- Food Ingredients & Additives

- Parmesan Cheese Market

Parmesan Cheese Market Size, Share, and Growth Forecast, 2025 - 2032

Parmesan Cheese Market By Material Type (Cow’s Milk Parmesan, Goat’s Milk Parmesan), Product Type (Grated Parmesan Cheese, Powdered Parmesan Cheese), Application, and Regional Analysis for 2025 - 2032

Parmesan Cheese Market Size and Trends Analysis

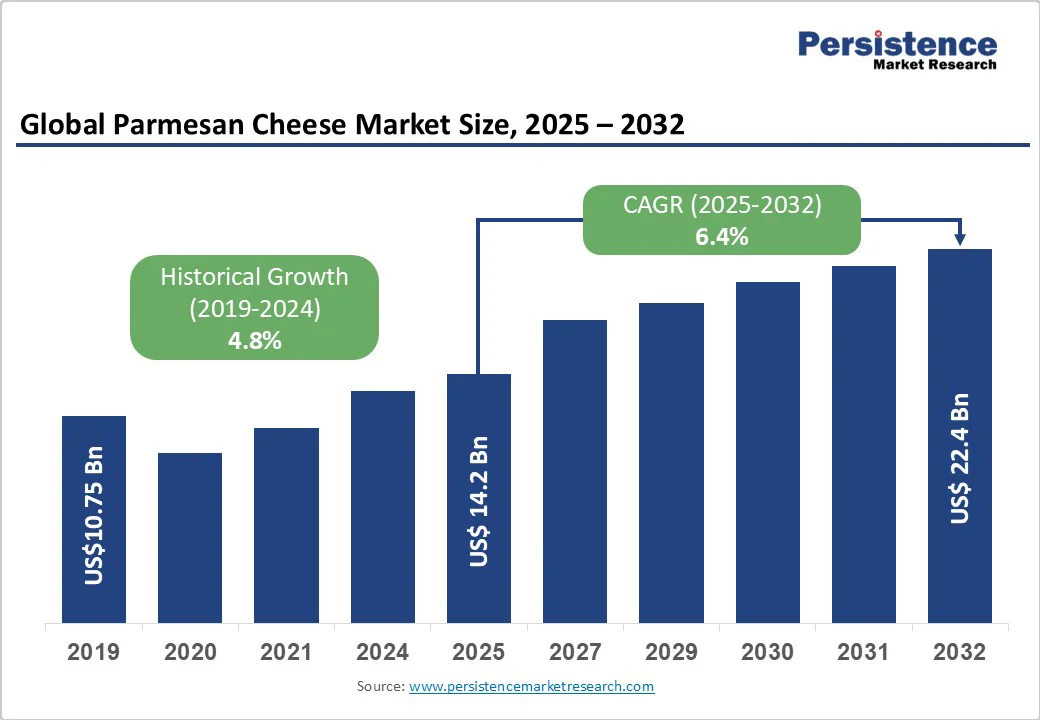

The global Parmesan cheese market size was valued at US$14.2 Bn in 2025 and is projected to reach US$22.4 Bn by 2032, growing at a CAGR of 6.4% between 2025 and 2032, driven by the rising consumer demand for convenient, ready-to-use ingredients and the rapid expansion of foodservice outlets. Premiumization trends, with higher adoption of authentic PDO (Protected Designation of Origin) cheeses such as Parmigiano-Reggiano, enhance overall market value.

Key Industry Highlights

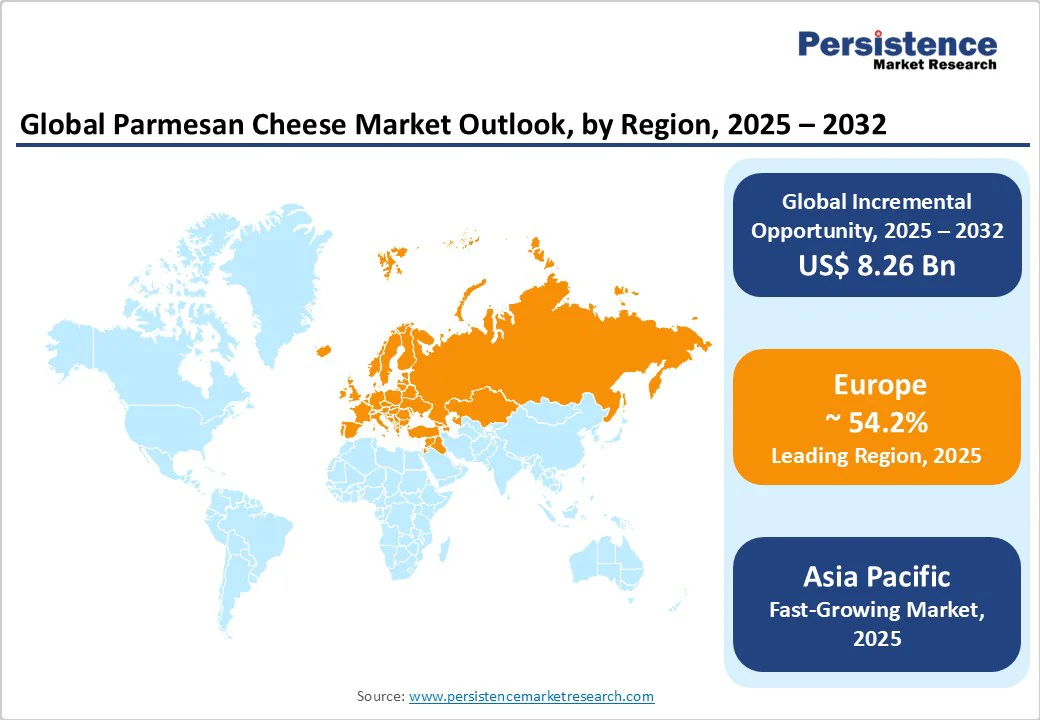

- Leading Region: Europe accounted for 54.2% of global revenue in 2025, driven by strong domestic consumption in Italy, Germany, and France, as well as strict PDO certifications.

- Fastest-growing Region: Asia Pacific is projected to grow at a CAGR of 7.8% between 2025 and 2032, led by the rising adoption of Western cuisines in China, India, and Japan.

- Investment Plans: Global dairy producers have invested over US$450 Mn since 2023 in lactose-free, organic, and value-added Parmesan cheese products to capture evolving consumer preferences.

- Dominant Product Type: The grated parmesan cheese segment is expected to hold a 38% market share in 2025, driven by its extensive use in pasta, pizza, sauces, and ready meals.

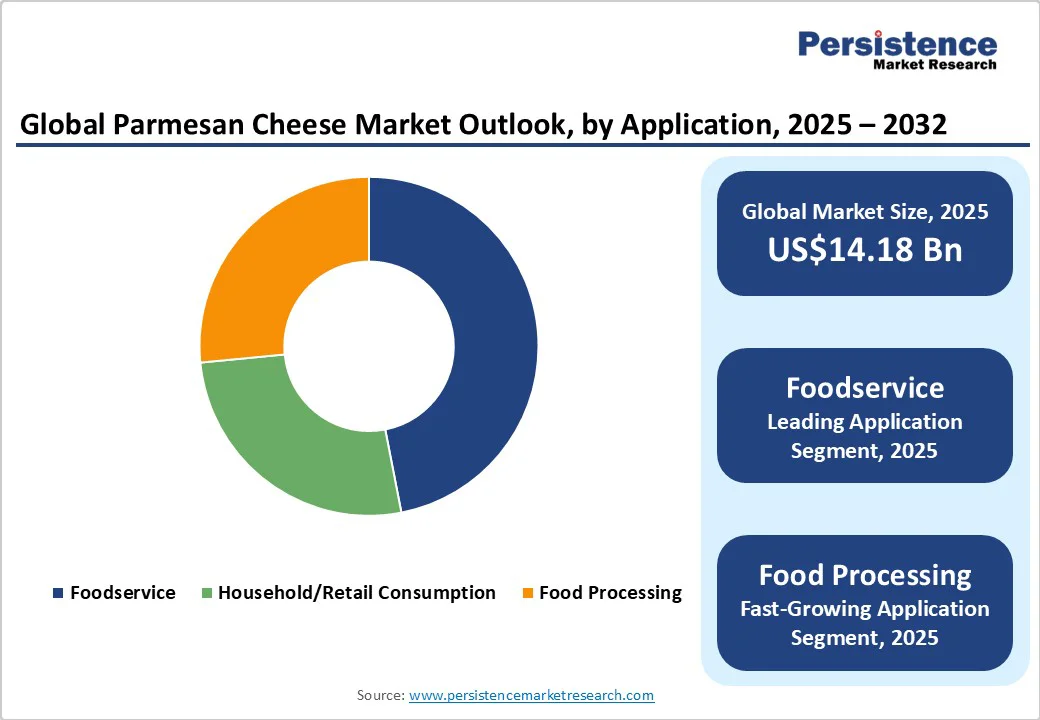

- Leading Application: The foodservice sector is anticipated to account for 46% of total demand in 2025, supported by restaurant chains, QSRs, and catering businesses worldwide.

| Key Insights | Details |

|---|---|

|

Parmesan Cheese Market Size (2025E) |

US$14.18 Bn |

|

Market Value Forecast (2032F) |

US$22.44 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Convenience, Foodservice Demand, and Premiumization

Global dietary patterns are shifting toward quick-preparation meals and restaurant dining. Parmesan cheese, particularly in its grated and powdered forms, aligns with this trend due to its ease of use in pasta, pizzas, salads, and baked goods. Quick-service restaurants (QSRs) and fast-casual outlets are expanding aggressively, creating steady demand for bulk and packaged Parmesan. Packaged retail innovations such as resealable tubs and single-serve sachets have expanded household penetration. For example, companies such as Kraft Heinz and Parmareggio supply bulk grated Parmesan to major quick-service restaurant chains, including Domino’s and Pizza Hut, enabling fast, consistent seasoning of pizzas and pasta dishes.

Consumers are increasingly willing to pay more for authentic Parmigiano-Reggiano and other PDO-certified varieties, which offer higher quality, traceability, and provenance. These cheeses often command 40% higher price points compared to non-certified counterparts. Aged variants, marketed for their stronger flavor profile, also benefit from premium positioning in specialty stores and gourmet e-commerce platforms.

For example, Consorzio del Parmigiano Reggiano markets authentic Parmigiano-Reggiano wheels with PDO certification through specialty stores and gourmet e-commerce platforms, such as Eataly and Murray’s Cheese, which command premium pricing due to their provenance and aging quality. This premiumization supports market bifurcation: commodity grated cheese dominates volumes, while artisanal PDO wheels capture high-margin segments. This dynamic is shaping dual supply chains where both mass production and artisanal production coexist.

Raw-Milk and Input Cost Volatility and Trade Barriers

Milk prices, feed costs, and energy expenses are highly volatile and significantly influence cheese production. As Parmesan requires extended aging, producers face additional financial exposure as capital remains tied up for 12-36 months. Historical price spikes in dairy feed have led to retail Parmesan price increases of 10-25% within a year, squeezing processor margins and discouraging new investment in capacity.

Parmesan cheese, particularly PDO varieties, faces risks from tariff impositions and trade disputes. U.S.-EU tariff tensions in recent years highlighted how duties directly increase landed costs, raising retail prices and depressing volumes. Import quotas and sanitary regulations further complicate cross-border flows. Such barriers make long-term planning difficult for exporters and can prompt buyers to turn to domestic substitutes.

Asia Pacific Expansion, and Packaged and E-Commerce Innovation

Urbanization, western diet adoption, and growing QSR presence are rapidly expanding the addressable market in the Asia Pacific. Pizza and pasta consumption is on the rise across China, India, and Southeast Asia, with Parmesan being a key ingredient. This region could contribute an additional US$7 Bn by 2032 compared to 2025 levels. Localized processing of grated and powdered formats, combined with strong cold-chain logistics, represents the clearest opportunity for growth-oriented players. Yili Group, one of China’s largest dairy companies, has invested in local processing facilities for grated Parmesan to cater to booming pizza and pasta consumption, supplying QSR chains like Pizza Hut and PizzaExpress.

Retail demand is shifting toward ready-to-use formats available online and through supermarkets. Packaged Parmesan, whether grated, powdered, or blended, benefits from e-commerce penetration and private-label expansion. Innovations such as single-use sachets for meal kits, resealable tubs for home use, and flavored blends are creating incremental demand. Digital channels also enable premium brands to communicate their origin, aging process, and traceability, thereby reinforcing consumer trust and boosting their willingness to pay. Chefbox in India has introduced single-serve Parmesan sachets as part of its subscription meal kits, helping busy urban consumers easily replicate Italian dishes at home.

Category-wise Analysis

Material Type Insights

In 2025, cow’s milk Parmesan continues to dominate the market, accounting for more than 75% of total sales. This stronghold is largely due to the widespread production and consumption of PDO-certified cheeses such as Parmigiano-Reggiano and Grana Padano, which are traditionally and exclusively made from cow’s milk. These varieties are deeply rooted in Italian culinary heritage and enjoy international recognition for their authenticity, quality, and consistent flavor profile. Consumer preference for the rich, nutty, and umami-packed taste of cow’s milk Parmesan further reinforces its market leadership. Cow’s milk Parmesan benefits from a well-established supply chain and broad distribution in both retail and foodservice sectors.

Goat’s milk Parmesan is emerging as the fastest-growing segment in the material type category, projected to register a robust CAGR of 7.1% from 2025 to 2032, fueled by the rising global awareness of lactose intolerance and the increasing popularity of dairy alternatives that are easier to digest. Goat’s milk naturally contains less lactose and different protein structures compared to cow’s milk, making it a preferred choice for individuals with sensitivities. The rise of specialty cheese consumption in premium retail outlets and gourmet foodservice establishments is driving demand for unique, artisanal offerings, such as goat’s milk Parmesan.

Product Type Insights

Grated Parmesan cheese is expected to lead the market in 2025, accounting for approximately 38% of the market share, driven by its widespread use in everyday cooking and commercial food preparation. Grated Parmesan offers unmatched convenience and is frequently used as a topping for pasta, pizza, soups, and salads, making it a staple in both home kitchens and professional foodservice operations. The format provides easy portion control, extended shelf life, and seamless integration into pre-packaged meals, further cementing its popularity.

Shredded Parmesan is expected to be the fastest-growing product segment, with a projected CAGR of 7.2% between 2025 and 2032. This growth is closely tied to the increasing consumption of frozen and refrigerated ready meals, salads, and gourmet casual dining dishes, particularly in North America and the Asia Pacific markets. Shredded Parmesan offers a more textured and visually appealing finish compared to grated formats, making it ideal for meal kits, artisan pizzas, and premium prepared foods. Its versatility and superior meltability also appeal to food manufacturers and chefs seeking to enhance the presentation and taste of their products.

Application Insights

The foodservice industry emerged as the largest end-use application segment in 2025, contributing to 46% of the total global demand for Parmesan cheese. Restaurants, catering companies, quick-service restaurants (QSRs), and institutional food providers are major buyers of Parmesan in bulk formats such as grated, shredded, and pre-portioned packs. Its rich flavor and versatility make it an essential ingredient in a wide variety of dishes, including pasta, pizza, Caesar salads, risottos, and gourmet sandwiches. High consumption volume in commercial kitchens and consistent menu presence ensure that foodservice remains the backbone of Parmesan demand.

The food processing segment is projected to be the fastest-growing application category, with an estimated CAGR of 7.5% through 2032. This growth is underpinned by the increasing incorporation of Parmesan into value-added products such as packaged snacks, savory sauces, frozen entrees, and ready-to-eat meals. The rise of convenience food culture, particularly in urban areas, is creating new opportunities for food processors to capitalize on Parmesan’s bold flavor and functional properties. Parmesan's ability to enhance taste, provide texture, and act as a natural preservative due to its low moisture content makes it highly suitable for processed food applications.

Regional Insights

Europe Parmesan Cheese Market Trends - PDO premium market protected by EU regulations and exports

Europe leads the market, with a share of 54.2% in 2025. Italy dominates production, with Parmigiano-Reggiano and Grana Padano serving as the gold standard of quality. Together, PDO cheeses account for more than half of European market revenues, with export demand adding substantial incremental value. Consumption within Germany, France, the U.K., and Spain also remains high, reflecting ingrained culinary traditions. Regulation under the EU PDO framework secures exclusivity for authentic Parmigiano-Reggiano and Grana Padano, reinforcing premium pricing while limiting geographic expansion of production. This system protects small cooperatives and ensures quality, but can restrict supply growth relative to surging global demand.

Investment in Europe emphasizes traceability systems, sustainable dairy practices, and modernization of aging facilities. Cooperative consortia are actively strengthening branding strategies to counter imitation Parmesan in global markets. Export demand from North America and Asia Pacific provides robust external growth opportunities.

Asia Pacific Parmesan Cheese Market Trends - Urbanization driving premium and mass-market growth

Asia Pacific is the fastest-growing region, benefiting from strong urbanization, dietary westernization, and rising disposable incomes. China, Japan, India, and ASEAN markets collectively drive demand. Pizza chains, casual dining restaurants, and international QSR brands are aggressively expanding, incorporating Parmesan as a staple ingredient in pasta, pizzas, soups, and bakery products. China and Japan represent the largest markets, with Japan displaying higher per-capita consumption due to earlier westernization. India and Southeast Asia, though starting from lower bases, are recording double-digit annual growth rates as organized retail and online grocery gain traction.

Regulatory environments remain fragmented, with China having strict labeling and safety requirements, while India imposes varying import duties. These create hurdles for European PDO exporters, though they also encourage multinational processors to establish local packaging and co-packing operations. Cold-chain infrastructure investment is accelerating, which will reduce barriers for fresh and specialty imports. With APAC’s middle-class population expanding rapidly, opportunities lie in both premium PDO imports targeted at affluent consumers and mass-market grated products tailored for mainstream households.

North America Parmesan Cheese Market Trends - Retail and QSR demand with tariff effects and private-label focus

North America represents one of the most dynamic markets for Parmesan cheese, with the U.S. leading consumption. Retail demand is concentrated in grated and powdered formats, widely sold under national brands and private labels. PDO imports from Italy remain significant but cater mainly to premium buyers. The QSR ecosystem, dominated by pizza and pasta chains, sustains bulk demand for grated Parmesan, while home cooking trends have reinforced supermarket sales.

Regulation plays a key role, as tariff changes on European imports directly impact shelf prices. For instance, previous tariff hikes temporarily elevated retail costs by more than 20% in certain stores, prompting some substitution with domestic products. Competitive intensity is high, with major players such as Kraft Heinz, Saputo, BelGioioso, and Sargento commanding strong brand equity. Looking forward, continued growth in e-commerce grocery sales and the popularity of meal kits will provide additional momentum.

Competitive Landscape

The global Parmesan cheese market is structurally split. PDO-certified and artisanal segments are fragmented, dominated by Italian cooperatives and consortia such as Parmigiano-Reggiano and Grana Padano. Conversely, the industrial grated and powdered segment is consolidated among a few multinational dairy processors such as Kraft Heinz, Saputo, and Lactalis. Private labels also exert pressure, especially in supermarkets. This dual structure creates both opportunities and risks: fragmented premium segments command high margins, while consolidated industrial processing fosters price competition and economies of scale.

Market leaders emphasize dual-track portfolios, balancing mass-volume grated cheese with premium PDO offerings. Strategies include long-term foodservice contracts, digital branding for provenance, and cost-hedging through diversified sourcing. Emerging business models integrate e-commerce subscription services, direct-to-consumer packaging, and localized processing in high-growth regions such as Asia Pacific.

Key Industry Developments

- In June 2024, Granarolo S.p.A. (Italy) launched a lactose-free Parmesan range in both block and grated formats, addressing growing concerns about lactose intolerance in domestic and export markets.

- In March 2024, Saputo Inc. (Canada) rolled out a parmesan-infused shredded cheese blend for the foodservice sector, targeting quick-service restaurants and pizza chains in North America.

Companies Covered in Parmesan Cheese Market

- Lactalis Group

- BelGioioso Cheese Inc.

- Granarolo S.p.A.

- Saputo Inc.

- Arla Foods

- Parmigiano-Reggiano Consortium

- Grana Padano Consortium

- Kraft Heinz Company

- Sargento Foods Inc.

- Grande Cheese Company

- Parmareggio S.p.A.

- Fonterra Co-operative Group

- Murray Goulburn/Saputo Australia

- Galbani (Lactalis)

- President Cheese (Groupe Lactalis)

- Emmi Group

- Hochland SE

- Valio Ltd.

- Dairy Farmers of America

- Tillamook County Creamery Association

Frequently Asked Questions

The Parmesan cheese market size is estimated at US$14.18 Bn in 2025.

By 2032, the market is projected to reach US$22.44 Bn, reflecting steady demand across retail and foodservice channels.

The rising consumption of convenience foods such as pasta, pizzas, and ready meals, and the growing demand for organic, lactose-free, and clean-label cheese products are some key trends.

The grated Parmesan cheese segment is anticipated to hold the largest market share at 38% in 2025.

The Parmesan cheese market is forecast to grow at a CAGR of 6.4% from 2025 to 2032.

The key players in the Parmesan cheese market are Lactalis Group, BelGioioso Cheese Inc., Granarolo S.p.A., Saputo Inc., and Arla Foods.