- Oil & Gas

- PDC Drill Bits Market

PDC Drill Bits Market Size, Share, and Growth Forecast 2026 - 2033

PDC Drill Bits Market by Product Type (Steel-Body PDC Bits, Matrix-Body PDC Bits, and Hybrid PDC Bits), Application (Oil and Gas Drilling, Geothermal Drilling, Mining Operations, Water Well Drilling, and Construction Projects), and Regional Analysis for 2026 - 2033

PDC Drill Bits Market Size and Share Analysis

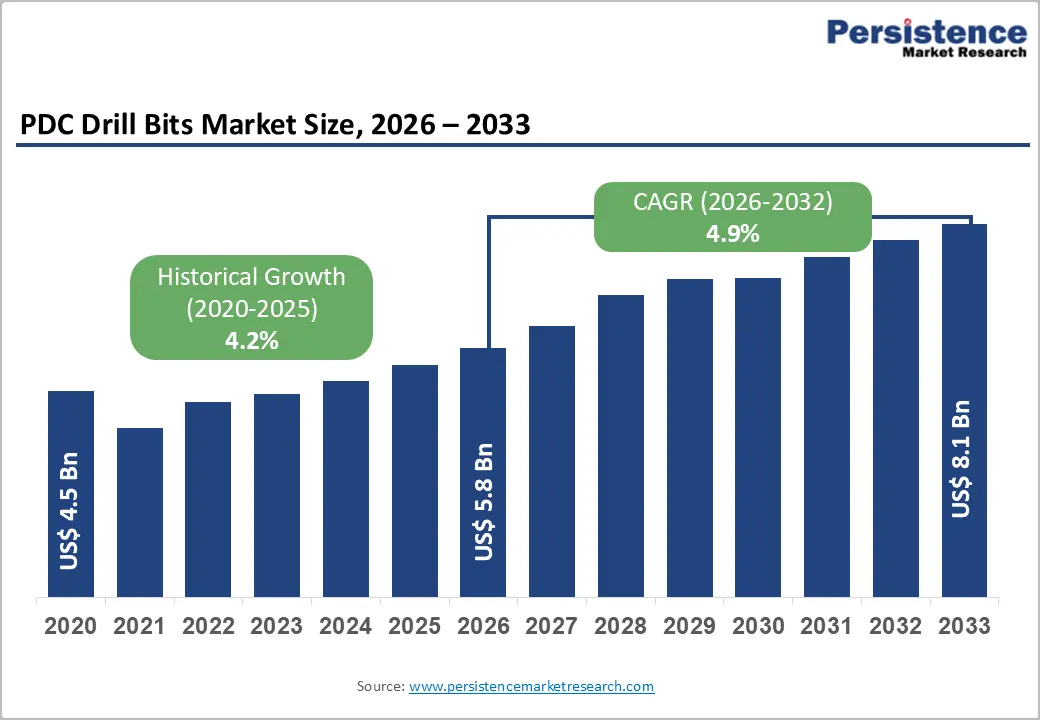

The global PDC drill bits market size is likely to be valued at US$ 5.8 billion in 2026 and is projected to reach US$ 8.1 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

The polycrystalline diamond compact (PDC) drill bits market is experiencing robust growth driven by accelerated unconventional resource development, particularly in shale gas and tight oil formations that dominate exploration activities across North America, China, and Southeast Asia. Technological advancements in cutter design and matrix formulations have enhanced penetration rates by up to 10% in challenging formations, directly reducing drilling costs and operational downtime.

Key Market Highlights:

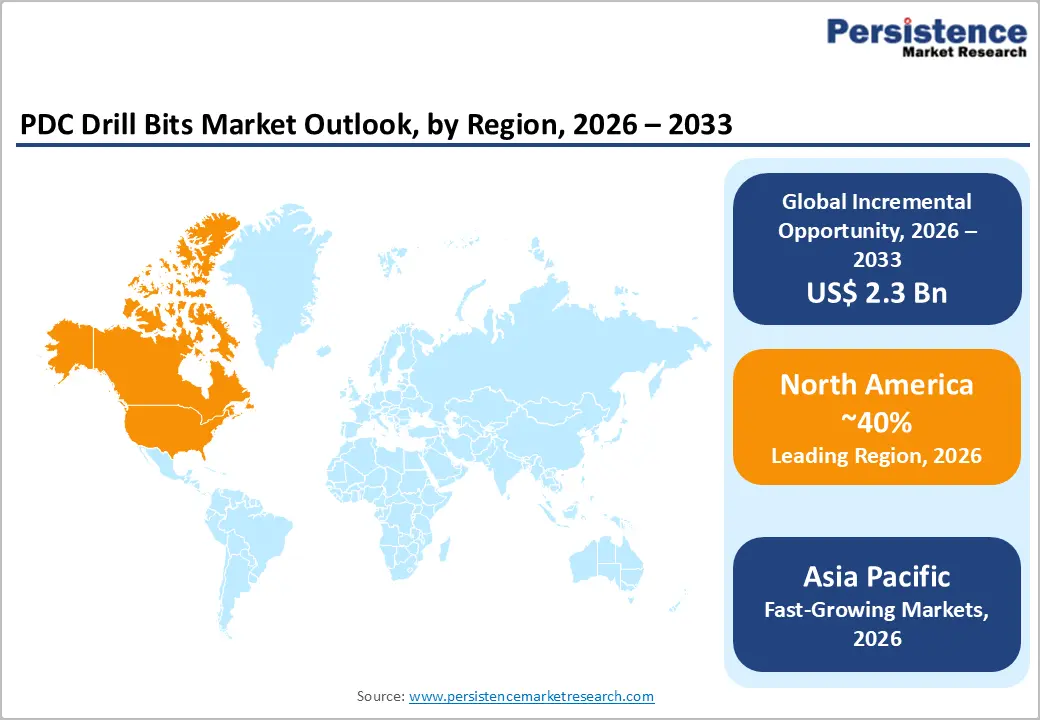

- Leading Region: North America maintains a dominant regional position, commanding approximately 40% of the global PDC drill bits market value through mature unconventional resource development, established offshore infrastructure, and premium product adoption, with Permian Basin horizontal drilling activity establishing performance benchmarks for advanced PDC bit designs.

- Fastest-Growing Region: Asia-Pacific represents the fastest-growing regional market, projected to expand at 5.6% CAGR through 2033, driven by Chinese domestic shale development, emerging deepwater exploration in Southeast Asia, and government investments in unconventional resource extraction.

- Dominant Product Type: Matrix-Body PDC Bits dominate the product category, commanding approximately 62% market share within product type classification, attributed to superior erosion resistance, extended bit life in abrasive formations, and thermal stability characteristics essential for deep-water, HPHT, and emerging geothermal drilling applications.

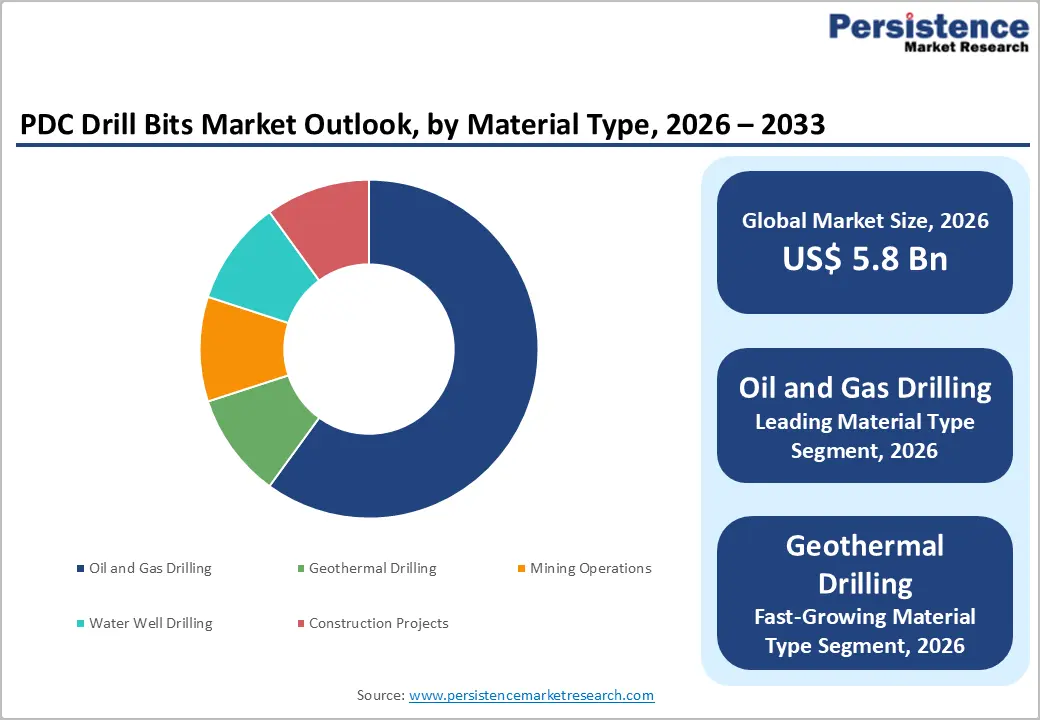

- Growing Material Type: Oil and Gas Drilling is the dominant application segment, accounting for 80% of global PDC drill bit consumption, with unconventional shale development in the Permian, Marcellus, and Chinese basins driving the fastest growth.

- Key Market Opportunity: Geothermal energy development emerges as a transformational market opportunity, with the global geothermal drilling market valued at US$ 6.3 billion in 2025, creating sustained demand for specialized matrix-body PDC bits engineered for ultra-high-temperature environments exceeding 300-400°C.

| Key Insights | Details |

|---|---|

| PDC Drill Bits Market Size (2026E) | US$ 5.8 Bn |

| Market Value Forecast (2033F) | US$ 8.1 Bn |

| Projected Growth CAGR (2026 - 2033) | 4.9% |

| Historical Market Growth (2020 - 2025) | 4.2% |

Market Dynamics

Drivers - Expansion of Unconventional Resource Development

The global surge in unconventional oil and gas exploration, particularly shale drilling in formations such as the Permian Basin, Eagle Ford Shale, and Marcellus Shale, has emerged as the primary growth catalyst for PDC drill bits. These challenging formations require specialized drilling tools capable of delivering a high rate of penetration (ROP) without compromising durability under extreme abrasive conditions. The Chinese government's Mineral Exploration Breakthrough Strategy has intensified domestic shale development, with recent discoveries totaling 180 million tonnes of shale oil reserves in the Bohai Bay Basin and Subei Basin, necessitating advanced drilling technologies.

PDC bits enable operators to reduce drilling time significantly. Field data from the Permian Basin demonstrate that horizontal wells completed with optimized PDC bit designs achieve 30-50% faster penetration rates than conventional roller cone bits, directly translating into reduced operational expenditure per well and enhanced project economics for exploration companies pursuing unconventional resources.

Technological Innovations in Cutter Design and Material Science

Continuous innovation in polycrystalline diamond cutter technology and tungsten carbide matrix formulations has revolutionized drilling efficiency across the industry. Leading manufacturers, including Schlumberger (SLB), Baker Hughes, and Halliburton, have introduced advanced shaped cutter elements, such as 3D conical diamond elements and enhanced blade geometries, that optimize rock destruction mechanisms for specific lithologies. Recent advancements in matrix body PDC bits, which represent approximately 62% of market share, demonstrate superior thermal stability, maintaining cutting efficiency at downhole temperatures exceeding 200°C, making them indispensable for deep-water drilling and geothermal applications.

Integration of real-time data analytics and artificial intelligence into drilling operations enables dynamic optimization of drilling parameters, with operator feedback indicating average ROP improvements of 10% and a 67% reduction in vibration levels in complex well trajectories, thereby extending bit life and minimizing non-productive time across diverse geological formations.

Restraint - Commodity Price Volatility and Exploration Budget Constraints

The PDC drill bit market is highly sensitive to crude oil and natural gas price fluctuations, which directly affect capital allocation decisions for exploration and production activities. Historical analysis reveals that periods of depressed energy commodity prices trigger contraction in upstream drilling budgets, with industry surveys indicating that a 30% decline in oil prices correlates to a 15-20% reduction in new well completions within 12-18 months.

The inherent capital intensity of PDC bit procurement, with advanced matrix-body designs commanding 40-60% premium pricing over conventional alternatives, creates procurement challenges for independent operators under margin pressure. The extended payback periods for exploration projects necessitate sustained commodity price stability, making the market vulnerable to macroeconomic shocks and geopolitical disruptions affecting global energy demand trajectories.

Environmental Regulations and Sustainability Pressures

Rise in regulatory frameworks governing drilling operations and environmental protection standards in developed markets, particularly across Europe and North America, imposes additional operational constraints and compliance costs on drilling service providers. The European Union's stringent environmental directives mandate comprehensive waste management protocols and limit drilling fluid additives, requiring specialized PDC bit designs compatible with environmentally acceptable drilling fluids that command premium pricing.

Corporate sustainability mandates and investor pressure toward energy transition strategies have prompted several major oil and gas operators to reduce exploration budgets and redirect capital toward renewable energy investments, directly constraining demand growth for drilling equipment in traditional oil and gas segments.

Opportunity - Geothermal Energy Expansion and Heat-Resistant Drilling Solutions

The global geothermal drilling market, valued at approximately US$ 6.3 billion in 2025 and projected to grow at 5.2% CAGR through 2033, represents a significant expansion opportunity for PDC drill bit manufacturers. Geothermal development initiatives in geologically favorable regions, including Iceland, New Zealand, Indonesia, and East Africa, require specialized drilling tools capable of sustained performance in ultra-high-temperature downhole environments reaching 300-400°C.

The global demand for geothermal power generation capacity is accelerating, with international energy agencies projecting cumulative installed capacity growth from 14 gigawatts in 2020 to 40+ gigawatts by 2030, directly driving demand for advanced matrix-body PDC bits specifically engineered for thermal stability.

Strategic partnerships between PDC bit manufacturers and geothermal drilling contractors, exemplified by collaborative development initiatives undertaken by Halliburton and regional drilling service providers, are accelerating the commercialization of specialized bit designs that can maintain operational efficiency in these demanding thermal conditions, creating substantial revenue opportunities for market participants capable of delivering thermal-optimized solutions.

Deep-Water and Ultra-Deepwater Offshore Drilling Expansion

Intensified investment in deep-water and ultra-deepwater exploration, particularly in the Gulf of Mexico, West Africa, Southeast Asia, and South China Sea, is driving demand for premium-grade PDC drilling technology engineered for extreme pressure and temperature conditions. The US Gulf of Mexico, which accounts for approximately 17% of total US crude oil production, continues to attract significant capital investment despite broader energy transition pressures, with operators prioritizing operational efficiency and cost reduction per barrel.

Advanced hybrid PDC bits and steel-body PDC designs engineered for impact resistance in fractured carbonate formations are critical enablers of cost-effective deep-water drilling, with case studies demonstrating 30% reductions in drilling time and 20% in operational costs compared to conventional bit designs. The expansion of Southeast Asian offshore assets by international oil companies and emerging national champions, combined with infrastructure development in emerging markets, creates a multi-billion-dollar opportunity window for PDC bit manufacturers with technical expertise in deep-water drilling applications and strong regional service networks.

Category-wise Analysis

Product Type Insights

Matrix-Body PDC Bits represent the dominant segment within the product type category, commanding approximately 62% market share in 2026 and anticipated to maintain leadership position through the forecast period. The superior performance characteristics of matrix-body designs, constructed from tungsten carbide metallurgically bonded with softer metallic binders, provide exceptional erosion and abrasion resistance essential for extended drilling intervals in highly consolidated and abrasive formations.

Field operations data from Permian Basin drilling campaigns corroborate that matrix-body PDC bits achieve 40-50% longer bit life compared to steel-body alternatives in medium-to-hard abrasive formations, directly justifying premium pricing despite higher upfront acquisition costs.

The thermal stability characteristics of matrix-body PDC bits, maintaining structural integrity at sustained downhole temperatures exceeding 250°C, position them as the preferred choice for deep-water exploration, HPHT (high pressure, high temperature) wells, and emerging geothermal drilling applications. Continuous innovation in matrix composition and advanced surface coatings, including proprietary hardfacing technologies deployed by manufacturers such as SLB, Baker Hughes, and Halliburton, further enhances competitive differentiation and justifies premium market valuations within this segment.

Application Insights

Oil and gas drilling maintains dominant market position, representing approximately 80% of global PDC drill bits consumption, driven by sustained exploration and production activities across conventional, unconventional, and deepwater reserve segments. Within oil and gas drilling, shale formations (including Permian, Marcellus, Eagle Ford, and Chinese Songliao Basin) represent the highest-growth sub-segment, as operators prioritize unconventional resource development to offset production declines in mature fields.

Sandstone and limestone formations remain significant application areas due to their prevalence in offshore development and global exploration portfolios, with PDC bits demonstrating superior drilling efficiency and cost-per-foot economics compared to roller cone alternatives. The rapid expansion of geothermal drilling applications, estimated at 5.2% CAGR, presents the fastest-growing segment within application categories, driven by renewable energy mandates and government investment commitments in European, Pacific Rim, and East African geothermal resources.

Water well drilling services, valued nearly US$ 5.0 billion globally in 2025 with 3/2% CAGR projection through 2033, utilize PDC bits for rapid penetration through diverse soil and rock formations, with demand strength in North American agricultural regions and Asian developing economies experiencing groundwater depletion.

Mining exploration drilling is a specialized segment that leverages PDC bits for hard-rock penetration in mineral discovery operations, supported by ongoing exploration activities in Australia, Canada, and emerging African mining jurisdictions. In construction drilling applications, including foundation pile drilling and tunnel excavation, PDC reamers and specialized bit designs are increasingly adopted to improve drilling speed and operational precision in urban infrastructure development projects.

Regional Insights

North America PDC Drill Bits Market Trends

North America commands approximately 40% of global PDC drill bits market value in 2026, establishing the region as the undisputed market leader driven by mature exploration infrastructure and dominant unconventional shale development. The Permian Basin in Texas and New Mexico represents the global epicenter of horizontal drilling activity, with recent productivity achievements including average lateral well lengths exceeding 10,000 feet and horizontal drilling rig deployments averaging 47 miles of lateral footage per quarter.

PDC bit adoption in the Permian has achieved near-universal penetration, as operators standardize on advanced designs to optimize drilling economics in highly competitive unconventional plays, where cost-per-foot drilling represents a critical competitive differentiator. The Eagle Ford Shale, the Marcellus Shale in Appalachia, and Canadian deep-basin unconventional resources similarly demonstrate strong PDC bit demand, with regional drilling service providers maintaining a specialized inventory of formation-optimized bit design.

Investment continuity in the Permian Basin, supported by improved drilling efficiency economics and sustained cash flow generation, is projected to maintain North American PDC drill bits demand growth at 3.2% CAGR through 2033, slightly moderating from historical 3.9% 2020 - 2025 CAGR as baseline production stabilizes and new well additions moderate from peak unconventional development phases.

Europe PDC Drill Bits Market Trends

Europe PDC Drill Bits market continues to be shaped by stringent regulatory environments and a strong emphasis on occupational health and safety. The European Union’s PPE regulations mandate rigorous performance standards, driving demand for certified, high-quality PDC Drill Bits across healthcare and industrial sectors. Countries such as Germany, the UK, and France lead regional consumption, supported by extensive hospital networks and robust manufacturing sectors that integrate PDC Drill Bits into routine safety protocols, not just during pandemic spikes. This regulatory backdrop, alongside increasing awareness of workplace safety and infection control, continues to stabilize demand even as post-COVID normalization progresses.

European market trends highlight a preference for reusable, ergonomic, and advanced face shield designs that align with sustainability goals and long-term cost efficiency. Growth is not limited to healthcare; sectors like construction, manufacturing, and laboratories are increasingly adopting PDC Drill Bits as part of comprehensive PPE kits to protect workers from chemical splashes, debris, and airborne particulates. Innovation in features such as anti-fog coatings and adjustable fittings is enhancing user comfort and broadening appeal across diverse end-use applications. Europe’s market is projected to grow steadily at a moderate CAGR, driven by regulatory compliance, industrial safety standards, and ongoing investments in health infrastructure.

Asia Pacific PDC Drill Bits Market Trends

Asia-Pacific emerges as the fastest-growing regional market for PDC drill bits, with projected CAGR 5.6% through 2033, driven by accelerated unconventional resource development in China, India, and Southeast Asian jurisdictions. China represents the primary growth engine, with government mandates to achieve energy independence spurring intensive exploration and development of domestic shale oil and gas reserves. Recent discoveries of 180 million tonnes of shale oil reserves in Bohai Bay Basin and Subei Basin, combined with successful production from Songliao Basin achieving 1 million tonnes annual output milestone in late 2025, demonstrate escalating commercial viability of Chinese unconventional resources and corresponding demand for advanced PDC drilling technology.

Indian petroleum sector development, including unconventional oil and gas exploration in regional sedimentary basins, is driving PDC bit adoption for accelerated exploration programs. Indonesia, Malaysia, and Vietnam pursue offshore and deep-water exploration with significant capital investment, necessitating advanced PDC designs engineered for extreme pressure and temperature conditions prevalent in Southeast Asian deepwater environments. Japanese and South Korean manufacturing expertise in advanced materials science enables regional PDC bit manufacturers to capture incremental market share through specialized product innovations. The region's manufacturing cost advantages and expanding technical expertise are attracting tier-1 international manufacturers to establish regional production facilities, further enhancing Asia-Pacific market competitiveness and driving sustained demand growth through 2033.

Competitive Landscape

The global PDC drill bits market demonstrates characteristics of moderate consolidation, with tier-1 multinational enterprises dominating market share while tier-2 regional specialists maintain niche positioning in specialized applications. Schlumberger Limited (SLB), Baker Hughes Company, Halliburton Company, and National Oilwell Varco (NOV) collectively command approximately 55-60% global market share, leveraging extensive research and development capabilities, global distribution networks, and integrated service offerings including real-time drilling optimization and data analytics platforms.

Tier-2 competitors including Sandvik AB, Varel International, Archway Engineering, and Chinese manufacturers such as Wuhan SML Tools and Cangzhou Great Drill Bits compete through cost-based positioning, regional market specialization, and product customization for formation-specific applications. Emerging business model innovations include performance-based contracting, where bit manufacturers assume operational risk and pricing is indexed to drilling performance metrics (cost-per-foot, total well time reduction) rather than unit-based procurement, fundamentally reshaping competitive dynamics toward integrated solution providers with advanced analytics capabilities.

Key Market Developments

- In September 2025, SLB expanded strategic collaborations with artificial intelligence and machine learning technology providers to integrate autonomous drilling optimization systems into PDC bit platforms, enabling dynamic parameter adjustment and extended bit life predictions, reducing non-productive time (NPT) in complex well trajectories.

- In November 2025, Baker Hughes Company commercialized Internet of Things (IoT)-enabled PDC drill bits featuring embedded sensors and cloud-based data analytics, enabling continuous downhole condition monitoring and remote drilling parameter optimization for operators pursuing autonomous drilling operations.

- In Decembers 2024, Halliburton unveiled advanced polycrystalline diamond compact (PDC) drill bits engineered for high-pressure, high-temperature (HPHT) environments, featuring proprietary diamond coating technologies and real-time performance monitoring systems enabling predictive maintenance and operational optimization in deep-water drilling applications.

Companies Covered in PDC Drill Bits Market

- Schlumberger

- BHGE

- Haliburton

- Baker Hughes Company

- Sandvik AB

- Archway Engineering (UK) Ltd

- Infinity Tool Manufacturing

- NOV (National Oilwell Varco)

- SLB

- Wuxi Geological Drilling Equipment Co.Ltd.

- Rockpecker Limited

- Cangzhou Great Drill Bits Co.Ltd.

- WUHAN SML TOOLS LIMITED

- Varel

- Rubicon Oilfield Inc.

Frequently Asked Questions

The global PDC drill bits market is projected to reach US$ 8.1 billion by 2033, growing from US$ 5.8 billion in 2026 at a CAGR of 4.9%. This growth trajectory reflects sustained demand from unconventional oil and gas exploration, deepwater development, and emerging geothermal energy projects across global markets.

Primary demand drivers include accelerated unconventional resource development in shale formations (particularly Permian Basin, Marcellus, and Chinese basins), technological innovations in polycrystalline diamond cutter design delivering 10% ROP improvements, extended horizontal drilling laterals averaging 10,000 feet, and expanding geothermal energy development mandates supporting renewable energy transition objectives globally.

Matrix-Body PDC Bits command approximately 62% market share within product type classification, attributed to superior erosion resistance, extended operational lifespan in abrasive formations, and thermal stability characteristics essential for deep-water exploration and geothermal drilling applications requiring premium performance specifications.

Asia-Pacific represents the fastest-growing regional market, expanding at 5.6% CAGR through 2033, driven by Chinese domestic shale development, emerging Southeast Asian deepwater exploration, government mandates for unconventional resource extraction, and regional manufacturing capability development supporting equipment localization and competitive pricing.

Geothermal energy development emerges as the transformational market opportunity, with global geothermal drilling expanding at 4.4% CAGR through 2033. Specialized matrix-body PDC bits engineered for ultra-high-temperature environments (exceeding 300-400°C) are essential for geothermal resource development supported by government renewable energy policies and corporate sustainability commitments across Europe, Pacific Rim, and East African jurisdictions.

Market leadership is concentrated among tier-1 multinational enterprises including Schlumberger Limited, Baker Hughes Company, Halliburton Company, and National Oilwell Varco (NOV), collectively commanding approximately 55-60% global market share. Tier-2 competitors including Sandvik AB, Varel International, and Chinese manufacturers (Wuhan SML Tools, Cangzhou Great Drill Bits) maintain niche positioning through regional specialization and cost-based competitive strategies.