- Healthcare Services

- Occupational Medicine Market

Occupational Medicine Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Occupational Medicine Market by Application (Workplace Health Surveillance, Substance Abuse Testing, Occupational Health Management, Health & Safety Compliance), Workforce Type (Industrial Workers, Healthcare Workers, Office Workers), End-User (Corporate Sector, Healthcare Sector, Government Sector), and Regional Analysis for 2026-2033

Occupational Medicine Market Share and Trends Analysis

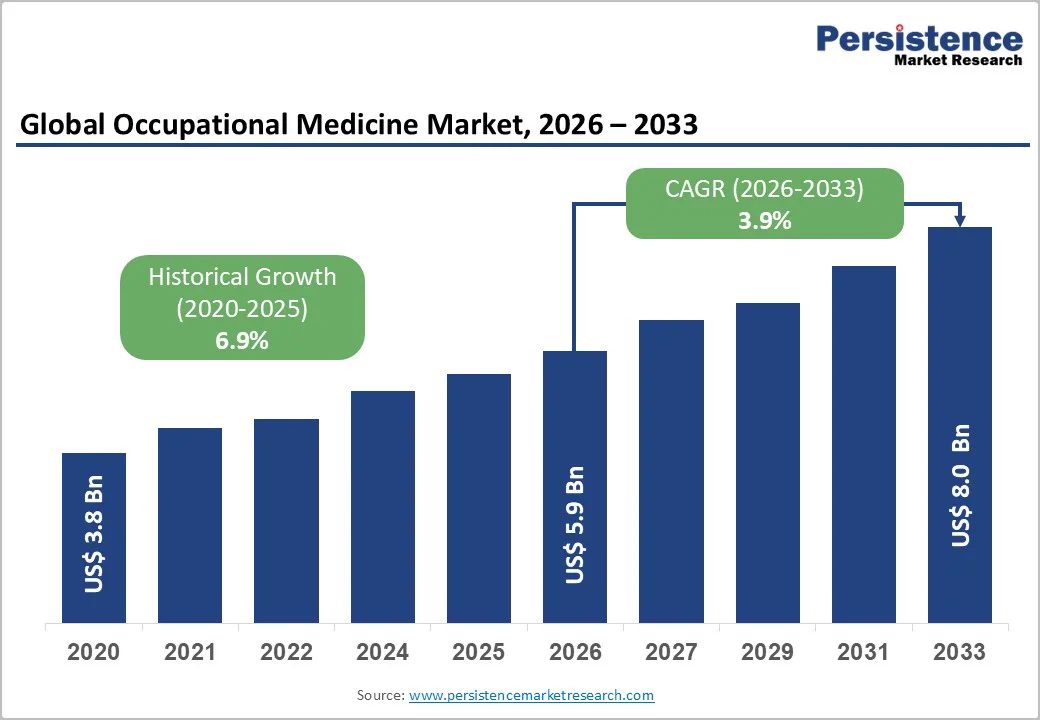

The global occupational medicine market size is likely to be valued at US$ 5.9 billion in 2026 and is estimated to reach US$ 8.0 billion by 2033, growing at a CAGR of 3.9% during the forecast period 2026−2033. Rising regulatory focus on workplace safety across developed and emerging economies has compelled organizations to adopt more comprehensive health and safety protocols, including mandatory health screenings, workplace assessments, and compliance documentation. The increasing burden of occupational diseases, ranging from musculoskeletal disorders and respiratory conditions to mental health challenges, has elevated employer awareness of the long-term costs associated with inadequate preventive care. In response, businesses are demanding integrated health services that not only meet compliance requirements but also actively reduce absenteeism, lower insurance premiums, and enhance overall workforce productivity through early intervention and wellness programs.

Key Industry Highlights

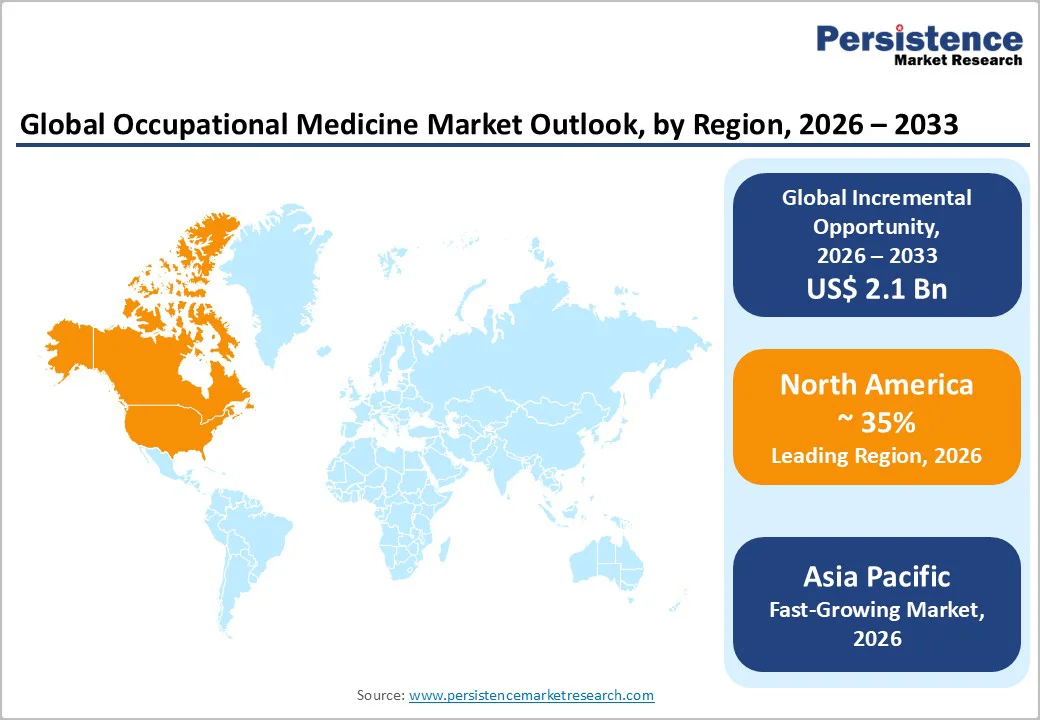

- Dominant Region: North America is expected to command about 35% market share in 2026, owing to strict workplace regulations and widespread awareness about employee rights.

- Fastest-growing Regional Market: Asia Pacific is likely to be the fastest-growing regional market through 2033, as a result of the high rate of economic industrialization and urbanization.

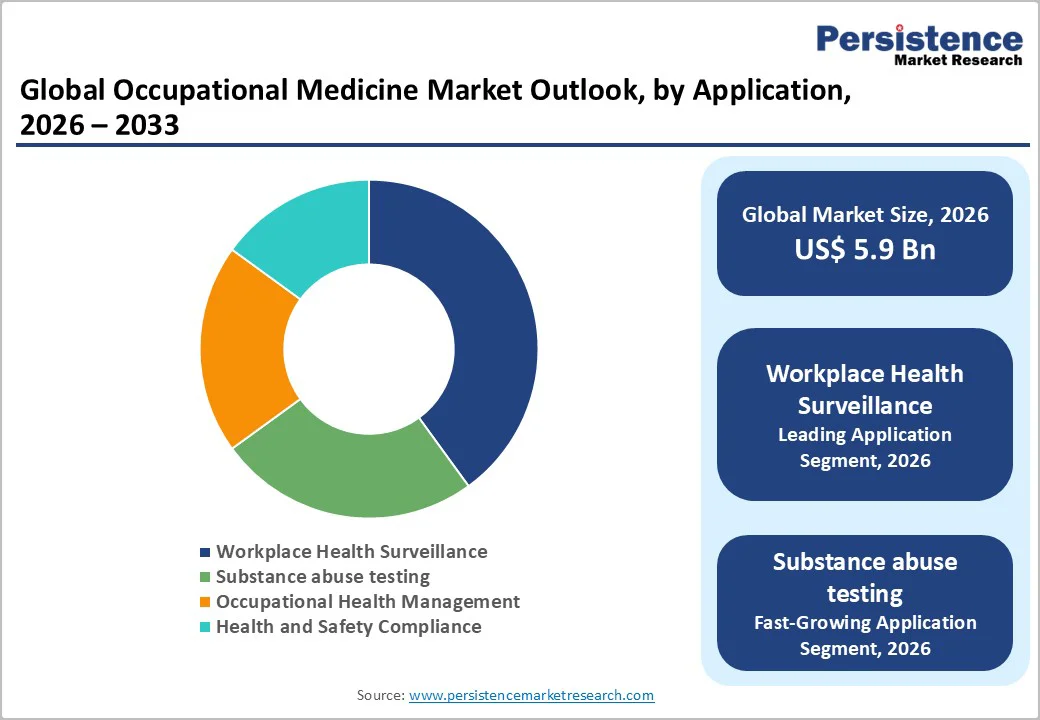

- Leading & Fastest-growing Product Types: Workplace health surveillance is set to dominate with approximately 40% revenue share in 2026, with substance abuse testing growing the fastest from 2026 to 2033.

- Dominant & Fastest-growing Workforce Types: The industrial worker segment is slated to lead with an estimated 45% share in 2026, while the healthcare workers segment is expected to be the fastest-growing between 2026 and 2032.

- Market Drivers: Work-related injuries and diseases are rising across sectors, undermining worker health and organizational productivity and fueling the market.

- Market Opportunities: Employers are prioritizing mental health at work, embedding support for stress, anxiety, and burnout into policies, benefits, leadership practices, and everyday culture.

| Key Insights | Details |

|---|---|

| Occupational Medicine Market Size (2026E) | US$ 5.9 Bn |

| Market Value Forecast (2033F) | US$ 8.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.9% |

| Historical Market Growth (CAGR 2020 to 2024) | 6.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Burden of Work Related Injuries and Diseases

Workplaces across diverse industries expose employees to a range of hazards such as physical strain, chemical exposure, noise, infectious agents, and chronic stress. Prolonged exposure to these risks can lead to gradual health deterioration, resulting in long-term illnesses or injuries that impair both work capacity and overall quality of life. When a significant number of workers are affected, businesses and entire economies experience consequences such as decreased productivity, increased absenteeism, and higher expenses related to healthcare and compensation. In response, governments are strengthening workplace safety regulations and shifting expectations for employers. Authorities now require organizations to proactively prevent harm rather than simply respond after incidents occur. This regulatory change is driving companies to implement preventive occupational medicine programs, including structured medical assessments, pre-employment screening, and regular monitoring for early signs of health issues such as respiratory conditions, musculoskeletal disorders, or hearing loss.

These proactive health measures help maintain workforce well-being, minimize operational disruptions, and demonstrate compliance with regulatory standards. For providers of occupational medicine services, this trend creates steady and predictable demand for clinic visits, onsite medical teams, and coordinated follow-up care. The need is especially pronounced in higher-risk environments such as manufacturing plants, construction sites, mines, hospitals, and transport and logistics operations, where daily tasks often involve significant physical or environmental challenges. By adopting preventive strategies, organizations not only safeguard employee health but also reduce long-term costs and ensure smoother business continuity, making occupational health a strategic priority for both employers and service providers.

Limited Awareness among Small and Medium Enterprises

Small and medium enterprises (SMEs) often prioritize daily operations and financial survival over comprehensive occupational health initiatives. These businesses typically lack dedicated budgets or in-house experts to develop formal safety programs, leading them to depend on temporary fixes or basic compliance measures. Managers frequently overlook the value of systematic health support, which could lower injury rates, boost employee satisfaction, and safeguard long-term viability. Research confirms that SMEs face higher occupational risks due to limited resources and awareness compared to larger firms.

Large corporations possess the capacity to establish robust health frameworks, employ specialists, and partner with external occupational medicine providers. This disparity results in mature services among big organizations but sparse coverage in the SME sector, restricting broader market penetration. The shortage of trained occupational health professionals further constrains availability across both segments. Providers can address this gap by offering affordable, scalable solutions such as shared clinics, digital tools, and simplified compliance packages tailored to SME constraints.

Increasing Emphasis on Mental Health in the Workplace

Organizations are increasingly recognizing the profound impact of work on mental well-being, acknowledging that stress, anxiety, and depression significantly impair both individual quality of life and business performance. To address these challenges, employers are integrating mental health support into occupational medicine programs by incorporating services such as counseling, resilience training, and structured return-to-work protocols for employees recovering from mental health conditions. This shift enables occupational medicine to evolve from a traditional focus on physical safety toward a comprehensive, holistic approach that safeguards both physical and psychological health.

Simultaneously, rapid industrialization in developing economies is driving the construction of factories, logistics hubs, and large-scale infrastructure projects. As these sectors expand, governments and international partners are placing greater emphasis on improving safety standards and establishing formal health protections. This regulatory and economic environment creates significant opportunities for occupational health providers to enter emerging markets with tailored solutions, ranging from essential health screenings and safety training to sophisticated, integrated wellness programs designed to meet local requirements.

Category-wise Analysis

Application Insights

Workplace health surveillance is likely to emerge as the leading application, commanding approximately 40% of the occupational medicine market revenue share in 2026. This dominance reflects the fundamental role that surveillance plays in both regulatory compliance and operational risk management for employers across sectors. Standard activities such as baseline and periodic medical evaluations, fitness-for-duty assessments, and targeted monitoring for specific occupational exposures such as chemical hazards, noise levels, and repetitive physical movements form the foundation of these programs. Because regulatory authorities and safety standards mandate these practices across numerous industries, and because non-compliance carries substantial financial and reputational penalties, employers maintain minimal discretion to reduce or defer these services.

Substance abuse testing is positioned as the fastest-growing segment through 2033, driven by converging pressures that are compelling employers to broaden scope and strengthen protocols. Safety-sensitive industries such as transportation, logistics, energy, and heavy manufacturing recognize elevated risk when impairment goes undetected, prompting expansion of testing panels, formalization of random testing schedules, and standardization of post-incident screening procedures. Evolving cannabis legislation and persistent opioid-related concerns are reshaping employer policies and driving adoption of advanced detection methods that identify recent consumption rather than historical use.

Workforce Type Insights

Industrial workers are projected to account for an estimated 45% of market revenue in 2026, reflecting the intense physical, chemical, and mechanical risks present in sectors such as manufacturing, mining, energy, heavy engineering, and large-scale logistics. These environments fall under strict safety regulations that require frequent pre-placement examinations, scheduled medical surveillance, and early intervention for strains, exposures, and trauma, far beyond what most office-based roles demand. In practice, large industrial employers often contract dedicated occupational health partners or establish on-site clinics, which creates stable, high-volume caseloads and long-term service contracts that underpin much of the market’s revenue base.

Healthcare workers are expected to form the fastest-growing workforce segment between 2026 and 2033, as hospitals and clinics sharpen their focus on staff protection. Daily exposure to infectious agents, needle-stick injuries, shift-related fatigue, heavy manual handling, and emotionally intense situations has led leadership teams to treat workforce safety and well-being as a core operational risk rather than a discretionary benefit. Experience during the pandemic exposed critical weaknesses in infection control, staffing resilience, and mental health support, prompting health systems to expand occupational medicine programs that combine vaccination and screening with ergonomic redesign, fatigue management, and psychosocial care pathways.

End-User Insights

The corporate sector currently leads the occupational health services market revenues, commanding approximately 55% of the total segmental share in 2026. Large enterprises manage complex operations across industries such as manufacturing, energy, logistics, technology, and services, often spanning multiple sites and countries. This complexity attracts regulatory scrutiny, creates reputational risk, and exposes organizations to meaningful financial liability if worker health issues are mishandled. In response, these corporations formalize their health and safety approach by creating policies, allocating budgets, and either contracting specialist occupational medicine providers or combining in-house teams with external partners.

The healthcare sector is anticipated to be the fastest-growing segment during the 2026-2033 forecast period, as workers in this sector are constantly exposed to multiple, escalating risks. Hospitals, clinics, and diagnostic centers must protect staff from infectious diseases, needle-stick injuries, aggressive or complex clinical workloads, and chronic physical strain. Post pandemic, leadership teams and regulators became much more sensitive to these vulnerabilities. That shift pushed organizations to move beyond basic compliance and invest in structured, well-resourced occupational health programs specifically for healthcare workers.

Regional Insights

North America Occupational Medicine Market Trends

North America is positioned to command approximately 35% of the occupational medicine market share in 2026, underpinned by rigorous regulatory frameworks, elevated employer awareness, and substantial purchasing capacity. Occupational Safety and Health Administration (OSHA) regulations at the federal level, combined with state-specific mandates, require organizations to implement comprehensive medical surveillance programs, drug and alcohol testing protocols, and formalized return-to-work procedures following injury or illness. Employers across the region demonstrate heightened sensitivity to legal liability, financial exposure, and reputational consequences associated with inadequate workplace health management. This awareness drives sustained investment in structured occupational health systems rather than reliance on reactive or informal arrangements, creating predictable demand for specialized providers who can deliver compliance assurance alongside measurable health outcomes.

The regional market also benefits from a mature healthcare and technology infrastructure that accelerates innovation and service delivery. Employers and occupational health providers in North America are early adopters of tele-occupational medicine platforms, integrated electronic health record (EHR) systems that link occupational and clinical data, and advanced analytics tools for risk prediction and intervention prioritization. These capabilities enable efficient scaling of programs across large, geographically dispersed workforces while generating evidence-based metrics such as injury reduction rates, faster return-to-work timelines, and improved employee engagement scores. Ongoing market consolidation, expansion of on-site employer clinics, and strategic technology partnerships maintain competitive intensity and operational sophistication.

Europe Occupational Medicine Market Trends

Europe stands out as a leading regional market for occupational medicine as worker protection is embedded in the legislations of the European Union (EU), social systems, and corporate practices. Most European countries require employers to take explicit responsibility for identifying health risks, monitoring employee well-being, and preventing harm, so occupational health becomes a core element of how both private and public organizations operate. Regulatory frameworks in countries such as Germany, the United Kingdom, and France set clear expectations for health surveillance, risk assessment, and follow-up interventions, which creates continuous demand for qualified occupational health services and multidisciplinary teams.

Across the EU, employers and policymakers are increasingly focused on psychosocial risks such as stress, burnout, harassment, and work overload, as well as the needs of an aging workforce and employees living with chronic diseases. This shift is pushing occupational health programs to move beyond basic physical examinations and accident prevention toward integrated models that include mental health support, ergonomic design, and long-term condition management. Efforts at EU level to align health and safety directives and reporting practices, particularly around psychosocial risks and mental well-being, further encourage more consistent standards and help spread best practices across member states.

Asia Pacific Occupational Medicine Market Trends

Asia Pacific is poised to be the fastest-growing regional occupational medicine market through 2033, as its economies industrialize and urbanize at exceptional speed. Rapid development of factories, infrastructure projects, logistics hubs, and large construction sites across China, India, and members of the ASEAN is placing millions of workers in environments with substantial physical, chemical, and ergonomic risks. As accident rates and work-related illness remain a concern, governments are tightening workplace safety regulations, strengthening enforcement, and embedding occupational health requirements into labor and industry policies. Employers in turn face mounting pressure to move beyond basic first aid or informal practices and to establish formal health programs that include medical surveillance, risk assessments, and structured return-to-work processes.

Multinational corporations (MNCs) are expanding their presence across the region and bringing global safety and health standards into local operations. These organizations expect consistent occupational health policies, audits, and reporting frameworks whether a facility is located in Europe or within ASEAN markets, which raises the baseline expectations for local suppliers and joint ventures. Technology adoption, including telemedicine, remote monitoring, and data-driven risk analytics, also enables occupational health providers to scale services into remote industrial zones and smaller urban sites at lower cost. Together, these factors are allowing Asia Pacific to outpace other regional markets in the growth of occupational health and occupational medicine services.

Competitive Landscape

The global occupational medicine market structure is moderately fragmented, with key players such as Concentra Inc., WorkCare Inc., Occucare International, and HealthWorks Medical LLC collectively holding 40–45% of the global market share. The sector features a wide array of competitors delivering tailored services like health assessments, disease management, regulatory compliance, and industry-specific wellness programs. Ongoing advancements in digital health technologies and a growing emphasis on proactive health strategies are reshaping the market, as providers increasingly leverage data analytics to refine risk management, streamline reporting, and boost the impact of occupational health initiatives. This focus on innovation, coupled with rising demand for integrated, data-driven solutions, positions the occupational medicine sector as a dynamic arena for strategic expansion and continuous service improvement.

Key Industry Developments

- In August 2025, Concentra, a leading U.S. provider of occupational health services, opened a new medical center in Union City, Georgia, expanding its footprint in the Atlanta area to better serve local employers and workers.

- In June 2025, AdventHealth announced the opening of Corporate Care Tampa, a dedicated occupational health clinic on North Dale Mabry Highway, to serve first responders and corporate clients across West Florida.

- In May 2025, Meena Health inaugurated the Meena Occupational Health Center in Riyadh, the city’s first dedicated facility focused solely on occupational health and safety, offering services such as pre-employment exams, periodic checkups, high-risk industry assessments, rehabilitation, and disability evaluations.

Frequently Asked Questions

The global occupational medicine market is projected to reach US$ 5.9 billion in 2026.

Increasingly stricter workplace safety regulations, rising work-related health risks, and employers’ need to reduce absenteeism and liability through structured health programs are driving the market.

The market is poised to witness a CAGR of 3.9% from 2026 to 2033.

Lucrative opportunities can be unlocked in digital and data-driven occupational health solutions, integrated mental health and wellness services, and expansion into fast-industrializing emerging markets.

Concentra Inc., WorkCare Inc., Occucare International, and HealthWorks Medical LLC are some of the key players in the market.