- Plastics, Polymers & Resins

- Polyacetal Resins Market

Polyacetal Resins Market Size, Share, and Growth Forecast, 2026 – 2033

Polyacetal Resins Market by Resin Type (Homopolymer, Copolymer), Application (Automotive Components, Electrical & Electronics, Industrial Machinery Parts, Consumer Goods, Healthcare & Medical Devices, Others), End-User (Automotive, Electronics, Industrial Manufacturing, Consumer Products, Healthcare), and Regional Analysis for 2026-2033

Polyacetal Resins Market Share and Trends Analysis

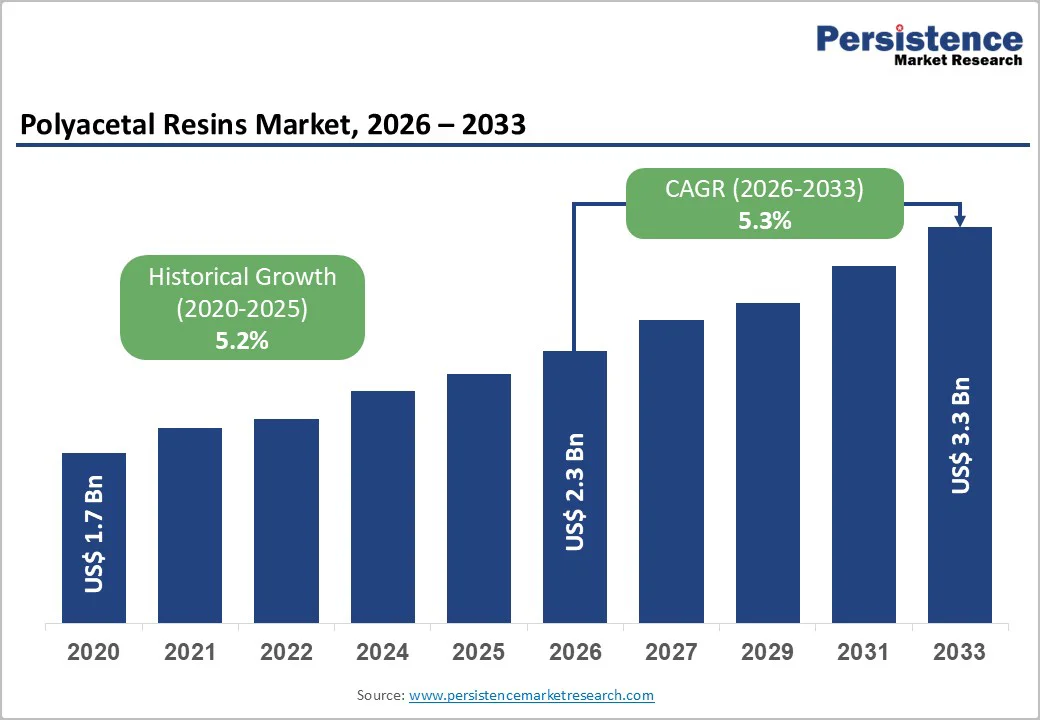

The global polyacetal resins market size is likely to be valued at US$ 2.3 billion in 2026 and is estimated to reach US$ 3.3 billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026−2033. Polyacetal resins, also known as polyoxymethylene (POM), offer high stiffness, excellent dimensional stability, low friction, and strong mechanical properties. These characteristics make them essential in precision engineering applications across automotive, electronics, industrial, and healthcare sectors. In automotive manufacturing, lightweighting trends drive fuel efficiency and emissions compliance, boosting the demand for durable polymer components. Rapid electrification and miniaturization in electronics further increase the need for precise, wear-resistant parts. Industrial machinery and consumer appliances are increasingly adopting these resins as manufacturers seek materials that outperform metals and conventional plastics in durability, longevity, and performance, reinforcing their role as a key engineering polymer.

Key Industry Highlights

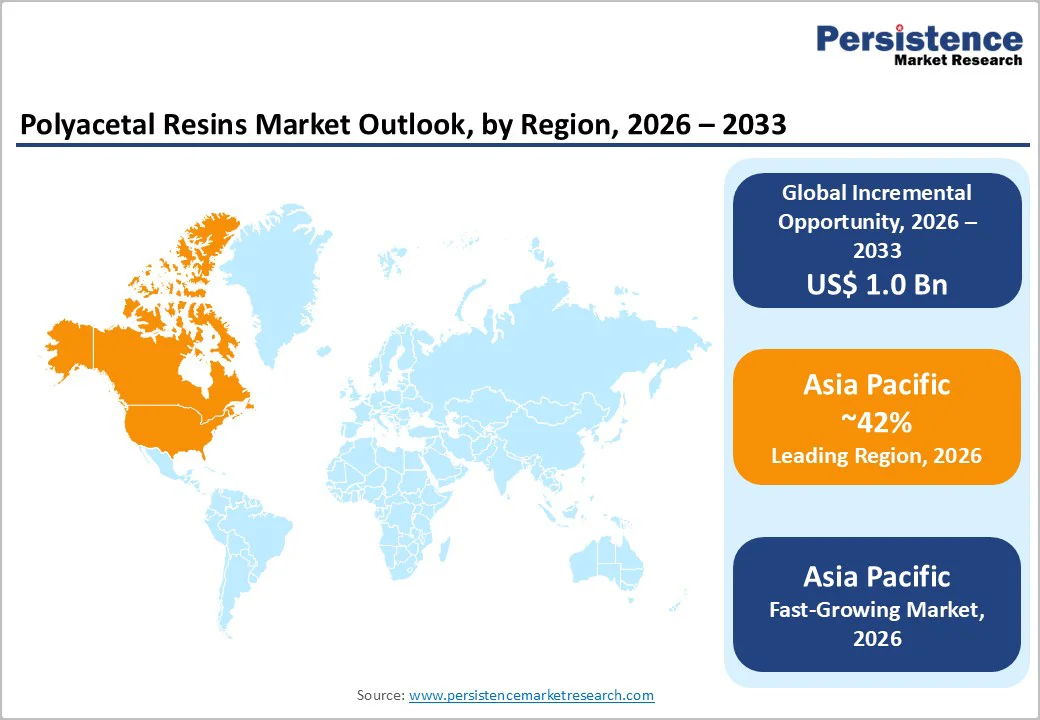

- Dominant Region: Asia Pacific is expected to lead the market in 2026 with around 42% share, supported by strong automotive, electronics, and industrial manufacturing activity.

- Fastest-growing Regional Market: Asia Pacific is projected to emerge as the fastest-advancing market between 2026 and 2033, propelled by rising automotive electrification, automation, and expanding electronics manufacturing.

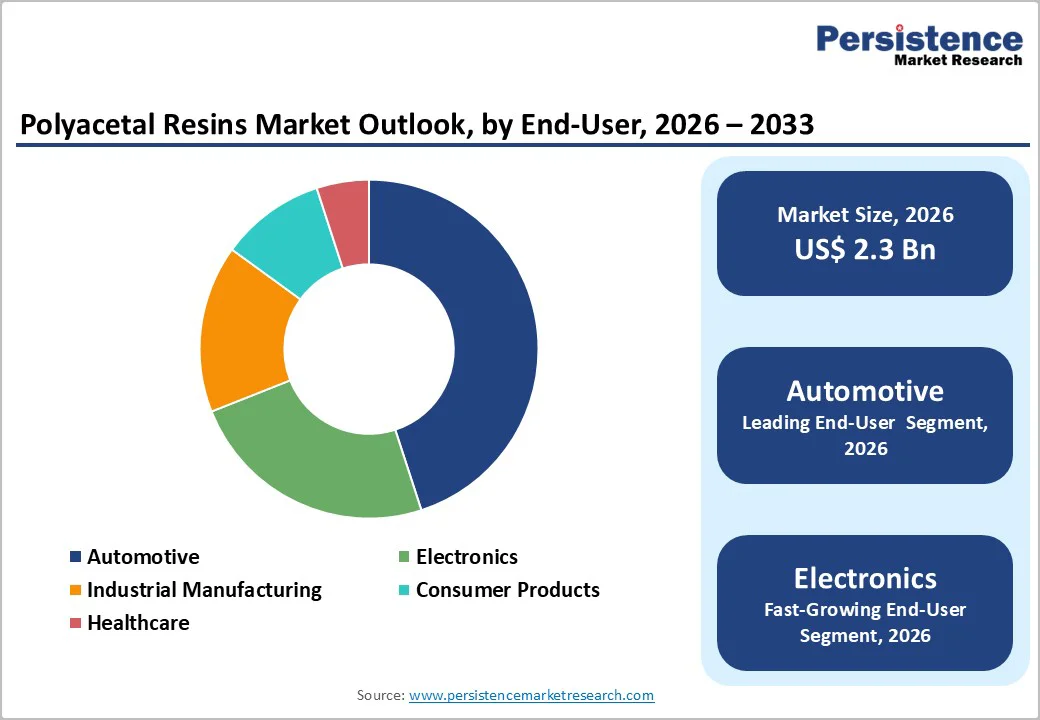

- Leading End-User: Automotive is poised to be the leading end-user with an estimated 45% revenue share in 2026, underpinned by high vehicle production and extensive use of polyacetal components.

- Fastest-growing End-User: Electronics is projected to be the fastest-growing end-user through 2033, driven by widespread device miniaturization trends.

| Key Insights | Details |

|---|---|

| Polyacetal Resins Market Size (2026E) | US$ 2.3 Bn |

| Market Value Forecast (2033F) | US$ 3.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Demand from the Automotive Sector

Increasing demand for robust polymers from the automotive sector drives the growth of polyacetal resins as manufacturers pursue lightweight, high-performance materials to meet stringent fuel efficiency and emissions standards. Automotive components such as fuel system parts, gears, bearings, and interior fittings require materials that maintain dimensional stability under temperature fluctuations and resist wear over long operational lifespans. Polyacetal resins provide low friction, high stiffness, and excellent chemical resistance, making them ideal for replacing metals in precision components while reducing overall vehicle weight. Lightweighting initiatives have shown potential to improve fuel efficiency by up to 10%, creating strong incentives for polymer adoption in engine, transmission, and structural parts.

Electrification trends and the rise of electric vehicles amplify demand for durable, precise, and thermally stable materials. Electric drivetrains and battery systems require components that endure repeated mechanical stress without compromising performance. Compact electronic modules and advanced sensor systems in modern vehicles depend on resins that combine mechanical strength with low friction and minimal thermal expansion. High adoption of these materials in automotive production lines reflects their ability to enhance efficiency, reliability, and longevity of vehicle components, positioning them as a critical solution for the evolving requirements of next-generation automotive manufacturing.

Regulatory Hurdles on Emissions and Sustainability

Strict implementation of emissions and sustainability regulations significantly limits the polyacetal resins market growth. The nature of these regulations is based on the reduction of carbon footprint and adherence to sustainability standards across manufacturing processes. Production of polyacetal resins involves formaldehyde-based polymerization, which emits volatile organic compounds (VOCs) and requires careful handling of chemical precursors. Compliance with emission limits increases operational complexity and production costs for manufacturers, affecting profitability and pricing competitiveness. Companies face investment requirements for emission control technologies, waste management systems, and sustainable raw material sourcing to meet regulatory standards.

Sustainability expectations also drive a shift toward bio-based and recyclable alternatives in automotive, electronics, and industrial applications. Customers are increasingly selecting materials that align with circular economy principles and low environmental impact. Pressure from regulators and end-users encourages manufacturers to innovate in product formulations and supply chain practices. Delays in approvals or failure to meet compliance can limit market access in key regions, restricting adoption of traditional polyacetal resins and slowing expansion in high-demand applications.

Technological Innovation and Bio?based Resin Development

Technological innovation drives opportunities in polyacetal resins by enabling the development of advanced formulations with enhanced performance characteristics. Improvements in polymer processing, stabilization, and blending techniques allow production of materials with superior thermal resistance, chemical stability, and mechanical strength. These advancements expand applications in high-precision industries such as automotive, electronics, and healthcare, where durability, accuracy, and reliability are critical. Innovations in additive integration and surface modification enhance wear resistance and friction performance, meeting evolving industry demands for lightweight and energy-efficient components. Continuous research into high-performance grades and custom formulations positions polyacetal resins as a strategic solution for engineering challenges that require both precision and scalability.

Bio?based resin development presents a strategic growth avenue by aligning materials with sustainability and environmental regulations. Development of renewable-source polyacetal alternatives reduces dependency on fossil-based feedstock and supports carbon footprint reduction goals for manufacturers. Adoption of bio-based variants resonates with environmentally conscious stakeholders and regulatory compliance initiatives in automotive and consumer sectors. Integration of sustainable production techniques and green chemistry principles enhances competitiveness, offering materials that deliver high performance while meeting emerging eco-friendly standards. Investment in bio-based innovations strengthens supply chain resilience and positions products as forward-looking solutions in industries emphasizing circular economy and responsible material sourcing.

Category-wise Analysis

Resin Type Insights

Homopolymer resin is likely to be the leading segment with a projected 55% of the polyacetal resins market revenue share in 2026 due to its superior mechanical strength, high tensile properties, and excellent dimensional stability. These characteristics make it ideal for high-performance automotive components such as gears and fuel system parts, where precision and durability under dynamic loads are critical. Industrial machinery and precision engineering applications also prefer homopolymer grades for components requiring tight tolerances and long service life. Widespread adoption across sectors, driven by reliability and consistent performance reinforces its position as the dominant product type.

Copolymer resin is anticipated to be the fastest-growing segment from 2026 to 2033 due to enhanced thermal and chemical resistance. Its properties suit demanding environments and emerging applications, including 5G infrastructure components, high-temperature electronics, and medical devices that require sterilization resistance. Innovations in formulation improve processability and enable sustainable production, meeting evolving industry standards. Companies increasingly adopt copolymer grades for applications where resilience, performance, and adaptability are critical, supporting rapid expansion across automotive, electronics, and healthcare sectors.

Application Insights

Automotive components are projected to hold 45% of the market revenue share in 2026, supported by high-volume vehicle manufacturing and continuous material substitution initiatives. Polyacetal resins support lightweighting strategies by replacing metal parts without compromising mechanical strength, dimensional stability, or chemical resistance. These properties enable widespread use in fuel system components, door locks, window regulators, and seat adjustment mechanisms. Adoption of polyacetal gears and clips in compact passenger vehicles, improving fuel efficiency, reducing assembly complexity, and enhancing long-term durability under repetitive mechanical stress.

Electrical and electronics is estimated to be the fastest-growing segment from 2026 to 2033, underpinned by rapid miniaturization and rising demand for precision-engineered components. Polyacetal resins deliver low friction, high dielectric strength, and excellent wear resistance, making them suitable for connectors, switches, and relay housings. Growth is further reinforced by expansion of consumer electronics manufacturing, smart appliances, and industrial automation systems. A representative example includes increasing use of polyacetal micro-connectors in smartphones and power distribution units, where consistent performance, tight tolerances, and resistance to thermal cycling are critical for operational reliability.

End-User Insights

The automotive end-user segment is slated to hold a dominant position, with an anticipated 45% of the polyacetal resins market revenues in 2026, supported by sustained global vehicle production and standardized component platforms. Polyacetal resins are widely integrated into fuel systems, safety mechanisms, and interior assemblies due to high mechanical strength, dimensional stability, and resistance to chemicals. Long vehicle development cycles promote material continuity across model generations. A valid example includes widespread use of polyacetal clips, gears, and fasteners in mass-market passenger vehicles, ensuring predictable demand volumes and cost-efficient manufacturing at scale globally.

The electronics segment is forecasted to be the fastest-growing between 2026 and 2033, boosted by accelerated innovation cycles and rising performance expectations across consumer and industrial devices. Miniaturization trends increase reliance on precision polymers that deliver low friction, electrical insulation, and wear resistance. Polyacetal resins support connectors, switches, and micro-gears operating under tight tolerances. A representative example includes deployment of polyacetal components within smartphone charging interfaces and automated control modules, where durability under thermal cycling and repetitive motion supports reliability benchmarks across high-speed data transmission and power management applications environments.

Regional Insights

North America Polyacetal Resins Market Trends

North America is estimated to remain a significant market for polyacetal resins, underpinned by advanced automotive and industrial manufacturing sectors. Established original equipment manufacturer (OEM) and Tier 1 supplier clusters in the United States, Canada, and Mexico integrate engineering polymers into fuel systems, door mechanisms, and interior assemblies. Focus on vehicle lightweighting and fuel efficiency drives substitution of metals with polyacetal resins. The market also includes mature electronics and industrial equipment production, where resins are used in precision connectors, switches, and gears. A representative example is extensive use of polyacetal gears in electric and hybrid vehicle assemblies, ensuring durability and reduced maintenance.

The North America market is expected to undergo steady growth, stimulated by electrification, automation, and advanced electronics adoption. Expansion of electric vehicle production, industrial robotics, and smart manufacturing systems drives demand for polymers offering dimensional stability, wear resistance, and thermal tolerance. Polyacetal resins are widely used in actuator systems and micro-connectors operating under repetitive motion and high-speed cycles. A representative example includes integration in electric vehicle charging infrastructure and industrial automation modules, where reliability is critical. Investments in research and development and manufacturing upgrades reinforce North America as a strategic growth market.

Europe Polyacetal Resins Market Trends

Europe is predicted to maintain a prominent share of the polyacetal resins market in 2026, anchored by well-established automotive and industrial manufacturing hubs. Key clusters in Germany, France, and Italy utilize polyacetal resins in fuel systems, door mechanisms, interior assemblies, and precision gears. Focus on vehicle lightweighting, energy efficiency, and strict regulatory compliance promotes replacement of metals with engineering polymers. Polyacetal resins also enhance performance in industrial equipment, including pumps, valves, and conveyor components.

The market in Europe is set to experience steady expansion, propelled by growth in electric vehicle production, industrial automation, and smart manufacturing deployment. Polyacetal resins are favored for actuator systems, micro-gears, and connectors functioning under high-speed cycles and thermal fluctuations. Rising adoption of electrified transport and renewable energy technologies increases demand for polymers with dimensional stability and wear resistance. Integration of polyacetal components in electric mobility platforms and automated production systems, where durability and consistent performance are critical. Investments in research and development, technology upgrades, and production optimization reinforce Europe as a strategic, resilient market.

Asia Pacific Polyacetal Resins Market Trends

Asia Pacific is positioned to dominate in 2026, capturing an estimated 42% of the polyacetal resins market share, reflecting structural advantages embedded across regional manufacturing ecosystems. The region hosts a dense concentration of automotive component suppliers, electronics assemblers, and industrial equipment producers that rely on engineering polymers for high-volume precision applications. Localized production of polyacetal resins reduces logistics complexity and shortens supply cycles, improving cost efficiency for downstream manufacturers. Government-supported industrial clusters across the region accelerate adoption of advanced thermoplastics in fuel systems, connectors, and motion-control components. A valid example includes the extensive use of polyacetal gears and sliding elements in large-scale automotive assembly operations, where scale-driven procurement and standardized specifications sustain consistently high material consumption.

Beyond current leadership, Asia Pacific is also forecast to emerge as the fastest-growing market through 2033, fueled by rapid automotive electrification, automation investments, and electronics capacity additions. Accelerated deployment of electric vehicles, robotics, and smart manufacturing systems increases demand for polymers offering dimensional stability, fatigue resistance, and low friction under continuous operation. Polyacetal resins gain preference in applications requiring tight tolerances and extended service life under thermal variation. Increasing integration of polyacetal actuator components and precision connectors in electric vehicle production facilities across India and Southeast Asia, where manufacturing upgrades and export-oriented capacity expansions drive sustained incremental demand beyond replacement-based consumption.

Competitive Landscape

The global polyacetal resins market exhibits a moderately consolidated structure, with multinational leaders such as Celanese Corporation, BASF, DuPont, Mitsubishi Gas Chemical Company, Inc., and Polyplastics Co., Ltd. controlling a substantial portion of worldwide production capacity. These corporations deploy sophisticated research and development (R&D) capabilities, proprietary process technologies, and extensive manufacturing footprints to serve demanding applications in automotive components, electronic housings, and precision industrial parts. Their scale advantages enable consistent quality, technical support, and supply reliability that critical end-users require. Regional producers occupy a different competitive space, focusing on price-sensitive segments, localized distribution, and niche applications where customization or proximity outweighs brand recognition.

Leading producers maintain their dominance through deliberate portfolio expansion, capacity investments in high-growth regions, and collaborative agreements that extend their reach into emerging and established markets. Continuous material innovation drives differentiation, as formulators develop grades with enhanced impact resistance, dimensional stability, or specialized additives that address evolving regulatory and performance standards. Companies that align product roadmaps with automotive lightweighting trends, electronics miniaturization, and industrial automation can command premium pricing and secure long-term supply agreements. For buyers and downstream manufacturers, partnering with established resin suppliers offers access to technical expertise, application development support, and supply chain resilience, while engaging regional suppliers can provide cost advantages and faster responsiveness for specific projects or geographies.

Key Industry Developments

- In October 2025, Asahi Kasei's polyacetal resin TENAC™-C ISCC PLUS certified grade was adopted by Takigen Manufacturing for its Bio-Resin Flat Torque Hinge.

The mass-balance polyacetal material reduces carbon footprint by approximately 50% compared to conventional petrochemical-derived resins while maintaining equivalent physical properties. - In October 2025, Polyplastics Group launched DURAST® Powder technology, producing fine, uniform resin powders for 3D printing and high?precision manufacturing, expanding applications in advanced engineering plastics.

- In May 2025, China imposed anti-dumping duties on polyacetal resin imports for five years, hitting Celanese's United States operations hardest at 74.9%. The duties target a market that imported approximately 427,000 tons of POM in 2024, with South Korea leading as the primary supplier, followed by Malaysia and the United States, as China accounts for more than half of global polyacetal demand.

Companies Covered in Polyacetal Resins Market

- Celanese Corporation

- BASF

- DuPont

- MITSUBISHI GAS CHEMICAL COMPANY, INC

- Polyplastics Co., Ltd.

- KEP.

- Asahi Kasei Corporation.

- SABIC

- LG Chem.

- Kolon ENP

Frequently Asked Questions

The global polyacetal resins market is projected to reach US$ 2.3 billion in 2026.

Growth in automotive, electrical and electronics, and industrial applications requiring high-strength, low-friction, and durable polymers are driving the market.

The market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Increasing deployment of lightweight automotive components, miniaturization of electronics, and development of sustainable, recyclable polyacetal applications are opening high-value market opportunities.

Celanese Corporation, BASF, DuPont, Mitsubishi Gas Chemical Company, Inc., Polyplastics Co., Ltd., and KEP are some of the key players in the market.