- Automotive Components & Materials

- Pantograph Charger Market

Pantograph Charger Market Size, Share, and Growth Forecast 2026 - 2033

Pantograph Charger Market by Component Type (Hardware, Software, Services), Charging Type (Direct Current Fast Charging (DCFC), Level 2 Charging, Level 1 Charging), Charging Infrastructure Type (Off-Board Top-Down Pantograph, On-Board Bottom-Up Pantograph), Application (Public Transit Charging, Depot Charging, Fleet & Commercial Charging), and Regional Analysis, 2026 - 2033

Pantograph Charger Market Size and Trend Analysis

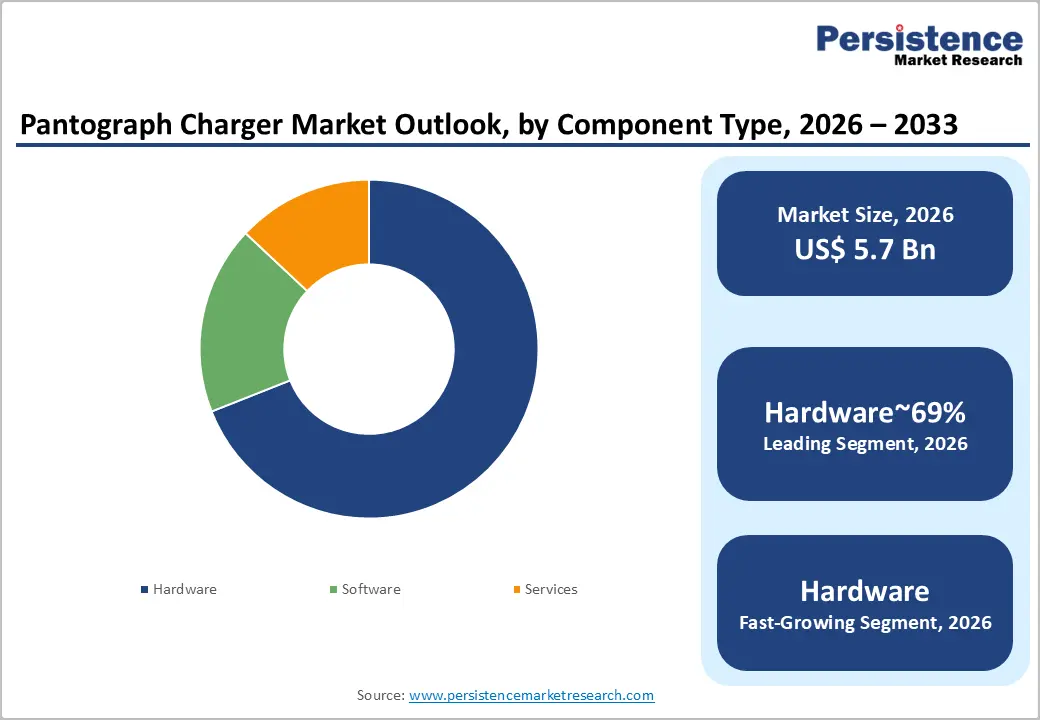

The global pantograph charger market is expected to be valued at US$ 5.7 billion in 2026 and is projected to reach US$ 29.1 billion by 2033, growing at a CAGR of 26.2% between 2026 and 2033.

Automated conductive charging infrastructure for zero-emission transit fleets is shifting from pilot-phase novelty to municipal procurement standard, compressing the technology adoption curve that once stretched a decade into fewer than five years.

Key Industry Highlights:

- Leading Region: North America's regulatory-driven procurement dominance positions the region to sustain its 37.0% global revenue share through 2030, with the Bipartisan Infrastructure Law's US$ 5.6 billion clean bus allocation creating a multi-year order backlog that insulates the region's leading suppliers from demand cyclicality, a structural advantage no other region currently replicates at this funding scale.

- Fast-Growing Region: Asia Pacific's 29.9% CAGR, the fastest of any region in the pantograph charger market, reflects the convergence of China's 600,000-unit electric bus fleet requiring infrastructure densification and India's PM e-Bus Sewa programme unlocking Tier-2 city demand; the region's state-directed procurement model compresses the 7-year adoption cycle typical of Western democratic procurement into 3-year deployment windows.

- Leading Segment: Hardware's 69.0% segment dominance is structurally durable because physical charging arms and power conversion units represent 20-year capital assets that municipalities budget as public infrastructure, not technology purchases, making them resistant to the commoditisation pressures that software and services segments typically face within five years of market maturation.

- Fast-Growing Infrastructure: On-Board bottom-up pantograph is the fast-growing infrastructure sub-segment, with Solaris Bus & Coach's 2024 Urbino 18 integration demonstrating a vehicle-mounted architecture that eliminates fixed station civil works, a critical cost reduction for dense urban networks deploying opportunity charging at multiple stops rather than concentrating investment in terminal infrastructure alone.

- Key Opportunity: Depot Charging's acceleration across private fleet operators, including intercity coach, school, and airport shuttle segments, represents the highest-margin strategic opportunity for integrated solution providers who combine pantograph hardware with demand-response energy management software, given that Wabtec Corporation's 2024 deployment showed demonstrable peak demand charge reduction, a financial outcome that shortens operator payback periods and accelerates purchasing decisions independent of regulatory mandates.

Market Dynamics

Drivers - Binding Zero-Emission Fleet Mandates Accelerating Municipal Charging Infrastructure Procurement

Transit authorities that delay pantograph charger investments now face contractual and regulatory non-compliance risk, making capital allocation a matter of operational continuity rather than discretionary spend. California's Advanced Clean Transit (ACT) regulation, enforced by the California Air Resources Board (CARB), requires all new transit bus purchases to be zero-emission from 2029, prompting agencies such as Los Angeles Metro to contract overhead pantograph charging systems across multiple depots since 2023.

Over the next two to three years, similar mandates cascading across Canada, Australia, and South Korea will replicate this procurement wave, sustaining double-digit annual order growth for automated charging system suppliers.

Expansion of High-Power Charging Standards: Reducing Interoperability Barriers

Fragmented charging interface standards historically forced transit operators to commit to single-vendor ecosystems, but converging global standards are now unlocking competitive multi-vendor procurement. The IEC 61851-23 standard for DC charging and the ISO 15118 vehicle-to-grid communication protocol together establish the technical baseline that ABB and Siemens Mobility have both integrated into their latest pantograph product families, effective 2023-2024. As standardisation matures, fleet operators gain negotiating leverage, broadening the addressable buyer base and pulling mid-tier municipalities, previously locked out by integration complexity, into the pantograph charger market.

Restraints - High Capital Expenditure and Civil Engineering Complexity Suppressing Tier-2 City Adoption

The installed cost of an off-board top-down pantograph charging station, encompassing grid connection upgrades, structural mounting, and power electronics, routinely exceeds US$ 150,000 per unit according to European Bank for Reconstruction and Development (EBRD) project assessments, creating a prohibitive barrier for smaller municipalities operating on constrained infrastructure budgets.

The U.S. Federal Transit Administration (FTA) requires matching fund contributions from local agencies under its Low or No Emission Vehicle Program, meaning cities without strong local tax bases struggle to unlock federal co-financing. New entrants without established financing partnerships face a structurally longer sales cycle than incumbents who bundle equipment supply with project finance solutions.

Supply Chain Concentration in Rare-Earth and Power Semiconductor Components

Pantograph charging hardware depends on high-power insulated-gate bipolar transistors (IGBTs) and silicon carbide wafer semiconductors, the supply of which remains concentrated among a small number of Asian fabricators, creating margin compression and lead-time risk for Western assemblers.

U.S. Section 301 tariffs on Chinese-origin electrical components, maintained and reviewed under the Office of the United States Trade Representative (USTR) in 2024, add an estimated 25% cost premium on imported power electronics, squeezing bill-of-materials costs for North American integrators. Incumbent suppliers with vertically integrated power electronics divisions absorb this friction more effectively than new entrants dependent entirely on spot-market semiconductor procurement.

Opportunities - On-Route Opportunity Charging Networks Enabling Battery Downsizing for Urban Bus Fleets

Infrastructure developers and rolling-stock manufacturers should jointly pursue on-route opportunity charging deployments at bus terminals and traffic signal dwell points, where a 30 second pantograph connection can extend a bus's daily range without requiring larger, heavier battery packs.

Heliox Energy deployed a scalable on-route pantograph charging corridor for Connexxion bus operations in the Netherlands in 2023, demonstrating that partial top-up charging at terminus points reduces battery capacity requirements by an estimated 30%, directly lowering bus acquisition costs. Charging infrastructure providers with modular, scalable architectures, particularly those compliant with open-protocol smart charging management, are best positioned, provided grid operators co-invest in local substation capacity.

EV Fleet Electrification for Private Coach and Long-Distance Bus Operators

Private coach operators and intercity bus companies represent an underserved buyer segment that is beginning to evaluate depot charging pantograph systems as fleet electrification economics improve with falling battery costs. Flixbus announced a pan-European electric coach expansion strategy in 2024, targeting overnight depot charging solutions that align precisely with high-power pantograph infrastructure capable of delivering 150 to 600 kW per session.

Technology providers offering turnkey depot charging solutions, combining hardware, energy management software, and grid balancing services, hold the strongest position, but realisation depends on continued reduction in long-haul electric bus total cost of ownership below that of diesel equivalents by 2027 - 2028.

Category-wise Analysis

Component Type Insights

Hardware commands 69% of the global pantograph charger market in 2026, equivalent to US$ 3.93 Billion, because the physical charging arm, power conversion unit, and mounting structure constitute the non-substitutable capital investment in every deployment. Municipal transit agencies, the dominant buyer class, procure charging hardware as long-life infrastructure assets with 15 year operational lifespans, making initial hardware selection a lock-in decision with minimal replacement frequency.

Alstom's SRS ground-level supply and pantograph product catalogue, widely adopted by European rail and bus operators, illustrates how hardware differentiation on reliability metrics creates durable competitive moats. Per Bloomberg New Energy Finance (BNEF) data, hardware accounts for the majority of total charging system cost in transit deployments, sustaining its revenue dominance.

Charging Type Insights

Direct current fast charging (DCFC) holds 57% of the global pantograph charger market in 2026, valued at US$ 3.25 Billion, driven by transit operators' non-negotiable requirement to recharge buses within driver turnaround windows of 10 minutes at terminus points. City bus operators in Stockholm and Amsterdam have deployed 450 kW DCFC pantograph systems from Furrer+Frey AG at major interchange hubs, enabling single-route buses to recharge between peak service cycles without returning to depot.

Level 2 Charging is the fastest-growing charging type segment, accelerated by overnight depot charging programmes where sustained lower-power delivery across 8 hour rest periods suits smaller urban minibus and paratransit fleets. Kempower launched its modular T-Series depot charging platform in 2023, designed for scalable Level 2 deployment across mixed electric bus fleets, and has secured contracts with Nordic and Baltic public transit operators.

Charging Infrastructure Type Insights

Off-Board Top-Down Pantograph infrastructure accounts for 72.0% of the global pantograph charger market in 2026, representing US$ 4.10 Billion, because ground-fixed overhead arm systems concentrate high-cost power electronics in the stationary infrastructure rather than the vehicle, reducing bus weight and per-vehicle capital cost. Municipal transit authorities in Geneva and Gothenburg rely on top-down fixed pantograph stations from Schunk Transit Systems at terminus points, where the charging arm descends automatically onto a bus roof contact as the vehicle parks, a fully automated process requiring zero driver interaction.

On-Board bottom-up pantograph is the fast-growing infrastructure sub-segment, gaining traction because vehicle-mounted pantograph arms allow charging at any standard overhead contact rail point, removing the need for dedicated fixed-station civil works. Solaris Bus & Coach integrated an on-board bottom-up pantograph system into its Urbino 18 electric articulated bus in 2024, targeting city contracts where retrofitting overhead charging infrastructure at multiple stops is cost-prohibitive.

Application Insights

Public transit charging represents 68.0% of the global pantograph charger market in 2026, equating to US$ 3.88 Billion, as city-operated electric bus fleets constitute the primary commercial deployment environment for automated conductive charging today. Urban transit authorities in Paris (RATP) and Berlin (BVG) have committed to full electric bus fleet transitions with integrated pantograph charging infrastructure, deploying systems at both terminus and mid-route points to maintain schedule adherence across high-frequency corridors.

Depot charging is the fast-growing application segment, propelled by fleet operators consolidating overnight recharging at centralised maintenance facilities to manage grid load and battery health through smart energy management systems. Wabtec Corporation deployed an integrated depot charging management platform for a North American commuter rail operator in 2024, demonstrating that depot-level pantograph systems can reduce peak grid demand charges by coordinating vehicle charging schedules with utility time-of-use tariffs.

Regional Insights

North America Pantograph Charger Market Trends and Insights

North America accounts for 37% of the global pantograph charger market in 2026, representing US$ 2.11 Billion, underpinned by the Bipartisan Infrastructure Law (BIL) of 2021, which allocated US$ 5.6 Billion specifically for clean transit bus procurement and charging infrastructure through the FTA's Low or No Emission Vehicle Program.

State-level zero-emission mandates in California, New York, and Washington are synchronising fleet replacement cycles with charging infrastructure buildout, creating concentrated procurement windows that reward suppliers capable of delivering turnkey automated charging solutions at scale. Over the next three years, federal grant disbursement acceleration under the BIL is expected to pull forward orders currently in feasibility stages into binding contracts.

- United States Pantograph Charger Market Size

The United States represents an estimated 82% of the North America regional pantograph charger market, reflecting the scale of its municipal transit network and the concentration of federal infrastructure funding through the FTA. Transit agencies such as New York's Metropolitan Transportation Authority (MTA) are actively tendering electric bus charging infrastructure as part of multi-year fleet electrification programmes. Continued grant disbursement under the BIL through 2026-2027 will sustain above-regional-average order growth in the U.S. market.

Europe Pantograph Charger Market Trends and Insights

Europe holds 28% of the global pantograph charger market in 2026, equivalent to US$1.60 billion, driven by the EU's Fit for 55 climate package target of reducing transport emissions by 55% by 2030 and national-level bus electrification programmes that have made Europe the most mature market for overhead pantograph automated charging deployment. The Clean Vehicles Directive (2019/1161), which sets minimum procurement quotas for zero-emission vehicles across EU member state public transport contracts, sustains a structural baseline of pantograph charger demand that is immune to political cycle fluctuations. Emerging Eastern European markets, supported by EU Cohesion Funds, are entering their first large-scale electric bus procurement cycles, extending the regional growth runway beyond core Western European markets.

- Germany Pantograph Charger Market Size

Germany accounts for an estimated 22% of the European pantograph charger market, driven by the Nationale Leitstelle Ladeinfrastruktur's (NOW GmbH) funding programmes supporting electric bus charging infrastructure across German municipalities. Siemens Mobility's domestic manufacturing base in Munich gives German transit operators a local-supply advantage for both hardware and integration services. Germany's Verkehrswende (transport transition) policy framework targeting 100% zero-emission urban buses before 2035 sustains long-duration procurement visibility.

- United Kingdom Pantograph Charger Market Size

The United Kingdom holds an estimated 15% of the Europe pantograph charger market, supported by the Zero Emission Bus Regional Areas (ZEBRA) scheme administered by the UK Department for Transport, which co-funded over 1,000 electric buses across English regions by 2024. First Bus and Go-Ahead Group have both invested in depot pantograph charging infrastructure as part of ZEBRA-funded fleet transitions. The UK's commitment to ending new diesel bus sales by 2032 provides a decade-long structural demand runway for charging infrastructure suppliers.

- France Pantograph Charger Market Size

France represents an estimated 13% of the European pantograph charger market, accelerated by RATP's commitment to operating a fully electric urban bus network in Paris by 2025, the first major European capital to set such a binding operational deadline. Île-de-France Mobilités, the regional transport authority, has contracted pantograph charging systems for multiple bus depots across the Greater Paris network. France's Plan d'Investissement dans les Transports allocates dedicated capital for charging infrastructure co-investment between national government and regional authorities through 2030.

Asia Pacific Pantograph Charger Market Trends and Insights

Asia Pacific accounts for 22.0% of the global pantograph charger market in 2026 advances at the a positive CAGR propelled by China's massive state-directed electric bus procurement programme and India's rapidly scaling PM e-Bus Sewa scheme targeting 10,000 electric buses across 169 cities. The region's combination of high urban density, state-owned transit operators with centralised procurement authority, and aggressive government subsidy frameworks compresses adoption timelines compared to Western markets. By 2030, Asia Pacific is on trajectory to surpass Europe as the second-largest regional market for pantograph charging infrastructure.

- China Pantograph Charger Market Size

China constitutes an estimated 62% of the Asia Pacific pantograph charger market, reflecting its position as the world's largest electric bus fleet operator with over 600,000 electric buses in service per Ministry of Transport data. CRRC Corporation Limited and BYD Company Limited integrate compatible pantograph charging interfaces into new electric bus platforms sold to municipal operators, creating co-dependent demand for domestic charging infrastructure. China's 14th Five-Year Plan targets for new energy vehicle public transit penetration sustain near-term procurement volume at scale.

- India Pantograph Charger Market Size

India represents an estimated 16% of the Asia Pacific pantograph charger market, a share expanding rapidly as the PM e-Bus Sewa programme, launched by the Ministry of Housing and Urban Affairs in 2023, deploys electric buses in Tier-1 and Tier-2 cities previously unreached by electrification. Tata Motors and Olectra Greentech are supplying electric buses to state transport undertakings, each requiring compatible depot and terminus charging infrastructure. India's centralised procurement through Convergence Energy Services Limited (CESL) is standardising charging interface specifications, which will accelerate pantograph system adoption over plug-in alternatives in large depot environments by 2027.

- Japan Pantograph Charger Market Size

Japan accounts for an estimated 12% of the Asia Pacific pantograph charger market, with demand anchored in Tokyo Metropolitan Bureau of Transportation's electric bus pilot programmes and national commitments under Japan's Green Growth Strategy targeting carbon neutrality by 2050. Hitachi Energy supplies power conversion and grid integration components for Japanese transit electrification projects, leveraging its established utility relationships. Japan's uniquely stringent seismic safety standards for electrical infrastructure create a technical barrier that favours domestic integrators and limits rapid market entry by foreign pantograph hardware suppliers.

Competitive Landscape

The pantograph charger market operates as a moderately concentrated oligopoly at the hardware tier, with ABB, Siemens Mobility, and Heliox Energy collectively holding an estimated 45-50% of global installed capacity, competing primarily on charging power output, uptime reliability guarantees, and depth of grid integration software.

The dominant strategic theme is vertical integration of energy management software with physical charging hardware, suppliers offering fleet operators a unified platform for smart charging scheduling, battery health monitoring, and demand response command, increasing switching costs, and extending contract tenure. The most consequential disruptive entrant is Kempower, which has grown from a Nordic niche player to a pan-European contender since 2021 by offering modular, scalable depot architectures that reduce civil engineering complexity, directly challenging the project-finance-heavy model of incumbents.

Key Developments:

- March 2024: ABB launched its Terra 360 Modular pantograph-compatible charging platform designed for transit depot deployments, supporting scalable power outputs from 90 kW to 360 kW per connection point without requiring additional civil works at existing depot sites.

- September 2024: Heliox Energy announced a strategic partnership with Transdev to deploy automated pantograph charging infrastructure across Transdev's electric bus operations in the Netherlands, France, and Germany, covering an estimated 800 charging points over a three-year rollout.

- January 2025: Ekoenergetyka-Polska secured a framework contract with the City of Warsaw to supply overhead pantograph charging systems for 200 Solaris electric buses, representing one of Central Europe's largest single pantograph charger procurement events to date.

Companies Covered in Pantograph Charger Market

- ABB

- Siemens Mobility

- Schunk Transit Systems

- Heliox Energy

- Kempower

- Wabtec Corporation

- ChargePoint

- Dekon Power

- Medha Servo Drives

- Ekoenergetyka-Polska

- Hitachi Energy

- Alstom

- Furrer+Frey AG

- CRRC Corporation Limited

- BYD Company Limited

- Solaris Bus & Coach

- Proterra

- Ampcontrol

- Conductix-Wampfler

- IPT Technology

Frequently Asked Questions

The global pantograph charger market is valued at US$ 5.7 billion in 2026 and is projected to reach US$ 29.1 billion by 2033 at a CAGR of 26.2%, with the primary growth catalyst being the binding zero-emission transit fleet mandates enacted by governments across North America, Europe, and Asia Pacific. The IEA's global electric bus fleet expansion forecast and accelerating municipal procurement cycles driven by AFIR and equivalent national regulations underpin the credibility of this trajectory.

Two primary drivers are propelling growth: first, CARB's Advanced Clean Transit regulation mandating zero-emission bus purchases in California from 2029 is replicating across multiple U.S. states, creating a structural procurement pipeline for automated charging infrastructure; second, the convergence of IEC 61851-23 and ISO 15118 interoperability standards is removing the single-vendor lock-in that previously constrained mid-tier municipal operators from committing to pantograph systems. Together, these forces are expanding the addressable buyer base from major transit authorities to smaller city and regional operators.

Hardware holds the largest segment share at 69.0% of the pantograph charger market in 2026, because physical charging arms, power electronics enclosures, and mounting infrastructure represent non-substitutable, long-life capital assets that form the majority of total system cost in every transit deployment. The segment's stability rests on 20 year asset lifespans and public infrastructure budgeting conventions that treat charging hardware equivalently to bus shelters or road fixtures, making volume replacement cycles predictable and margin erosion from software commoditisation largely irrelevant to near-term revenue.

North America leads the pantograph charger market with 37.0% share in 2026, supported by two structural factors: the US$5.6 billion clean bus allocation under the Bipartisan Infrastructure Law, creating a funded multi-year procurement pipeline, and state-level zero-emission fleet mandates in California, New York, and Washington synchronising demand across the continent's largest transit agencies. North America's dominance is expected to remain intact through 2030, even as Asia Pacific's faster CAGR begins to close the absolute revenue gap.

The highest-value opportunity lies in deploying on-route opportunity charging networks at urban bus terminus and dwell points, enabling battery downsizing that cuts electric bus acquisition costs by an estimated 30%, a value proposition validated by Heliox Energy's Netherlands corridor deployment. Infrastructure developers and grid operators who co-invest in local substation capacity upgrades are best positioned to capture this opportunity, which materialises fully once CharIN's Megawatt Charging System (MCS) standard achieves broad vehicle-side adoption across European and North American bus manufacturers by approximately 2027.

ABB, Siemens Mobility, and Heliox Energy lead the pantograph charger market, competing primarily on charging power output reliability, smart energy management software integration depth, and ability to offer project finance bundling for large municipal contracts.