- Specialty & Fine Chemicals

- Pearlescent Pigment Market

Pearlescent Pigment Market Size, Share, and Growth Forecast, 2025 - 2032

Pearlescent Pigment Market By Product Type (Titanium-Dioxide Coated Mica, Ferric-Oxide Coated Mica, Others), Application (Paints & Coatings, Plastics, Others), End-user, and Regional Analysis for 2025 - 2032

Pearlescent Pigment Market Size and Trends Analysis

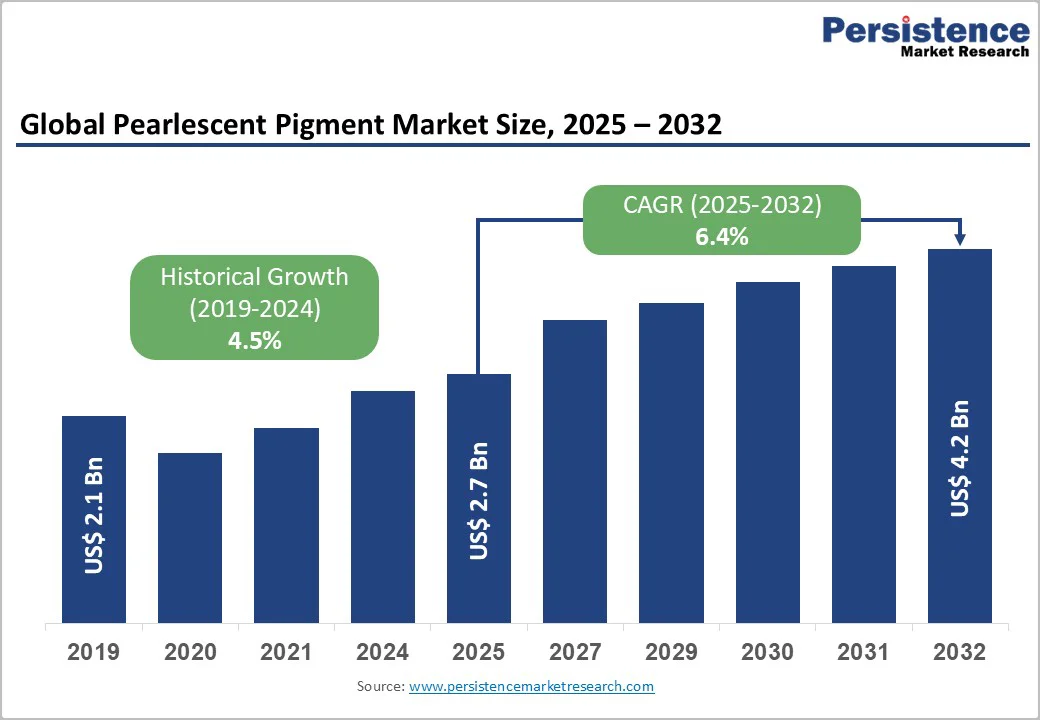

The global pearlescent pigment market is expected to reach US$2.7 billion in 2025. It is expected to reach US$4.2 billion by 2032, growing at a CAGR of around 6.4% over the forecast period from 2025 to 2032, driven by the specialty materials sector, which supplies high-value optical effects to industries such as automotive coatings, cosmetics, plastics, packaging, and industrial finishes.

Demand is rising as manufacturers seek advanced color styling, premium visual effects, and cleaner formulations. Growth is driven by the rapid adoption of advanced mica-based and synthetic substrates that offer higher chroma, heat stability, and sustainability while meeting stricter regulatory and consumer requirements for performance and traceability.

Key Industry Highlights

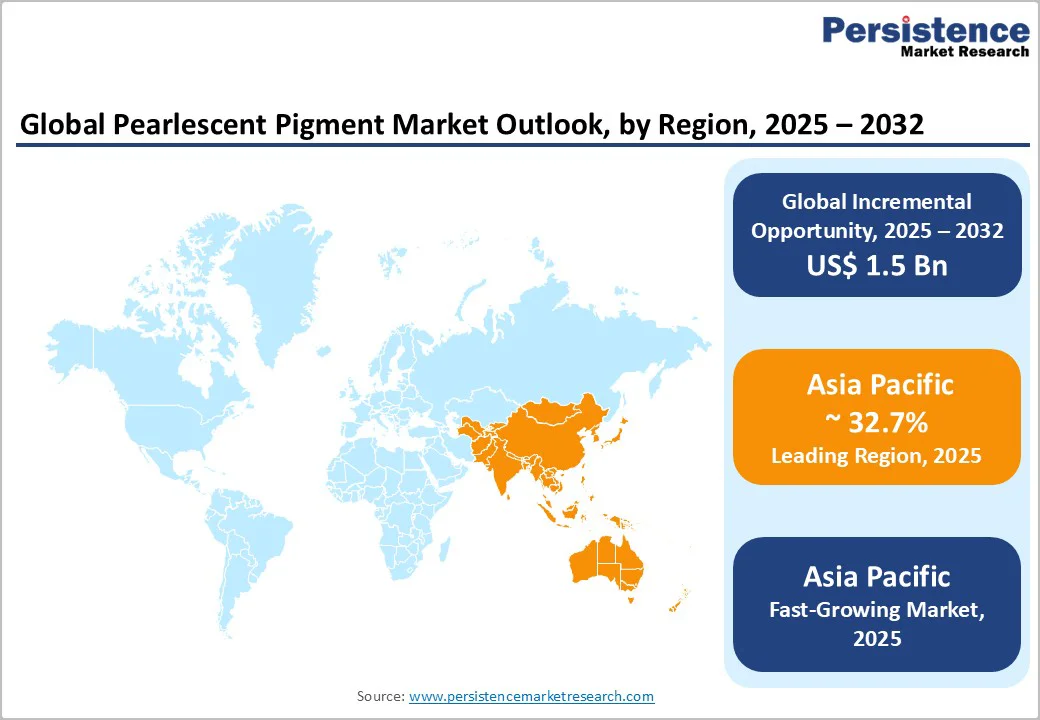

- Leading Region: Asia Pacific remains the largest regional market, accounting for approximately 32.7% of global revenue due to strong manufacturing scale in China, high-value demand from Japan, and rapid growth in India.

- Fastest Growing Region: Asia Pacific region leads growth, with India demonstrating some of the highest country-level expansion rates globally, often estimated in the high single to low double digit range due to rising cosmetics, coatings, and packaging consumption.

- Investment Plans: Manufacturers are increasing investments in synthetic mica capacity, high chroma engineered platelets, and sustainability-compliant production upgrades. Recent corporate activity includes expansions in Asia Pacific, new product launches for EV coatings, and clean beauty formulations.

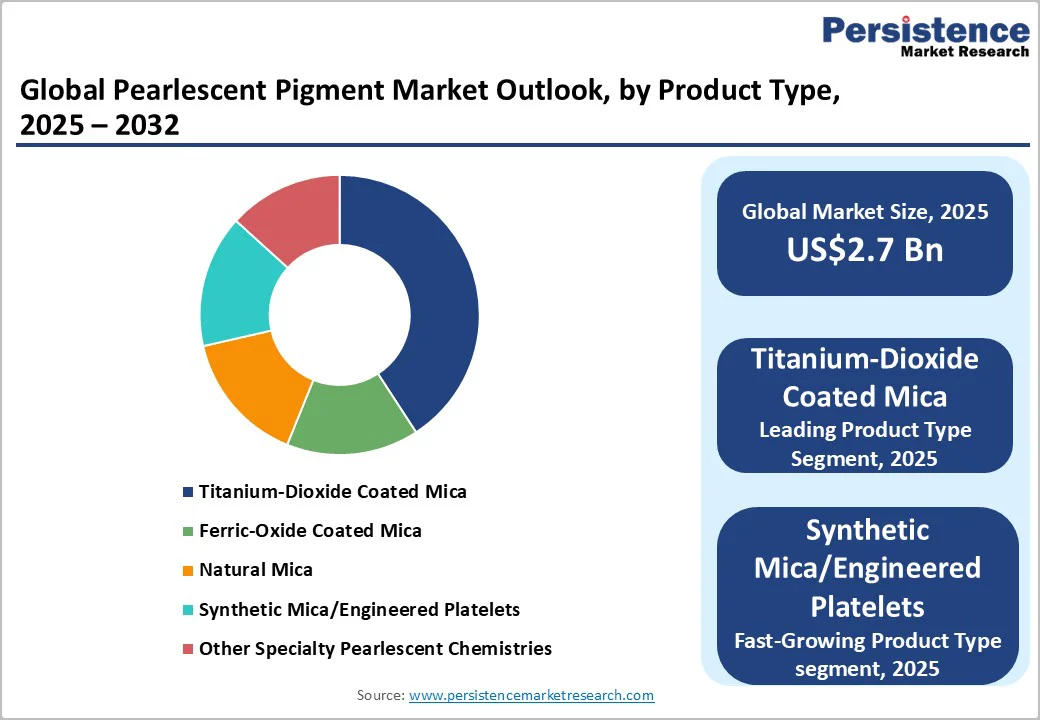

- Dominant Product Type: Titanium dioxide-coated mica remains the largest product type, representing close to 39.3% of market revenue. Its broad adoption across automotive, packaging, and high-end cosmetics maintains its leadership position.

- Leading Application: Paints and coatings remain the largest application segment, accounting for roughly 35.5% of total demand, supported heavily by automotive OEM finishes, refinish coatings, and premium architectural and industrial effects.

| Key Insights | Details |

|---|---|

| Market Size (2025E) | US$2.7 Bn |

| Market Value Forecast (2032F) | US$4.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Automotive Finishes and Personalization

Automotive OEMs continue expanding color and finish offerings, especially metallic and pearlescent whites, color-travel effects, and special-edition finishes. As global light-vehicle production stabilizes and gradually grows through the second half of the decade, pigment demand rises almost linearly with vehicle output and effect-finish take-rates.

Each vehicle finished with an effect coating requires significantly higher pigment loading than traditional solids, making this end-user one of the most volume-intensive and value-generating segments.

Expansion of Cosmetics, Personal Care, and Premium Packaging

Color cosmetics, personal-care formulations, hair-care products, and specialty soaps continue to adopt pearlescent effects for aesthetic differentiation. Growth in APAC’s beauty sector, combined with continued adoption of shimmer and highlighting trends, supports elevated demand.

Premium packaging, especially rigid containers, labels, and luxury goods, also contributes meaningfully. The increasing availability of natural-certified or solvent-free pearlers has further expanded adoption in clean-label formulations.

Material Innovation and Substitution

Advances in synthetic mica, engineered platelet technologies, and improved coating architectures (including surface-treated TiO2, iron oxides, and functional multi-layer systems) have elevated performance standards. These innovations improve heat resistance, chroma, dispersion, and unique visual effects such as interference color travel.

Technology upgrades command higher average selling prices and open new opportunities in plastics, e-mobility systems, consumer electronics, and radar-transparent pigments for emerging mobility applications.

Barrier Analysis - Raw Material and Ethical Sourcing Challenges

Natural mica, one of the primary substrates for pearlescent pigments, is associated with supply-chain risk in certain mining regions due to inconsistent traceability, labor concerns, and environmental effects. These issues pose reputational and compliance challenges for global brands.

Price volatility for natural mica and titanium dioxide periodically squeezes manufacturer margins. While synthetic mica reduces many of these concerns, it continues to cost more to produce than natural alternatives, limiting full substitution in cost-sensitive applications.

Inconsistent Market Definitions and Reporting

The market is fragmented in terms of how vendors categorize pearlescent pigments; some count only mica-based effect pigments, while others include pearlizers used in personal-care surfactants or metallic-interference systems. As a result, published global market sizes range from about US$2 Billion to more than US$4 Billion for similar years. This makes benchmarking and investment analysis challenging unless a single definitional scope is aligned upfront.

Opportunity Analysis - Synthetic Mica and Ethically Sourced Materials

Growing scrutiny on supply-chain ethics is prompting brands to shift toward certified natural mica or fully synthetic mica alternatives. Synthetic mica offers improved purity, thermal stability, and controlled particle geometry, enabling more consistent optical effects.

If ethical and synthetic grades capture even 10-15% additional market share through the decade, the incremental premium potential reaches several hundred million dollars globally. The highest growth in demand for traceable and sustainable pigment sources is emerging in APAC and Europe.

High-value Coatings for EVs and Consumer Electronics

Electric-vehicle manufacturers and consumer electronics brands seek signature finishes that enhance product differentiation. Pearlescent pigments, especially advanced interference and multi-layer platelets, support unique visual depth and color-shift properties

. Applications include EV exteriors, interior trim, chargers, housings, wearables, and premium accessories. Suppliers that achieve automotive-grade qualification or long-term electronics partnerships gain access to recurring multi-year contracts.

Category-wise Analysis

Product Type Insights

Titanium dioxide-coated mica remains the largest pearlescent pigment segment, accounting for 39.3% of the market, due to its versatile optical properties and consistent performance across applications. Its superior whiteness, brightness, and UV stability make it indispensable in automotive coatings, where pearlescent whites and silvers are top OEM color choices.

The pigment is highly valued in high-end cosmetics, adding refined shimmer to pressed powders, liquid highlighters, foundations, and radiance-focused skincare. In plastics, it provides decorative appeal and heat resistance for molded consumer goods, including appliance housings, electronics, compact cases, and luxury packaging.

It also enhances visual impact in packaging applications, such as caps, rigid bottles, and specialty printing. Its ability to deliver consistent white and silver interference effects at competitive cost ensures continued high-volume adoption and reinforces its leading market position.

Synthetic mica and engineered platelets represent the fastest-growing segment, driven by superior purity, thermal stability, and precise particle-geometry control. They are ideal for high-performance plastics, specialty coatings, and e-mobility components exposed to heat and mechanical stress.

Synthetic mica is increasingly used in EV battery casings, connectors, and interior parts, while engineered platelets, such as PVD-coated and multilayer interference pigments, enable dramatic color-travel effects in luxury automotive finishes, gaming accessories, premium smartphones, and special-edition packaging. Ethical sourcing further boosts cosmetic adoption.

Application Insights

Paints and coatings remain the largest application segment, accounting for 35.5% of the pearlescent pigment market, driven by strong demand across automotive, architectural, industrial, and consumer goods sectors. Automotive OEM and refinish applications use substantial volumes of these pigments to achieve depth, sparkle, and refined interference effects in exterior body finishes, wheel coatings, and interior components.

In industrial coatings, pigments enhance the appearance of appliances, machinery, and electronics housings, helping manufacturers differentiate premium product lines. Architectural coatings also contribute significantly as designers incorporate pearlescent effects into decorative interior paints, feature walls, and high-end residential and commercial finishes.

Coatings typically require higher pigment loading than plastics, inks, or cosmetics, further boosting market value.

Cosmetics and personal care are the fastest-growing application category, fueled by global beauty trends favoring shimmer, glow, and multidimensional effects. Pearlescent pigments are widely used in highlighters, eyeshadows, lipsticks, lip glosses, blushes, nail lacquers, foundations, and complexion enhancers.

Clean beauty trends accelerate demand for synthetic mica and ethically sourced pigments. Pearlescent effects are also popular in shampoos, body washes, and hand soaps, especially in Asia Pacific, where rising disposable incomes and social media-driven beauty trends are expanding consumption.

Regional Insights

North America Pearlescent Pigment Market Trends - U.S. Demand Driven by Automotive, Premium Coatings, and EV Color Innovation

North America, led by the U.S., is a mature yet high-value market for pearlescent pigments, driven by strong demand from automotive coatings, personal care, premium packaging, and industrial applications. Per-capita consumption is relatively high due to established automotive clusters, a sophisticated cosmetics industry, and robust R&D capabilities, supporting steady demand across coatings, plastics, and personal care formulations.

Vehicle production and aftermarket refinish activity sustain volumes, while the rise of electric vehicle models has spurred interest in high-chroma whites, signature colorways, and advanced optical effects for special-edition trims.

Premium SUVs and pickup trucks, which dominate the region, frequently use pearlescent finishes for visual differentiation. Regulatory focus on low-VOC coatings, safer materials, traceable raw materials, and comprehensive documentation favors suppliers offering compliance support and transparent sourcing.

Recent developments include expansions of technical centers by leading pigment producers, showcases of sustainable effect pigments at U.S. trade shows, and collaborative programs with electric vehicle manufacturers to create exclusive optical finishes for next-generation vehicles, highlighting innovation and sustainability as key market drivers.

Europe Pearlescent Pigment Market Trends - Sustainability and Regulatory Compliance Shape Advanced Effect Pigment Adoption

Europe is a high-value, innovation-driven market that prioritizes sustainability, safety, and full material traceability. Germany remains a core hub thanks to its strong automotive and specialty chemicals industries, while France leads in global cosmetics R&D and innovation. The U.K. and Spain also contribute meaningful demand through packaging, beauty, and design-focused consumer goods.

Strict chemical regulations and eco-design standards are accelerating the transition toward synthetic mica, certified natural mica, and pigments supported by detailed documentation of origin, ethical sourcing, and environmental impact. European automakers continue to adopt advanced effect finishes incorporating multilayer optical structures, radar-transparent pigments for driver-assistance systems, and heat-stable materials suitable for electric vehicles.

Recent trends include the launch of fully traceable, low-carbon pearlescent pigment lines developed to meet evolving sustainability targets, along with new product families presented at major European coatings and beauty exhibitions.

The region has also undergone a notable restructuring of pigment production capacity following the sale and reorganization of a major premium effect pigment manufacturer, reshaping competition and reinforcing the importance of Asia-to-Europe supply chains.

Asia Pacific Pearlescent Pigment Market Trends - Rapid Growth Led by China, Japan, and Expanding High-Value Applications

Asia Pacific remains both the largest and fastest-growing region, holding a 32.7% market share, supported by strong manufacturing ecosystems, rising consumer demand, and expanding end-user industries. China leads the region with its extensive production base, strong domestic consumption, and global export capability. The country continues to invest in high-value synthetic mica and advanced multilayer pigments for automotive, cosmetics, and electronics applications.

Japan serves as a key hub for high-performance demand, driven by its advanced automotive and electronics sectors that require pigments with precise particle control, consistent optical behavior, and excellent thermal stability.

India records some of the highest global growth rates, as increasing cosmetics usage, rapid expansion of paints and coatings, and a growing packaging sector fuel demand. ASEAN economies such as Thailand, Indonesia, and Vietnam add momentum through rising automotive assembly, industrial output, and consumer goods manufacturing.

Across the region, manufacturers supplying international brands are progressively aligning with global standards for ethical sourcing and quality assurance, accelerating the shift toward synthetic mica and enhanced supply-chain transparency.

Notable developments include major capacity expansions in China for both natural and synthetic mica pigments, the acquisition of a premium effect-pigment producer by an Asia-based materials group, increased investment in automotive-focused pigments for EV platforms, and rapid growth in India’s domestic pigment production to meet rising demand in coatings and personal care.

Competitive Landscape

The global pearlescent pigment market is moderately consolidated, with a few multinational specialty chemical firms dominating premium and high-performance segments through advanced titanium dioxide-coated mica, multilayer interference structures, and engineered substrates. These leaders leverage strong R&D, technological expertise, and vertically integrated production for consistent quality.

Commodity and mid-grade segments are fragmented, with regional Asian producers offering cost-competitive alternatives. Asia Pacific is a key growth region due to its consumer base and manufacturing strength. Long-term partnerships with OEMs and brands, along with sustainable, low-carbon, and recyclable pigment innovations, increasingly shape competition.

Key Industry Developments

- In March 2025, ECKART launched a new laser-marking pigment called Lasersafe 020, optimized for dark polymers and low loading; the pigment is also food-contact compliant.

- In June 2025, Oxen Chemicals introduced its “HOT NEW Effect 15-4” pigment, a high-gloss and non-toxic pearlescent pigment with enhanced resistance to weather, heat, and chemicals, suited for water, solvent, and powder coatings.

Companies Covered in Pearlescent Pigment Market

- Susonity

- BASF

- ECKART

- DIC Corporation

- Sun Chemical

- Ferro Corporation

- SCHLENK

- Sudarshan Chemical Industries

- Fujian Kuncai

- RIKA Technology

- Geotech International

- KROMACHEM

- Sensient

- Oxen Special Chemicals

- Kolortek

- CQV

- Yortay Fine Chemicals

- Ruicheng Metallic Pigment

- Lansco Colors

- Venator Materials

Frequently Asked Questions

The global pearlescent pigment market is estimated at approximately US$2.7 Billion in 2025.

By 2032, the pearlescent pigment market is projected to reach US$4.2 Billion, reflecting sustained growth across coatings, cosmetics, plastics, and packaging applications.

Key trends include the rising use of synthetic mica and engineered platelets for performance and ethical sourcing, growing demand in cosmetics for shimmer, expansion in premium automotive finishes, increased use of high-value pigments in packaging and electronics, with sustainability and traceability driving product development.

Titanium dioxide coated mica is the dominant product type, due to its high brightness, UV stability, and versatility across automotive coatings, cosmetics, and packaging.

The pearlescent pigment market is expected to grow at a CAGR of 6.4% from 2025 to 2032, driven by premiumization in end-user industries, technological innovations in synthetic and coated pigments, and regional expansion in Asia Pacific.

Major companies include Susonity, BASF, ECKART, DIC Corporation / Sun Chemical, and Ferro Corporation.