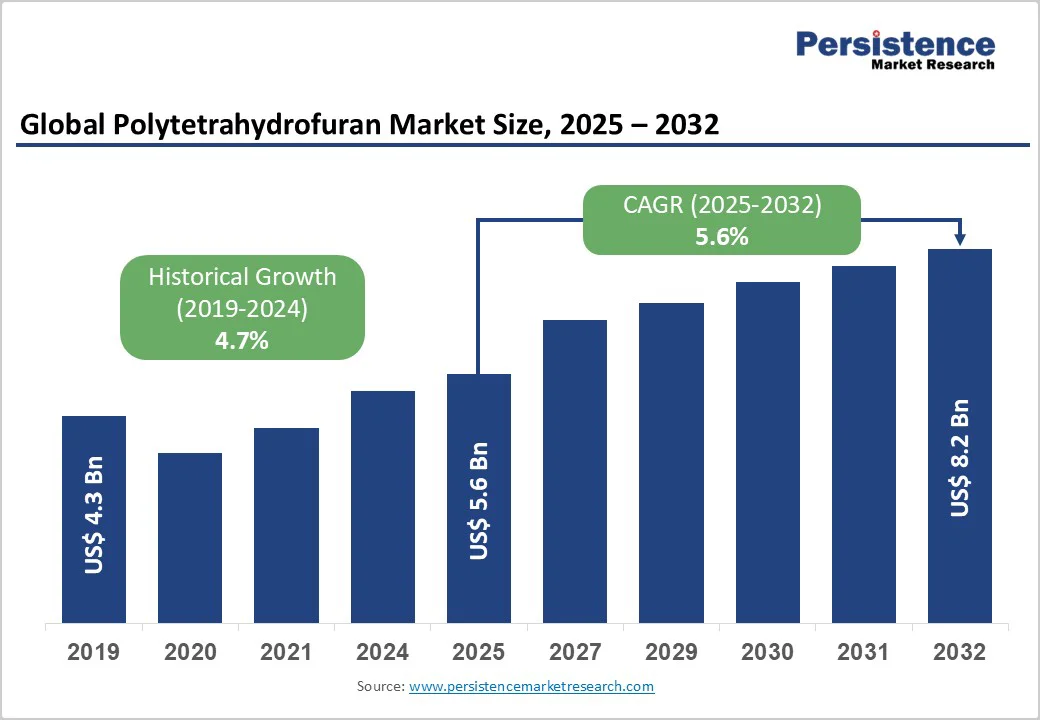

The global polytetrahydrofuran market size was valued at US$5.6 billion in 2025 and is projected to reach US$8.2 billion by 2032, growing at a CAGR of 5.6% during the forecast period from 2025 to 2032.

The rising consumption of spandex fibers and thermoplastic polyurethane (TPU) is driven by the ongoing expansion of the athleisure and performance apparel markets, as well as by increasing industrial use in automotive applications, adhesives & sealants, and artificial leather.

Strategic sustainability initiatives, such as the introduction of low-carbon products and the development of bio-based PTMEG, are also further strengthening long-term structural demand.

Key Industry Highlights

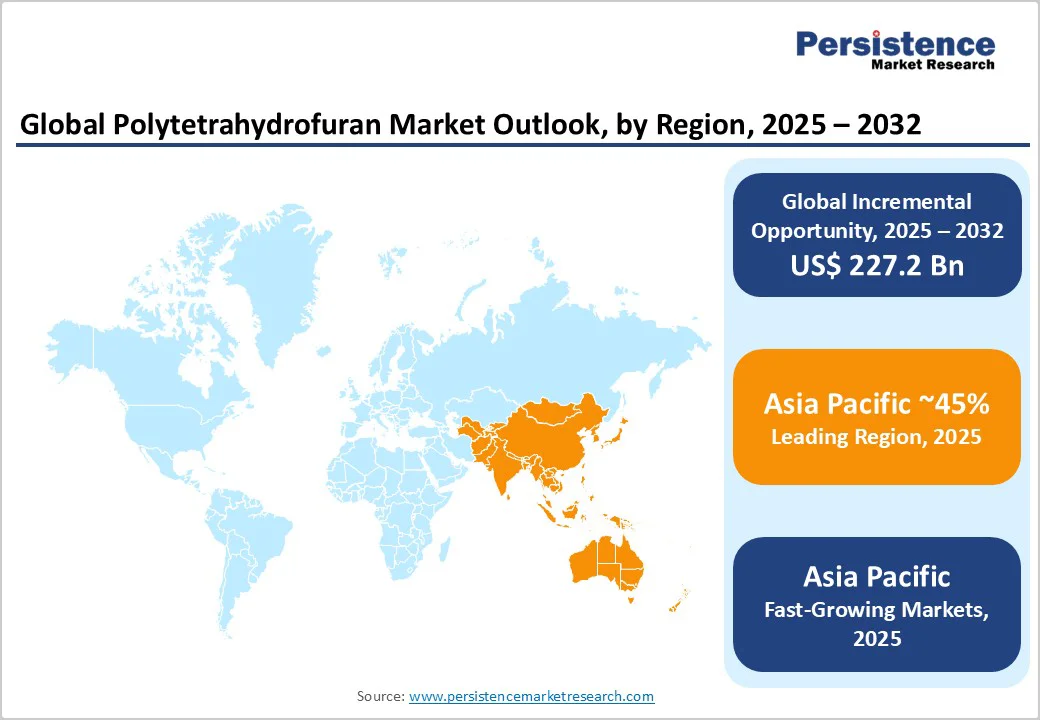

- Leading Region: Asia Pacific is the leading region, underpinned by China’s integrated spandex value chain, competitive production advantages, and ongoing capacity investments supporting global apparel and elastomer demand.

- Fastest-Growing Country: China is the fastest-growing country opportunity, with capacity additions, rising domestic consumption, and expanding downstream applications across apparel, footwear, and automotive components.

- Leading Application Segment: Spandex fibers are the dominant application, reflecting sustained growth in athleisure, intimates, and medical textiles, where elasticity, rebound, and comfort are critical performance attributes.

- Fastest-Growing Application Segment: Thermoplastic polyurethane (TPU) is the fastest-growing application, driven by automotive lightweighting, footwear performance needs, and 3D printing adoption, expanding PTMEG’s industrial demand base.

- Key Market Opportunity: Bio-based PTMEG and low-PCF grades present the key opportunity, aligning with brand/OEM sustainability goals, regulatory pressures, and premiumization opportunities across apparel, footwear, and medical devices.

| Key Insights | Details |

|---|---|

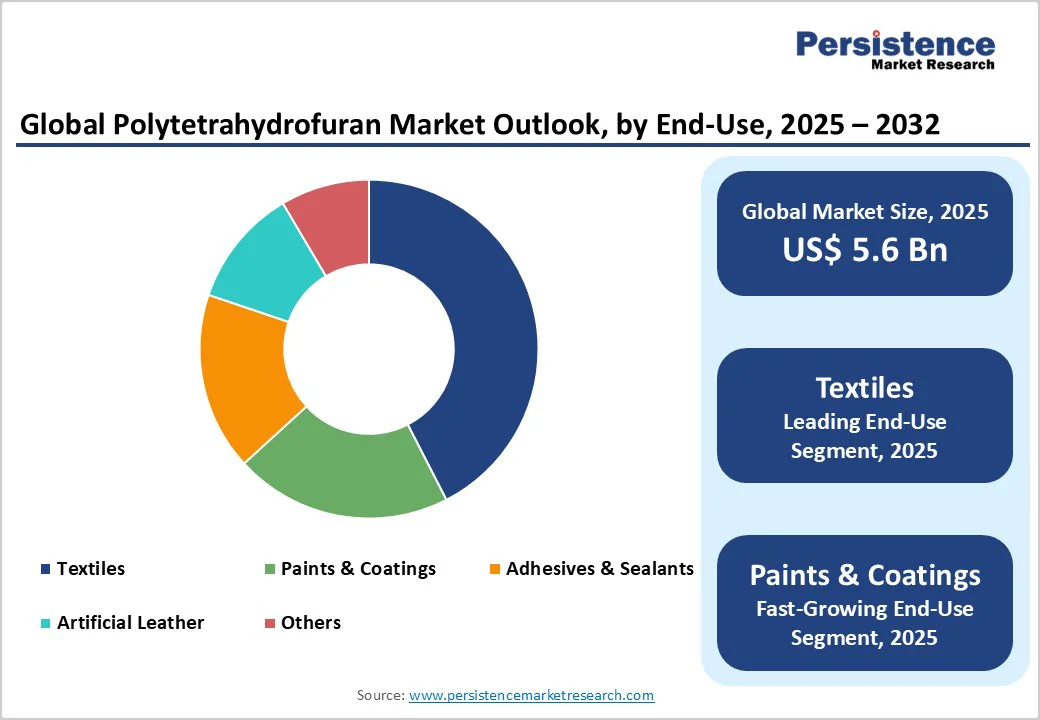

| Polytetrahydrofuran Size (2025E) | US$5.6 Bn |

| Market Value Forecast (2032F) | US$ 8.2 Bn |

| Projected Growth CAGR (2025-2032) | 5.6% |

| Historical Market Growth (2019-2024) | 4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Bold Expansion of Spandex-led Consumption

The growing demand for spandex fibers is a primary driver of the polytetrahydrofuran (PTMEG) or Polytetramethylene ether glycol (PolyTHF/PTMEG) market, fueled by the rising demand for athleisure, sportswear, intimate apparel, and medical textiles. PTMEG serves as a key polyol in spandex production, forming the flexible backbone that imparts elasticity, strength, and durability to fibers.

The continued shift toward comfort-driven apparel and performance textiles, coupled with fast-moving e-commerce fashion cycles and private-label expansion, sustains steady consumption growth. Brand investments in high-stretch fabrics and compression garments further elevate the importance of PTMEG in the textile value chain.

From a supply-side perspective, robust availability of 1,4-butanediol and tetrahydrofuran (THF) PTMEG’s essential feedstocks ensures stable production. Improved vertical integration and optimized logistics networks in Asia, particularly China and India, reinforce supply continuity.

As urbanization, disposable incomes, and fitness trends accelerate across emerging economies, PTMEG consumption tied to spandex applications is poised for continued, broad-based expansion.

TPU Penetration across Automotive, Footwear, and 3D Printing

Polytetrahydrofuran demand is also expanding through its critical role in thermoplastic polyurethane (TPU) formulations. PTMEG-based TPU delivers exceptional hydrolysis resistance, abrasion strength, and low-temperature flexibility properties highly valued across diverse industries.

In automotive applications, TPU supports lightweighting and durability goals for interior trims, seals, battery pack insulation, and vibration-damping components essential for electric vehicles. This transition aligns with OEM sustainability and performance targets, promoting higher-value PTMEG grades.

In the footwear sector, leading brands are increasingly using TPU for midsoles, outsoles, and films, capitalizing on its rebound resilience and long-term comfort performance. The growing applications of PTMEG-based TPU in 3D printing, particularly for functional prototypes and flexible components, further widens the polytetrahydrofuran market scope.

These multi-sectoral applications diversify PTMEG demand beyond traditional textiles, stabilize market cyclicality, and motivate producers to innovate through low-carbon-footprint variants and enhanced processing consistency to meet global quality and environmental standards.

Barrier Analysis - Feedstock Price Volatility and Supply Disruptions

The PTMEG industry remains highly exposed to fluctuations in THF and 1,4-butanediol (BDO) prices, driven by energy market dynamics, refinery maintenance, and regional production outages. Feedstock availability disruptions, particularly in Asia, can strain downstream operations, impacting spandex and TPU manufacturers. The Reppe process, a key production route, is also sensitive to raw material quality and environmental regulation shifts.

Trade policies, tariffs, and logistics constraints often compound volatility by disrupting supply consistency and regional balance. To manage uncertainty, producers are increasingly focusing on multi-sourcing, long-term contracts, and regional warehousing strategies. However, these measures elevate working capital requirements, challenging smaller players and limiting flexibility during demand fluctuations.

Rising Sustainability Compliance and Regulatory Costs

Tightening environmental regulations such as REACH, CLP, and carbon footprint reporting are reshaping PTMEG production economics. Manufacturers must invest in cleaner technologies, process transparency, and compliance audits to meet evolving sustainability mandates. Introducing bio-based or low-PCF PTMEG variants enhances brand positioning but demands higher R&D and certification costs.

The transition toward sustainable supply chains also involves mass-balance certifications and energy-efficient process redesigns, adding operational complexity. While such upgrades support long-term competitiveness and attract OEM partnerships, they raise short-term expenses and reduce profit margins. Smaller producers, in particular, face challenges in scaling sustainability investments without strong feedstock integration or financial backing.

Opportunity Analysis - Scale-up of Bio-based PTMEG and Low-PCF Portfolios

The shift toward bio-based and low-PCF PTMEG is emerging as a transformative opportunity in the polymer value chain. Renewable feedstocks such as bio-BDO, derived from succinic acid or furfural, are progressing from pilot to commercial-scale production, enabling manufacturers to lower carbon intensity without compromising performance.

Biomass balance models and certified renewable inputs enhance traceability and align with global decarbonization trends across textiles, footwear, and industrial applications.

Collaborations with leading apparel, footwear, and medical-device OEMs allow producers to co-develop high-performance bio-elastomers tailored to sustainability mandates. Early adopters can gain pricing leverage and secure long-term supply agreements, benefiting from brand-driven demand for sustainable materials.

This transition not only improves portfolio resilience against regulatory tightening but also aligns with customers’ Scope 3 emission reduction goals, positioning suppliers as strategic sustainability partners.

Medical Devices, Wearables, and Additive Manufacturing

Healthcare and medical technology segments present strong growth potential for PTMEG-based TPU due to its superior biocompatibility, optical clarity, and mechanical resilience. It is increasingly used in catheters, tubing, and implantable housings requiring flexibility, sterilization stability, and patient comfort.

The expansion of wearable medical devices, remote monitoring systems, and soft robotics further accelerates adoption, as these applications demand materials that can endure repeated stress while remaining skin-safe and lightweight.

In parallel, the additive manufacturing sector is unlocking new opportunities for PTMEG-based TPU in 3D-printed elastomer components. Its excellent layer adhesion, elasticity, and dimensional stability enable the production of customized automotive, healthcare, and industrial parts

. These high-value niches offer manufacturers improved margins, diversified demand streams, and reduced dependence on cyclical textile sectors, supporting long-term market stability and technological leadership.

Category-wise Analysis

Source Insights

Petro-based PolyTHF remains dominant with around 96% market share in 2025, driven by mature integration across the BDO-THF-PTMEG value chain and well-established global capacities. Proven process economics, consistent polymer quality, and optimized Reppe-route energy efficiency continue to reinforce its cost competitiveness and suitability for large-scale spandex and TPU production.

In contrast, bio-based PTMEG is expanding rapidly from a small base, supported by sustainability mandates and brand-driven decarbonization efforts. The rise of biomass balance certifications and low-PCF product portfolios enables producers to capture early mover advantages in performance apparel, footwear, and medical applications. This transition marks a strategic pivot toward circular and traceable supply chains.

Application Insights

Spandex fibers dominate the polytetrahydrofuran market with about 68% share in 2025, underpinned by its vital role in elastane chemistry and global fashion trends emphasizing stretch, recovery, and comfort. Strong demand from athleisure, lingerie, swimwear, and medical textiles ensures stable base load volumes, particularly across Asia’s textile hubs.

Thermoplastic polyurethane (TPU) follows as the second-largest and fastest-growing application, benefiting from rising use in automotive interiors, footwear cushioning, protective films, and additive manufacturing. Other smaller but high-value applications, such as co-polyester-ether and cast polyurethane elastomers, address performance-critical industrial segments requiring chemical resistance and fatigue durability.

End-user Insights

The textiles sector leads overall PTMEG consumption, leveraging its elasticity and durability in performance wear, intimate apparel, and healthcare fabrics. Continuous fashion innovation and sportswear expansion sustain strong consumption, while the growth of e-commerce accelerates demand for comfort-focused garments.

Beyond textiles, PTMEG-based polyurethane chemistry supports adhesives and sealants used in construction, electronics, and industrial assembly. Artificial leather applications in footwear and automotive interiors reflect sustainability and aesthetic shifts away from natural leather. Meanwhile, paints, coatings, and cable jacketing represent niche uses, where abrasion resistance and weatherability expand PTMEG’s technical reach.

Regional Insights

North America Polytetrahydrofuran Trends

The U.S. anchors North American PTMEG demand, driven by its strong base in athletic footwear, apparel, and automotive manufacturing. Major brands and OEMs increasingly emphasize material performance alongside environmental transparency, accelerating the shift toward low-PCF and certified mass-balance PTMEG.

Advanced polymer R&D capabilities, additive manufacturing hubs, and medical device clusters across states such as California, Texas, and Massachusetts foster innovation in high-performance TPU and elastomer applications.

E-mobility growth further propels PTMEG adoption in lightweight, durable automotive components, while nearshoring in textiles and flexible packaging strengthens local supply resilience. The region’s prioritization of compliance, quality assurance, and innovation-driven differentiation sustains its position as a premium PTMEG consumer base, even amid moderate volume growth compared to Asia.

Europe Polytetrahydrofuran Trends

Europe’s polytetrahydrofuran market reflects rigorous adherence to REACH compliance, product stewardship, and fast-evolving sustainability directives. Producers across Germany, France, the U.K., and Spain are scaling biomass balance and low-PCF PTMEG offerings to meet automotive and medical-grade performance standards.

These transitions align closely with European OEMs’ decarbonization goals and circular economy commitments, creating opportunities for co-developing bio-based elastomer systems.

Harmonized regulations enhance market predictability and reward certified, traceable supply chains. While the region experiences slower apparel-driven consumption compared to Asia, its strength lies in high-value industrial, healthcare, and specialty applications. Europe’s focus on quality, environmental accountability, and technological sophistication ensures stable and higher-margin PTMEG demand through the forecast period.

Asia Pacific Polytetrahydrofuran Trends

Asia Pacific dominates the global PTMEG landscape, led by China’s vast production and consumption base integrated with spandex manufacturing chains and cost-efficient logistics. Continuous capacity expansions across major chemical clusters underscore long-term confidence in elastane, TPU, and performance polymer markets. China’s large-scale integration with 1,4-BDO and THF production further enhances regional competitiveness.

Japan drives the development of advanced TPU and elastomer grades for electronics and automotive uses, while India and ASEAN benefit from textile manufacturing migration and surging domestic apparel demand.

Policy-driven industrial upgrading and export competitiveness in garments, footwear, and automotive components sustain the region’s leadership. Collectively, Asia Pacific’s integration depth, scale, and innovation adaptability reinforce its role as the global growth engine for PTMEG production and downstream applications.

Competitive Landscape

The global polytetrahydrofuran market is moderately consolidated, with top producers commanding substantial global capacity, while mid-tier participants compete through regional specialization, technology licensing, and tailored formulations. Competitive differentiation relies on strong feedstock integration, consistent polymer quality for spandex and TPU applications, and advancing sustainability credentials such as low-PCF and mass-balance certifications.

Strategic initiatives increasingly emphasize capacity optimization, bio-based PTMEG scale-up, and partnerships with apparel, footwear, and medical OEMs to secure long-term demand. Companies enhancing supply chain resilience through multi-regional production footprints and offering premium technical support maintain pricing leverage and reinforce their market positioning amid tightening sustainability and performance requirements.

Key Industry Developments

- In May 2024, BASF expanded its biomass balance portfolio for BDO, THF, and PolyTHF at select production sites, increasing certified renewable-feedstock availability. This expansion strengthens supply chains for European and North American customers seeking sustainable, traceable intermediates in high-performance spandex, TPU, and elastomer products.

- In September 2024, Huafon announced a large-scale investment to produce bio-based PTMEG from renewable feedstocks. The project aims to accelerate the shift toward sustainable elastomers, supporting low-carbon spandex, TPU, and other performance polymer applications while meeting increasing OEM and regulatory sustainability requirements.

- In December 2023, BASF introduced low-PCF grades for BDO, THF, and PolyTHF, helping customers cut Scope 3 emissions. These grades support sustainability goals in textiles and elastomers, offering lower carbon footprint alternatives while maintaining performance and quality standards for spandex and TPU applications.

Companies Covered in Polytetrahydrofuran Market

- BASF SE

- INVISTA

- Dairen Chemical Corporation (DCC)

- Chongqing Jianfeng Industrial Group

- Mitsubishi Chemical Corporation

- Korea PTG, Co. Ltd.

- Shanxi Sanwei Group Co., Ltd.

- HYOSUNG

- Hangzhou Sanlong New Materials Co., Ltd.

- Shaanxi Shanhua Coal Chemical Group

- Lycra Company

- Gantrade Corporation

- Lubrizol Advanced Materials, Inc.

Frequently Asked Questions

The polytetrahydrofuran market is projected to grow from US$5.6 Billion in 2025 to US$8.2 Billion by 2032, at a CAGR of 5.6%, after expanding at 4.7% historically during 2019-2024.

The primary driver is spandex fiber expansion in athleisure, performance apparel, intimates, and medical textiles, reinforced by diversified growth in TPU for automotive, footwear, and 3D printing.

Spandex Fibers lead with an estimated ~68% share, driven by durability, stretch, and comfort requirements across global apparel and healthcare textiles.

Asia Pacific dominates the polytetrahydrofuran market, led by China’s integrated spandex value chain, cost-efficient production, and sustained capacity investments supporting exports and domestic demand.

Scaling bio-based PTMEG and low-PCF certified grades to meet brand and OEM sustainability targets, enabling premium positioning and long-term offtake partnerships.

Leading companies in the polytetrahydrofuran market include BASF SE, INVISTA, Mitsubishi Chemical Corporation, Dairen Chemical Corporation (DCC), HYOSUNG, Lycra Company, Korea PTG, and Shanxi Sanwei Group.