- Off-Road Equipment & Machinery

- Plowing and Cultivating Machinery Market

Plowing and Cultivating Machinery Market Size, Share, and Growth Forecast, 2026 - 2033

Plowing and Cultivating Machinery Market by Product Type (Plows, Cultivators & Tillers, Others), Power Source (Tractor-mounted, Others), Technology Type (Conventional, Others), Application (Land Preparation, Others), and Regional Analysis 2026 - 2033

Plowing and Cultivating Machinery Market Size and Trends Analysis

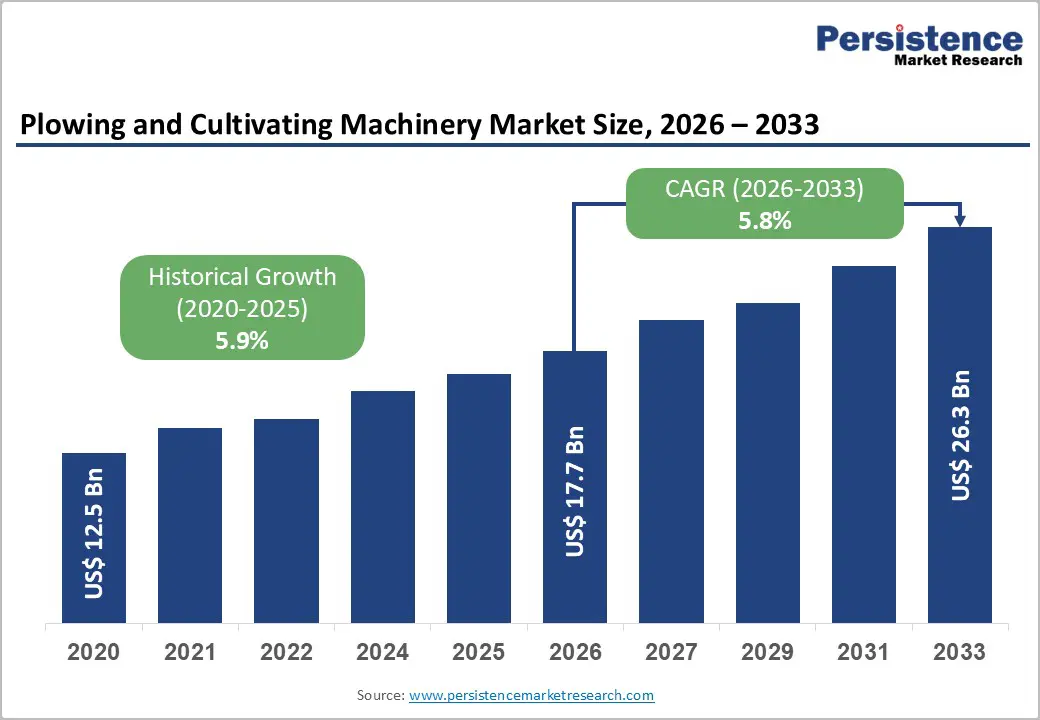

The global plowing and cultivating machinery market size is likely to be valued at US$17.7 billion in 2026 and is expected to reach US$26.3 billion by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033, driven by the accelerating adoption of precision agriculture technologies, including GPS-integrated and autonomous machinery, which optimize soil health and operational efficiency.

A critical global shortage of agricultural labor is also compelling farm owners to transition from manual or semi-mechanized methods to fully automated and high-capacity cultivating solutions. Adoption of precision agriculture technologies, including GPS-guided systems, boosts productivity while reducing inputs, supported by government subsidies.

Key Industry Highlights:

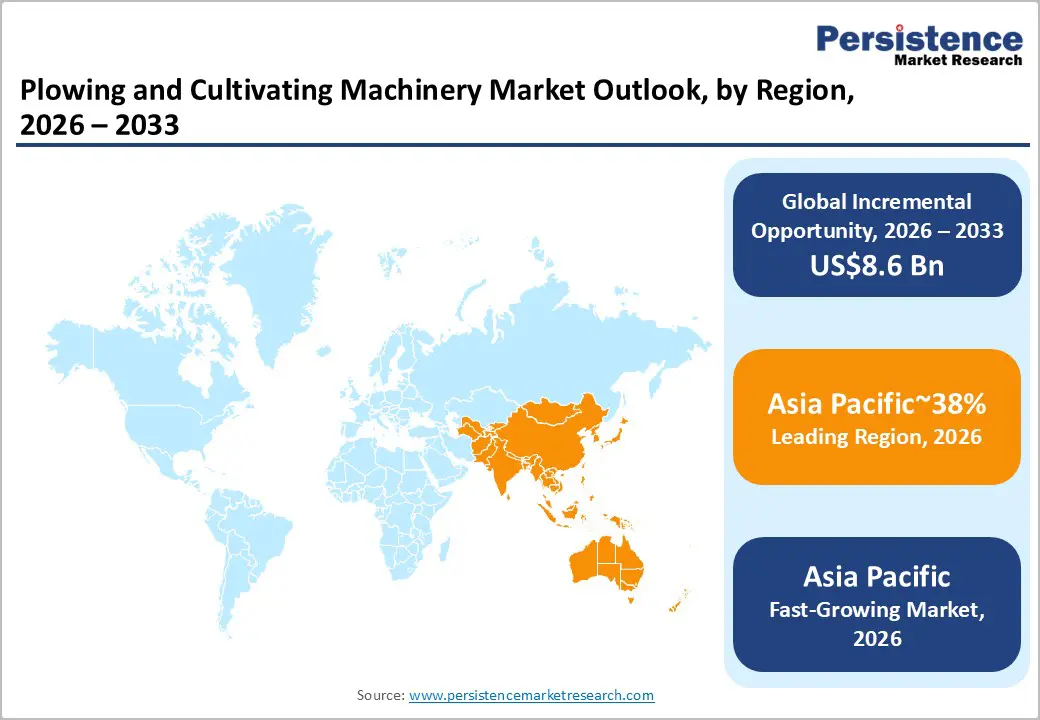

- Leading Region: Asia Pacific is projected to lead due to strong agricultural mechanization demand, expanding cultivated land intensity, and government-backed farm modernization initiatives, accounting for approximately 38% share.

- Fastest-growing Region: Asia Pacific, due to rapid industrialization of agriculture, policy-backed equipment financing, and increasing mechanization across small and medium farms.

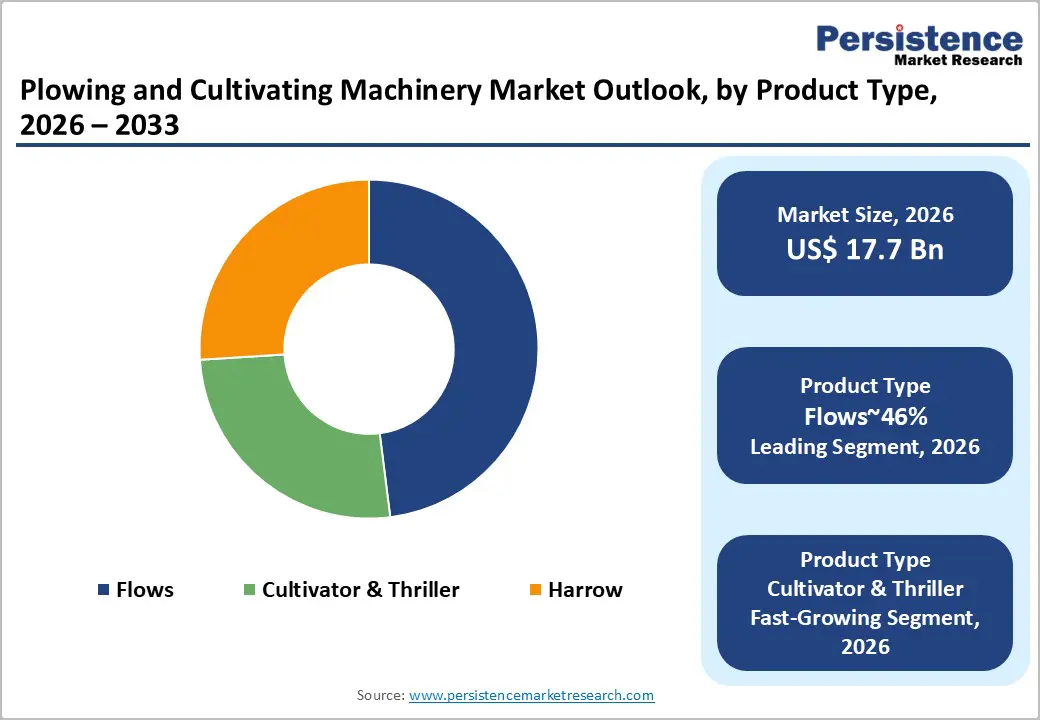

- Leading Product Type Segment: Plows are expected to lead, accounting for approximately 46%, supported by their foundational role in primary tillage, soil turnover efficiency, and widespread adoption across large-scale farming operations.

- Leading Power Source Segment: Tractor-mounted machinery is projected to dominate for operational simplicity, cost-efficiency, and broad compatibility across farm sizes, holding approximately 72% share.

| Key Insights | Details |

|---|---|

|

Plowing and Cultivating Machinery Market Size (2026E) |

US$17.7 Bn |

|

Market Value Forecast (2033F) |

US$26.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Adoption of Precision Agriculture and Soil Health Focus

The rapid integration of precision agriculture technologies is structurally redefining demand dynamics in the cultivating machinery market. Modern equipment increasingly incorporates ISOBUS connectivity, GPS guidance, and real-time soil sensing, transforming implements into data-driven platforms capable of site-specific tillage execution. By modulating cultivation intensity according to soil compaction and residue conditions, these systems directly align with regenerative agriculture frameworks and soil health preservation mandates. This evolution elevates machinery from standardized mechanical assets to intelligent agronomic infrastructure, increasing value per unit and reinforcing demand for higher-specification components, embedded electronics, and software-enabled control architectures across the agricultural equipment value chain.

From a regulatory and cost-structure standpoint, sustainability-linked subsidy regimes in Europe and North America strengthen the investment case for advanced machinery by partially offsetting capital outlays. GPS-integrated systems, representing a meaningful installed base, reduce fuel consumption through minimized overlap and controlled field passes, lowering operating expenditure while mitigating soil degradation risks. As compliance, efficiency, and environmental performance become procurement criteria, manufacturers face rising R&D intensity and integration complexity, but benefit from margin accretion tied to technology-enabled differentiation and recurring data-driven service ecosystems.

Increasing Food Demand and Farm Mechanization

Rising global food requirements driven by demographic expansion are structurally intensifying pressure on agricultural productivity, accelerating the transition from labor-intensive practices toward mechanized cultivation systems. Limited availability of arable land constrains horizontal expansion, compelling producers to improve yield per hectare through precision soil preparation and optimized field operations. Mechanized plowing and cultivation enhance soil aeration, residue incorporation, and depth consistency, directly influencing crop establishment and input efficiency. As rural labor availability tightens and wage pressures rise, mechanization becomes an economic imperative rather than a discretionary upgrade, embedding farm machinery deeper into primary production value chains.

At the market level, public subsidy frameworks and rural modernization programs in emerging economies lower capital barriers for equipment acquisition, reinforcing equipment penetration across small and mid-sized holdings. Increased mechanization intensity expands demand not only for primary implements but also for maintenance services, replacement parts, and financing solutions, broadening the revenue base across upstream manufacturing and downstream aftermarket ecosystems. Regulatory emphasis on food security and sustainable land management further supports investment in efficient cultivation technologies, structurally linking agricultural output targets with sustained demand for mechanized field equipment across diverse regional markets.

Barrier Analysis - Abrasive Soil Conditions and Elevated Total Cost of Ownership

Abrasive and rocky soil profiles present a structural constraint for the plowing and cultivating machinery market. Implements such as plowshares, discs, and tines operate under continuous mechanical stress and frictional wear, making them inherently high-consumption components. In geographies characterized by coarse-textured soils, gravel content, or subsurface rock fragments, wear rates accelerate significantly, increasing replacement frequency and maintenance cycles. This directly inflates the total cost of ownership, particularly for small and mid-sized farm operators with limited capital buffers.

The restraint intensifies as equipment complexity increases. Modern integrated machinery, equipped with precision depth controls, hydraulic systems, and sensor-based optimization modules, relies on specialized, high-grade alloy or composite wear parts. These components carry higher procurement costs and may face supply chain constraints in developing agricultural markets. As a result, farmers in abrasive-soil regions often defer upgrading to advanced systems, favoring simpler, modular equipment with lower replacement costs and easier part availability. This dynamic moderates technology adoption rates and creates a persistent price-sensitivity barrier within high-wear agricultural zones.

Shift Toward No-Till and Conservation Farming Practices

The global transition toward Conservation Agriculture is structurally constraining demand for conventional plowing and heavy cultivation equipment. No-till and reduced-till frameworks prioritize minimal soil disturbance to mitigate erosion, preserve soil structure, and limit carbon release from intensive mechanical turnover. As environmental policy increasingly links agricultural practices to climate mitigation targets, regulatory incentives and carbon-credit mechanisms are reinforcing the adoption of low-disturbance farming systems. This realignment weakens replacement cycles for traditional moldboard plows and deep-tillage cultivators, compressing volume visibility across legacy product categories within the primary tillage equipment value chain.

At the market level, the shift rebalances capital allocation from high-horsepower tillage implements toward seeding, residue management, and precision nutrient placement systems compatible with conservation regimes. Equipment manufacturers with portfolios concentrated in conventional plowing face structural demand erosion and heightened price competition in mature regions where sustainability compliance is institutionalized. Simultaneously, compliance-driven agronomic standards elevate technology integration costs for remaining tillage applications, tightening margins in a segment already exposed to cyclical farm income volatility and extended machinery replacement intervals.

Opportunity Analysis - Integration of AI-Based Weed Recognition and Targeted Mechanical Weeding

The convergence of herbicide resistance and tightening agrochemical regulations is structurally expanding the addressable market for intelligent mechanical weeding systems. AI-enabled vision modules integrated into cultivators can differentiate crops from weeds in real time, enabling selective, high-speed physical removal without blanket chemical application. This transforms conventional row-crop cultivators into precision agronomic platforms that combine mechanical actuation with machine vision, edge processing, and algorithmic crop recognition. The resulting value proposition aligns with sustainability mandates, residue reduction targets, and regulatory scrutiny of synthetic herbicide usage across major agricultural regions.

The integration of camera arrays, processing units, and responsive actuation systems increases component intensity and elevates the technological content per implement. This shifts competitive positioning from purely mechanical fabrication toward software-hardware integration and data-driven performance optimization. As environmental compliance and input-cost volatility reshape farm economics, demand migrates toward solutions that reduce chemical dependency while preserving yield integrity, expanding margin pools for suppliers capable of delivering reliable, field-validated AI-enabled cultivation architectures.

Expansion into Soil Health Sensing Implements

The plow represents a strategically positioned platform for subsurface data acquisition, as it consistently engages with deeper soil strata during primary tillage operations. Integrating real-time soil sensing technologies within plowshares or tines enables continuous measurement of critical agronomic parameters such as nitrogen, phosphorus, potassium, moisture content, and pH levels. This “mapping-while-plowing” capability transforms conventional tillage equipment into an intelligent agronomic interface, generating high-resolution field data without requiring additional field passes.

This opportunity aligns directly with precision agriculture frameworks that prioritize data-driven input optimization. By embedding sensors within cultivating implements, manufacturers can position plows as dual-function assets combining mechanical soil preparation with diagnostic intelligence. The resulting geospatial datasets support variable-rate fertilization strategies in subsequent crop cycles, improving nutrient-use efficiency and reducing input waste. For equipment OEMs, this integration creates differentiation beyond hardware durability, enabling value capture through data services, software compatibility, and interoperability with farm management platforms. This convergence of mechanical engineering and agronomic analytics strengthens the plow’s role within digitally integrated farming ecosystems.

Category-wise Analysis

Power Type Insights

Tractor-mounted is expected to lead, accounting for approximately 72% share in 2026, anchored in the universal installed base of agricultural tractors across global farming systems. This modularity enables farmers to rotate implements seasonally while retaining one core power unit, sustaining volume demand in both smallholder and commercial settings. Technology upgrades such as ISOBUS Class 3 control logic and hybrid ePTO systems such as John Deere eAutoPowr enhance precision and energy efficiency within mounted configurations. Established manufacturers, including Kuhn Group, Kverneland Group, and LEMKEN, continue to expand advanced mounted portfolios, reinforcing ecosystem lock-in and long-term service cycles.

Self-propelled is expected to be the fastest-growing segment, driven by large-scale farm consolidation, shrinking cultivation windows, and rising labor constraints. Integrated power-and-implement architectures optimize traction, stability, and field speed, enabling high-capacity tillage beyond conventional tractor-mounted limitations. Purpose-built chassis designs with distributed weight systems minimize field pressure and enhance soil stewardship, shifting procurement preferences among commercial operators. Autonomous and cab-less platforms from innovators such as HORSCH and AgXeed accelerate the adoption of swarm-based cultivation models. Modular carrier concepts such as those advanced by Nexat further integrate plow, seeder, and crop-care modules into a unified system, positioning self-propelled platforms to outpace overall market expansion.

Product Type Insights

Plows are expected to lead, accounting for approximately 46% share in 2026, supported by their central role in primary tillage across heavy-soil cereal systems. Their structural relevance stems from deep-soil inversion capability, residue burial efficiency, and durability under continuous high-load operations on expanding farm sizes. Large-scale operators prioritize plows for predictable soil turnover and pest management, particularly in mechanized regions with consolidated acreage. Ongoing modernization through automated depth control and digital tillage integration strengthens replacement cycles and equipment longevity. Manufacturers such as John Deere, Kuhn Group, Kverneland Group, and LEMKEN continue to refine high-durability steel frames and precision-guided plowing systems. This installed base strength and operational indispensability sustain plows as the value anchor of structured tillage programs.

Cultivators & tillers are expected to be the fastest-growing segment, driven by rising demand for secondary tillage, weed control, and soil aeration in diversified cropping systems. Farmers increasingly favor precision cultivators that enhance germination conditions without aggressive soil inversion, aligning with conservation-oriented field practices. Growth is reinforced by AI-enabled smart weeding, GPS-integrated depth stabilization, and electric power platforms suited for smallholder and horticultural settings. Companies including Kubota, Mahindra & Mahindra, VST Tillers Tractors, and AGCO Corporation are scaling rotary tillers, compact cultivators, and electrified variants to address labor shortages and fuel efficiency mandates. As digital farm management platforms integrate directly with field implements and mechanization deepens across labor-constrained regions, cultivators and tillers are gaining structural momentum in mainstream farm operations. Their alignment with precision weeding, soil aeration optimization, and autonomous functionality positions them to expand faster than traditional primary tillage equipment.

Regional Insights

Asia Pacific Plowing and Cultivating Machinery Market Trends

Asia Pacific is expected to remain the leading and fastest-growing region, accounting for approximately 38% in 2026, supported by expansive arable land concentration and accelerating mechanization intensity. Structural demand is projected to strengthen as governments advance farm modernization policies to offset rural labor contraction and enhance productivity per hectare. Large-scale agricultural activity in China and India is anticipated to sustain high-volume equipment absorption across primary and secondary tillage categories. Simultaneously, regional manufacturing depth is positioned to reinforce supply resilience through localized production of tractor-mounted implements and precision cultivation systems. Technology diffusion, including GPS-enabled depth control and sensor-integrated soil preparation tools, is set to elevate equipment sophistication while maintaining cost competitiveness. This alignment between scale economics, policy incentives, and industrial capability positions Asia Pacific at the center of global volume and growth momentum.

China is expected to anchor regional expansion as land consolidation policies and cooperative farming structures enable the adoption of higher-capacity, technology-integrated machinery platforms. Domestic manufacturers such as Kubota and regional equipment producers are anticipated to scale autonomous tillers and precision-mounted implements tailored to diversified crop systems. Industrial policy emphasis on domestic production of advanced implements is projected to reduce import dependence while strengthening export competitiveness within Southeast Asia. Investment flows are likely to prioritize precision cultivation, electrified tillers, and digitally connected platforms aligned with smart agriculture initiatives. As enterprise-scale farms expand and equipment financing ecosystems mature, China is positioned to shape regional technology standards and vendor strategies, reinforcing Asia Pacific’s dual role as both demand epicenter and innovation accelerator.

North America Plowing and Cultivating Machinery Market Trends

North America is expected to remain a structurally advanced and innovation-led market, supported by large-scale commercial farming and high precision-technology penetration. Demand is projected to remain anchored in high-horsepower tractors and ultra-wide implements engineered for expansive Midwestern and Prairie acreages. The region is positioned to prioritize productivity per labor unit, driving sustained integration of GPS guidance, variable-rate tillage, and real-time soil analytics into mainstream operations. Conservation-aligned field practices are anticipated to accelerate the adoption of vertical tillage and strip-till platforms that reduce disturbance intensity while preserving yield performance. A consolidated OEM ecosystem, led by companies such as John Deere and CNH Industrial, is set to reinforce platform interoperability and lifecycle service monetization across enterprise farms.

The U.S. is expected to anchor regional momentum as scale-driven farming models incentivize continuous equipment upgrading and digital retrofitting strategies. Retrofit autonomy solutions that integrate sensors, AI control modules, and machine vision into legacy tillage fleets are projected to extend asset life while enhancing operational precision. Federal conservation alignment is likely to further institutionalize reduced-disturbance systems, shaping procurement toward data-enabled strip-till and vertical tillage configurations. Investment flows are anticipated to concentrate on software-defined equipment architectures, enabling predictive diagnostics and remote calibration within farm management ecosystems. As enterprise growers pursue higher acreage efficiency and lower input volatility, the U.S. is positioned to define technology standards and vendor strategy across the broader North American market.

Europe Plowing and Cultivating Machinery Market Trends

Europe is expected to remain a mature and sustainability-driven market, supported by policy-aligned precision agriculture frameworks and premium implement manufacturing depth. Regional demand is projected to center on reduced-disturbance tillage, mechanical weeding, and carbon-conscious soil management systems aligned with the Common Agricultural Policy and Green Deal objectives. Mixed-farming structures are anticipated to sustain strong uptake of reversible plows, advanced power-harrows, and high-precision seedbed preparation equipment. Replacement cycles are set to accelerate as farmers transition toward ISOBUS-compatible machinery capable of seamless integration with digital farm management platforms. A concentrated ecosystem of high-specification implement producers, including LEMKEN, Amazone, and Kuhn Group, is positioned to reinforce Europe’s leadership in engineered tillage solutions and compliance-ready platforms.

Germany is expected to anchor regional momentum through its role as a manufacturing and engineering nucleus for precision implements and digitalized tillage systems. Industrial investment is likely to prioritize smart implementations capable of automated documentation, task mapping, and regulatory reporting integration within enterprise software ecosystems. Vendor strategies are anticipated to emphasize sensor-embedded plows and cultivators that optimize depth, fuel efficiency, and soil conditioning in real time. As sustainability-linked compliance frameworks intensify and farm consolidation gradually advances, Germany is positioned to shape equipment interoperability standards and export-oriented innovation across the broader European market.

Competitive Landscape

The global plowing and cultivating machinery market is moderately consolidated, with leadership concentrated among global suppliers such as John Deere, CNH Industrial, AGCO Corporation, Kubota, and Mahindra & Mahindra. Market power is reinforced through vertically integrated portfolios spanning tractors, mounted implements, precision software, and global dealer networks, enabling end-to-end procurement alignment for commercial farms. These leaders shape technology standards, interoperability protocols, and financing ecosystems, influencing replacement cycles and enterprise-level equipment standardization. Competitive positioning increasingly differentiates along digital integration depth rather than mechanical durability alone, with OEMs embedding ISOBUS compatibility, telematics, and data-driven soil optimization into core platforms.

Within the implement sub-segment, competitive intensity remains comparatively fragmented, particularly across European specialists such as LEMKEN, Kuhn Group, and Amazone, which compete on agronomic precision and engineered steel technologies. Industry dynamics are expected to favor ecosystem consolidation, retrofit autonomy upgrades, and software-defined equipment architectures that extend asset life cycles. Mergers, joint development programs, and platform alliances are positioned to accelerate as vendors seek to control data flows between tractor and implement, strengthening service-led revenue models and long-term customer lock-in.

Key Industry Highlights:

- In December 2025, CLAAS introduced the "XERION 12 Series" specialized for heavy-duty disc harrows. It featured a reinforced drawbar and hydraulic flow optimized for the largest cultivating implements in the North American market.

- In April 2025, CNH Industrial (Case IH) introduced the high-speed "Speed-Tiller 475" with updated disk technology. This upgrade enables effective residue management at speeds up to 10mph, significantly reducing the land preparation window.

- In January 2025, John Deere launched the 9RX series high-horsepower tractors with "Autonomy-Ready" tillage kits. Integrated sensors allow for real-time soil consistency mapping while plowing, optimizing fuel consumption by 15%.

Companies Covered in Plowing and Cultivating Machinery Market

- Deere & Company

- CNH Industrial

- AGCO Corporation

- Kubota

- Mahindra & Mahindra

- CLAAS

- LEMKEN

- Kuhn Group

- HORSCH

- Amazone

- Kverneland Group

- Great Plains Manufacturing

- Maschio Gaspardo

- Väderstad

- ISEKI

- Escorts Kubota Limited

Frequently Asked Questions

The global plowing and cultivating machinery market is projected to be valued at US$17.7 billion in 2026 and is expected to reach US$26.3 billion by 2033, driven by precision agriculture adoption, farm labor shortages, and the need to boost crop yields per hectare.

GPS-guided and ISOBUS-integrated machinery enables site-specific tillage, reducing input overlap and fuel consumption while improving soil health. This aligns with regenerative agriculture mandates and sustainability-linked subsidies, transforming machinery from mechanical assets into intelligent agronomic infrastructure that delivers measurable efficiency gains.

The plowing and cultivating machinery market is forecast to grow at a CAGR of 5.8% from 2026 to 2033, reflecting steady mechanization intensity and replacement demand across both developed and emerging agricultural regions.

Asia Pacific is both the leading and fastest-growing regional market, accounting for approximately 38% share, underpinned by large-scale government farm modernization programs, rising mechanization across India and China, and the need to offset rural labor contraction.

The market is moderately consolidated, with global leaders such as John Deere, CNH Industrial, AGCO Corporation, and Kubota dominating through vertically integrated tractor-implement-software portfolios. European specialists, including LEMKEN, Kuhn Group, and Väderstad, compete on agronomic precision and engineered durability in the implement sub-segment.