- Technology

- Polyfunctional Robots Market

Polyfunctional Robots Market Size, Share, and Growth Forecast, 2025 - 2032

Polyfunctional Robots Market By Component (Hardware, Software/Platform, Services), Robot Type (Collaborative Robots, Autonomous Robots, Humanoid Robots, Soft Robots, Others), Vertical, and Regional Analysis for 2025 - 2032

Polyfunctional Robots Market Size and Trends Analysis

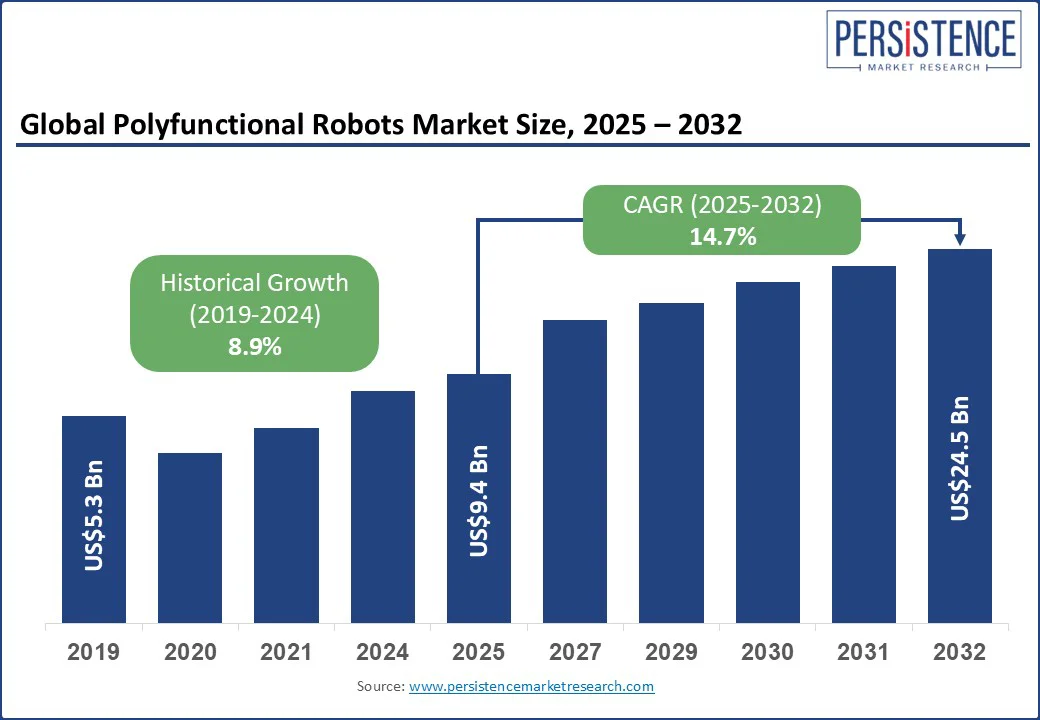

The global polyfunctional robots market size is projected to rise from US$9.4 Bn in 2025 to US$24.5 Bn by 2032. It is anticipated to witness a CAGR of 14.7% during the forecast period from 2025 to 2032.

The polyfunctional robots market growth is driven by the rising demand for automation across industries to boost efficiency, cut labor costs, and tackle workforce shortages. Polyfunctional robots, capable of executing multiple functions such as assembly, inspection, and material handling, are essential for adaptable manufacturing. Advancements in AI and sensor technologies also enhance their versatility and operational autonomy.

Key Industry Highlights:

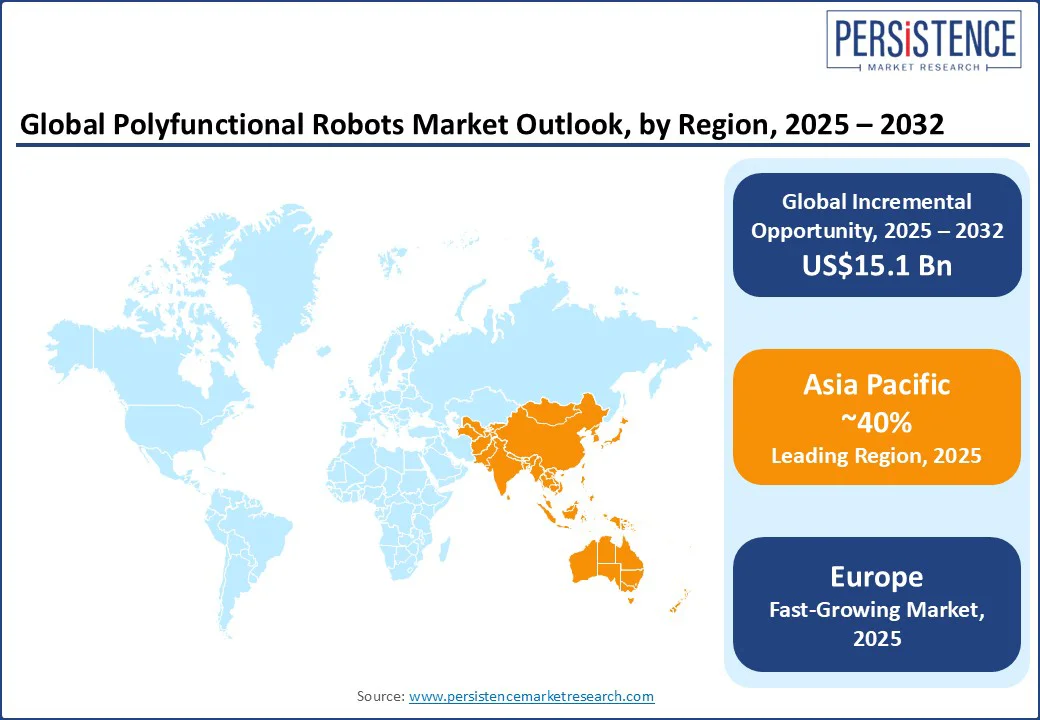

- Leading Region: Asia Pacific is projected to hold over 40% of the market share in the polyfunctional robots market in 2025, driven by rapid industrialization, rising labor costs, and acute workforce shortages due to aging populations.

- Fastest-growing Region: Europe, driven by acute labor shortages, especially in post-Brexit U.K. and industrial regions such as Germany and Italy, which are pushing industries to adopt automation.

- Investment Plans: Germany’s €350 million (US$382 Mn) High-Tech Strategy and France’s 2030 robotics reindustrialization initiative.

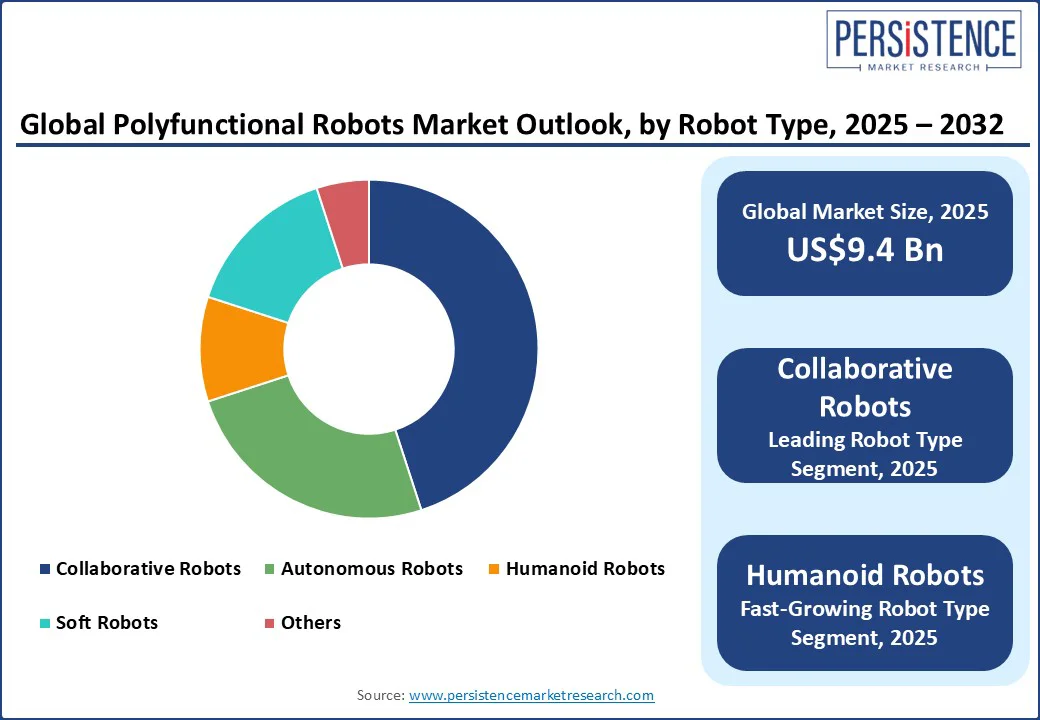

- Dominant Robot Type: Collaborative robots (Cobots), over 35% share due to their ease of deployment, safety in shared human workspaces, and plug-and-play usability.

- Leading Vertical: Manufacturing, holding more than 37% market share in 2025, led by the demand for flexible, multi-role robots capable of functioning in high-mix, low-volume production setups.

|

Global Market Attribute |

Key Insights |

|

Polyfunctional Robots Market Size (2025E) |

US$9.4 Bn |

|

Market Value Forecast (2032F) |

US$24.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

14.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.9% |

Market Dynamics

Driver - Cost Pressures and Labor Shortages Driving the Shift Toward Flexible Automation

Organizations are under increasing pressure to improve margins, reduce waste, and boost productivity, prompting a shift from just-in-time to just-in-case production models. This change demands systems that can quickly switch between different products or processes without frequent reconfigurations. Polyfunctional robots enable this flexibility, helping firms avoid frequent equipment changes. This shift is backed by government-supported automation schemes and EU initiatives such as Horizon Europe, which aim to accelerate digital transformation and automation adoption in 2025.

Rising labor costs and skilled worker shortages further intensify the need for automation. According to the U.S. Bureau of Labor Statistics, the Employment Cost Index for Q4 2024 showed a 0.9% increase in wages and a 0.8% rise in benefit costs from September to December 2024. In March 2024, the European Commission reported that 63% of SMEs struggled to find skilled workers, pushing companies toward robotic solutions. Polyfunctional robots provide a cost-effective solution by operating continuously, cutting overtime costs, and eliminating recruitment and training efforts, especially valuable in industries with high turnover.

Restraint - Complex Maintenance Needs and Downtime Challenges

Polyfunctional robots, while offering unmatched versatility, come with complex mechanical, electrical, and software systems that increase the probability of technical failures. These systems require frequent, often specialized, maintenance, posing a significant restraint for industries with tight production timelines or limited in-house technical expertise. According to a study, in manufacturing, aging equipment accounts for 60% - 65% of downtime incidents, and unplanned downtime costs industrial manufacturers up to US$50 Bn annually.

The challenge is amplified in synchronized production environments such as automotive and electronics manufacturing, where a single robot’s failure can halt multiple processes, causing cascading delays and financial losses. In high-stakes sectors such as healthcare and precision electronics, robotic malfunctions can jeopardize output quality or even patient safety. Maintenance often demands precise calibration and diagnostic expertise, increasing reliance on OEMs or support teams, raising operational costs, and limiting scalability for smaller businesses.

Opportunity - Growth in Service Robotics Fuels Adoption of Compact, Versatile Systems

Miniaturization, driven by advancements in microelectronics, actuators, and precision manufacturing, enables the design of smaller, lighter, yet more capable robotic systems. These compact robots can be deployed in constrained environments such as hospitals, homes, retail spaces, and even within the human body. This technical shift supports the development of polyfunctional robots that can perform a range of tasks while maintaining a minimal footprint, significantly enhancing their versatility and appeal across sectors.

Service robotics is experiencing a surge due to labor shortages, aging populations, and demand for high-efficiency services. For instance, hospitals increasingly use robots for patient lifting, health monitoring, and supply delivery. According to the International Federation of Robotics, global sales of professional service robots rose by 30% in 2023, totaling over 205,000 units Asia Pacific accounted for nearly 80% of these (162,284 units). Countries across Asia and Europe are investing heavily in robotics R&D, with a strong focus on making service robots smaller, smarter and more cost-effective to address healthcare and logistics challenges. As sensors, batteries, and processors become smaller and more energy-efficient, total ownership costs drop, making polyfunctional robots more accessible to SMEs and public institutions.

Polyfunctional Robots Market Key Trend

Emergence of Human-Robot Collaboration in Workplaces

The shift toward high-mix, low-volume production models, driven by supply chain uncertainties and evolving consumer preferences, creates strong momentum for the adoption of polyfunctional robots. Cobots with user-friendly interfaces and plug-and-play components are increasingly in demand, particularly those that can perform tasks such as inspection, assembly, packing, and logistics with minimal reprogramming. Companies, including DHL and FedEx, already utilize such cobots for simultaneous picking, sorting, and packaging functions that previously required separate machines, highlighting the growing need for dynamic and scalable robotic systems.

The growing emphasis on worker safety and ergonomics in post-pandemic workplaces is accelerating the adoption of polyfunctional robots. Polyfunctional robots offer operational continuity by adapting to various roles based on task and workforce availability, especially in healthcare, where cobots assist in patient handling, medication delivery, and sanitization. The South Korean government's K-Humanoid Alliance, launched in April 2025, and China's surge in humanoid robot procurement and related tech jumped from 4.7 million yuan (US$658,000) in 2023 to 214 million yuan (US$29.96 Mn) in 2024, reflecting strong institutional backing, driving the adoption of multifunctional robotic platforms across industries.

Category-wise Analysis

Robot Type Insights

Based on robot type, the market is divided into collaborative robots, autonomous robots, humanoid robots, soft robots & others. Among these, collaborative robots are expected to account for over 35% share in 2025 due to their flexibility, ease of deployment, and ability to safely work alongside humans without requiring extensive safety infrastructure. Their plug-and-play nature, intuitive programming, and compatibility with AI-driven vision and sensing systems make them ideal for dynamic manufacturing lines.

Humanoid robots are expected to grow at the highest rate due to their ability to replicate human actions, enabling seamless integration into human-centric environments such as healthcare, customer service, and education. Advancements in AI, motion control, and natural language processing further enhance their utility across diverse tasks. Growing government and private sector investments in R&D are also accelerating their adoption.

Vertical Insights

By verticals, the market is segregated into manufacturing, healthcare, logistics & warehousing, defense & security, agriculture, construction & infrastructure, retail & hospitality & others. Out of these, manufacturing is expected to account for more than 37% share in 2025 due to the increasing adoption of automation in assembly lines, quality control, and material handling. Industries are prioritizing flexible, multi-tasking robots to enhance productivity and address labor shortages. These robots support high-mix, low-volume production and reduce operational downtime. The rising demand for cost-efficient and scalable robotic solutions further drives adoption.

The healthcare sector is projected to grow at the highest rate due to increasing demand for automation in surgery, elderly care, rehabilitation, and hospital logistics. The aging global population and chronic disease burden are driving the need for robotic support in patient care and assistance. Polyfunctional robots seamlessly switch between roles such as surgical assistant, disinfection units, and patient interaction aids, enhancing their appeal in hospitals and clinics.

Regional Insights

North America Polyfunctional Robots Market Trends

In the U.S., the automotive sector accounted for about 33% of all robot installations in 2023 (14,678 robots), driven by the shift toward EV assembly and the need for robots with precise component handling and flexible reprogramming. Polyfunctional robots capable of welding, part transport, and quality inspection are especially valued on production lines that produce multiple vehicle variants or battery systems. Tariffs on Chinese imports of sensors and robot components have doubled the cost of some units, such as Unitree’s humanoid robot (from US$16k to approximately US$40k), prompting manufacturers to adopt multi-tasking robots that reduce parts count and lower their dependence on imported systems.

With the U.S. Census Bureau projecting that over 20% of the population will be aged 65 and older by 2030, the healthcare sector is under pressure to innovate. Polyfunctional robots offer scalable, efficient support to meet growing healthcare demands without proportional workforce expansion. In Canada, particularly in provinces such as Ontario, Alberta, and British Columbia, manufacturers and resource extraction industries such as mining and forestry are accelerating automation to address labor shortages. For instance, mining companies in Alberta are using polyfunctional robots for inspection, transport, and minor machinery repairs.

Asia Pacific Polyfunctional Robots Market Trends

Asia Pacific is expected to account for a share of more than 40% in 2025. China, Japan, India, and South Korea are witnessing strong demand due to demographic and industrial shifts. According to China’s State Administration for Market Regulation, as of December 2024, there were 451,700 enterprises in the intelligent robotics industry with total registered capital exceeding 6.44 trillion yuan (US$884 Bn). Labor shortages and rising wages are pushing Chinese manufacturers toward automation. In Japan, a severe labor shortage caused by an aging population of 36 million people aged 65 or older in 2024 has driven the adoption of polyfunctional robots, particularly in healthcare and eldercare. The Ministry of Economy, Trade and Industry (METI) is supporting this through subsidies and pilot projects where robots assist in rehabilitation, delivery, and companionship.

South Korea’s Smart Factory Initiative, led by the Ministry of SMEs and Startups, aims to digitize over 30,000 SMEs by 2025, with polyfunctional robots playing a central role due to their modularity and adaptability. The country’s strong electronics export sector also necessitates robotic solutions for mixed production lines. In India, automation is rising in the automotive, pharmaceuticals, and consumer electronics sectors, supported by the Production Linked Incentive (PLI) scheme to boost export competitiveness. Although labor costs are relatively low, polyfunctional robots are being adopted for quality control, welding, and pick-and-place operations.

Europe Polyfunctional Robots Market Trends

In Germany, 77% of employees in a mid-2025 survey supported robots for dangerous and repetitive tasks, addressing skill shortages and sustaining competitiveness. Germany’s High-Tech Strategy 2025, backed by €350?million (US$382 Mn) in robotics R&D, supports this push. Both Germany and the U.K. are also initial deployment targets for Baidu-Lyft robotaxi services launching in 2026, highlighting growing interest in autonomous systems and mobility robotics. In the U.K., polyfunctional robot demand is fueled by post-Brexit labor shortages, with the Office for National Statistics (ONS) reporting ongoing workforce gaps in manufacturing as of early 2025.

The U.K.’s logistics and retail warehousing sectors, propelled by e-commerce, are integrating mobile polyfunctional robots for tasks like handling, packaging, and sorting. The France 2030 initiative promotes reindustrialization and robotics investments in aerospace, pharmaceuticals, and agri-tech, where infrastructure constraints necessitate flexible robotic deployment. Italy sees growth within its industrial clusters in Emilia-Romagna and Lombardy, especially in textiles, food processing, and automotive, where SMEs benefit from reduced capex and increased versatility. In Russia, despite sanctions and supply chain issues, domestic manufacturing in defense, aerospace, and heavy machinery prioritizes automation, with polyfunctional robots valued for military-grade adaptability across reconnaissance, manipulation, and transport.

Competitive Landscape

The global polyfunctional robots market is moderately fragmented, with a mix of established robotics giants and emerging tech innovators competing for market share. Manufacturers are focusing on advanced features such as multi-tasking capabilities, human-robot collaboration, and AI integration. Many players invest heavily in R&D to improve flexibility, miniaturization, and user interfaces. Strategic partnerships with automation solution providers and end-user industries help expand their market reach.

Key Industry Developments:

- In July 2025, Pudu Robotics launched the PUDU CC1 Pro, an AI-powered autonomous cleaning robot designed for large commercial spaces. Building on its predecessor, the CC1 Pro features real-time floor cleanliness detection, adaptive cleaning strategies, visual SLAM navigation, and self-monitoring components. It delivers enhanced cleaning efficiency with AI-driven spot scrubbing and visualized performance dashboards to support human-robot collaboration.

- In June 2025, Seiko Epson Corporation launched its first industrial collaborative robot, the AX6-A901S. This all-in-one solution includes a compact 6-axis carbon arm, RC-A101 controller, and AX Portal programming system. Cleanroom-ready (ISO Class 5, IP54), it delivers high-precision automation for manufacturing, logistics, and life sciences, with Python support for seamless integration.

Companies Covered in Polyfunctional Robots Market

- FANUC Corporation

- ABB Ltd.

- Yaskawa Electric Corporation

- KUKA AG

- Universal Robots (UR)

- Mitsubishi Electric Corporation

- Techman Robot Inc.

- Staubli Robotics

- Nachi-Fujikoshi Corp.

- Neura Robotics GmbH

- Doosan Robotics

- Epson Robotics

- Comau S.p.A.

Frequently Asked Questions

The global Polyfunctional robot market is projected to be valued at US$9.4 Bn in 2025.

The need for flexible automation to address labor shortages, increasing production complexity, and cost-efficiency is a key market driver.

The Polyfunctional robot market is poised to witness a CAGR of 14.7% from 2025 to 2032.

The rise of human-centric, non-industrial applications and Robotics-as-a-Service (RaaS) is lowering adoption costs and accelerating deployment, creating strong growth opportunities in service-oriented sectors.

FANUC Corporation, ABB Ltd., Yaskawa Electric Corporation, KUKA AG, Universal Robots (UR), and Mitsubishi Electric Corporation are among the leading key players.