- Industrial Machinery

- Pasteurization Vessel Market

Pasteurization Vessel Market Size, Share, and Growth Forecast, 2026 - 2033

Pasteurization Vessel Market by Capacity (< 500 L, 500-1000 L, 1001-5000 L, 5001-10000 L, and > 10000 L), By Method (Batch and Continuous), Industry (Dairy Industry, Beverage Industry, Fruit & Vegetable Processing Industry, and Others), and Regional Analysis for 2026 - 2033

Pasteurization Vessel Market Size and Trends Analysis

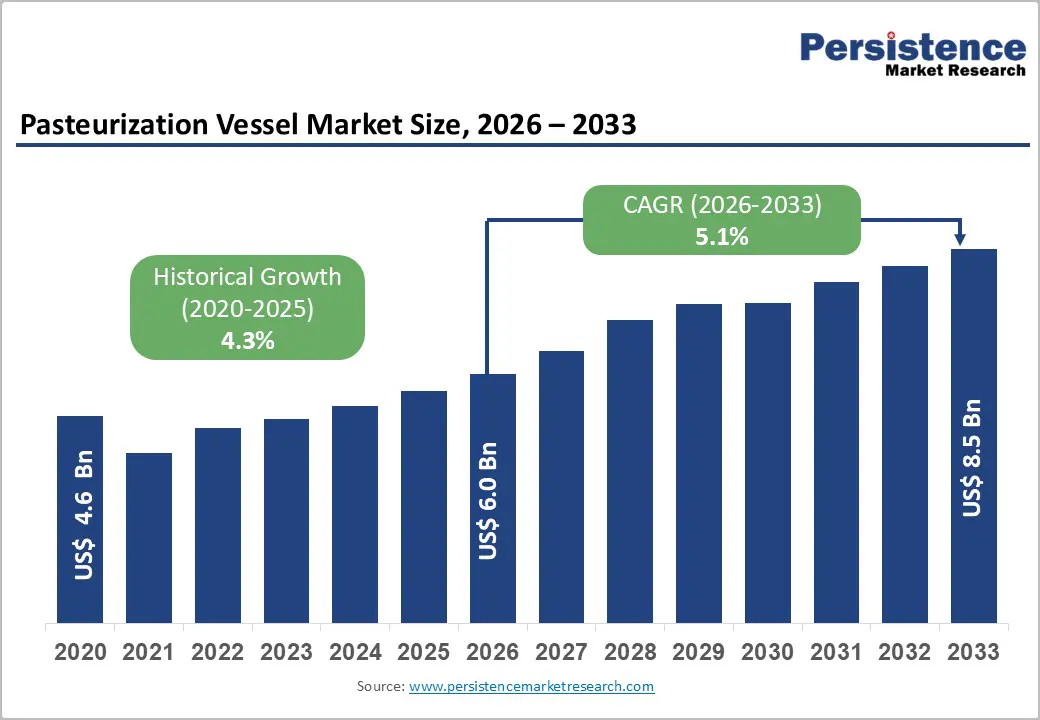

The global pasteurization vessel market size is likely to be valued US$ 6.0 Billion by 2026, further expanding to US$ 8.5 Billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

This market expansion is driven by heightened food safety regulations, increasing demand from the dairy and beverage industries, and technological advancements in thermal processing equipment. Rising consumer awareness regarding pathogenic contamination in food and beverages, coupled with stringent regulatory frameworks in developed economies, continues to propel investments in advanced pasteurization infrastructure. The shift toward continuous pasteurization methods and mid-range capacity vessels (1001-5000 liters) reflects industry adaptation to evolving production efficiencies and cost optimization strategies.

Key Industry Highlights:

- Dominant Capacity Segment: 1001-5000 liter capacity vessels command above 35% revenue share as an optimal balance between throughput and capital efficiency; 5001-10000 liter segment demonstrates accelerated 6.0% CAGR growth driven by processor consolidation trends.

- Technology Transition Dynamics: Continuous pasteurization methods expanding at 6.2% CAGR, reflecting superior operational efficiency; segment transition creating equipment replacement opportunities through 2033.

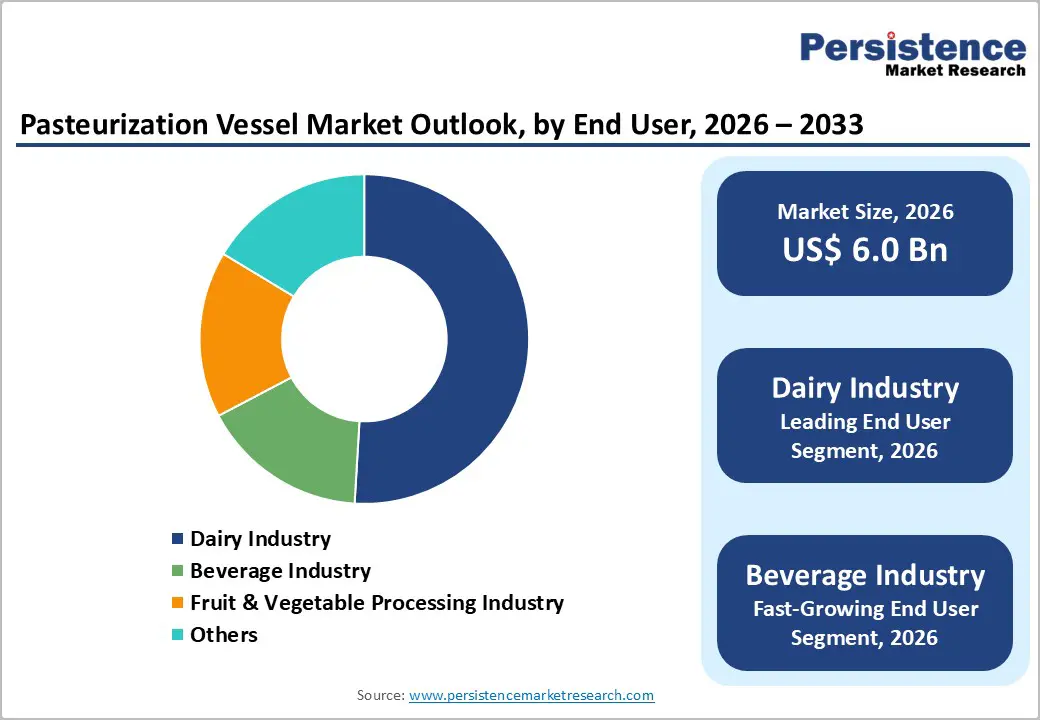

- End-Use Leadership and Growth: Dairy industry dominates with 50%+ revenue share; beverage industry emerging as fastest-growing segment at 6.3% CAGR driven by functional beverage category expansion and regulatory intensification.

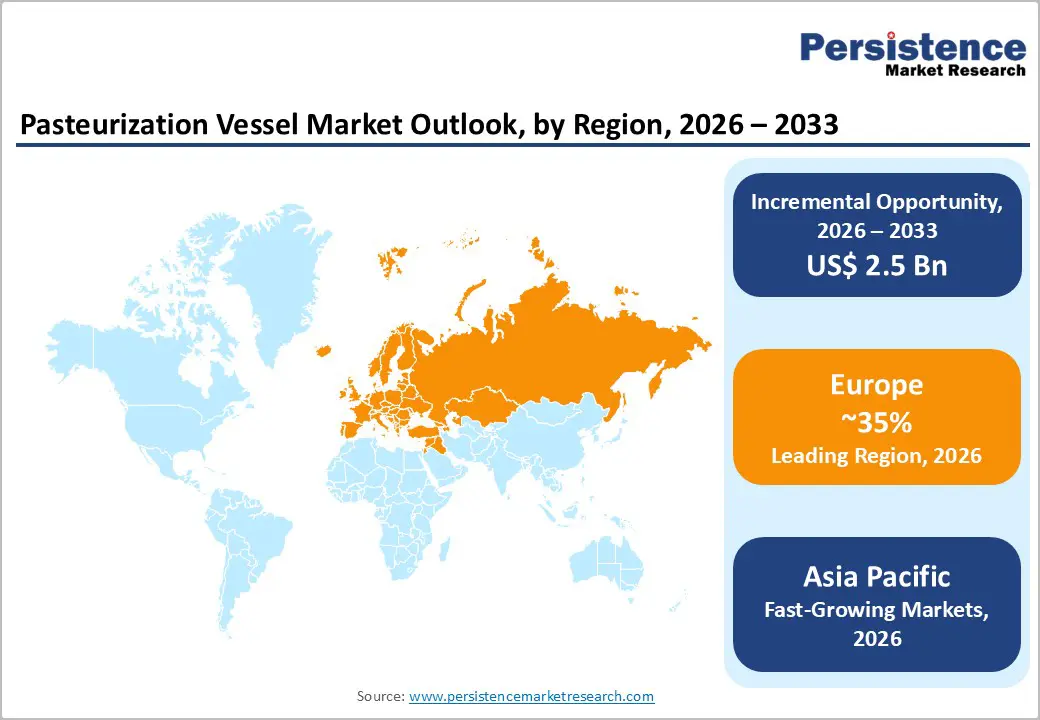

- Regional Growth Acceleration: Asia-Pacific emerging as fastest-growing region at 6.5% CAGR, projected to increase market share from 25-28% to 32-36% by 2033; Europe maintains largest current share above 35%; North America represents mature market at 3.8-4.2% growth.

- Strategic Investment Focus: Digital integration, automated compliance documentation, and energy-efficient system design represent primary competitive differentiation vectors; technology partnerships and regional manufacturing facility investments drive competitive positioning in emerging markets.

| Key Insights | Key Insights |

|---|---|

| Pasteurization Vessel Market Size (2026E) | US$ 6.0 Bn |

| Market Value Forecast (2033F) | US$ 8.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Drivers - Rise in Food Safety Regulations and Compliance Requirements

Food safety regulations have become significantly more stringent across global markets, particularly in North America, Europe, and developed Asia-Pacific regions. The FDA's Pasteurized Milk Ordinance (PMO), coupled with EU Regulation 853/2004, mandates specific thermal processing parameters that require validated pasteurization equipment. Government agencies worldwide have intensified inspections and penalty structures for non-compliance, creating a compliance-driven market demand.

According to industry reports, approximately 85% of dairy processing facilities have upgraded or are planning to upgrade pasteurization systems to meet evolving regulatory standards within the 2023-2028 period. This regulatory pressure translates directly into capital expenditure requirements, with facilities investing in advanced vessel designs that provide real-time monitoring, automated temperature control, and comprehensive documentation capabilities. The economic impact is substantial: non-compliant facilities face production shutdowns and significant penalties, with reported compliance costs ranging from US$ 150,000 to US$ 500,000 per facility upgrade, depending on production capacity. This creates a structural growth floor for the pasteurization vessel market, independent of commodity price fluctuations.

Restraint - High Capital Investment Requirements and Extended ROI Cycles

Pasteurization vessels represent significant fixed capital expenditures, with mid-range capacity equipment (5000-10000 liters) typically costing US$ 200,000-US$ 600,000, and large-capacity systems exceeding US$ 1.2 Million. For small to medium-sized enterprises (SMEs) operating with constrained capital access, these investments present substantial barriers to market entry or capacity expansion. ROI cycles typically span 6-9 years under baseline operational assumptions, creating reluctance among processors with uncertain demand forecasts. Working capital constraints are particularly acute in developing markets where equipment financing options are limited, financing costs range from 12-18% annually, and lender risk premiums remain elevated.

Approximately 40% of potential dairy processor investments in ASEAN and South Asian markets remain unrealized due to capital scarcity, according to trade association data. This structural constraint disproportionately affects geographic regions with high growth potential but limited institutional financing infrastructure. Small-scale artisanal and cooperative processors, which constitute significant segments in emerging markets, face capital rationing that perpetuates the continued use of older, less efficient equipment despite regulatory and efficiency arguments for modernization.

Opportunity - Expansion into Emerging Markets with Developing Dairy Infrastructure

India, Vietnam, and Southeast Asian nations are experiencing rapid dairy sector modernization, driven by government policies supporting rural dairy development and processing infrastructure investment. India's National Program for Dairy Development allocated US$ 480 Million during the 2022-2027 period specifically for processing infrastructure upgrades, with pasteurization equipment representing a primary investment category. This government commitment creates a forecastable demand stream of approximately US$ 180-220 Million annually for pasteurization vessels in the Indian market alone through 2030.

Vietnam's dairy industry is projected to grow at 8.5% annually, requiring corresponding processing capacity expansion. These emerging markets remain underserved relative to infrastructure investment needs, with currently installed pasteurization capacity operating at 65-72% utilization rates-indicating significant room for capacity addition without market saturation. Market entry strategies emphasizing financing partnerships with development banks, localized manufacturing, and service networks adapted to regional technical expertise levels present sustainable competitive advantages. First-mover advantages in these geographies remain available, with market shares still fragmented among 15-20 regional and international competitors.

Category-wise Analysis

Capacity Insights - Mid-Capacity Pasteurization Vessels Dominate Revenue as Larger Systems Drive Growth

The 1001-5000 liter capacity segment leads the global pasteurization vessel market, accounting for over 35% of total revenue. This capacity range offers an optimal balance between production throughput and capital efficiency, making it the preferred choice for medium-to-large dairy processors, particularly in developed markets. Facilities operating within this range typically cater to regional distribution networks spanning 50-100 km, aligning well with cold-chain logistics and minimizing distribution losses. With vessel prices ranging from US$ 180,000 to US$ 400,000, these systems fall within accessible capital budgets for most institutional processors, supporting shorter replacement and upgrade cycles compared to ultra-large installations. The segment’s dominance is further reinforced by consolidation among dairy cooperatives, which has created medium-scale processing entities, and by the gradual adoption of European processing standards in emerging economies. In these markets, 2000-3000 liter vessels are often selected as benchmark systems for initial modernization investments.

In contrast, the 5001-10000 liter capacity segment represents the fastest-growing category, expanding at a 6.0% CAGR, well above the overall market growth rate of 5.1%. Growth is driven by industry consolidation, where regional processors merge into larger operations requiring higher single-unit processing capacities. Large cooperatives in India, Southeast Asia, and Eastern Europe are increasingly investing in 6000-8000 liter systems to replace multiple smaller vessels, thereby reducing operational complexity and maintenance costs. Adoption by large-scale beverage manufacturers seeking standardized batch sizes further supports this segment’s rapid expansion.

Method Insights - Batch Systems Dominate Pasteurization Vessels While Continuous Methods Drive Accelerating Growth

Batch pasteurization systems remain the leading method in the global pasteurization vessel market, accounting for over 60% of total revenue. Their dominance is largely attributed to widespread installed capacity and long-standing adoption across dairy and food processing facilities. Batch systems offer high operational flexibility, allowing processors to handle multiple product variants such as whole milk, skimmed milk, cream, and specialty dairy products with minimal reconfiguration between production cycles. In addition, their comparatively simple installation requirements make them well-suited for retrofitting into existing plants, avoiding the need for major infrastructure upgrades. These advantages make batch systems particularly attractive to small- and mid-scale processors. However, higher per-unit operating costs associated with labor intensity and energy consumption are gradually creating pressure for efficiency-driven upgrades.

In contrast, continuous pasteurization systems represent the fastest-growing segment, expanding at a CAGR of approximately 6.2%. Growth is driven by substantial efficiency gains, as continuous systems reduce processing time from 30-45 minutes in batch operations to just 15-25 seconds. This rapid processing significantly improves throughput while lowering energy consumption per unit of output. Large-scale dairy processors, beverage manufacturers, and specialty juice producers increasingly favor continuous systems despite their 10-15% higher upfront capital costs. Strong regulatory endorsement of their superior microbial control and seamless integration with automated filling and packaging lines further supports accelerating adoption.

Industry Insights -Dairy Dominates Pasteurization Vessel Demand While Beverage Applications Drive Fastest Growth

The dairy industry remains the leading end-use segment in the global pasteurization vessel market, accounting for over 50% of total revenue. Dairy applications form the foundation of pasteurization technology, as regulatory frameworks such as the Pasteurized Milk Ordinance (PMO) in North America and EC Regulation 853/2004 in Europe mandate validated thermal processing for all fluid milk and derivative products. The global dairy market generates approximately US$ 620 billion in annual revenue, with processing infrastructure representing nearly 8-12% of total supply chain investment. Milk production volumes continue to expand at 1.8-2.3% annually in developed markets and 4.5-6.2% in emerging economies, sustaining long-term demand for pasteurization capacity. This segment’s dominance is further reinforced by technology maturity and installed base, as dairy facilities account for nearly 65% of global pasteurization vessel installations.

In contrast, the beverage industry represents the fastest-growing end-use segment, expanding at a CAGR of 6.3%, significantly outpacing dairy growth of 2.8%. Growth is driven by the rapid rise of functional and specialty beverages, including plant-based drinks, cold-brew coffee, kombucha, and vitamin-fortified products, all of which require effective thermal processing for pathogen control and shelf-life extension. The global beverage market is growing at 4.8% annually, with functional segments advancing at 8.2-9.5%. Increasing regulatory scrutiny, higher product diversification, and underpenetration in emerging markets further support accelerated adoption of pasteurization vessels in this segment.

Regional Insights and Trends

Europe Leads Pasteurization Vessel Market Through Regulation, Technology Leadership, and Sustainability Focus

Europe represents the largest regional market for pasteurization vessels, accounting for over 35% of global revenue in 2026. The market is expanding at a steady CAGR of 5.2%, supported by a combination of strict food safety regulations and strong technological leadership. Germany, France, and the United Kingdom together contribute nearly 55-60% of total European demand, reflecting their well-established dairy and beverage processing industries.

Germany leads regional demand, driven by its globally recognized dairy processing equipment manufacturing base and rigorous regulatory compliance requirements. France follows, supported by ongoing dairy industry modernization initiatives, while Spain’s expanding beverage sector provides additional growth momentum. In the United Kingdom, post-Brexit regulatory harmonization and the introduction of independent standards are accelerating equipment replacement and upgrade cycles.

The regulatory environment remains a key market driver. EU Regulation 853/2004 and harmonized EN standards enable standardized equipment specifications across member states, benefiting pan-European manufacturers. Sustainability initiatives under the EU Green Deal, including carbon neutrality targets by 2050, are further encouraging adoption of energy-efficient systems. Additionally, circular economy regulations emphasizing repairability and material recovery are shaping product design strategies.

The competitive landscape is mature, with 8-12 established manufacturers holding strong positions. Competition centers on energy efficiency, automation integration, and sustainability-focused innovation, supported by engineering hubs in Germany, Switzerland, and the Netherlands.

Asia-Pacific Emerges as Fastest-Growing Pasteurization Vessel Market Driven by Dairy Expansion

Asia-Pacific stands out as the fastest-growing regional market for pasteurization vessels, expanding at a robust CAGR of 6.5%, well above the global average growth rate of 5.1%. The region currently accounts for approximately 25-28% of global market revenue and is projected to increase its share to 32-36% by 2033, reflecting strong macroeconomic fundamentals and rapid industrialization of food and beverage processing. China, India, and Japan together contribute nearly 70-75% of total regional market volume, underlining their central role in shaping demand dynamics.

Growth is primarily driven by China’s ongoing dairy industry modernization and the rapid expansion of its beverage manufacturing sector, both of which require large-scale, efficient pasteurization infrastructure. Government-led initiatives supporting rural dairy development and investments in food processing facilities further create predictable and sustained equipment demand. In India, rising milk production, growing consumption of packaged dairy products, and the development of export-oriented processing plants are driving substantial capital expenditure on pasteurization systems. Meanwhile, ASEAN countries such as Vietnam, Thailand, and Indonesia represent emerging high-potential markets, supported by increasing dairy consumption and relatively low existing installed capacity.

From a supply-side perspective, Asia-Pacific benefits from lower labor costs and improved technical capabilities, enabling cost-competitive local manufacturing. Strategic investments by global equipment suppliers and technology partnerships with regional manufacturers are accelerating localization, technology transfer, and long-term market penetration.

Competitive Landscape

The global pasteurization vessel market exhibits moderate consolidation characteristics, with the top 5-7 manufacturers controlling approximately 50-55% of global market share, indicating a competitive market structure with meaningful opportunities for differentiated competitors. Market leadership is concentrated among European and North American manufacturers with established reputations for quality and regulatory compliance. Fragmentation in developing markets provides opportunities for regional manufacturers with localized cost advantages and customer relationship strengths.

Market concentration is increasing gradually, driven by technology investments requiring substantial capital and regulatory expertise, creating competitive advantages for larger, better-capitalized manufacturers. Competitive positioning differentiates along dimensions of technology sophistication (automation, digital integration), manufacturing quality and certifications, service network breadth, and product line comprehensiveness.

Key Developments:

- In 2023, leading manufacturers, including GEA Group and Tetra Pak Technologies, have introduced IoT-enabled pasteurization systems with cloud-based monitoring platforms enabling remote diagnostics, predictive maintenance scheduling, and automated compliance documentation.

Companies Covered in Pasteurization Vessel Market

- Alfa Laval AB

- APV, An SPX FLOW Brand

- Bucher Industries AG

- C. van't Riet Dairy Technology B.V.

- Della Toffola S.p.A.

- Dion Engineering Ltd.

- Feldmeier Equipment, Inc.

- GEA Group AG

- IDMC Limited

- INOXPA S.A.

- JBT Corporation

- KHS GmbH

- Krones AG

- Marlen International, Inc.

- MicroThermics, Inc.

- Paul Mueller Company

- Pentair plc

- Schneider Electric SE

- SPX FLOW, Inc.

- Tetra Pak International S.A.Other Market Players

Frequently Asked Questions

The Pasteurization Vessel market is estimated to be valued at US$ 6.0 Bn in 2026.

The key demand driver for the Pasteurization Vessel market is the rapid expansion of industrial dairy and beverage processing driven by stricter food safety regulations and rising consumption of packaged products.

In 2026, the Europe region will dominate the market with an exceeding 35% revenue share in the global Pasteurization Vessel market.

Among end-use industries, the dairy industry has the highest preference, capturing beyond 50% of the market revenue share in 2026, surpassing other end use industries.

Alfa Laval AB, APV, An SPX FLOW Brand, Bucher Industries AG, C. van't Riet Dairy Technology B.V., Della Toffola S.p.A., Dion Engineering Ltd., Feldmeier Equipment, Inc., GEA Group AG, and IDMC Limited are a few leading players in the Pasteurization Vessel market.