- Healthcare Services

- Office-Based Lab Market

Office-Based Lab Market Size, Share, and Growth Forecast 2026 - 2033

Office-Based Lab Market by Set-up Model (Single Specialty, Multi-specialty, Hybrid), by Service (Peripheral Vascular Intervention, Interventional Radiology, Endovascular Therapy, Cardiovascular, Venous, Non-vascular), by Specialist (Vascular Surgeons, Interventional Cardiologists, Interventional Radiologists, Others), by End User (Physician offices, Clinics, Research institutions, Others), by Regional Analysis, 2026-2033

Office-Based Lab Market Size and Trend Analysis

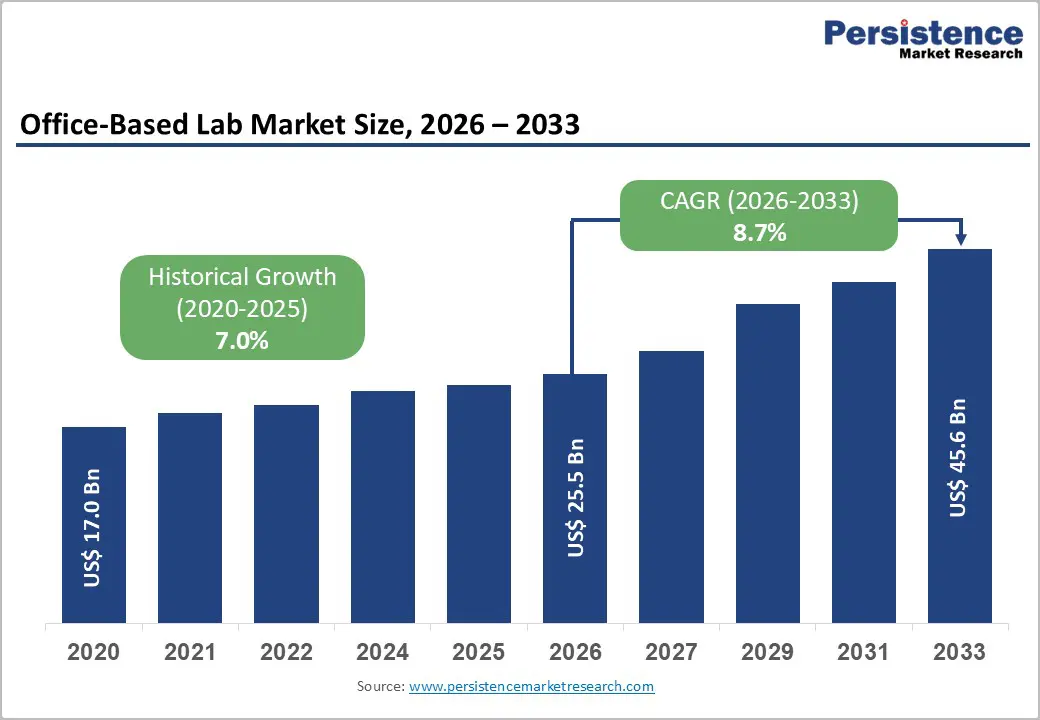

The global office-based lab market size is expected to be valued at US$ 25.5 billion in 2026 and projected to reach US$ 45.6 billion by 2033, growing at a CAGR of 8.7% between 2026 and 2033.

The office-based lab market is experiencing robust growth driven by the convergence of healthcare spending pressures and demographic shifts. Rising prevalence of chronic diseases, combined with an aging global population, has intensified demand for accessible diagnostic and interventional services. According to the Centers for Medicare & Medicaid Services (CMS), per capita personal health care spending for individuals aged 65 and older was $22,356 in 2020, representing more than 5 times higher spending compared to children. This demographic imperative, coupled with healthcare systems seeking cost-efficient service delivery models, positions office-based labs as strategically valuable infrastructure for meeting population health needs outside traditional hospital settings.

Key Market Highlights

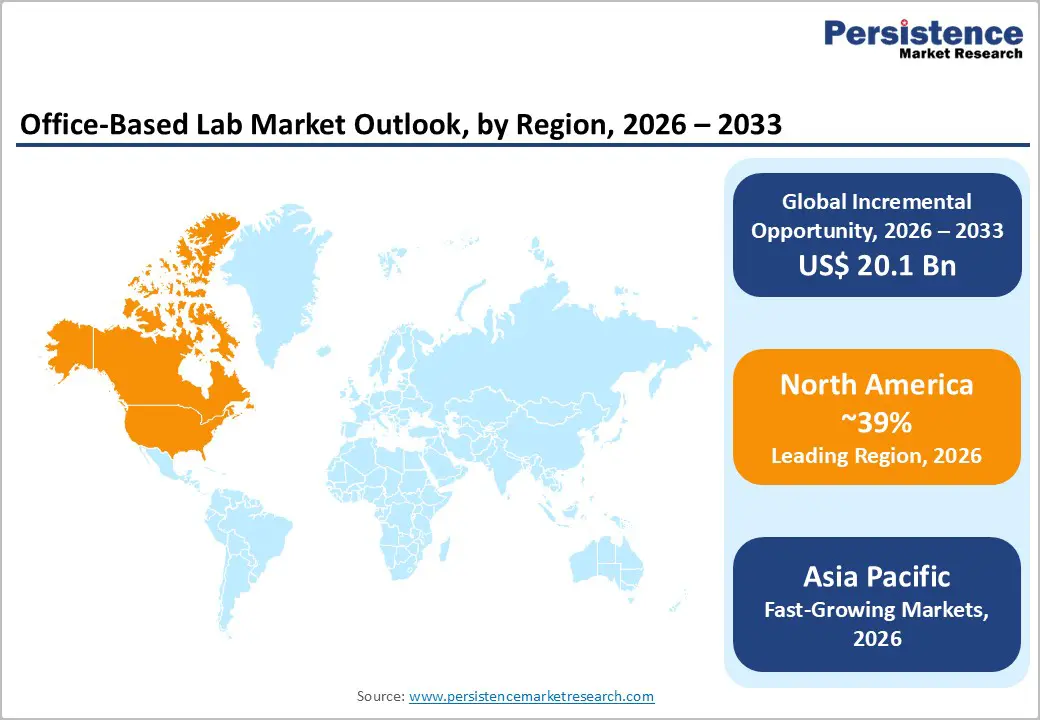

- North America Dominance: North America holds 39% market share in 2025, supported by high cardiovascular disease prevalence, advanced healthcare infrastructure, and strong regulatory support for office-based labs.

- Fastest Growing Region: Asia Pacific is the fastest-growing market due to large patient populations, rising cardiovascular disease burden, healthcare decentralization, and cost advantages.

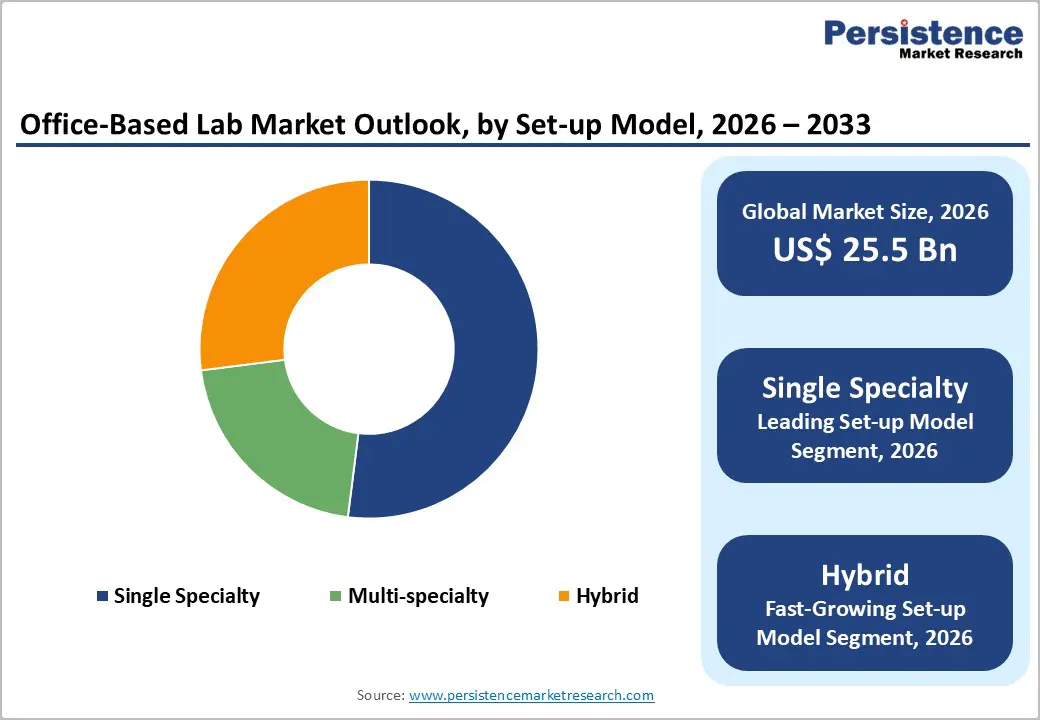

- Dominant Segment: Single-specialty setups account for 52% market share in 2025, driven by operational efficiency, focused expertise, and strong financial sustainability.

- Fastest Growing Segment: Hybrid setup models show the fastest growth through 2032, benefiting from flexible operations, higher facility utilization, and expanded reimbursement options.

- Key Opportunity: Growth in point-of-care testing and decentralized diagnostics is driven by regulatory support, telemedicine integration, and patient demand for convenient care.

| Global Market Attributes | Key Insights |

|---|---|

| Office-Based Lab Market Size (2026E) | US$ 25.5 billion |

| Market Value Forecast (2033F) | US$ 45.6 billion |

| Projected Growth CAGR (2026-2033) | 8.7% |

| Historical Market Growth (2020-2025) | 7.0% |

Market Dynamics

Market Growth Drivers

Increasing Prevalence of Cardiovascular and Vascular Diseases

Cardiovascular and peripheral vascular diseases represent a significant and growing disease burden globally, directly accelerating demand for office-based lab facilities. According to medical literature, cardiovascular diseases contribute to approximately 30.3% of mortality among aging populations worldwide, with peripheral arterial disease (PAD) affecting approximately 7% of the adult population in developed nations. Aging demographics, sedentary lifestyles, and rising obesity rates amplify this disease prevalence. The shift toward minimally invasive interventional approaches, including peripheral vascular interventions, endovascular therapy, and cardiovascular interventions, has made office-based settings increasingly viable for specialty-focused practices. Vascular surgeons and interventional cardiologists increasingly prefer dedicated office-based facilities where they can maintain specialized expertise, optimize resource utilization, and deliver timely patient care. This concentration of disease burden and treatment modality specialization creates sustained market expansion opportunities.

Rising Healthcare Expenditures and Investment in Diagnostic Infrastructure

Global healthcare spending continues to accelerate, with governments and private healthcare systems prioritizing infrastructure investments in decentralized diagnostic and interventional capabilities. This investment trend reflects recognition that office-based models reduce overall healthcare system costs through faster patient throughput, lower overhead compared to hospital settings, and reduced dependence on hospital beds and emergency departments. The shift toward value-based care models and quality payment programs incentivizes healthcare providers to establish efficient, patient-centric service delivery mechanisms. Physician offices, clinics, and research institutions are receiving increased reimbursement support and regulatory encouragement to establish office-based testing infrastructure. Healthcare spending growth, particularly in North America and the Asia Pacific regions, provides capital for facility development and technology adoption, driving market expansion across both established and emerging economies.

Market Restraints

High Capital Investment and Equipment Maintenance Costs

Establishing and maintaining office-based lab facilities requires substantial upfront capital expenditure for specialized equipment, regulatory compliance infrastructure, and trained personnel. Single-specialty and hybrid labs necessitate advanced diagnostic and interventional equipment including imaging systems, analyzers, and interventional devices with significant acquisition and maintenance costs. Small and independent practices often lack financial capacity to absorb these costs, limiting market participation to well-capitalized healthcare organizations. Furthermore, ongoing compliance with Clinical Laboratory Improvement Amendments (CLIA) regulations and quality assurance requirements impose recurring operational expenses that constrain profitability, particularly for lower-volume facilities. Price competition from large hospital-based and reference laboratories, which benefit from economies of scale and purchasing power, further pressures margins, making independent office-based labs economically challenging to sustain.

Regulatory Complexity and Compliance Burden

Office-based labs operate under stringent federal regulatory frameworks administered by the Food and Drug Administration (FDA), Centers for Medicare & Medicaid Services (CMS), and Centers for Disease Control and Prevention (CDC). All laboratory testing performed in office settings requires appropriate CLIA certification, with different certificate types including Certificate of Waiver (CoW), Certificate of Registration (COR), and Certificate of Compliance (COC) depending on test complexity levels. Non-compliance with regulatory standards results in significant penalties, suspension of reimbursement, or laboratory closure, creating substantial operational risk. The complexity of regulatory requirements, combined with continuous updates to waived test lists and quality standards, requires dedicated compliance management resources. These regulatory barriers disproportionately affect smaller practices and emerging market entrants, limiting market expansion and consolidating opportunities among larger, better-resourced healthcare organizations.

Market Opportunities

Expansion of Point-of-Care Testing and Decentralized Diagnostics

Point-of-care testing (POCT) and decentralized diagnostic solutions represent a rapidly expanding market opportunity as healthcare systems prioritize convenient, accessible testing modalities. The COVID-19 pandemic accelerated adoption of POCT technologies significantly, demonstrating the clinical and operational value of rapid, on-site diagnostic capabilities. Expansion of POCT beyond respiratory illnesses to include sexually transmitted infections, antimicrobial resistance testing, and autoimmune disease diagnostics is creating new service lines for office-based labs. Interventional radiologists and specialty practitioners increasingly integrate POCT capabilities into clinical workflows to enable immediate clinical decision-making without external laboratory dependencies. Regulatory agencies have expanded CLIA waived test categories from approximately 8 tests in 1992 to over 40 tests currently, creating opportunities for independent practices to establish minimal-complexity lab services. Investment in advanced POCT technologies and integration with telemedicine platforms positions office-based labs to capture growing demand for decentralized, patient-centered diagnostic services, particularly in underserved geographic regions.

Medical Tourism and Healthcare Access Expansion in Emerging Markets

Emerging economies in Asia Pacific, Latin America, and Middle East & Africa regions are experiencing accelerated healthcare infrastructure development driven by rising medical tourism, increasing healthcare spending, and government initiatives to expand diagnostic access. China, India, and Southeast Asian nations are actively establishing office-based interventional facilities to reduce pressure on hospital capacity and improve healthcare accessibility in primary care settings. According to healthcare investment data, emerging markets offer significantly lower capital and operational costs compared to developed nations, enabling rapid facility expansion with lower financial barriers. Government healthcare reform initiatives in major emerging markets prioritize decentralized testing infrastructure and localized diagnostic services as pathways to achieving universal health coverage targets. The combination of large patient populations, rising incidence of chronic diseases, growing medical tourism sectors, and supportive regulatory environments creates substantial opportunities for market expansion. Companies establishing manufacturing, research and development, or service delivery operations in these regions can capitalize on cost advantages while serving rapidly growing patient populations, driving significant market growth in Asia Pacific and other emerging regions through 2033.

Category-wise Insights

Set-up Model Analysis

The single specialty setup model dominates the office-based lab market with 52% market share in 2025, establishing itself as the leading segment through specialized service delivery and operational focus. Single-specialty labs concentrate resources and expertise on specific medical disciplines including cardiology-focused interventional centers, vascular surgery-dedicated facilities, and endovascular intervention suites. This specialization model enables practitioners to achieve superior clinical proficiency through high patient volume concentration, deploy highly specialized equipment optimized for narrow therapeutic areas, and develop deep expertise that multi-specialty competitors cannot easily replicate. For example, cardiology-focused labs maintain sophisticated cardiac imaging technologies and dedicated teams of interventional cardiologists, enabling superior outcomes for cardiovascular conditions. The laser focus on single specialties, combined with investment-efficient operations targeting narrow patient populations, generates superior financial returns and clinical outcomes compared to broader facilities. However, the hybrid setup model emerges as the fastest-growing segment, operating as office-based facilities during certain weeks and ambulatory surgery centers (ASCs) during other periods, thereby maximizing facility utilization, expanding reimbursement opportunities, and increasing procedural volume through flexible operational models.

Service Type Analysis

The peripheral vascular intervention service represents the leading service category within office-based labs, driven by rising prevalence of peripheral arterial disease and increased clinical adoption of minimally invasive vascular interventions. Peripheral vascular diseases affect significant patient populations, with peripheral arterial disease (PAD) prevalence reaching 7% in developed nations and increasing substantially in aging populations. The clinical demand for procedures addressing blocked peripheral arteries, reduced blood flow, and tissue damage prevention creates consistent procedural volume for office-based vascular intervention facilities. Interventional radiologists and vascular surgeons increasingly perform peripheral vascular interventions, endovascular therapy, and venous interventions in office settings, capitalizing on specialized equipment availability and streamlined surgical workflows. The market for cardiovascular interventions, including coronary stenting, angioplasty, and acute coronary syndrome management, continues expanding as aging populations and rising cardiovascular disease prevalence increase procedural demand. Non-vascular services including gastroenterology, ophthalmology, and urology interventions represent emerging service expansion opportunities as office-based models prove economically viable and clinically effective across diverse specialty disciplines.

End User Analysis

Physician offices represent the dominant end-user category for office-based labs, reflecting the fundamental business model architecture of dedicated medical practices operating specialized diagnostic and interventional services. Independent physician offices and group practices increasingly establish office-based labs as strategic revenue generators and competitive differentiation mechanisms, providing convenient in-house testing that enhances patient satisfaction and practice profitability. Clinics serving diverse patient populations establish office-based labs to improve patient access, reduce external laboratory dependencies, and generate additional revenue through test billing. Research institutions utilize office-based lab infrastructure for clinical research, diagnostic validation, and translational medicine studies. The preference for office-based service delivery among physician offices reflects operational advantages including immediate test result access, streamlined clinical decision-making, and enhanced patient experience through integrated care delivery in single locations. As healthcare reimbursement increasingly emphasizes outcomes and patient satisfaction metrics, physician offices and clinics expand office-based lab offerings to demonstrate value-based care delivery capabilities and maintain competitive positioning in value-based payment models.

Regional Insights

North America Office-Based Lab Market Trends and Insights

North America establishes itself as the dominant regional market with 39% market share in 2025, driven by the highest prevalence of cardiovascular and chronic diseases requiring office-based interventional services. The United States healthcare system's emphasis on minimally invasive procedures, combined with advanced technological infrastructure and favorable reimbursement policies, creates optimal conditions for office-based lab proliferation. According to Centers for Medicare & Medicaid Services (CMS) data, healthcare spending patterns in the region reflect substantial allocation toward cardiovascular disease management, incentivizing providers to establish specialized office-based intervention facilities. The presence of major medical device manufacturers headquartered in North America including Edwards Lifesciences, Medtronic, Abbott, and Philips ensures readily available access to cutting-edge equipment and continuous innovation in interventional technologies.

The regulatory environment in North America actively supports office-based lab development through reimbursement policies and regulatory clarifications facilitating localized testing. Multiple U.S. states have implemented policies promoting reimbursable at-home sample collection and local lab testing, effectively reducing patient access barriers in rural and underserved areas.

Asia Pacific Office-Based Lab Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market, representing the highest-potential expansion opportunity driven by massive patient populations, rising healthcare spending, and government initiatives prioritizing decentralized diagnostic infrastructure. China, India, and Japan demonstrate accelerating healthcare system modernization, with increasing prevalence of cardiovascular diseases, diabetes, and chronic conditions driving demand for accessible interventional services. According to healthcare data, India experiences an estimated 28.13% of mortality attributed to cardiovascular diseases, establishing enormous clinical need for interventional capacity expansion. The region's large patient populations remain significantly underserved regarding advanced diagnostic and interventional services, creating substantial capacity-building opportunities for office-based lab development.

Government healthcare policy initiatives in China and India actively promote localized testing infrastructure and decentralized diagnostic services as mechanisms to reduce pressure on overburdened hospital systems and expand healthcare accessibility. Medical tourism industries in Thailand, India, and Southeast Asian nations attract international patients seeking cost-effective, quality interventional procedures, driving investment in advanced office-based facilities. Manufacturing cost advantages in Asia Pacific enable substantial healthcare equipment and technology production, reducing capital expenses for facility development compared to Western regions. The rapid expansion of multispecialty hospital networks in China, India, and Japan increasingly incorporates office-based intervention units as differentiation mechanisms and revenue generators. Growing medical tourism coupled with rising healthcare spending creates financial capacity for infrastructure investment, positioning Asia Pacific as the primary growth driver for global office-based lab market expansion through 2033, with fastest growth rates exceeding other regional markets.

Competitive Landscape

Market Structure Analysis

The Office-Based Lab (OBL) market is highly competitive, driven by a mix of global medical device manufacturers, diagnostic service providers, and outpatient care specialists. Key players compete on technology innovation, procedural efficiency, and integrated service offerings. Companies focus on expanding geographic reach, enhancing lab automation, and adopting minimally invasive procedure solutions to attract high-volume clinical practices. Strategic partnerships, mergers, and acquisitions are common to consolidate market presence and offer end-to-end solutions.

Key Market Developments

- In June 2023, Royal Philips announced that it had teamed up with BIOTRONIK (Lake Oswego, Oregon, United States), a leading global medical device company offering products and services to improve the lives of patients with cardiovascular and endovascular diseases, to expand the range of cardiovascular devices available for Philips SymphonySuite customers.

Companies Covered in Office-Based Lab Market

- Panasonic Corporation

- Duracell

- Energizer Holdings, Inc.

- GP Batteries International Limited

- Spectrum Brands Holdings, Inc.

- FDK Corporation

- Highpower International, Inc.

- Huanyu Battery Co., Ltd.

- Primearth EV Energy Co., Ltd.

- Ansmann AG.

- Varta AG

- Uniross

- GS Yuasa International Ltd.

- NEXcell Battery Company

- BYD Company Limited

Frequently Asked Questions

The global office-based lab market is expected to be valued at US$ 25.5 billion in 2026, growing from historical levels and demonstrating strong market momentum driven by rising chronic disease prevalence, aging populations, and healthcare system emphasis on decentralized diagnostic and interventional service delivery.

The office-based lab market growth is primarily driven by rising prevalence of cardiovascular and peripheral vascular diseases affecting aging populations globally, with peripheral arterial disease affecting 7% of adult populations in developed nations.

North America dominates the office-based lab market with 39% market share in 2025, driven by highest cardiovascular disease prevalence, advanced healthcare infrastructure, strong regulatory support for office-based operations, favorable reimbursement policies, and concentration of major medical device manufacturers.

Point-of-care testing expansion and decentralized diagnostic integration represent primary market opportunities, driven by FDA expansion of CLIA-waived test categories, pandemic-accelerated POCT adoption, integration with telemedicine platforms, and patient demand for convenient testing services.

Major market players include Medtronic, Edwards Lifesciences, Abbott Laboratories, Philips Healthcare, Siemens Healthineers, General Electric Healthcare, Canon Medical Systems, and Carestream Health.