- Biotechnology

- Omnichannel Customer Engagement Market

Omnichannel Customer Engagement Market Size, Share, and Growth Forecast, 2026 - 2033

Omnichannel Customer Engagement Market by Offering (Software, Services), Deployment (Cloud-based, On-premises), Application (Customer Data & CRM Platforms, Marketing Campaign Orchestration, Conversational Customer Engagement, Mobile & Digital Messaging Engagement, Social Customer Interaction Management, Customer Engagement Analytics, Others, Industry, and Regional Analysis for 2026 - 2033

Omnichannel Customer Engagement Market Size and Trends

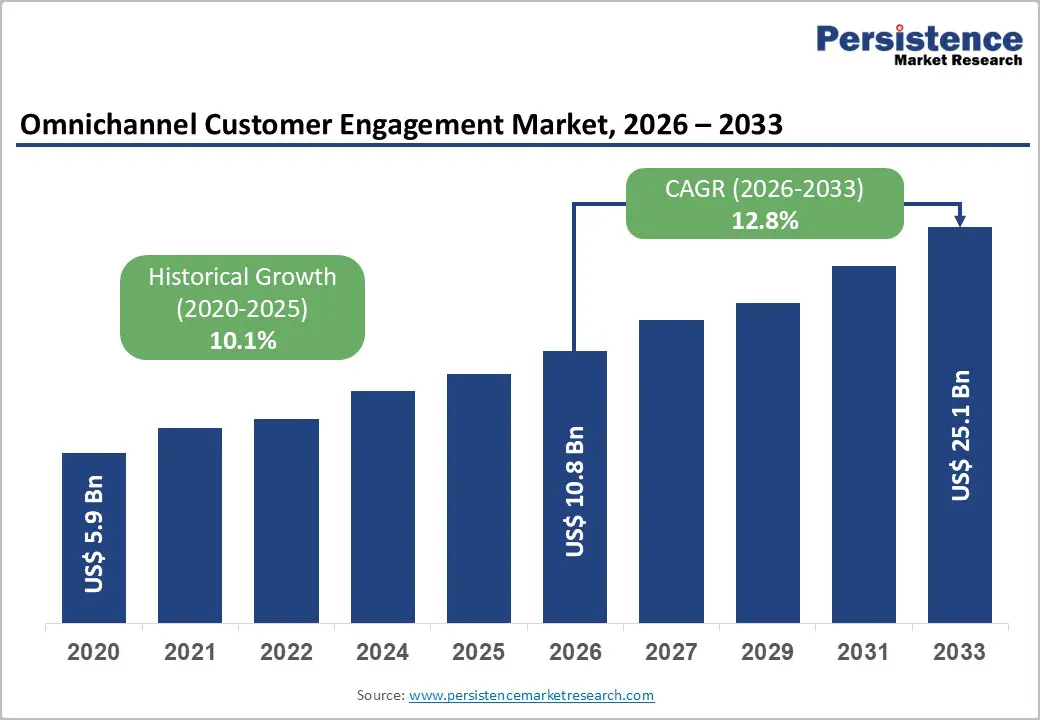

The global omnichannel customer engagement market size is projected to rise from US$10.8 Bn in 2026 to US$25.1 Bn by 2033. It is expected to grow at a CAGR of 12.8% from 2026 to 2033.

This substantial growth trajectory reflects accelerating digital transformation initiatives across enterprises worldwide, driven by rising customer expectations for seamless, consistent multi-channel interactions. Market expansion is further supported by the convergence of advanced data analytics and artificial intelligence, which enhances personalization and automation. Growing adoption of cloud-based deployments is enabling scalable omnichannel engagement across enterprises of all sizes.

Key Industry Highlights:

- Prominent Offering: Software dominates the market with over 65% share in 2026, valued at more than US$ 7.0 Bn, driven by the need to unify customer interactions, enable real-time personalization, and deploy AI-powered analytics across channels. Services are the fastest-growing segment at a 14.8% CAGR, supported by rising demand for implementation, integration, managed services, and continuous optimization of complex omnichannel ecosystems.

- Leading Deployment: On-premises holds over 45% market share in 2026, valued at more than US$ 4.9 Bn, preferred by enterprises requiring strict data control, regulatory compliance, and deep customization. Cloud-based is the fastest-growing at an 18.2% CAGR, fueled by SaaS adoption, scalability, rapid deployment, lower IT overhead, and continuous feature upgrades.

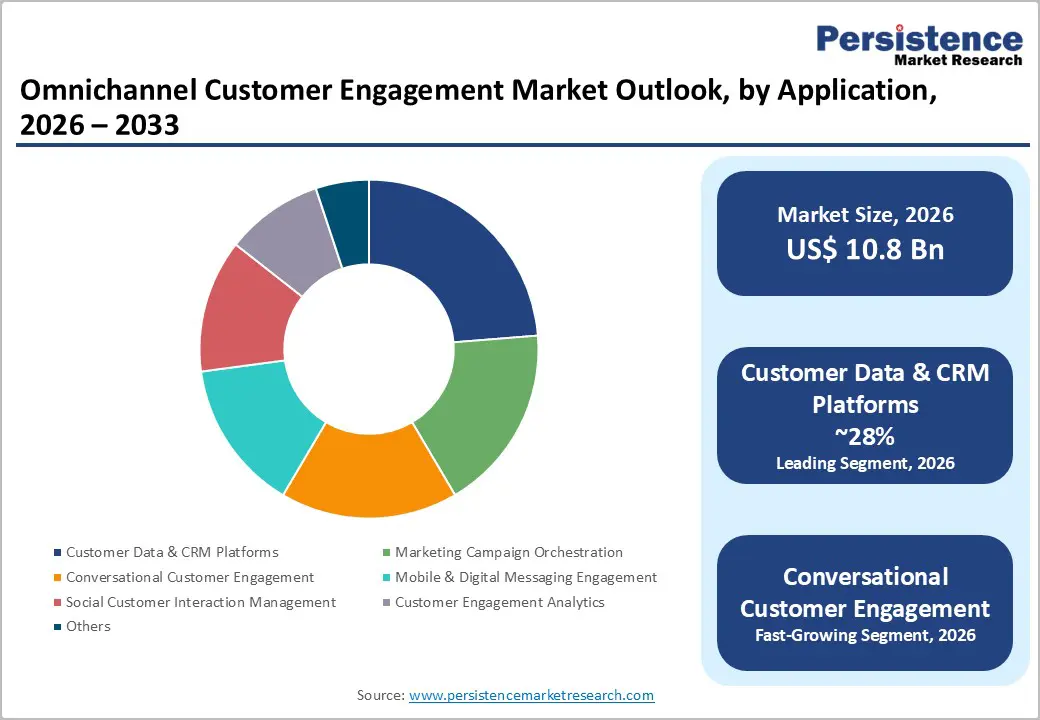

- Leading Application: Customer Data & CRM platforms account for more than 28% share in 2026, exceeding US$3.0Bn, as unified customer profiles form the foundation for personalization, segmentation, and journey orchestration. Conversational customer engagement is the fastest-growing application at a 17.9% CAGR, driven by AI-powered chatbots, messaging platforms, and rising demand for instant, conversational support.

- Leading Industry: Retail & e-commerce command the largest share at over 25% in 2026, valued above US$ 2.7 Bn, due to intense competition, omnichannel commerce requirements, and customer lifetime value optimization. Healthcare is the fastest-growing sector, with a 17% CAGR, driven by telehealth expansion, patient experience transformation, and compliance-driven secure engagement needs.

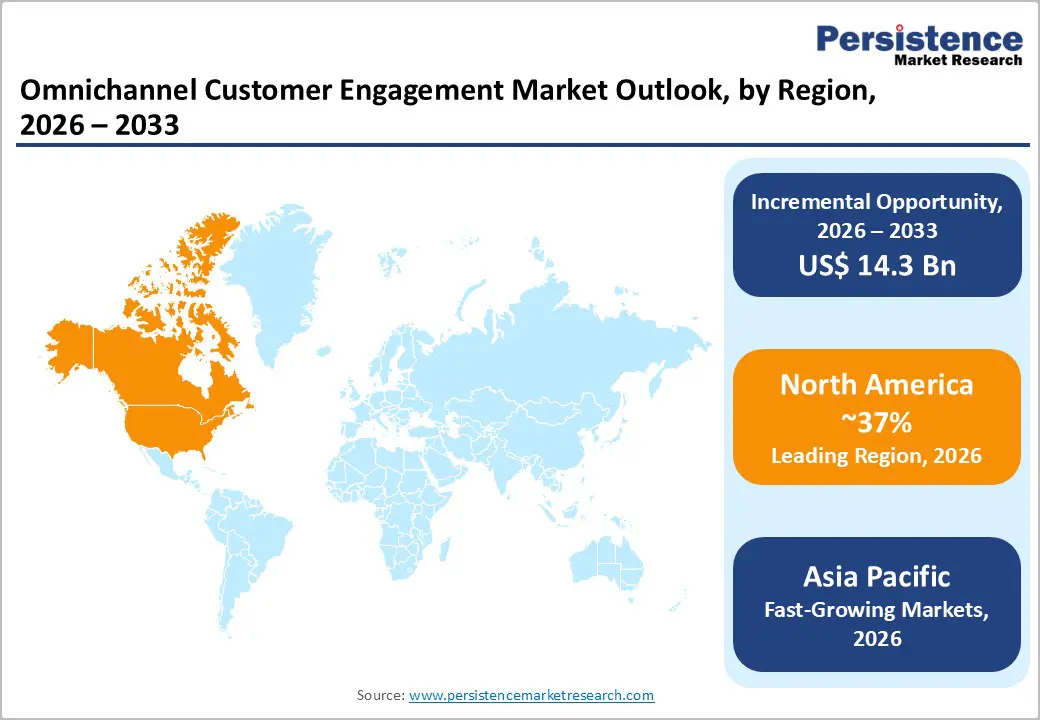

- Leading Region: North America leads with over 37% market share in 2026, valued at around US$ 4.0 Bn, supported by mature digital infrastructure, high AI adoption, and strong enterprise spending. Asia Pacific is the fastest-growing region at a 19.1% CAGR, driven by massive digital populations, e-commerce growth, fintech innovation, and accelerating AI adoption. Europe holds over 23% share, shaped by stringent GDPR compliance and strong demand for data governance-focused platforms.

| Key Insights | Details |

|---|---|

| Omnichannel Customer Engagement Market Size (2026E) | US$10.8 Bn |

| Market Value Forecast (2033F) | US$25.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.1% |

Market Dynamics

Driver - Enterprise AI and Analytics Integration Enabling Predictive Engagement

The integration of enterprise AI and advanced analytics is transforming omnichannel customer engagement by enabling predictive engagement, where businesses anticipate customer needs before interactions occur. By analyzing vast amounts of customer data across channels, AI identifies patterns, preferences, and behavior trends, allowing for highly personalized and timely communications. This predictive capability improves customer satisfaction, increases conversion rates, and strengthens loyalty.

Businesses adopting AI-driven insights optimize campaigns, reduce churn, and deliver seamless experiences across digital, in-store, and mobile touchpoints. The demand for omnichannel engagement solutions that support AI and analytics integration is growing rapidly, driving market expansion. According to Adobe's 2025 AI and Digital Trends in Customer Engagement report, 87% of organizations leveraging AI-driven personalization have already seen a boost in customer engagement.

Accelerating Digital-First Consumer Behaviors and Omnichannel Expectations

Accelerating digital-first consumer behaviors has fundamentally reshaped how customers interact with brands, with a strong preference for online, mobile, and self-service touchpoints. Over 2.77 billion people worldwide will shop online in 2025, representing roughly a third of the global population and underscoring widespread digital adoption in commerce.

Consumers now expect seamless, consistent experiences across channels such as websites, mobile apps, social media, messaging platforms, and physical stores. This shift is driving demand for omnichannel customer engagement solutions that unify customer data and interaction histories in real time. Businesses need these platforms to personalize communication, respond instantly, and maintain context across channels. Rising expectations for convenience, speed, and continuity are pushing enterprises to invest in integrated engagement technologies to improve satisfaction, retention, and lifetime value.

Restraint - Integration Complexity and Legacy System Fragmentation

Enterprises operate with siloed CRM, ERP, contact center, and marketing systems that lack interoperability, making real-time data unification difficult. Legacy infrastructure often lacks support for APIs, cloud-native architectures, or AI-driven analytics, limiting seamless channel orchestration. Customer data remains inconsistent across touchpoints, undermining personalization and journey continuity. These challenges extend integration timelines, require heavy customization, and discourage small and mid-sized enterprises from adopting advanced omnichannel solutions.

Data Privacy Regulations and Consent Management Burden

Data privacy regulations, such as GDPR, CCPA, and emerging national data protection laws, significantly constrain the market by limiting how customer data can be collected, stored, and used across channels. Strict consent management requirements increase operational complexity, as enterprises must track, update, and honor user permissions in real time across multiple touchpoints. Fragmented consent frameworks reduce the ability to unify customer profiles, weakening personalization and journey orchestration. Compliance costs related to legal audits, data governance infrastructure, and penalties for non-compliance further strain budgets. Deployment cycles slow down, and innovation in data-driven engagement capabilities is constrained.

Opportunity

Shift Towards Subscription and Loyalty Models

The shift toward subscription and loyalty-based business models is creating sustained, high-frequency interactions between brands and customers, increasing the need for seamless omnichannel engagement. Subscription models require consistent, personalized communication across apps, email, web, chat, and physical touchpoints to manage renewals, upgrades, and usage insights. Loyalty programs rely heavily on real-time data integration to deliver personalized rewards, offers, and experiences across channels.

Over 90% of people worldwide now belong to at least one loyalty program, indicating massive global adoption of loyalty models. As customers expect unified visibility of points, benefits, and service history, enterprises are investing in omnichannel platforms to centralize customer data. This shift also drives demand for AI-powered engagement tools to predict churn, optimize lifetime value, and enhance long-term customer relationships.

Rise in Real-time Messaging and Chatbots & Demand for Unified Analytics and Reporting

The rapid adoption of real-time messaging channels such as WhatsApp, RCS, web chat, and in-app messaging, along with AI-driven chatbots, is enabling enterprises to deliver instant, always-on customer interactions at scale. This shift is increasing demand for omnichannel platforms that seamlessly manage both automated and human-assisted conversations across multiple channels. Enterprises require unified analytics and reporting to obtain a consolidated view of customer journeys, interaction history, and engagement performance.

By integrating real-time conversational data with centralized analytics, omnichannel customer engagement solutions enable better decision-making, personalization, and experience optimization. These capabilities are creating significant growth opportunities in the omnichannel customer engagement market.

Category-wise Analysis

Offering Insights

Software dominates the global market, capturing more than 65% of the market share in 2026 with a value exceeding US$ 7.0 Bn, as businesses increasingly need advanced platforms to unify customer interactions across channels, personalize experiences, and analyze engagement data in real time. Companies require software solutions to manage growing touchpoints, track customer journeys, and automate marketing and support activities efficiently. These solutions also help meet rising customer expectations for seamless, consistent, and timely communication, which is critical to retention and loyalty.

Services demonstrate the highest growth rate at 14.8% CAGR due to businesses increasingly requiring tailored support to implement, manage, and optimize complex omnichannel strategies. Companies need services to ensure seamless customer experiences across multiple touchpoints. The rising demand for personalization, real-time analytics, and system scalability further drives reliance on expert service providers. Many organizations prefer outsourcing technical and operational tasks to reduce internal resource burden and accelerate deployment.

Deployment Insights

On-premises hold over 45% market share in 2026, with a value exceeding US$ 4.9 Bn, as they give businesses full control over their data, security, and customization. Organizations with complex workflows or strict regulatory requirements prefer on-premises systems to meet compliance needs. They also allow integration with existing IT infrastructure, ensuring a consistent customer experience across channels. On-premises setups support high-performance demands and provide flexibility to tailor features exactly to business requirements. This makes them ideal for enterprises prioritizing reliability and control.

Cloud-based is expected to grow at the highest rate, with a CAGR of 18.2% due to the shift toward managed SaaS platforms, reduced IT infrastructure burden, and improved deployment flexibility. It offers distinct advantages, including automatic security updates, a continuous feature-release cadence, scalability without capital investment, and rapid deployment timelines measured in weeks. The cost-efficiency further drives adoption, especially among SMEs and digitally transforming enterprises.

Application Insights

Customer data & CRM platforms are expected to hold more than 28% in 2026, with a value exceeding US$ 3.0 Bn. These platforms consolidate customer information from disparate sources into unified customer profiles, enabling consistent engagement across channels. Sophisticated data unification and identity resolution capabilities have elevated CDP importance as the essential foundation for personalization, segmentation, and activation. With rising demand for data-driven decisions, real-time engagement, and loyalty management, organizations prioritize CRM solutions to meet these needs efficiently.

Conversational customer engagement is expected to grow at a 17.9% CAGR, driven by AI advancements and customer preference for instant support channels. Chatbots and voice assistants now handle 30-50% of routine customer inquiries across banking, e-commerce, and telecommunications sectors. Conversational platforms integrate with backend systems to enable transactional capabilities, including order placement and account updates through natural language interfaces. Integration with natural language processing and sentiment analysis enhances customer experience quality and interaction effectiveness.

Industry Insights

Retail & e-commerce command the largest market share at over 25% in 2026 with a value exceeding US$ 2.7 Bn. Intense competition, high customer acquisition costs, and the importance of optimizing customer lifetime value drive substantial investments in omnichannel platforms. Omnichannel capabilities enable seamless integration of online and physical store experiences, creating competitive differentiation in commoditized retail sectors. Retailers use platforms to gain real-time inventory visibility, personalized product recommendations, and dynamic promotional optimization. Growing consumer demand for convenience and faster response times reinforces the reliance on omnichannel solutions.

Healthcare is expected to grow at a CAGR of 17%, driven by patient experience improvement imperatives and telehealth integration requirements. Healthcare omnichannel solutions enable appointment scheduling, patient communication, health outcome tracking, and integrated care coordination across primary and specialty care providers. HIPAA-compliant secure messaging and audit-trail capabilities justify substantial investments by large healthcare organizations in specialized omnichannel solutions. Regulatory compliance benefits, combined with improvements in patient experience, drive strong adoption momentum.

Regional Insights

North America Omnichannel Customer Engagement Market Trends

North America accounts for over 37% of the market in 2026, reaching US$4.0 Bn, led by the U.S., which accounts for more than 70% of regional revenue. Market leadership is supported by mature digital infrastructure, high enterprise technology spending, and sophisticated customer engagement practices. Regulatory frameworks such as CCPA, GDPR applicability, and state-specific privacy laws drive demand for advanced compliance and consent management solutions.

The region’s innovation ecosystem, spanning Silicon Valley tech centers, venture-backed platforms, and established enterprise software vendors, fuels continuous capability advancement, while intense competition, venture capital investment, and M&A activity encourage consolidation and “best-of-suite” strategies. North America also leads global AI marketing, accounting for over 32% of revenue, supported by record U.S. data center construction of $40 billion in 2025 to meet AI and digital workload demands for advanced omnichannel platforms.

Asia Pacific Omnichannel Customer Engagement Market Trends

Asia-Pacific is expected to grow at the fastest pace, with a 19.1% CAGR, driven by rapid digital infrastructure development and e-commerce expansion. China leads with a massive e-commerce market, advanced fintech adoption, and strong local platform vendors, while India offers greenfield opportunities with its rising digital population, smartphone adoption, and UPI-driven payments, ~49% of global real-time transactions. Japan’s mature digital ecosystem and high e-commerce penetration demand sophisticated omnichannel solutions, whereas ASEAN markets such as Indonesia, Vietnam, Thailand, and the Philippines are emerging markets with growing middle-class populations.

Regional payment integration, compliance, and platform adaptation, supported by tech adoption, over 80% of Chinese decision-makers used Generative AI by mid-2024 to enhance digital transactions and customer engagement.

Europe Omnichannel Customer Engagement Market Trends

Europe is expected to hold more than 23% share by 2026, with Germany alone contributing more than 22%, followed by the UK, France, and Spain. The region’s stringent GDPR compliance, data residency mandates, and high privacy expectations drive demand for platforms with robust data governance, leading to premium valuations. Germany’s manufacturing and automotive sectors, supported by Industry 4.0 initiatives, and the UK’s financial services sector continue to drive omnichannel investments, while France and Spain show growing adoption of digital transformation.

European markets favor local vendors or global providers with European data centers and compliance certifications, with regional system integrators leveraging established relationships. With 94% of Europeans using the internet in the last three months in 2025, the digital-ready population forms a strong addressable base for omnichannel engagement.

Competitive Landscape

The omnichannel customer engagement market exhibits moderate consolidation. Leading vendors maintain strong competitive positions through comprehensive platform functionality, established customer relationships, ecosystem partnerships, and significant R&D investments. Mid-tier vendors maintain specialized positions through vertical expertise and innovative capabilities. The market exhibits high switching costs for integrated platforms consolidating multiple functions, creating network effects that favor established market leaders.

Key Developments:

- In April 2025, Google announced the next generation of its Customer Engagement Suite, introducing AI-powered enhancements across Conversational Agents, Cloud CCaaS, Agent Assist, and Conversational Insights. Key updates to Conversational Agents include 30 lifelike voice models, a unified no-code console for building hybrid AI agents, prebuilt task-specific agents, and expanded connectors for seamless automation of business processes.

- In May 2024, Salesforce enhanced its Service Cloud Digital Engagement, enabling contact centers to unify customer conversations across channels like WhatsApp, Instagram, TikTok, and more, all through the Einstein 1 Platform. Agents can now access complete customer profiles, respond on-the-go via mobile, and deliver seamless, personalized experiences while all data is harmonized in Salesforce Data Cloud.

Companies Covered in Omnichannel Customer Engagement Market

- Salesforce, Inc.

- Microsoft Corporation

- Oracle Corporation

- Adobe Inc.

- SAP SE

- Genesys Telecommunications Laboratories, Inc.

- IBM

- Zendesk, Inc.

- ServiceNow, Inc.

- Freshworks Inc.

- HubSpot, Inc.

- Zoho Corporation Pvt. Ltd.

- Others

Frequently Asked Questions

The global omnichannel deployment customer engagement market is projected to be valued at US$10.8 Bn in 2026.

The need for seamless, personalized, and consistent customer experiences across multiple channels, enabling businesses to enhance loyalty, satisfaction, and sales, is a key driver of the market.

The omnichannel customer engagement market is expected to witness a CAGR of 12.8% from 2026 to 2033.

Leveraging AI-driven personalization, advanced analytics, and integrated platforms to optimize customer interactions, boost engagement, and unlock new revenue streams is creating strong growth opportunities.

Salesforce, Inc., Microsoft Corporation, Oracle Corporation, Adobe Inc., SAP SE, and IBM are among the leading key players.